Global

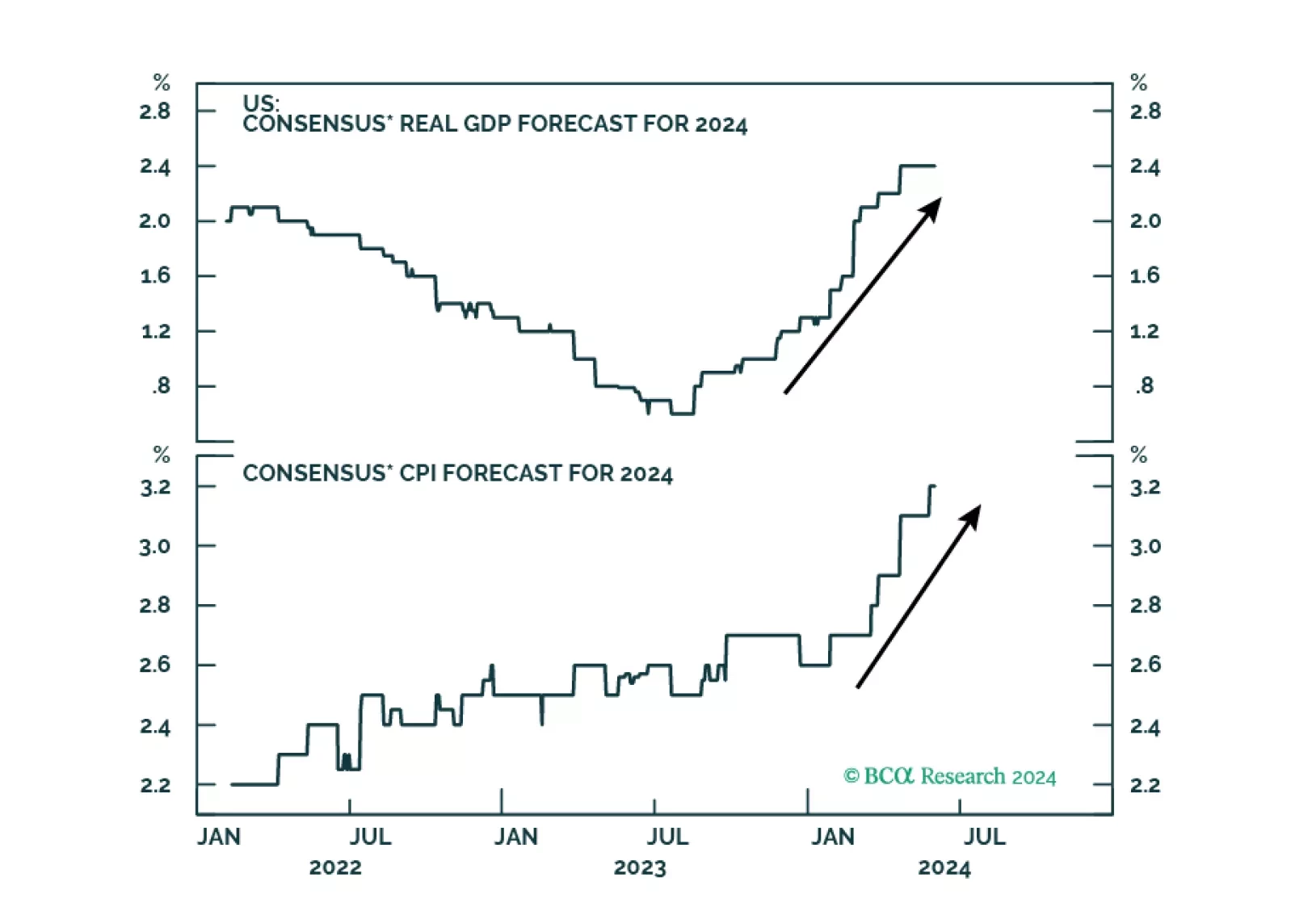

The US economy is in the “Overheating” phase, so stronger growth brings higher inflation. Tight monetary policy means recession is still likely over the next 12 months. Stay defensive.

In this report, we gauge the outlook for the dollar given client visits in Africa.

According to BCA Research’s US Political Strategy service, Trump’s conviction will not be a game changer in the upcoming Presidential election. President Trump was convicted of 34 felony charges by a 12-person jury in a New York state court on May 30 for…

Copper prices have returned a whopping 25.6% YTD, briefly breaking above USD 5 earlier this month. The red metal accounts for a large share of industrial metals indices and it is being buoyed by the same late-cycle dynamics as they are. Copper is deriving…

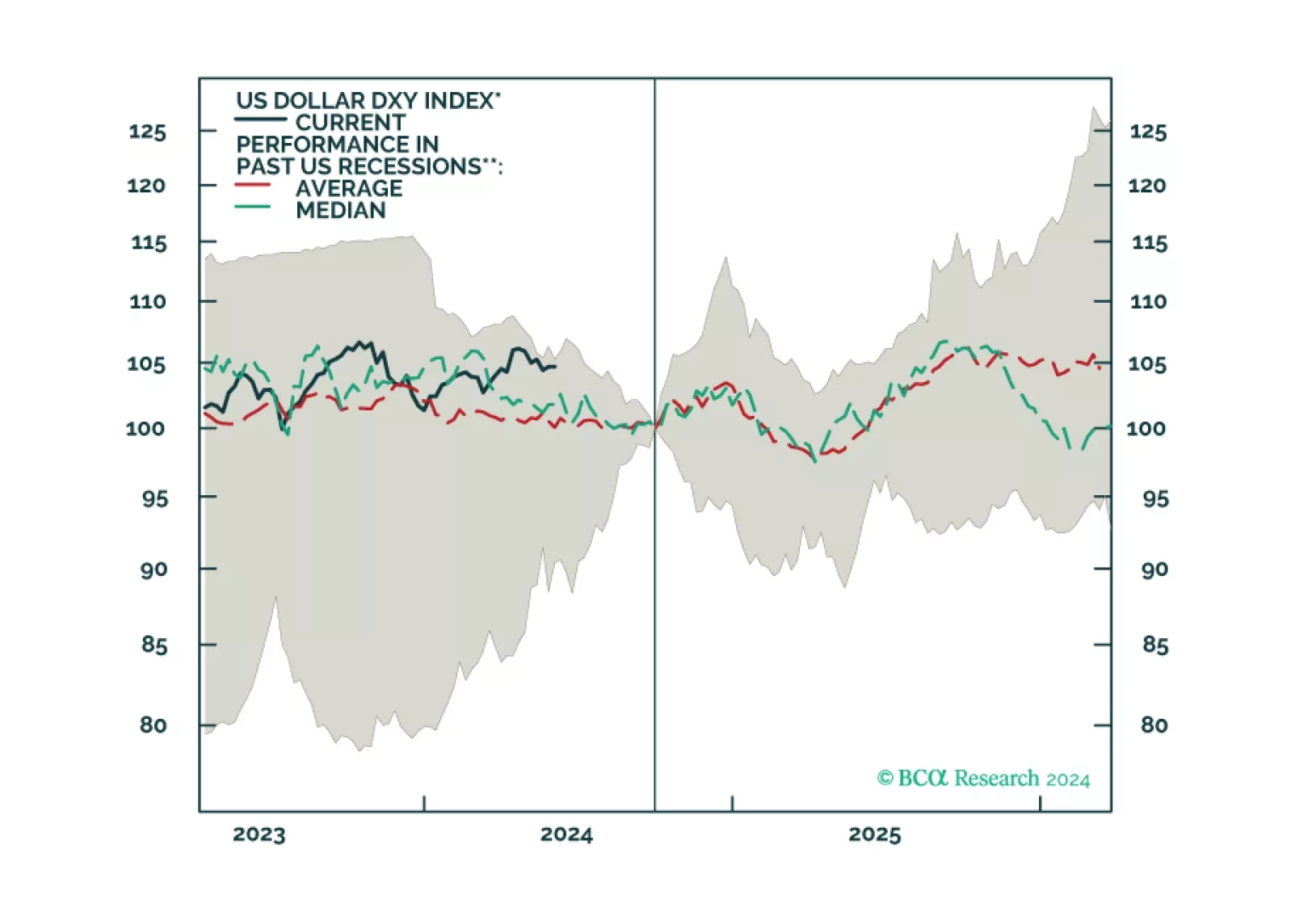

The greenback typically moves in the opposite direction of global growth. The US economy is indeed more highly geared towards services than manufacturing, compared with the rest of the world. Therefore, when global growth reaccelerates, capital typically…

The US manufacturing cycle has followed a surprisingly stable pattern for over seven decades. History suggests that this cycle tends to last for about 36 months, with a down leg spanning 18 months, followed by an up leg approximately spanning another 18…

According to BCA Research’s Counterpoint service, the non-US developed economy is “demand-constrained” whereas the US economy is “supply-constrained”. This schism will continue but in reverse. The team has highlighted that following the surge in…

Preliminary estimates suggest that manufacturing activity generally improved across DM economies in May. Manufacturing PMIs for the US, the Eurozone, Japan and the UK all improved from their April levels. Notably, manufacturing activity started growing…

According to BCA Research’s Commodity & Energy Strategy service, the sudden increase in investor optimism about copper and lopsided long positioning has led to a short squeeze. Short squeezes are typically short-lived and are followed by a rapid unwinding…

Industrial metals have outperformed the broad commodity complex this year and raced above the broad commodity complex even more meaningfully since the beginning of April. Our Commodity and Energy strategists have highlighted that the overrepresentation of…