Global

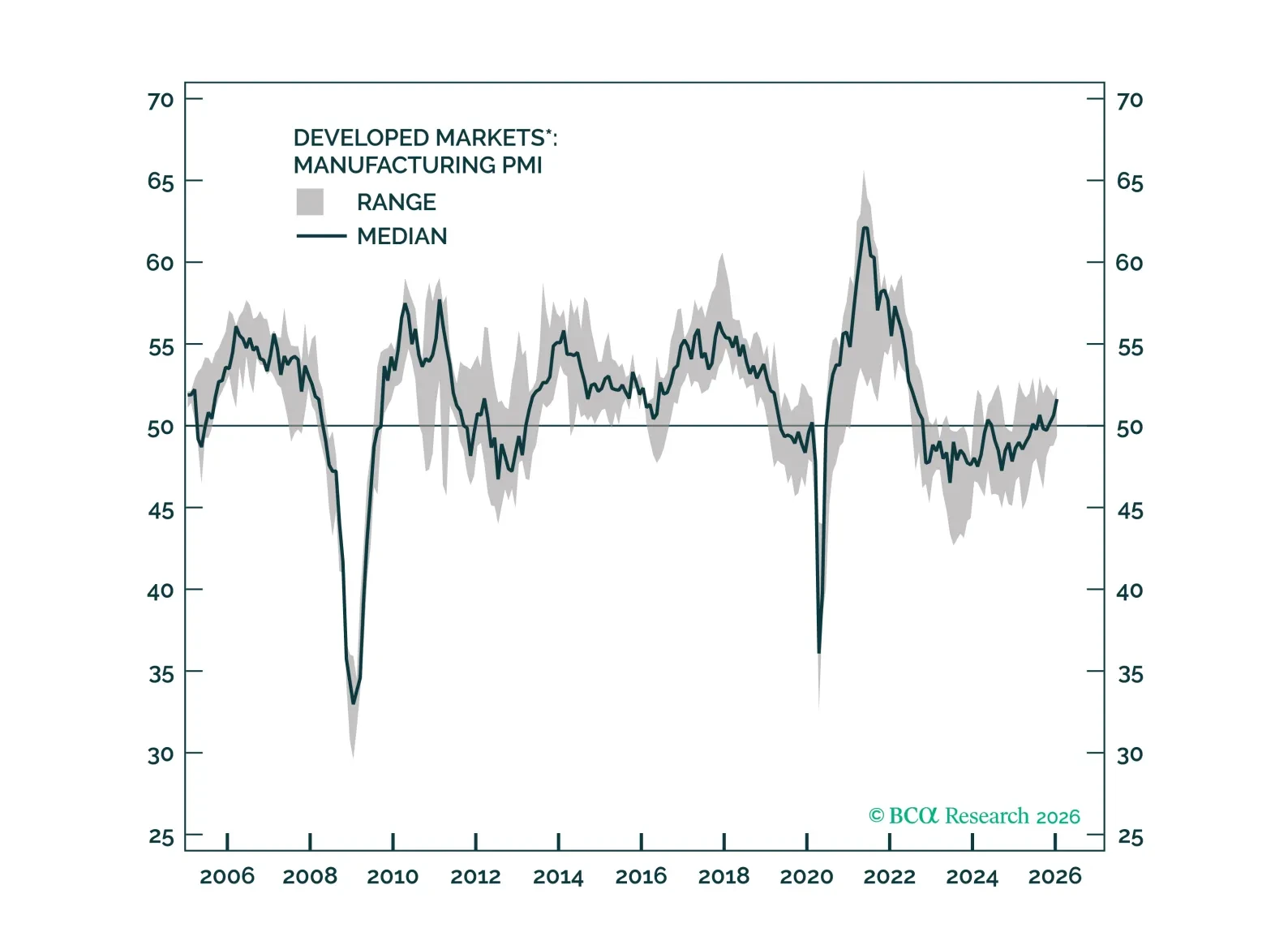

The actions of the Trump administration have dominated the headlines over the past month. They are all noise. Focus on the reactions from the rest of the world. Policy makers outside of the US are now determined to stimulate and reform their domestic economies. Global growth is accelerating without a corresponding increase in inflation. This combination is not only positive for risk assets but is also supercharging returns for Ex-US stocks. Downgrade Fixed Income and duration.

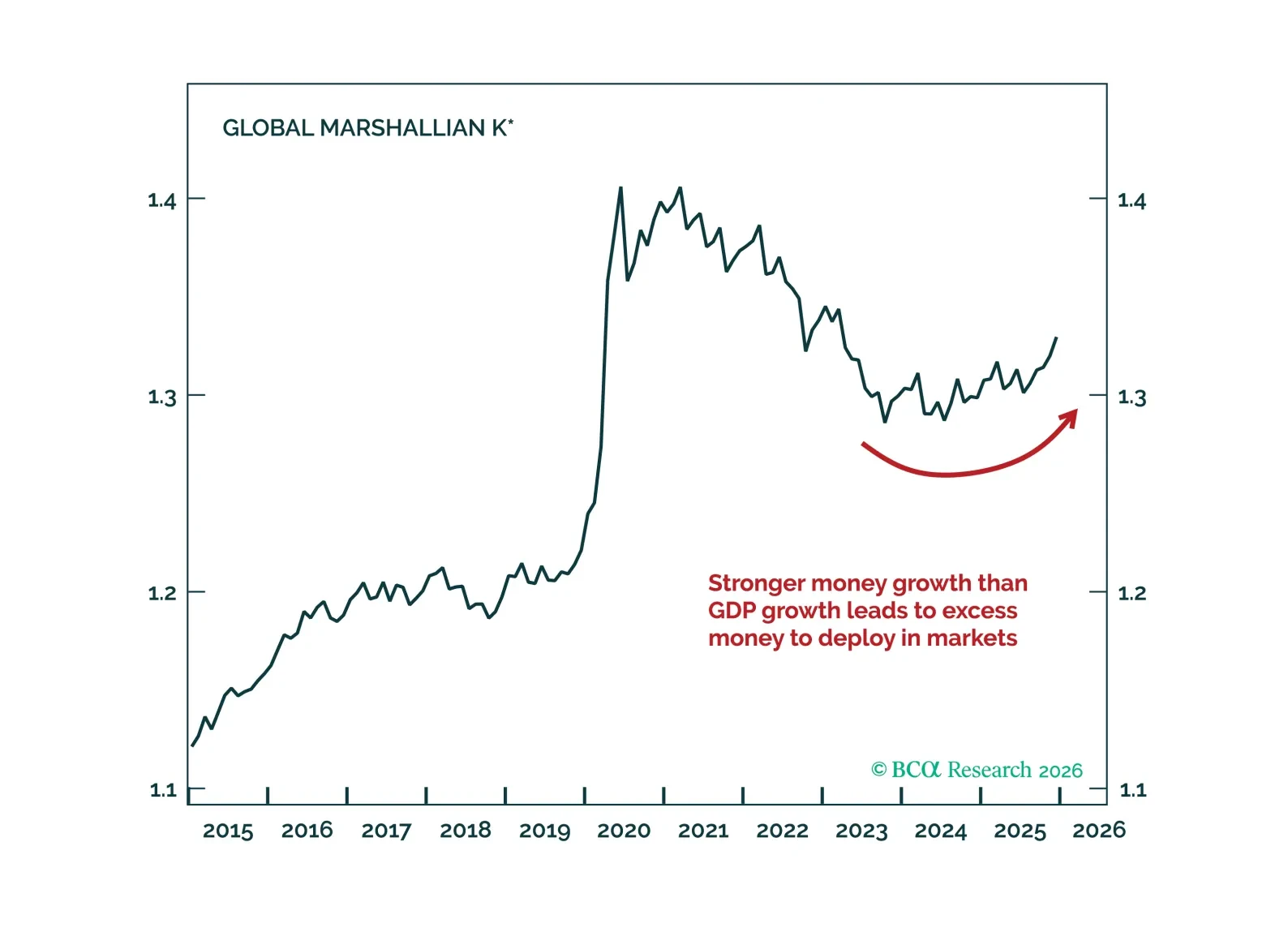

Global liquidity has been the decisive macro variable in 2025, and should stay broadly supportive through most of 2026. We therefore stay neutral equities versus bonds (valuations are stretched), keep a positive bias toward metals (especially gold), and prefer European and Japanese equities over US ones. The key risk is a late-2026 volatility regime shift as overheating fears force a repricing in rates.

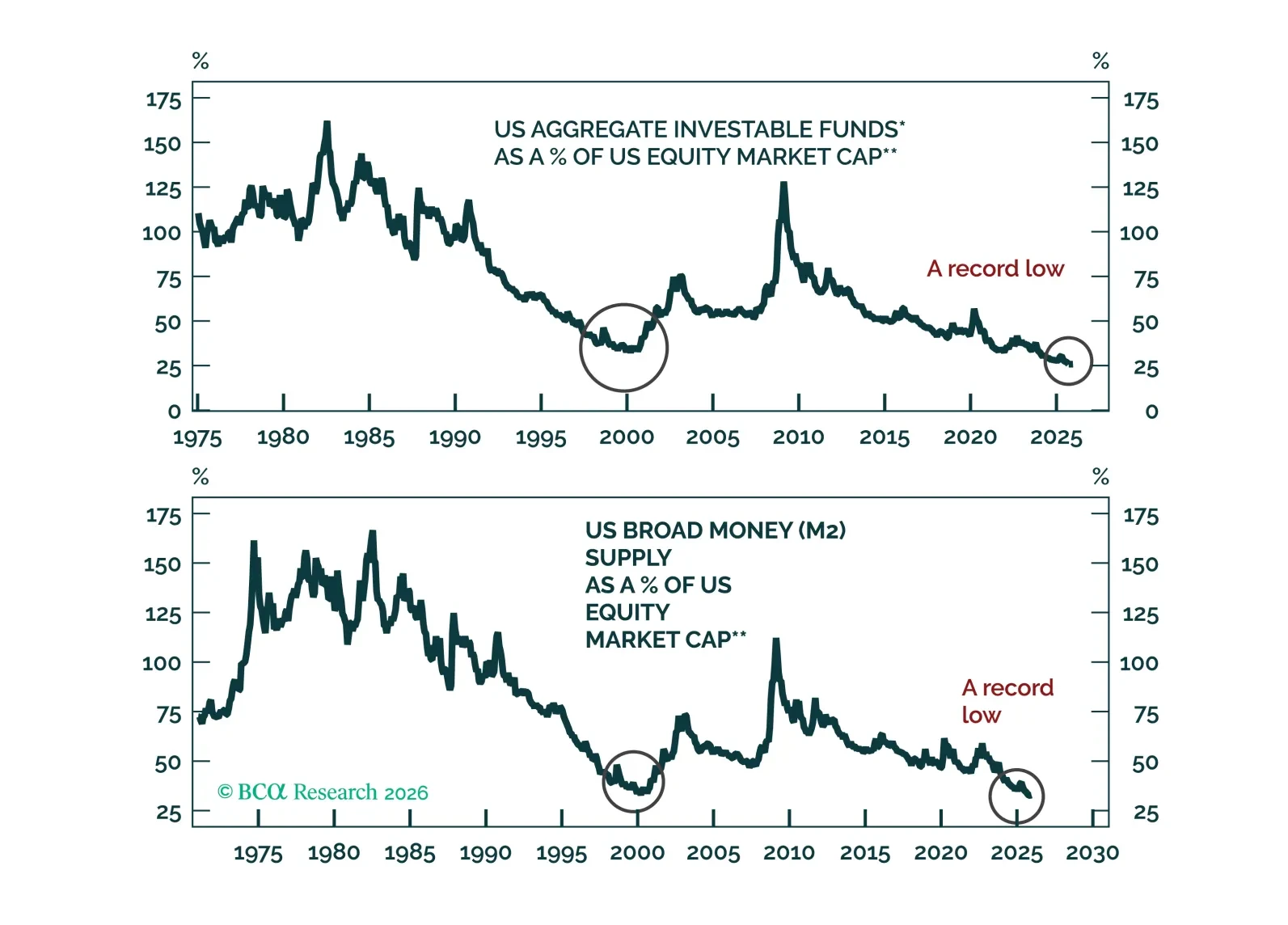

Contrary to widespread narratives, there is little cash on the sidelines. The aggregate amount of investable funds-to-equity market cap ratio is at an all-time low in the US and very low in other developed markets.

Every year, the Global Asset Allocation team compiles a list of our favorite books, essays, and articles from our strategists ahead of the holiday season. This year, we focus on writings by practitioners in the world of finance, business, and beyond. While diverse in their backgrounds, one theme stands out: Adaptation.

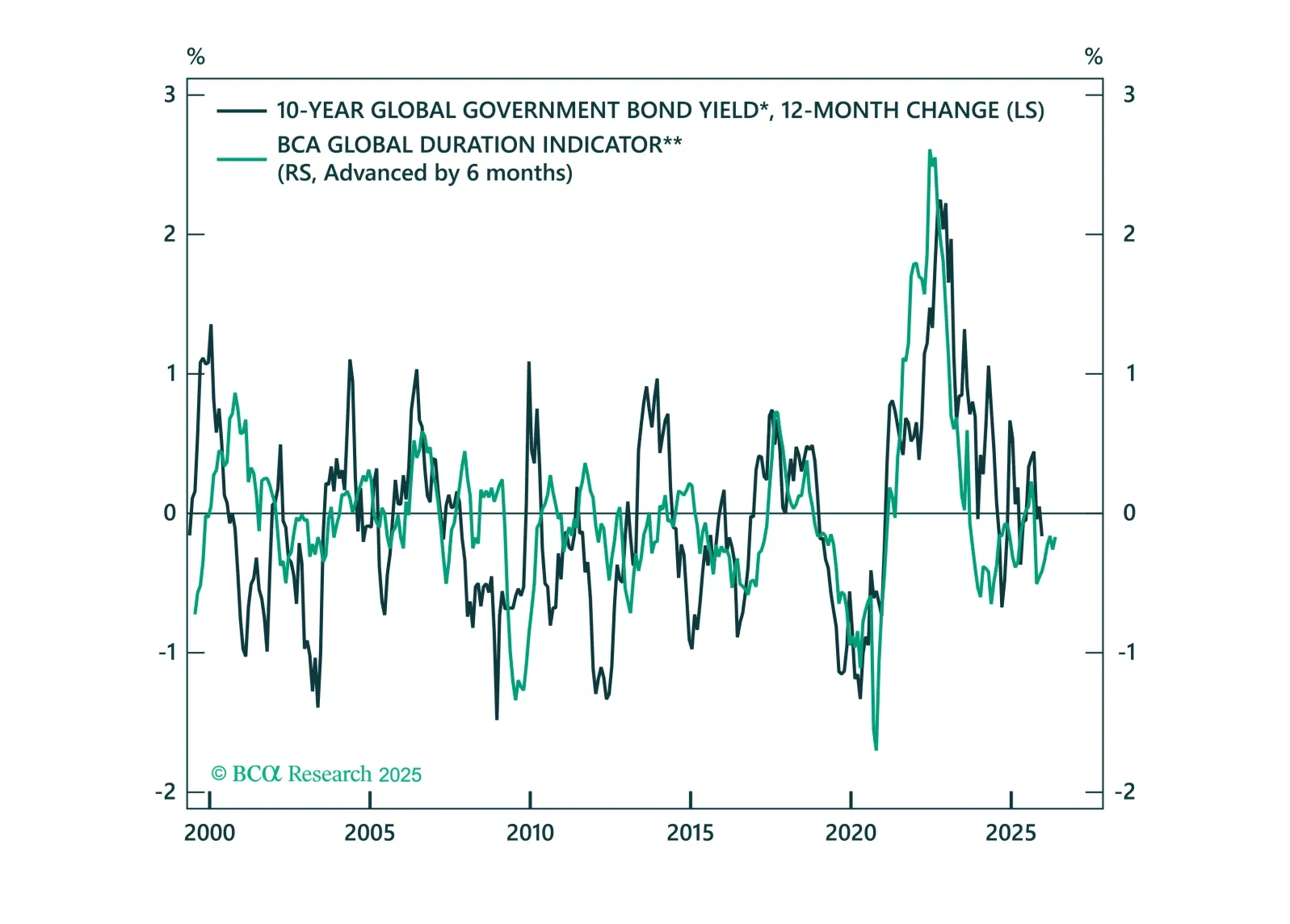

We present our five key views for global fixed income markets in 2026. A year that will see the global easing cycle come to an end.

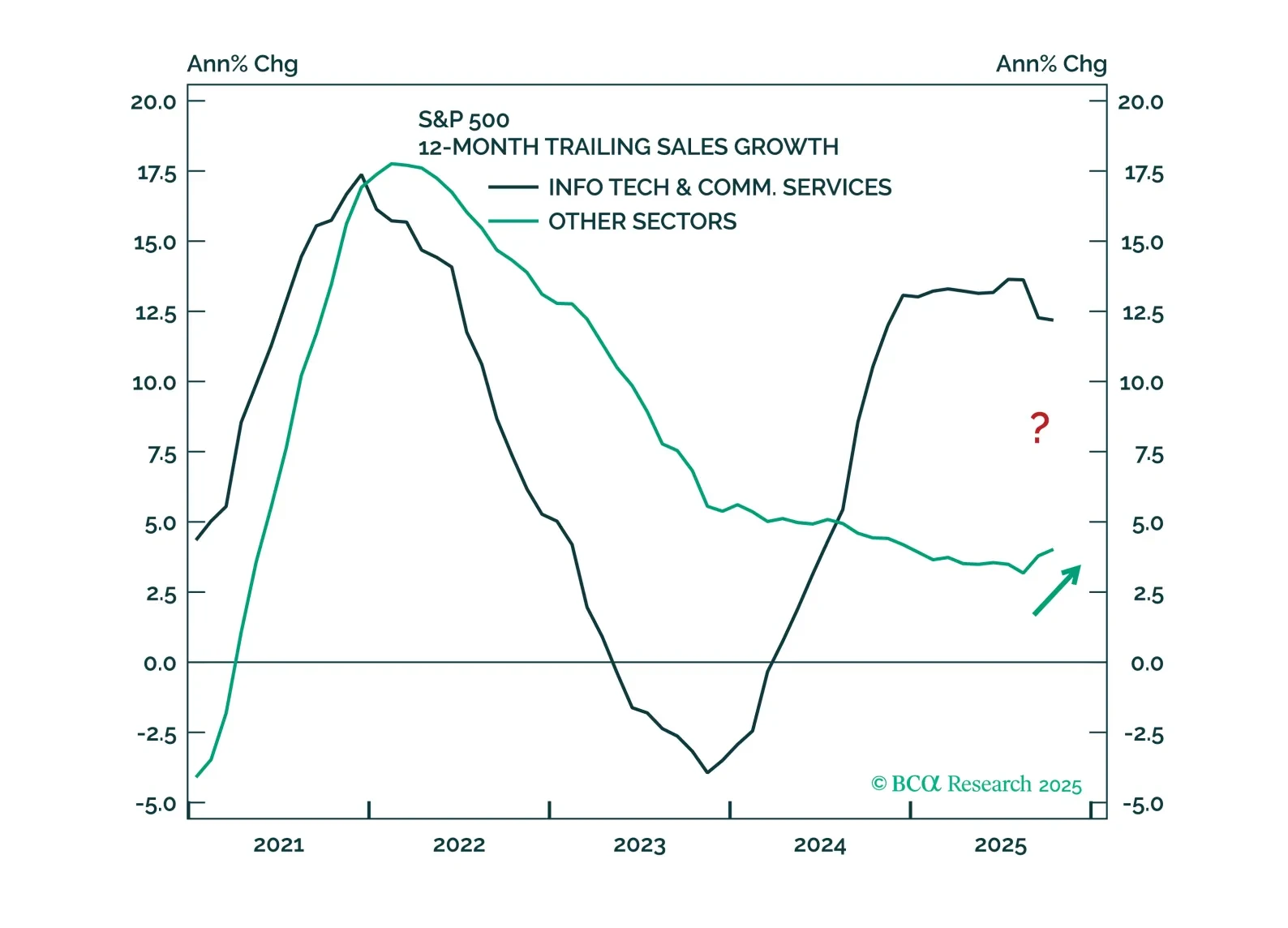

The K-shaped economy will likely reverse in 2026, with the cyclical parts of the economy doing better. Upgrade Financials and Materials from neutral to overweight. Downgrade Communication Services and Utilities from overweight to neutral. Favor value stocks. Upgrade Bitcoin from neutral to overweight.

Today, we are sending you the BCA annual outlook for 2026. The report is an edited transcript of our recent conversation with Mr. X and his daughter Ms. X, who are long-time BCA clients. Our discussion featured BCA’s economic and financial market outlook for the year ahead.