Geopolitics

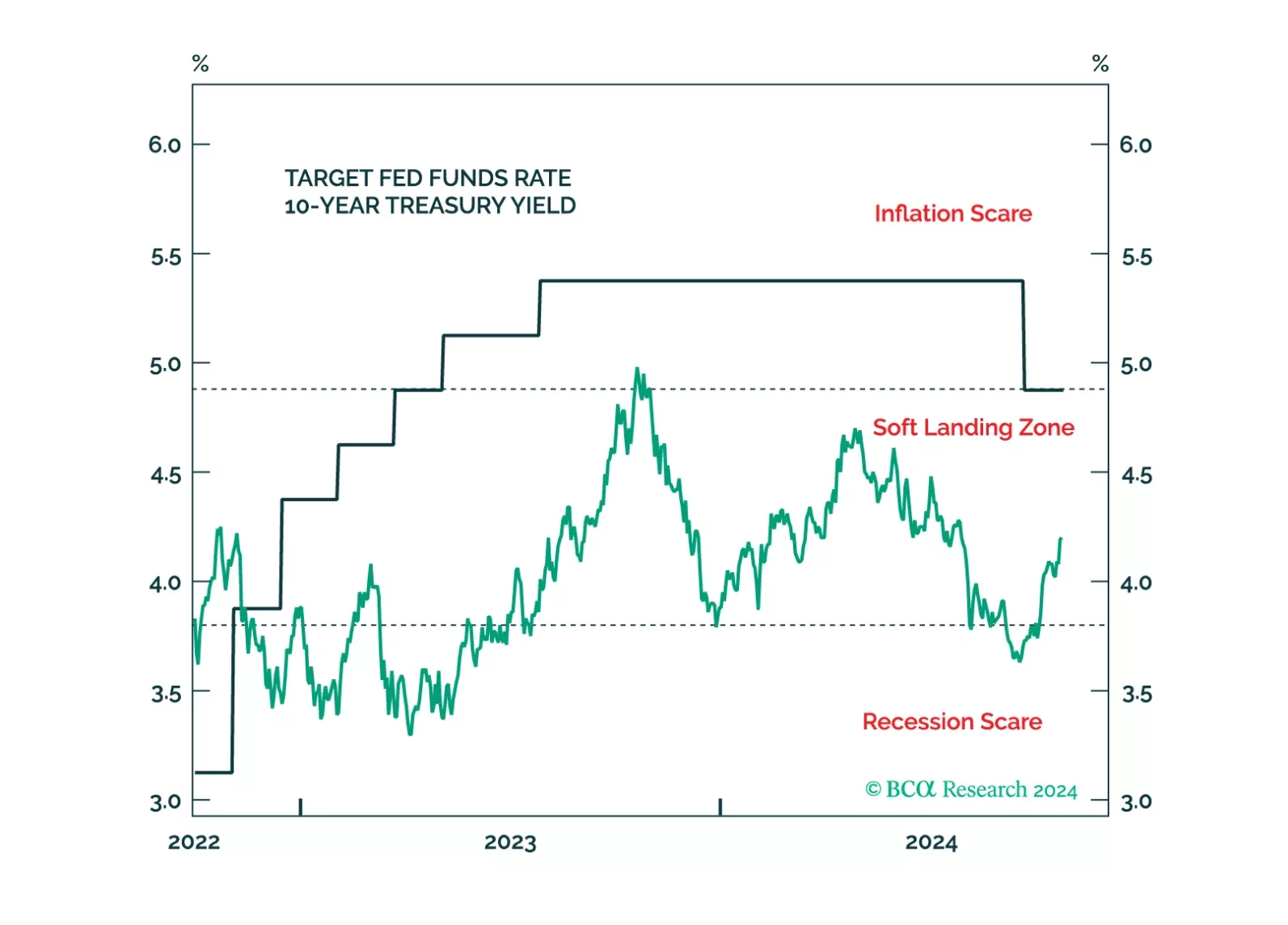

A Donald Trump victory would send bond yields higher during the next few weeks, but yields will fall in 2025 no matter the election outcome.

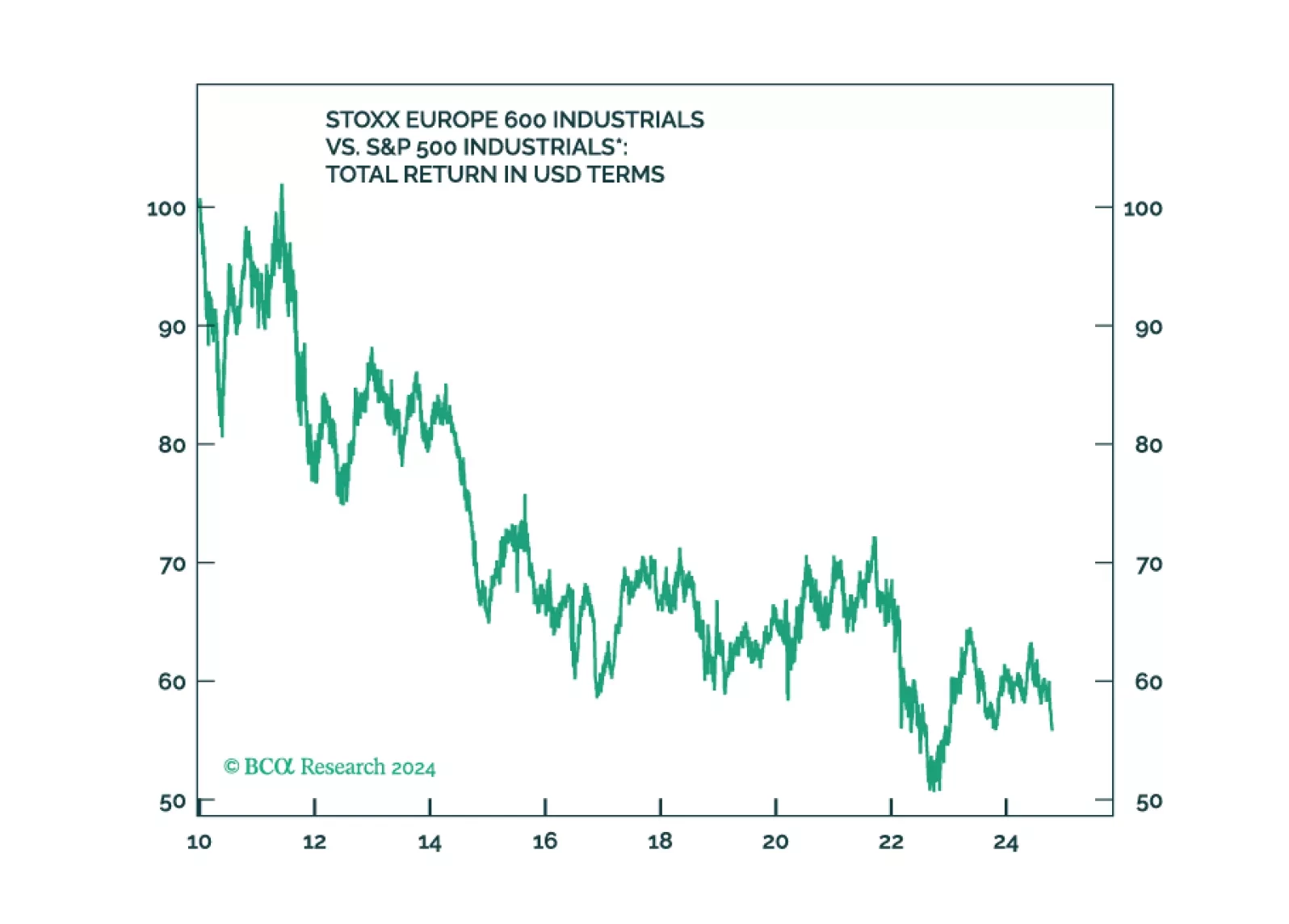

In this Special Report, Marko Papic, Chief Strategist of BCA Research’s GeoMacro Strategy, and Mathieu Savary, Chief Strategist of BCA Research’s European Investment Strategy, together argue that the conflict in Ukraine is already frozen, already losing support in the West, and is likely to taper off over the course of 2025. However, there is no easy alpha left to harvest from that conclusion, the market has already moved on. Some long-term investment opportunities remain in broad European assets.

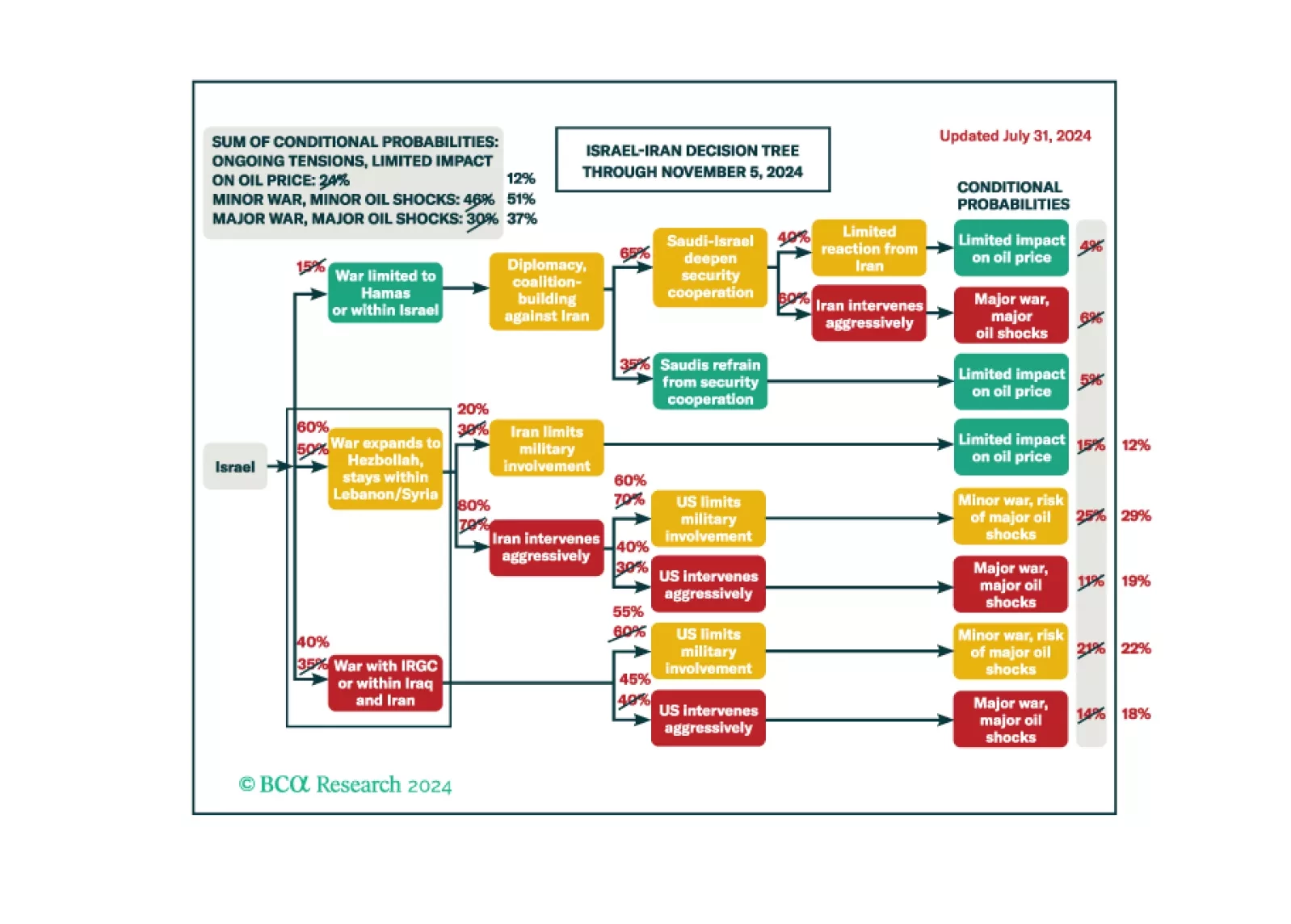

We maintain 37% odds of a major recessionary oil shock, 51% odds of minor shocks, and 12% odds of no shocks.

The month of October ahead of a US general election tends to be a volatile month with negative outcome for equities. As such, it is prudent to remain on the sidelines until after the election.

The US election underscores three long-term trends of Generational Change, Peak Polarization, and Limited Big Government. Investors should expect more volatility around the election and should assess the results before adding more risk. While we predicted the October surprise from the Middle East, more surprises are coming before the final vote is cast.