France

Highlights So What? The yellow vest movement has not soured our optimistic view on France – if anything, it tells us it is time to turn more bullish. Why? The constraints on Macron pursuing reforms are overstated; he has no choice but to double-down. France has multiple tailwinds: strong demographic trends, comparative advantages in exports, and an increasingly pro-business market environment. Also … The roadmap for the European Union to change structurally is set, though it will need political will to materialize. Feature “La réforme oui, la chienlit non!” Charles De Gaulle, May 1968 “France is only herself when she leads fights that are bigger than herself.” Emmanuel Macron, August 2018 “When France sneezes the rest of Europe catches cold.” Prince Clemens von Metternich, 1848 In May 2017, the election of 39-year-old Emmanuel Macron brought an end to the seemingly unstoppable tide of populist nationalism in the developed world. As it turned out, the median voter in France was not as angry as the median voter in the U.K. and the U.S. The reforms implemented since the French election have hardly made headlines outside of domestic media. The struggles of Italy, akin to la commedia dell’arte, and the jousting between London and Brussels, have drawn more attention. More recently, the yellow vest protests have reaffirmed the usual stereotypes about France. Behind the headlines, however, one cannot ignore the market relevance of what is happening in France. Thought to be condemned to stagnation by the rigidity of its labor market and the size of its state, the country is now looking to undo the malaise of the past two decades. The only surprise about the protests is that they did not occur sooner in Macron’s term. In this Special Report, we assess the ongoing yellow vest protests, review the reforms conducted since 2017, and give Macron favorable chances of reforming France further. We also highlight structural tailwinds that will support the French economy in the long run. Finally, we briefly go over the European Union’s roadmap for reforms. How Relevant Are The Yellow Vest Protests? Where there are reforms, there are protests. Or, as an astute client once told us: Buy when blood is in the streets. Had there been no protest against President Macron’s reforms, it would have signaled they lacked teeth. Protests were inevitable as soon as Macron set in motion his ambitious pro-growth and pro-business reform agenda. The yellow vest movement is not a coherent force led by a clear leadership. The demands of the group are many: lower taxes, better services, less of the current reforms (specifically in education), and more of other reforms. But despite this lack of clarity, the protesters have convinced most of the public that the reform agenda should pause, or at least slow down (Chart 1).

Chart 1

What started on social media as a protest against the fuel tax in rural areas has evolved into a movement against President Macron. This transition occurred in part because a large segment of the population believes that Macron’s reforms have mainly benefited the wealthy. In fact, 77% of respondents in a recent poll view him as the “president of the rich.” The modification of the “wealth tax” – which mostly shifts the focus toward real estate assets instead of financial assets – was highly criticized for favoring the wealthiest households. It resonated strongly with the perception that past governments helped the wealthiest households to accumulate more wealth at the expense of the middle class. But it is not clear how intense or durable this popular sentiment will be, given that this type of inequality is not extreme in France and has not been rising (Chart 2). Chart 2What Income Inequality?

What Income Inequality?

What Income Inequality?

Public support for the protests has hovered around 70% for several weeks since they started in November 2018, but is now coming down (Chart 3). There are now more respondents who think that the protests should stop than those who believe they should continue (Chart 4). As a sign of things to come, a demonstration against the yellow vests and in support of Macron and his government – held by the “red scarves” – managed to gather more people on the streets of Paris than the regionally based yellow vests have done in the capital city.1

Chart 3

Chart 4

Who are the yellow vests? The profile is shown in Diagram 1. They are mostly rural, mostly hold a high school degree (or less), and overwhelmingly support anti-establishment political leaders Marine Le Pen (right-wing leader of the National Rally) or Jean-Luc Mélenchon (left-wing leader of La France Insoumise). This suggests that the movement has failed to cross the ideological aisle and win converts from the center. Diagram 1The Profile Of A 'Yellow Vest' Protester

France: La Marche A Suivre?

France: La Marche A Suivre?

How many French people are actually protesting? Although there was a slight pickup in protests at the beginning of January, nationwide numbers are not high. In fact, they are far from what they were back in November and therefore would have to get much larger for markets to become concerned anew (Chart 5). If we are to compare these protests to those in 1995 or 2010, the numbers pale in comparison (Table 1). For instance, the protest of December 1995 brought a million people onto the streets while the demonstrations against the Woerth pension reform in 2010 lasted for seven months and gathered close to nine million protesters across eight different events (Chart 6).

Chart 5

Table 1In A Glorious History Of Protests, 'Yellow Vests' Are A Footnote

France: La Marche A Suivre?

France: La Marche A Suivre?

Chart 6

Instead we would compare the yellow vest protests to the 15-month long Spanish Indignados in 2011, which gathered between six and eight million protesters overall, and the U.S. Occupy Wall Street protests that same year. The two movements were similarly disorganized and combined disparate and often contradictory demands. In both cases, the governments largely ignored the protesters. In the Spanish case, the right-of-center government of Mariano Rajoy plowed ahead with painful, pro-market reforms that have significantly improved Spain’s competitiveness. Thus the yellow vests should not have a major impact on Macron’s reform agenda. Although they have dragged his approval rating to historic lows (Chart 7), there is no constitutional procedure for the French president to lose power. The president’s mandate runs until 2022 and he has a solid 53% of the seats in the Assemblée Nationale. In other words, despite the consensus view – including among voters (Chart 8) – that he will not be able to implement the reforms he had planned, he still has the political power to push forward new initiatives. Chart 7...Although Macron Wishes He Was Sarkozy!

...Although Macron Wishes He Was Sarkozy!

...Although Macron Wishes He Was Sarkozy!

Chart 8

Nevertheless, Macron will certainly have to adjust course to calm the protesters. For example, the recent increase in the minimum wage that the government announced in response to the demonstrations was not supposed to be implemented until later in the presidential term. The reforms brought forward in response to the protest are highlighted in Table 2. This should help reduce the movement’s fervor or otherwise its support. Table 2Macron’s Reforms: The Scorecard

France: La Marche A Suivre?

France: La Marche A Suivre?

More importantly, Table 2 provides a list of the main reforms that have been implemented, proposed, or are yet to be completed since the election. The pace and breadth of these reforms come close to a revolution by the standards of the past forty years.2 What really matters is how these reforms tackle the following three key issues: the size of the state, the cost of financing such a large state, and the inflexible labor market. Macron is making progress on the latter two. Labor reforms, effective since the beginning of 2018, simplify a complex labor code to allow for more negotiations at the company level, leaving unions outside the process. They also establish ceilings on damages awarded by labor courts, which represent a real burden on small and medium-sized French companies. The objective is to better align firm-level wage and productivity developments and encourage hiring on open-ended contracts. Education and vocational reforms aim at reducing the slack in the economy by reallocating skills. The youth unemployment rate, and the percentage of the youth population not in education, employment, or training, are both high (Chart 9). This is very relevant for the labor market given that the lack of skilled labor is the most important barrier to hiring (Chart 10), more so than regulation or employment costs. Chart 9Stagnant Youth Employment Figures...

Stagnant Youth Employment Figures...

Stagnant Youth Employment Figures...

Chart 10...Are A Product Of Skill Deficiencies And Economic Uncertainty

...Are A Product Of Skill Deficiencies And Economic Uncertainty

...Are A Product Of Skill Deficiencies And Economic Uncertainty

The administration’s weak spot is the large size of the state, which is undeniably at the root of the French malaise. At 55% of GDP, total government spending makes the French state the largest amongst developed economies (Chart 11). Although cutbacks have been announced, they have not materialized yet. These would include bringing the defense budget back to 2% of GDP, decreasing the number of deputies in the National Assembly by 30%, and cutting 120,000 jobs in the public sector.

Chart 11

On the bright side, polls show that the French people understand the need to pare back the state. Indeed, 71% are in favor of the announced 100 billion euro cuts in government spending by 2022. Even Marine Le Pen campaigned on the promise of cutting the size of the public sector. Despite having a relatively good opinion of government employees, the majority of respondents approve of increasing work hours and job cuts for redundant government employees (Chart 12).

Chart 12

The fundamental problem of a large public sector is that it has to be financed by taxing the private sector. This has fallen on the shoulders of businesses. However, under Macron, the corporate tax rate is set to decline progressively from 33.33% to 25% by 2022 – a cut of 8.3% in the corporate tax rate over four years (Chart 13). Chart 13Respite Coming For The Private Sector

Respite Coming For The Private Sector

Respite Coming For The Private Sector

Bottom Line: The yellow vest protests were to be expected – they are the natural consequence of Emmanuel Macron’s push to reform the French economy and state. However, when compared to previous efforts to derail government reforms, the numbers simply do not stack up. Their disunited and broad objectives are likely to limit the effectiveness of the movement going forward. The global media’s focus on the protests ignores the structural reforms that Paris has already passed. This is a mistake as the reforms have been significant thus far, though much remains to be done. What To Expect Going Forward? Macron stands in what we call the “danger zone” of the J-Curve of structural reform (Diagram 2). Cutting the size of the state might be what he needs to get out of that zone over the course of his term. Diagram 2In The Danger Zone Of The J-Curve

France: La Marche A Suivre?

France: La Marche A Suivre?

Unlike the last two presidents, Macron’s term has begun with a whirlwind. If he stops now, it is highly unlikely that he will recover his support levels. As such, there is no strategic reason why he would reverse course. His popularity is already in the doldrums. His only chance at another term is to plow ahead and campaign in 2022 on his accomplishments. He just needs to ensure that he will not plow into a rock. As expected, Macron has not made any mention of changing course on his most business-friendly reforms, which we see as a signal to investors that despite the recent chaos, the plan remains the same. Pension reforms, however, will likely be postponed given the ongoing protests. Macron hoped to introduce a universal, unified pension system by the middle of 2019 to replace an overly complex and fragmented system in which 42 different types of pension coexist, each one with its own calculation rules. Though protests (both yellow vest and otherwise) have been unimpressive by historical standards (Table 1), it might be too risky for the government to push the pension reform so close to these events. Bottom Line: Macron has turned France into one of the fastest-reforming countries in Europe. Do not read too much into the lows in approval rating and the protests. Macron has no choice but to own the reform agenda and try to campaign on it in 2022. France Is Not Hopelessly Condemned To Stagnation No country elicits investor doom and gloom like France. It is like the adage that Brazil has been turned on its head: France is the country of the past and always will be. However, we think that such pessimism ignores three important structural tailwinds. Demographics From 2015 to 2050, the age distribution will remain broadly unchanged (Chart 14). The same cannot be said of Italy or Germany, where low fertility rates and ageing populations will permanently shift the demographic picture. Indeed, France has the highest fertility rate amongst advanced economies and less than 20% of the population is older than 65 (Chart 15). And France is far from relying on net migration to keep its population growing; migration represented only 27% of total population growth between 2013 and 2017, lower than in the U.S., the U.K. and Germany even if we were to exclude the migration crisis (Chart 16).

Chart 14

Chart 15France Has Healthy Demographics…

Positive Demographic Trends

Positive Demographic Trends

Chart 16

Whenever one mentions France’s positive demographics, criticism emerges that the high fertility rate is merely the result of migrants having lots of kids. This is not entirely correct. While data is scarce due to nineteenth century laws prohibiting censuses based on race or religious belief, data from neighboring European states shows that the birth rate among migrants and citizens of migrant descent essentially declines to that of the native population by the second generation, which in France remains at the replacement level.3 Solid population growth will be a boon to the French economy. A stable dependency ratio – the ratio of working-age to very old or very young people – should limit the burden on government budgets. Further, France will avoid the downward pressure on aggregate household savings associated with an ageing population, the negative implications of a smaller pool of funds available to the private sector, and the resulting inflationary pressures. We also expect the structural rise in European elderly labor force participation to finally take effect in France. The aftermath of the Great Recession and the burden of having to provide for unemployed youth should spur French retirees to work longer. At 3.1%, France is still some way behind Germany at 7% and the average of 6% for European countries (Chart 17). Chart 17Time For Pépère To Get Back To Work

Time For Pépère To Get Back To Work

Time For Pépère To Get Back To Work

Together, these forces imply a higher long-term French potential growth. Based on demographic divergence alone, the European Commission expects French nominal GDP to overtake German nominal GDP by 2040. The French Savoir-Faire France has lost competitiveness in the global marketplace. French export performance has suffered from decades of rigidities and high unit-labor costs while some of France’s peers, such as Germany, benefited greatly from an early implementation of labor reforms (Chart 18). While pro-growth and pro-market reforms ought to reverse some of these trends, France can still rely on a manufacturing savoir-faire that gives it a strong foothold in high value-added sectors of manufacturing, such as in transportation, defense, and aeronautics. Chart 18The Hartz Reforms Gap

The Hartz Reforms Gap

The Hartz Reforms Gap

Table 3 lists the 10 largest export sectors as a share of total exports for France and Germany. These two economies share five similar categories of exports amongst their largest exports, representing respectively 23.8% and 24.3% of their total exports. However, France displays a substantially higher revealed comparative advantage (RCA) in its flagship sectors.4 In other words, the level of specialization of these sectors relative to the world average is higher in France than in Germany. Going forward, it is precisely this level of specialization in the high value-added sectors that will support the French manufacturing industry. Table 3France Vs. Germany: Closer Than You Think

France: La Marche A Suivre?

France: La Marche A Suivre?

We also view the bullish trends for defense spending and arms trade, and the burgeoning EM demand for transportation goods, as important tailwinds for French manufacturing. France is the world’s fourth-largest global defense exporter and will benefit from shifting geopolitical equilibriums caused by multipolarity. France is also well positioned in the transportation sector where its exports to EM countries represent 20% of its overall transportation exports – a share that more than doubled in the past 15 years (Chart 19). While this trend is currently declining with the end of Chinese industrialization, we expect that it will resume over the next several decades as more EM and FM economies grow. Chart 19EM: A Growth Market For France

EM: A Growth Market For France

EM: A Growth Market For France

France Is Much More Business-Friendly Than You Think A surge in the number of businesses created followed the election of the French president. Last year, more than 520,000 new businesses were created (Chart 20). Chart 20The New 'Start-Up Nation'

The New "Start-Up Nation"

The New "Start-Up Nation"

The ease of doing business has improved on various metrics and the economy-wide regulatory and market environment should continue on this trend, as measured by the OECD product market regulation indicator (Chart 21). For instance, it takes only three and a half days to set up a business in France and no more than five steps, which is much easier than in most European countries.

Chart 21

France also ranks 10th on the Global Entrepreneurship Index – a measure of the health of entrepreneurship ecosystems in 137 countries. It appears prepared for more tech start-ups as it ranks amongst the top countries on the Technological Readiness Index. Overall, France is now a much more attractive destination for investments (Chart 22). It appears that Brexit uncertainty is also driving some long-term capital investments. Between 2016 and 2017, the number of FDI projects in France jumped by 31% and Paris has become the most attractive European city for foreign direct investments (Chart 23).

Chart 22

Chart 23Paris: The City Of (Love) FDI

Paris: The City Of (Love) FDI

Paris: The City Of (Love) FDI

Cyclical View Despite the end of QE, markets do not expect the ECB to start hiking rates in the next 12 months – the expected change in ECB policy rate as discounted by the Overnight Index Swap curve is only 7 bps. This means the private sector will keep benefiting from extremely low lending rates, nearing 2%. Bank loans to the private sector will continue growing at a solid pace (Chart 24). Chart 24Banks Are Itching To Lend

Banks Are Itching To Lend

Banks Are Itching To Lend

A lower unemployment rate and accelerating wage growth are positive for both consumer spending and residential investment. Average monthly earnings have strongly rebounded in the past five quarters (Chart 25). These two trends could put a floor under deteriorating household confidence and support consumer spending (Chart 26). Should household confidence rebound, consumers might spend more and stimulate the economy given their high savings rate. Chart 25Consumers Are Primed To Consume

Consumers Are Primed To Consume

Consumers Are Primed To Consume

Chart 26But Protests Have Dented Confidence

But Protests Have Dented Confidence

But Protests Have Dented Confidence

How does this dynamic translate in economic growth? Despite the setback experienced by the euro area – due to weaker external demand, or “vulnerabilities in emerging markets” to use the European Central Bank’s (ECB) own words – and the negative economic impact of the yellow vests, French real GDP grew by 1% (annualized) in the fourth quarter. The concessions made by Macron to answer the protests will bring the budget deficit close to 3.2% of GDP – from an earlier projection of 2.8%. The fiscal thrust will contribute positively to GDP growth (Chart 27), though 2020 may witness a larger fiscal drag. Chart 27Macron Has Given Up On Austerity

Macron Has Given Up On Austerity

Macron Has Given Up On Austerity

Bottom Line: The overall fundamentals of the economy are not as bad as the pessimists say. Cyclical and structural tailwinds will support the French economy going forward and should be reinforced by reforms. Can Europe Be Set En Marche Too? Macron’s presidency offers the European Union a window of opportunity to change structurally. He is already perceived as the “default leader” of Europe and might be the answer to the EU’s desperate need for strong leadership. What we have so far looks like a roadmap for a roadmap, but some progress could materialize this year. The European Stability Mechanism (ESM) – the European instrument for economic crisis prevention – is supposed to be granted new powers. At the Euro Summit in December, the ministers agreed on the terms of reference of the common backstop to the euro zone bank resolution fund (SRF), which would allow the ESM to lend to the SRF should a crisis or number of crises suck away all its funds. It would be ready from 2024 to come up with loans for bank resolution. While this may appear to be too late to make a difference in the next recession, we would remind clients that all dates are malleable in the European context. The possibility of the ESM playing a role in a potential sovereign debt restructuring in the future, like a sort of “European IMF,” was also discussed. However, some – including the ESM’s leadership – argue that such an expanded role will necessitate a greater injection of capital, which obviously Berlin must accept. Second, the stalled Banking Union project requires Berlin’s intimate involvement. In fact, Germany remains practically the only member state against the European Deposit Insurance Scheme (EDIS). This deposit insurance union would go a long way toward stabilizing the Euro Area amid future financial crises. However, a high-level working group should report by June 2019. As such, with Merkel sidelined and Macron taking leadership of the reform process, there could be movement on the EDIS by mid-year. Bottom Line: As Merkel exits the stage, France is likely to seize the opportunity to take the leading role from the Germans. By delivering the reforms he promised during his campaign and thus performing effectively at home, Macron hopes to obtain the legitimacy to set the EU en marche as well. Some material progress could be achieved as early as June this year. Stay tuned. Jeremie Peloso, Research Analyst jeremiep@bcaresearch.com Footnotes 1 According to the government, 10,500 “red scarves” marched in Paris on January 27, 2018. 2 Sans the guillotine! 3 Rojas, Bernardi, and Schmid, “First and second births among immigrants and their descendants in Switzerland,” Demographic Research 38:11 (2018), pp. 247-286, available at https://www.demographic-research.org/Volumes/Vol38/11/Ariane Pailhé, “The convergence of second-generation immigrants’ fertility patterns in France: The role of sociocultural distance between parents’ and host country,” Demographic Research 36:45 (2017), pp. 1361-1398, available at https://www.demographic-research.org/Volumes/Vol36/45/Kulu et al., “Fertility by Birth Order among the Descendants of Immigrants in Selected European Countries,” Population And Development Review 43:1 (2017), pp. 31-60, available at https://doi.org/10.1111/padr.12037 4 A country displays a revealed comparative advantage in a given product if it exports more than its “fair” share, that is, a share that is equal to the share of total world trade that the product represents.

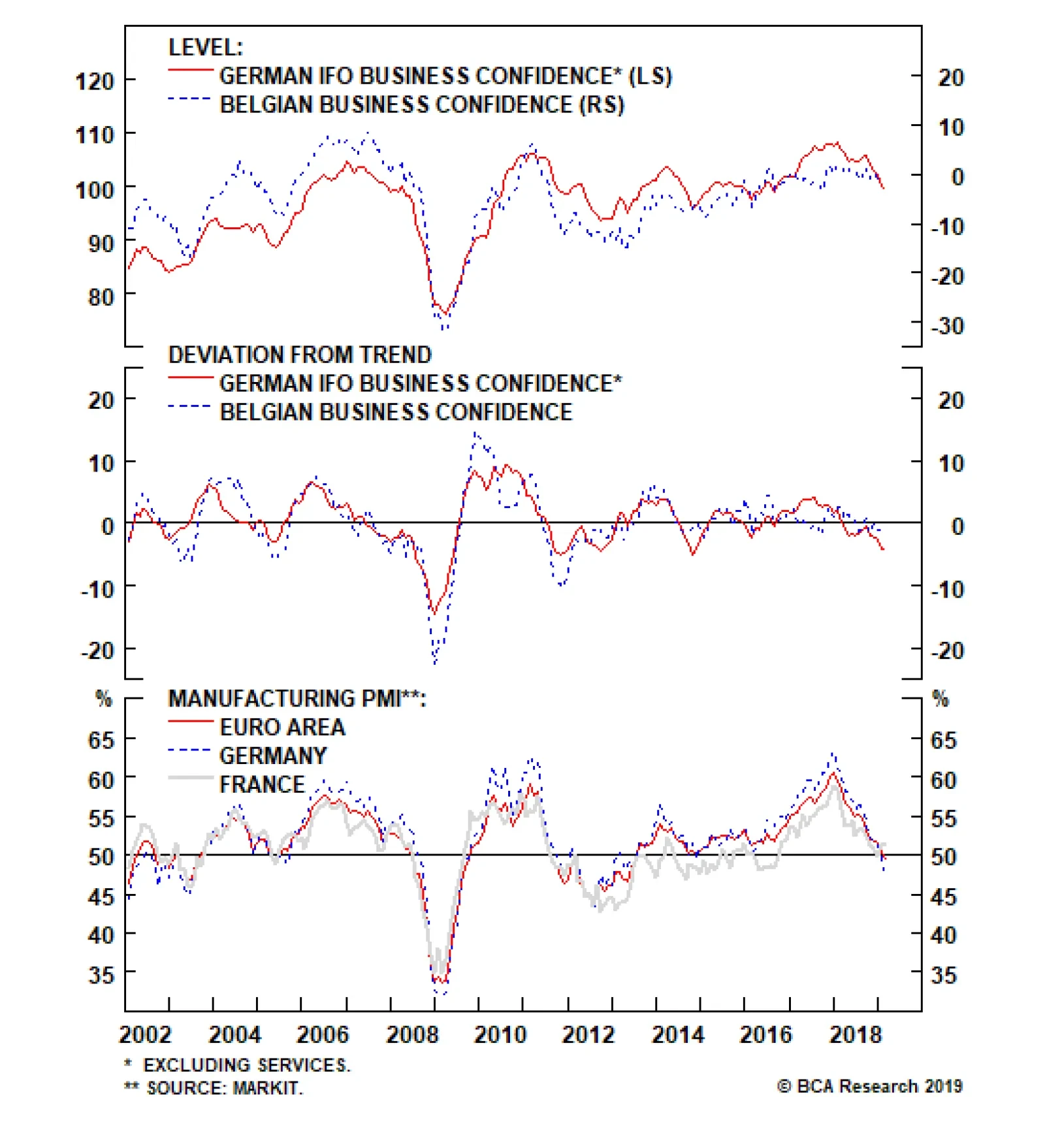

The European economic slowdown shows no sign of ending. This morning, both the German Ifo and the Belgian business confidence decelerated further, with the former falling to 98.5 from 99.3, and the latter weakening from -1.5 to -1.7. Interestingly, as the…

Highlights The global economic mini-cycle is set to weaken while the euro is set to grind higher. Upgrade Telecoms to overweight. Also overweight Healthcare and Airlines. Underweight Banks, Basic Materials and Energy. Overweight France, Ireland, U.K., Switzerland and Denmark. Underweight Italy, Spain, Sweden and Norway. The Eurostoxx50 will struggle to outperform the S&P500. Feature We are strong believers in Investment Reductionism, a philosophy synthesized from the Pareto Principle and Occam's Razor.1 Investment reductionism offers a liberating thesis - the incessant barrage of investment research, newsfeeds and ten thousand word commentaries is largely superfluous to the investment process. What seems like a complexity of investment choice usually reduces to getting a few over-arching decisions right. Chart of the WeekIn Quadrant 4, Overweight Domestic Defensives And Underweight International Cyclicals

The Four Quadrants Of Cyclical Investing

The Four Quadrants Of Cyclical Investing

For equity sector and country allocation, two over-arching decisions dominate: Whether the global economic mini-cycle is set to strengthen or weaken (Chart I-2). Whether the domestic currency is set to strengthen or weaken. Chart I-2The Empirical Evidence For Credit And Economic Mini-Cycles Is Irrefutable

The Empirical Evidence For Credit And Economic Mini-Cycles Is Irrefutable

The Empirical Evidence For Credit And Economic Mini-Cycles Is Irrefutable

The four permutations of these two decisions create the four quadrants of cyclical investing (Chart of the Week). Right now, European investors find themselves in quadrant four: the global economic mini-cycle is set to weaken while the euro is set to grind higher. This favours an overweight stance to defensives, especially domestic-focused defensives. Therefore today, we are upgrading Telecoms to overweight. We also recommend an underweight stance to the most cyclical sectors, especially international-focused cyclicals such as Basic Materials and Energy. Country allocation then just drops out of this sector allocation. The Global Economic Mini-Cycle Is Set To Weaken We can predict the changes of the seasons and the tides of the sea with utmost precision. How? Not because we have an ingenious leading indicator for the seasons and tides, but because we recognise that these phenomena follow perfectly regular cycles. Regular cycles create predictability. Significantly, global bank credit flows also exhibit remarkably regular cycles with half-cycle lengths averaging around eight months. Recognizing these mini-cycles is immensely powerful because, just as for the seasons and the tides, it creates predictability. Furthermore, if most investors are unaware of these cycles, the next turn will not be discounted in today's price - providing a compelling investment opportunity for those who do recognise the predictability. The empirical evidence for credit mini-cycles is irrefutable. The theoretical foundation is also rock solid, based on an economic model called the Cobweb Theory.2 This states that in any market where supply lags demand, both the quantity supplied and the price must oscillate. Given that credit supply clearly lags credit demand, the quantity of credit supplied and its price (the bond yield) must experience mini-cycles (Chart I-3). And as the quantity of credit supplied is a marginal driver of economic activity, economic activity will also experience the same regular oscillations. Today, the global 6-month credit impulse is turning from mini-upswing to mini-downswing, with all three subcomponents - the euro area, the U.S. and China - now in decline (Chart I-4). This is exactly in line with prediction. Mini half-cycles average eight months, and the latest mini-upswing started eight months ago. Chart I-3The Global Economic Mini-Cycle##br## Is Set To Weaken

The Global Economic Mini-Cycle Is Set To Weaken

The Global Economic Mini-Cycle Is Set To Weaken

Chart I-4All Three Subcomponents Of The Global 6-Month ##br##Credit Impulse Are Now Declining

All Three Subcomponents Of The Global 6-Month Credit Impulse Are Now Declining

All Three Subcomponents Of The Global 6-Month Credit Impulse Are Now Declining

More importantly, as we enter a mini-downswing, we can also predict that global growth is likely to experience at least a modest deceleration through the coming two to three quarters. The Euro Is Set To Grind Higher, Except Versus The Yen Chart I-5Lost In Translation

Lost In Translation

Lost In Translation

Nowadays, mainstream stock markets tend to be eclectic collections of multinational companies which happen to be quoted on bourses in Frankfurt, Paris, New York, and so on. For example, BASF is not really a German chemical company, it is a global chemical company headquartered in Germany. For operational hedging, multinational companies like BASF will intentionally diversify their sales and profits across multiple major currencies, say euros and dollars. But of course, the primary stock market quotation will be in the currency of its home bourse, euros. Therefore, when the euro strengthens, the company's multi-currency profits, translated back into a stronger euro, will necessarily weaken (Chart I-5). Clearly, more domestic-focused companies like telecoms will not experience such a strong currency-translation headwind. We expect the main euro crosses to continue strengthening over the next 8 months, with the exception being the cross versus the Japanese yen. Our central thesis is that the payoff profile for a foreign exchange rate just tracks the bond yield spread. This means that when a central bank has already taken bond yields close to their lower bound, its currency possesses a highly attractive asymmetry called positive skew. In essence, as the ECB is at the realistic limit of ultra-loose policy, long-term expectations for the ECB policy rate possess an asymmetry: they cannot go significantly lower, but they could go significantly higher. Exactly the same applies to long-term expectations for the BoJ policy rate. In contrast, long-term expectations for the Fed policy rate possess full symmetry: they could go either way, lower or higher. This stark asymmetry of central bank 'degrees of freedom' favours the euro and the yen over the dollar. Which Sectors And Countries To Own And Which To Avoid? Pulling together the preceding two sections, the global economic mini-cycle is set to weaken while the euro is set to grind higher. This puts Europe in quadrant four of our four quadrant framework for cyclical investing. Unsurprisingly, the relative performance of the most cyclical sectors - Banks, Basic Materials and Energy - very closely tracks the regular mini-cycles in the global 6-month credit impulse. In a mini-downswing these cyclical sectors always underperform (Chart I-6, Chart I-7 and Chart I-8). Accordingly, underweight these three sectors on a two to three quarter horizon. Chart I-6In A Mini-Downswing, ##br##Banks Always Underperform

In A Mini-Downswing, Banks Always Underperform

In A Mini-Downswing, Banks Always Underperform

Chart I-7In A Mini-Downswing,##br## Basic Materials Always Underperform

In A Mini-Downswing, Basic Materials Always Underperform

In A Mini-Downswing, Basic Materials Always Underperform

Chart I-8In A Mini-Downswing,##br## Energy Always Underperforms

In A Mini-Downswing, Energy Always Underperform

In A Mini-Downswing, Energy Always Underperform

Conversely, overweight the relatively defensive Healthcare sector. Also overweight the Airlines sector. Airlines' performance is a mirror-image of the oil price cycle, given that aviation fuel comprises the sector's main variable cost. Furthermore, as aviation fuel is priced in dollars, it also insulates European Airlines against a strengthening euro. Today, we are also upgrading the Telecoms sector to overweight given its relative non-cyclicality (Chart I-9), its domestic-focus, and the excessively negative groupthink towards it (Chart I-10). Chart I-9In A Mini-Downswing, ##br##Telecoms Always Outperform

In A Mini-Downswing, Telecoms Always Outperform

In A Mini-Downswing, Telecoms Always Outperform

Chart I-10Telecoms Are Due ##br##A Trend Reversal

Telecoms Are Due A Trend Reversal

Telecoms Are Due A Trend Reversal

In summary: Overweight: Healthcare, Telecoms, and Airlines Underweight: Banks, Basic Materials and Energy Then to arrive at a country allocation, just combine the cyclical view on the major sectors with the country sector skews in Box 1. The result is the following unchanged European equity market allocation. Overweight: France, Ireland, U.K., Switzerland and Denmark Neutral: Germany and Netherlands Underweight: Italy, Spain, Sweden and Norway Lastly, what is the prognosis for the Eurostoxx50 relative to the S&P500? Essentially, this reduces to a battle between the multinational cyclicals - especially banks - that dominate euro area bourses and the multinational technology giants that dominate the U.S. stock market. With the global economic mini-cycle set to weaken and the euro set to grind higher, the Eurostoxx50 will struggle to outperform the S&P500. Box 1: The Vital Few Sector Skews That Drive Country Relative Performance For major equity indexes in the euro area, the dominant sector skews that drive relative performance are as follows: Germany (DAX) is overweight Chemicals, underweight Banks. France (CAC) is underweight Banks and Basic Materials. Italy (MIB) is overweight Banks. Spain (IBEX) is overweight Banks. Netherlands (AEX) is overweight Technology, underweight Banks. Ireland (ISEQ) is overweight Airlines (Ryanair) which is, in effect, underweight Energy. And for major equity indexes outside the euro area: The U.K. (FTSE100) is effectively underweight the pound. Switzerland (SMI) is overweight Healthcare, underweight Energy. Sweden (OMX) is overweight Industrials. Denmark (OMX20) is overweight Healthcare and Industrials. Norway (OBX) is overweight Energy. The U.S. (S&P500) is overweight Technology, underweight Banks. Dhaval Joshi, Senior Vice President Chief European Investment Strategist dhaval@bcaresearch.com 1 The Pareto Principle, often known as the 80-20 rule, says that 80% of effects come from just 20% of causes. Occam's Razor says that when there are many competing explanations for the same effect, the simplest explanation is usually the best. 2 Please see the European Investment Strategy Special Report 'The Cobweb Theory And Market Cycles' published on January 11, 2018 and available at eis.bcaresearch.com. Fractal Trading Model* This week's recommended trade is to short the Helsinki OMX versus the Eurostoxx600. Apply a profit target of 3% with a symmetrical stop-loss. In other trades, we are pleased to report that short Japanese Energy versus the market achieved its 8% profit target at which it was closed. This leaves four open positions. For any investment, excessive trend following and groupthink can reach a natural point of instability, at which point the established trend is highly likely to break down with or without an external catalyst. An early warning sign is the investment's fractal dimension approaching its natural lower bound. Encouragingly, this trigger has consistently identified countertrend moves of various magnitudes across all asset classes. Chart 11

Helsinki OMX Vs. Eurostoxx 600

Helsinki OMX Vs. Eurostoxx 600

The post-June 9, 2016 fractal trading model rules are: When the fractal dimension approaches the lower limit after an investment has been in an established trend it is a potential trigger for a liquidity-triggered trend reversal. Therefore, open a countertrend position. The profit target is a one-third reversal of the preceding 13-week move. Apply a symmetrical stop-loss. Close the position at the profit target or stop-loss. Otherwise close the position after 13 weeks. Use the position size multiple to control risk. The position size will be smaller for more risky positions. * For more details please see the European Investment Strategy Special Report "Fractals, Liquidity & A Trading Model," dated December 11, 2014, available at eis.bcaresearch.com Fractal Trading Model Recommendations Equities Bond & Interest Rates Currency & Other Positions Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch##br## - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch##br## - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch##br## - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch##br## - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights French labor reforms stack up well against German and Spanish predecessors; We remain bullish on French industrials versus German industrials; Populism is overrated in Germany - European integration may not accelerate, but it will continue; The U.K.'s position remains weak in Brexit talks ... don't expect much from sterling. Feature On recent travels across Asia Pacific, the U.K., and the U.S., Europe has rarely featured in our conversations with clients. We proclaimed European politics a "trophy red herring" in our annual Strategic Outlook.1 Following the defeat of populists in Austria, the Netherlands, Spain, and particularly France, the market now agrees with us (Chart 1). Chart 1European Political Risk Was Overstated

European Political Risk Was Overstated

European Political Risk Was Overstated

In this report, we ask whether there is anything left to say about Europe. First, we provide an update on French structural reforms, which we predicted with enthusiasm in February.2 Second, we give a post-mortem of the German election. Third, we dissect U.K. Prime Minister Theresa May's speech in Florence. We remain positive on near-term and mid-term prospects for European assets. We have recently closed our unhedged long Euro Area equities trade for a 7.88% gain (open from January 25 to September 6). We have reopened the position on September 6 with a currency hedge given our view that there is some downside risk for the euro in the near term. We also remain long French industrials / short German industrials, with gains of 9.30% since February 3. The French Revolution Continues President Emmanuel Macron has ignored tepid union protests and signed five decrees overhauling French labor rules on September 22. While there is more to be done, Macron's swift action just five months after assuming office justifies our optimism about France earlier this year. As we posited in February, investors are surprised every decade by a developed market that defies all stereotypes and catches the markets off guard with ambitious, pro-market and pro-business structural reforms. Margaret Thatcher's laissez-faire reforms pulled Britain out of the ghastly 1970s. Sweden surprised the world in the 1990s. At the turn of the century, Germany's Social Democratic Party (SPD) defied its own "socialist" label and moved the country to the right of the economic spectrum. Finally, the past decade's reform surprise came from Spain, which undertook painful labor and pension reforms that have underpinned its impressive recovery. How do French labor reforms stack up against the German and Spanish efforts? Table 1 surveys the measures and classifies them into three categories. On unemployment benefits, Macron's effort falls short of the considerable cuts implemented as part of the Hartz reforms in Germany. However, while benefits will still be generous, France's unemployed will now be cut off if they refuse job offers that pay within 25% of the salary they previously held. On increasing labor market flexibility, we give France high marks. Reforms will simplify the termination process for economic reasons and cap damages that can be awarded to employees, in line with the Spanish experience. Macron has also managed to neuter the power of national unions by allowing firm-level collective bargaining to take precedence. France's labor bargaining reform is also a carbon copy of the Spanish effort and both are attempts to create a more German-like management-employee context. Table 1Measuring French Reforms Against German And Spanish Reforms

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

What should investors expect as a result? Spain is instructive. While its unemployment rate remains 5.8% above the Italian rate and 7.3% above the French rate, it still fell from a high of 26.3% in 2013 to 17.1% today. Meanwhile, Italian and French unemployment rates remain stubbornly high (Chart 2). In addition, Spain's export competitiveness has had one of the sharpest recoveries in Europe since 2008, whereas Italy and France continue to languish (Chart 3). Spain accomplished this feat via a considerable reduction in labor costs relative to peers (Chart 4). Chart 2Italy, France: Unemployment Still High

Italy, France: Unemployment Still High

Italy, France: Unemployment Still High

Chart 3Spain Regained Competitiveness

Spain Regained Competitiveness

Spain Regained Competitiveness

Chart 4Spain Cut Labor Costs

Spain Cut Labor Costs

Spain Cut Labor Costs

The key pillar of Prime Minister Mariano Rajoy's reforms was to create a more flexible labor market so as to restore competitiveness to the economy by aligning labor costs with productivity. Reforms, passed in February 2012, removed stringent collective bargaining agreements and replaced them with firm-level agreements. This has made it easier for firms to negotiate their own labor conditions, including reducing wages as an alternative to termination of employment. France is now on the path to do the same. True, it is difficult to establish a clear causal connection between Rajoy's structural reforms and Spain's economic performance since 2008. Nevertheless, reforms also work as a signaling mechanism, encouraging investment and unleashing animal spirits by affirming the government's commitment to a pro-business agenda. Under Rajoy's leadership, Spain has moved from 62nd in the World Bank "Ease of Doing Business" survey in 2009 to 32nd in 2017, 18 spots above Italy. Given the speed and commitment of the Macron administration, we would expect an even stronger signaling effect in France. German Hartz reforms are easier to assess because more time has passed since 2005 (when the final stage, Hartz IV, was implemented). Prior to the reforms, Germany's GDP growth rate was falling and unemployment was rising (Chart 5). At least on these two broad measures, it appears that reforms were positive. Chart 5Hartz Reforms Marked Turning Point In Germany

Hartz Reforms Marked Turning Point In Germany

Hartz Reforms Marked Turning Point In Germany

Chart 6German Long-Term Unemployment Benefits Were Cut Down To OECD Average

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

Germany's problem prior to the Hartz reforms was that generous unemployment benefits discouraged unemployed workers from finding employment. Long-term benefits could be as high as 53% of the terminated salary and eligible for indefinite renewal! The Hartz IV reforms specifically targeted these benefits, with the intention of forcing the unemployed to get back to work. Germany brought these benefits into line with the OECD average (Chart 6). The long-term impact of the Hartz reforms was a dramatic decline in the unemployment rate from a bottom of 9.2% in 2001 to the still falling 3.7% of today! Reforms have also seen a steady increase in wage growth, despite the conventional view saying the opposite. Wages have been steadily rising since implementation in 2005, only slowing down during the global financial crisis and the subsequent European debt crisis (Chart 7). This does not mean that labor reforms failed. The intention of the Hartz reforms was to push people back into the labor force, not necessarily suppress their wages. Chart 8 shows the effect on the hours worked in the economy, with a clear uptrend after the reform was enacted. Chart 7German Wages Recovered...

German Wages Recovered...

German Wages Recovered...

Chart 8...While Working Hours Increased

...While Working Hours Increased

...While Working Hours Increased

In line with the previous labor reform efforts in Europe, we think that investors should expect three broad developments from French labor reforms: Competitiveness: As Chart 3 suggests, Spain and Germany have had the best export performance in Europe. By allowing companies some flexibility in setting costs, these economies were able to regain export competitiveness. As a play on this theme, we are long French industrials relative to German peers. Unemployment: Forcing the unemployed back to the labor market by ending their unemployment benefits if they refuse a job offer within 25% of the previous income level should encourage workers to get back to the labor force. Confidence: Macron's labor reforms are only the beginning of a packed agenda that also includes reducing the size of the public sector, reducing the wealth tax on productive assets, and cutting corporate taxes significantly. What of the opposition to the reform effort? What if the French leadership backs down in the face of protest? First, we must ask, what protest? The labor union response has been underwhelming. In part, this is because Macron's reforms are packed with pro-union clauses. The intention is to empower union activity at the firm level in order to neuter its activity at the national level. Second, Macron's electoral victory was overwhelming, both the presidential and legislative. Yes, turnout was low. And yes, many voted for Macron just so that Marine Le Pen would not become president. But the fact remains that 85% of the seats in the National Assembly are held by pro-reform parties, including the pro-business, right-wing Les Républicains, who want even stricter reforms. Bottom Line: Our clients, colleagues, friends, and family all tell us that France will not reform. But we have seen this film before, with Germany in the 2000s and Spain in the 2010s. One day, investors will wake up and France will be more competitive. Fin. A German Election Post-Mortem The media narrative before and after the German election tells of the rise of Alternative für Deutschland (AfD), a far-right party that campaigned on an anti-EU and anti-immigration platform. Indeed, the performance of the center-right Christian Democratic Union (CDU) and center-left Social-Democratic Party (SPD), which have dominated German politics since the Second World War, was historically poor (Chart 9). Chart 9Germany's Dominant Parties Underperformed...

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

Despite the media hysterics, there were no surprises this year. The AfD performed in line with its polls, only outperforming their long-term polling average by around 2%. Meanwhile, the historic underperformance of the CDU and SPD was also due to the solid performance of the other two establishment parties, the liberal Free Democratic Party (FDP) and the center-left Greens (Chart 10). The FDP stormed back into the Bundestag by more than doubling their performance from 2013, while the Greens maintained their roughly 9% performance. Die Linke, a left-wing party whose Euroskeptic tendencies have dissipated, also gained around 9% of the vote. From a historical perspective, the combined CDU and SPD performance was bad, but roughly in line with their 2009 election result. Chart 10... While Minor Parties Outperformed

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

That said, there was no once-in-a-lifetime global recession this time around to excuse the poor performance of the two establishment parties. German GDP growth is set to be 2.1% in 2017 and the unemployment rate is at a historic 3.7%. Meanwhile, support for the euro is at 81% (Chart 11), which begs the question of why 12.6% voters decided to entrust AfD with their votes. Chart 11Germans Love The Euro

Germans Love The Euro

Germans Love The Euro

The simple answer is immigration and the 2015 asylum crisis. The more complex answer is that AfD's performance was particularly strong in East Germany, where the party is now the second largest after the CDU. The same forces that fueled the Brexit referendum and the election of President Donald Trump are at work in Germany. Voters who feel left behind by the transition to a globalized, service-oriented economy have rebelled against a system that favors the educated and mobile voters. In Germany, the angst is particularly notable in the East, where economic progress has lagged that of the rest of the country. On the other hand, it is ludicrous to compare AfD to Brexit and Trump. After all, AfD received only 12% of the vote. This is in line with, or slightly trails, the performance of other right-wing parties in Europe (Chart 12). Yes, it is disturbing to see a far-right party back in the Bundestag, but it was also naïve to believe that Germany could remain a European outlier forever. In fact, like other right-wing parties in Europe, the party is beset with internal rivalries. Party chairwoman Frauke Petry, who represents the moderate wing of the party, decided to quit one day after the election.3 We would suspect that the party will struggle going forward, particularly now that the influx of asylum seekers has trickled down to insignificance (Chart 13). Chart 12German Far Right Performed In Line With Other European Anti-Establishment Parties

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

Chart 13Refugee Crisis Is Over In Germany And Europe

Refugee Crisis Is Over In Germany And Europe

Refugee Crisis Is Over In Germany And Europe

Going forward, Chancellor Angela Merkel will retain her hold on power. However, she will likely have to do so via a "Jamaica coalition" with the FDP and the Greens.4 Forming such a challenging coalition could take until the New Year. Particularly problematic are the positions of the FDP and the Greens on Europe. The former are mildly Euroskeptic, the latter are rabidly Europhile. Merkel's 2009-13 coalition with the FDP was similarly challenging. The FDP moved towards soft Euroskepticism after the Great Financial Crisis. It combined with CDU's Bavarian sister party - the Christian Social Union (CSU)5 - to vote against a number of European rescue efforts and institutional changes (Chart 14). Merkel had to rely on the opposition SPD, which is staunchly Europhile, to push several European reforms through the Bundestag. More broadly, both the FDP and the CSU were a brake on Merkel during this period, leading to Berlin's halting response to the Euro Area crisis. Chart 14The FDP Hampered German Rescue Efforts Amid Euro Crisis

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

Going forward, a Jamaica coalition is investment-relevant for three reasons: First, it would likely pour cold water on recent enthusiasm about accelerated European integration spurred by the election of President Emmanuel Macron in France. But investors should not read too much into it. As Chart 11 clearly illustrates, Germans are not Euroskeptic. The Euro Area works for Germany. If there is a future crisis, Germany will react to it in an integrationist fashion, shoving aside any coalition agreements to the contrary. And if Merkel has to rely on opposition SPD votes to push through the evolving European agenda, she will do so, regardless of what is said between now and December. Second, Merkel will have to respond to the poor performance of her party. She has to give in to the right wing on illegal immigration. Investors should expect to see tighter border enforcement on Europe's external borders. More relevant to the markets, we expect mildly Euroskeptics critics in her own party, as well as in the FDP and CSU, to be satisfied by officially pushing for Jens Weidmann's presidency at the ECB. Weidmann has recently toned down his criticism of ECB policies - publically defending low interest rates - which is likely a strategy to make himself palatable as the next president. Third, it is widely being discussed that the FDP will demand the finance ministry from Merkel, replacing Wolfgang Schäuble. This would definitely complicate any future efforts to deal with Euro Area sovereign debt crises, were they to emerge. However, the FDP is making a mistake. If they take the finance portfolio, they will be signing off on bailouts in the future. That is a guarantee. Europe is full of moderately Euroskepic finance ministers who have done the same (see: Austria, Finland, and the Netherlands in particular). Finally, the election was a clear failure by Merkel to defend her brand. While she has not signaled a willingness to resign, it is highly likely that she will try to groom her successor over the next four years. The 63 year-old has been in power since 2005. At the moment, the list of potential names for CDU leadership is long, but devoid of star power (Box 1). The one quality of all the potential candidates, however, is that they are pro-Europe. Bottom Line: In the short term, markets have read German elections overly negatively. The euro reacted on the news as if the currency bloc breakup risk premium had risen. It hasn't. In fact, the election could prove to be a long-term bullish euro outcome, given that Merkel will likely have to acquiesce to Jens Weidmann's candidacy for the ECB presidency. The German Bundestag remains overwhelmingly pro-Europe. The now-in-opposition SPD is pro-integration, as are the likely new coalition members, the Greens. Die Linke has evolved from anti-capitalist, soft Euroskeptics to left-of-SPD Europhiles. While FDP remains committed to a mildly Euroskeptic line (pro-Europe, but opposed to further integration), its members will likely have to sacrifice this position in order to be in government in the long term. They won't say that they are doing that, but trust us, they are. The performance of Germany's populist right wing is largely in line with that of other European countries. As such, it signals that Germany is a "normal country," not that there is something particularly disturbing going on. Box 1 Likely Successors To German Chancellor Angela Merkel If Merkel decides to retire, who are her potential successors? Ursula von der Leyen (CDU): Leyen, who has served most recently as defense minister, is often cited as a likely replacement for Merkel. However, she is not seen favorably by most of the population: she has not won first place in her district in any of the past three general elections. She is a strong advocate of further European integration and has supported the creation of a "United States of Europe." Leyen has argued that the European refugee crisis and debt crisis are similar in that they will ultimately force Europe to integrate further. As a defense minister, she has promoted the creation of a robust EU army. She has also been a hardliner on Brexit, saying that the U.K. will not re-enter the EU in her lifetime. The markets and pro-EU elites in Europe would love Leyen, who handled U.S. President Trump's statements on Germany, Europe, Russia and NATO with notable tact. Thomas De Maizière (CDU): Maizière, who has served as minister of interior and minister of defense, is a close confidant of Chancellor Merkel. He was her chief of staff from 2005 to 2009. Like Schäuble, he is somewhat of a hawk on euro area issues (he drove a hard bargain during negotiations to set up a fiscal backstop, the European Financial Stability Fund, in 2010) and as such could become a compromise candidate between the Europhiles and Eurohawks within CDU ranks. Though he has been implicated in scandals as defense minister, he has remained popular by drawing a relatively hard line on immigration policy and internal security. Julia Klöckner (CDU): A CDU deputy chairwoman from Rhineland-Palatinate, Klöckner is a socially conservative protégé of Merkel and a hence a likely candidate to replace her. While remaining loyal to Merkel, she has taken a more right-wing stance on the immigration crisis. She is a staunch Europhile who has portrayed the Euroskeptic AfD as "dangerous, sometimes racist," though she has insisted that AfD voters are not all "Nazis" but are mostly in the middle of the political spectrum and need to be won back by the CDU. We think that she would be a very pro-market choice as she combines a popular, market-irrelevant wariness about immigration with a market-relevant centrism that favors further European integration. Hermann Gröhe (CDU): Gröhe last served as minister of health and is a former CDU secretary general. He is very close to Merkel. He is a staunch supporter of the euro and European integration. Markets would have no problem with Gröhe, although they may take some time to get to know who he is! Volker Bouffier (CDU): As Minister President of Hesse, home of Germany's financial center Frankfurt, Bouffier is in a position to capitalize on Brexit. He is a heavyweight within the CDU's leadership and a staunch Europhile. He has already declared he will run for the top state office again in 2018, though he will be 67 years old by then. The U.K.: Fall In Florence Prime Minister Theresa May tried to reset Brexit negotiations with the EU recently by giving a speech in Florence. We were told by clients and colleagues that it would be an important event, so we tuned in and listened. The speech was largely a dud. It confirmed to us the constraints on London's negotiating position as well as the challenges that Brexit poses to the British economy. May's team is struggling to navigate both. There are three things that investors should take from the speech - most which we have been emphasizing for over a year: The EU exit bill: The U.K. will pay. The one concrete point that Prime Minister May agreed with, for the first time ever, is that London will continue to pay into the current EU seven-year budget period (2014-2020). This should never have been in doubt. Britain's refusing to pay would be the equivalent of a tenant giving notice that he is ending his lease in 24 months, then refusing to pay in the interim. What May did not say is whether the U.K. would pay anything beyond its share of contribution to the EU budget. At the moment, the answer appears to be no, but we don't expect that to be the final word. Services really (really) matter: The U.K. has a competitive advantage in services. This is why May has tried to signal that she wants the broadest trade deal possible, since regular free trade agreements (FTAs) do not provide for deep integration in services. What will the U.K. give in return? May appears to want a Norway-type EU trade agreement with Canada-type liabilities. This won't fly in Brussels. The transition deal will last two years at minimum: This was never in doubt. But due to domestic political pressures, May was afraid of voicing it in public until today. Below we provide excerpts of the most relevant (or irrelevant, but comical) parts of May's speech.6 Our running commentary is in brackets. Theresa May's Florence Speech On Brexit, September 2017: A Reinterpretation By GPS It's good to be here in this great city of Florence today at a critical time in the evolution of the relationship between the United Kingdom and the European Union. It was here, more than anywhere else, that the Renaissance began - a period of history that inspired centuries of creativity and critical thought across our continent and which in many ways defined what it meant to be European. [GPS: Strong opening by May. Odd location for the speech, however. Unless she was looking to ingratiate herself with Matteo Renzi, former mayor of Florence, former prime minister of Italy, and current leader of the ruling Democratic Party]. * * * The British people have decided to leave the EU; and to be a global, free-trading nation, able to chart our own way in the world. For many, this is an exciting time, full of promise; for others it is a worrying one. I look ahead with optimism, believing that if we use this moment to change not just our relationship with Europe, but also the way we do things at home, this will be a defining moment in the history of our nation. [GPS: This is a crucial argument by proponents of Brexit, that leaving the EU is not just about leaving the bloc's oversight, but also about domestic renewal. At the heart of this view is the belief that the EU has shackled the U.K.'s potential economic output with its regulatory oversight and protectionist trade policies. For this to be true, the U.K. has to replace significance labor force growth - from the EU Labor Market - with even greater productivity growth. If the U.K. fails to do this, its potential GDP growth rate will be substantively lower in the future. We do not buy the optimism. For one, the EU has not been a drag on the U.K.'s World Bank Ease Of Doing Businness rankings, where the country ranks seventh. Second, several other EU member states are in the top 20, including Sweden, Estonia, Finland, Latvia, Germany, Ireland and Austria. Third, developed economies have been dealing with sub-standard productivity growth for over a decade, both EU members and non-members. As such, we are pretty certain that the U.K.'s potential GDP growth rate will be lower over the next decade, not higher.] And it is an exciting time for many in Europe too. The European Union is beginning a new chapter in the story of its development. Just last week, President Juncker set out his ambitions for the future of the European Union. [GPS: A nod to the reality that without the U.K. stalling its integration, Europe is now better able to build its "ever closer union." May is essentially conceding here to Charles de Gaulle's argument, articulated in the 1960s, that letting Britain into the club would ultimately be a mistake.]7 There is a vibrant debate going on about the shape of the EU's institutions and the direction of the Union in the years ahead. We don't want to stand in the way of that. [GPS: Reality check: it has literally been the foreign policy of the U.K. to "stand in the way of" of a united Europe for at least six hundred years ...] * * * Our decision to leave the European Union is in no way a repudiation of this longstanding commitment. We may be leaving the European Union, but we are not leaving Europe. Our resolve to draw on the full weight of our military, intelligence, diplomatic and development resources to lead international action, with our partners, on the issues that affect the security and prosperity of our peoples is unchanged. Our commitment to the defence - and indeed the advance - of our shared values is undimmed. Our determination to defend the stability, security and prosperity of our European neighbours and friends remains steadfast. [GPS: As we have argued repeatedly, the U.K. and EU share crucial geopolitical and economic links. As such, it is difficult to see negotiations devolving into the sort of acrimony that many have expected. May understands this and is reminding Europe of how important the U.K. role is, and will continue to be, geopolitically for Europe.] * * * The strength of feeling that the British people have about this need for control and the direct accountability of their politicians is one reason why, throughout its membership, the United Kingdom has never totally felt at home being in the European Union. [GPS: A not-so-slight dig at Europe. Basically, May is saying that U.K. voters live in a democracy. EU voters live in something else.] And perhaps because of our history and geography, the European Union never felt to us like an integral part of our national story in the way it does to so many elsewhere in Europe. [GPS: This is true and can be empirically measured (Chart 15).] Chart 15Brits Have A Strong Sense Of National Identity

Brits And Only Brits

Brits And Only Brits

* * * For while the UK's departure from the EU is inevitably a difficult process, it is in all of our interests for our negotiations to succeed. If we were to fail, or be divided, the only beneficiaries would be those who reject our values and oppose our interests. [GPS: This is all true and very well put. But it also appears to be a line of argument designed to tug at Europe's emotional strings. Like a husband asking his wife to take it easy on him in a divorce "for the sake of the children."] So I believe we share a profound sense of responsibility to make this change work smoothly and sensibly, not just for people today but for the next generation who will inherit the world we leave them. [GPS: Literally the line about the kids followed immediately!] * * * But I know there are concerns that over time the rights of EU citizens in the UK and UK citizens overseas will diverge. I want to incorporate our agreement fully into UK law and make sure the UK courts can refer directly to it. Where there is uncertainty around underlying EU law, I want the UK courts to be able to take into account the judgments of the European Court of Justice with a view to ensuring consistent interpretation. On this basis, I hope our teams can reach firm agreement quickly. [GPS: An important concession - the first in the speech so far, and we are more than halfway through: London will apparently take into account ECJ rulings when dealing with EU citizens living in the U.K. That is a huge concession to Europe and an arrangement unlike anywhere else in the world.] * * * The United Kingdom is leaving the European Union. We will no longer be members of its single market or its customs union. For we understand that the single market's four freedoms are indivisible for our European friends. We recognise that the single market is built on a balance of rights and obligations. And we do not pretend that you can have all the benefits of membership of the single market without its obligations. [GPS: As we have said in the past, May's decision to concede this point in January was a major concession to the EU and is the reason that the negotiations are not and will not be acrimonious. If the U.K. demanded access to the Common Market without accepting the "four freedoms," it would have received an acrimonious response, given that its request would have been construed as "special treatment."] So our task is to find a new framework that allows for a close economic partnership but holds those rights and obligations in a new and different balance. But as we work out together how to do so, we do not start with a blank sheet of paper, like other external partners negotiating a free trade deal from scratch have done. In fact, we start from an unprecedented position. For we have the same rules and regulations as the EU - and our EU Withdrawal Bill will ensure they are carried over into our domestic law at the moment we leave the EU. [GPS: May is correct. The EU-U.K. trade negotiations should be relatively smooth given that the U.K. is not starting from scratch in negotiating the relationship. The Canada-EU FTA took seven years because they were starting from scratch.] So the question for us now in building a new economic partnership is not how we bring our rules and regulations closer together, but what we do when one of us wants to make changes. One way of approaching this question is to put forward a stark and unimaginative choice between two models: either something based on European Economic Area membership; or a traditional Free Trade Agreement, such as that the EU has recently negotiated with Canada. I don't believe either of these options would be best for the UK or best for the European Union. European Economic Area membership would mean the UK having to adopt at home - automatically and in their entirety - new EU rules. Rules over which, in future, we will have little influence and no vote. [GPS: We pointed out why such an arrangement would be illogical in March 2016. Essentially, the U.K. would leave the EU due to its onerous regulation and infringement on sovereignty only to accept the onerous regulation as a fait accompli with no room for British sovereignty (Diagram 1)!] Diagram 1The Central Paradox Of Brexit

Is There Anything Left To Say About Europe?

Is There Anything Left To Say About Europe?

Such a loss of democratic control could not work for the British people. I fear it would inevitably lead to friction and then a damaging re-opening of the nature of our relationship in the near future: the very last thing that anyone on either side of the Channel wants. As for a Canadian style free trade agreement, we should recognise that this is the most advanced free trade agreement the EU has yet concluded and a breakthrough in trade between Canada and the EU. But compared with what exists between Britain and the EU today, it would nevertheless represent such a restriction on our mutual market access that it would benefit neither of our economies. [GPS: This is, by far, the most critical part of May's speech. She is essentially saying that a Canadian FTA deal would benefit the EU more than it benefits the U.K., a point we have made for nearly two years now. This is true. The U.K. needs access to the EU services market, where British exporters have a comparative advantage. Were they to secure an FTA deal with the EU instead, they would be giving Europe a massive advantage, given the bloc's comparative advantage in tradable goods (Chart 16). However, this takes us back to Diagram 1. What kind of a relationship does May expect to get from the EU when she is unwilling to accept any of the liabilities inherent in such a deep trade deal? That is precisely what the Common Market is for.] Chart 16Brexit Hinders U.K.'s Comparative Advantage

Brexit Hinders U.K.'s Comparative Advantage

Brexit Hinders U.K.'s Comparative Advantage

Bottom Line: Prime Minister May's Florence speech has shown the limits of the U.K.'s negotiating position. May set a friendly tone with Europe, but she has nothing to bargain with. Much of the speech reiterated British commitment to Europe's security and its capacity to defend the continent from external threats. In exchange, May argues, the U.K. ought to receive the deepest and most expansive access to the EU Common Market without any of the liabilities that go with it. In particular, she wants access to the EU's services market, where U.K. exporters have a comparative advantage. The problem with the tradeoff between U.K. geopolitical benefits and EU economic benefits is that it suggests that London has an alternative to being a geopolitical ally to Europe! As if it could suddenly shift its geopolitical, military, and diplomatic focus elsewhere. Berlin, Brussels, and Paris will call London's bluff. The U.K. is not in North America, it is in Europe. As such, Europe's problems are the U.K.'s problems, and the U.K. must defend against them even if it receives little in return. We expect the U.K. to succumb to the reality that the EU holds most of the cards in the negotiations. The U.K. will have a lower potential GDP growth rate after Brexit. But before Brexit is solidified, we expect considerable domestic political upheaval. In the short term, there is some upside for the pound. In the long term, it is a sell. Marko Papic, Senior Vice President Chief Geopolitical Strategist marko@bcaresearch.com Jesse Anak Kuri, Research Analyst jesse.kuri@bcaresearch.com 1 Please see BCA Geopolitical Strategy Strategic Outlook, "Strategic Outlook 2017: We Are All Geopolitical Strategists Now," dated December 14, 2016, available at gps.bcaresearch.com. 2 Please see BCA Geopolitical Strategy and Foreign Exchange Strategy Special Report, "The French Revolution," dated February 3, 2017, available at gps.bcaresearch.com. 3 Although she has herself played a role in kicking out the original, even more moderate, founders of the party. 4 The CDU, FDP, and Greens coalition is dubbed the "Jamaica coalition" because of their traditional colors - black, yellow, and green - which combine to make the colors of the Jamaican flag. 5 The CSU does not directly compete against the CDU on the federal level. It only fields candidates in Bavaria, where the CDU does not compete. 6 For the full transcript, please see "Theresa May's Florence speech on Brexit, full text," The Spectator, September 22, 2017, available at blogs.spectator.co.uk. 7 In turn, this will allow the EU to build up its power, develop a navy, and finally conquer the British Isles with a new armada somewhere around 2066! Geopolitical Calendar

Highlights Even isolated North Korean attacks are unlikely to lead to a full-scale war; The USD sell-off will start to reverse once Trump makes Gary Cohn his official pick for Fed chairman; Europe is not a risk for investors ... even Italy is only a longer-term risk; France is reforming; stay long French industrials versus German. Feature Last week, in London, we were scheduled to give a talk on Sino-American tensions, East Asian geopolitical risks, and North Korea specifically. We submitted our topic of choice about a month ahead of the event, when tensions between Pyongyang and Washington were at their height. As tensions temporarily subsided following Supreme Leader Kim Jong-Un's decision to delay the planned missile launch towards Guam, several colleagues wondered if the topic was still a pertinent one. We stressed in our research that tensions would not dissipate and would continue to be market-relevant, if not critical for S&P 500.1 Unfortunately, we have been proven right. Forecasting geopolitics requires insight, multi-disciplinary methodology, and a treasure trove of empirical knowledge. But sometimes it also just comes down to using Google and looking at a calendar. For example, given the present context of heightened tensions, the annual U.S.-South Korean military exercises - Key Resolve, which occurs normally in the spring, and Ulchi-Freedom Guardian, which occurs in August - are obvious dates to monitor. They are provocations that North Korea has to respond to for both foreign and domestic audiences. Pyongyang has chosen to do so by firing an ICBM across Japan and testing a sixth nuclear device, allegedly a miniaturized hydrogen bomb. While both these actions qualitatively expand on previous acts (missile and nuclear tests), neither cross a threshold. We are still in the realm of "territorial threat display." President Trump and Supreme Leader Kim are angling their "swords," but have not dared to cross them yet. Nonetheless, our clients have pointed out that our "arch of diplomacy" approach leaves a lot to imagination. Therefore, the first insight from the road of this week is that we need to put our thinking cap on and imagine a scenario where tensions do blow over into open conflict. How do we imagine such a scenario occurring and why would it not devolve into full out war that forces the U.S. to attack the North Korean mainland? Is North Korea About To Become A Praying Mantis? We can imagine a scenario where North Korea commits an act that takes us beyond the nuanced thresholds set by recent history (Chart 1). For example, we have cited to clients that an attack against international shipping in the Yellow Sea or Sea of Japan by North Korean submarines would be an unprecedented act that the U.S. and Japan would likely retaliate against.2 We could see the U.S. following the script from 1988 Operation Praying Mantis in the Persian Gulf - the largest surface engagement by the U.S. Navy since the Second World War - when the U.S. sunk half of Iran's navy in retaliation for the mining of the guided missile frigate USS Samuel B. Roberts. In the case of North Korea, this would primarily mean taking out its approximately 20 Romeo-class submarines and an unknown number of domestically-produced - Yugoslav-designed - newly built submarines.3 Chart 1North Korean Provocations Rarely Affect Markets For Long

North Korean Provocations Rarely Affect Markets For Long

North Korean Provocations Rarely Affect Markets For Long