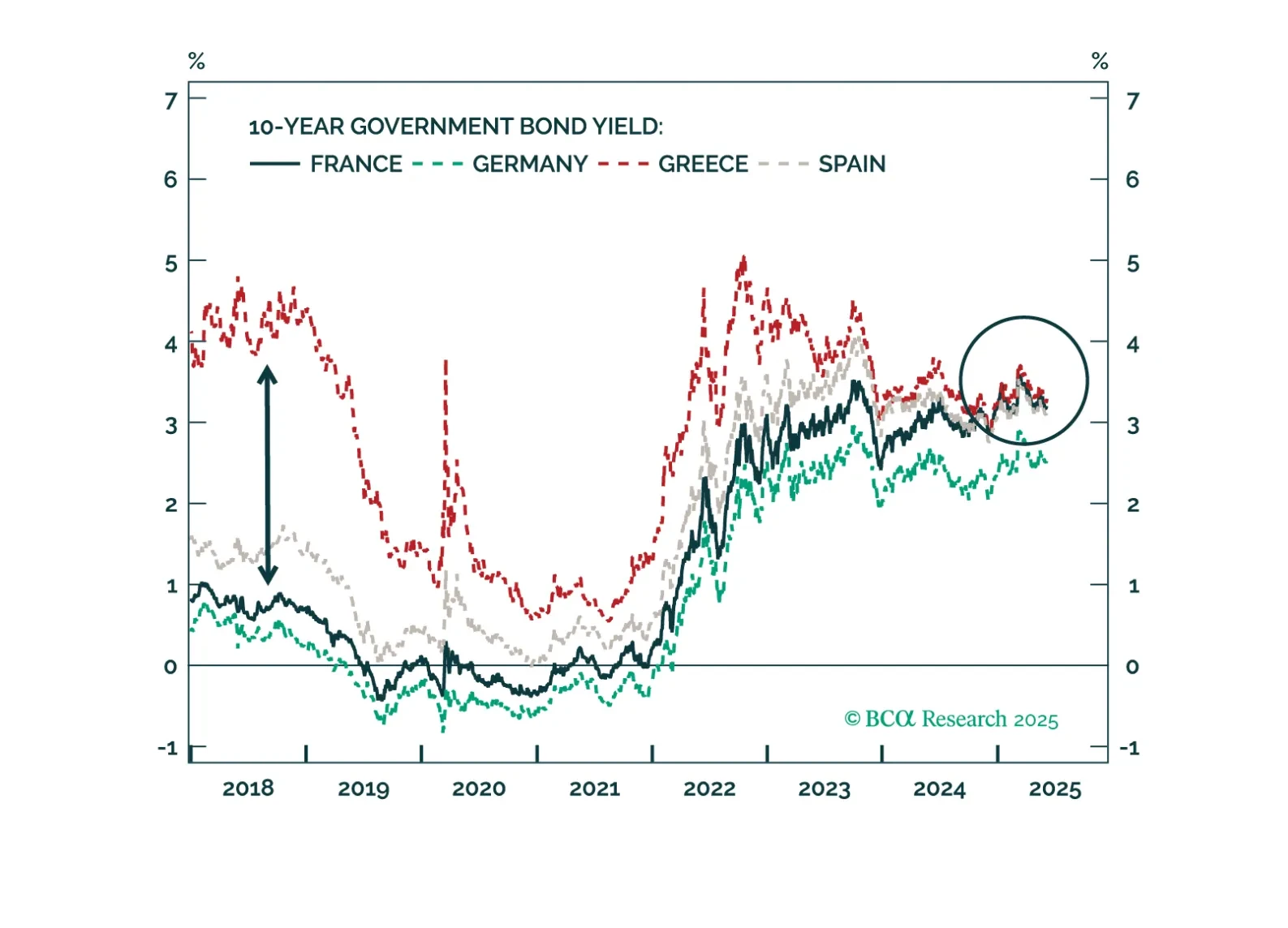

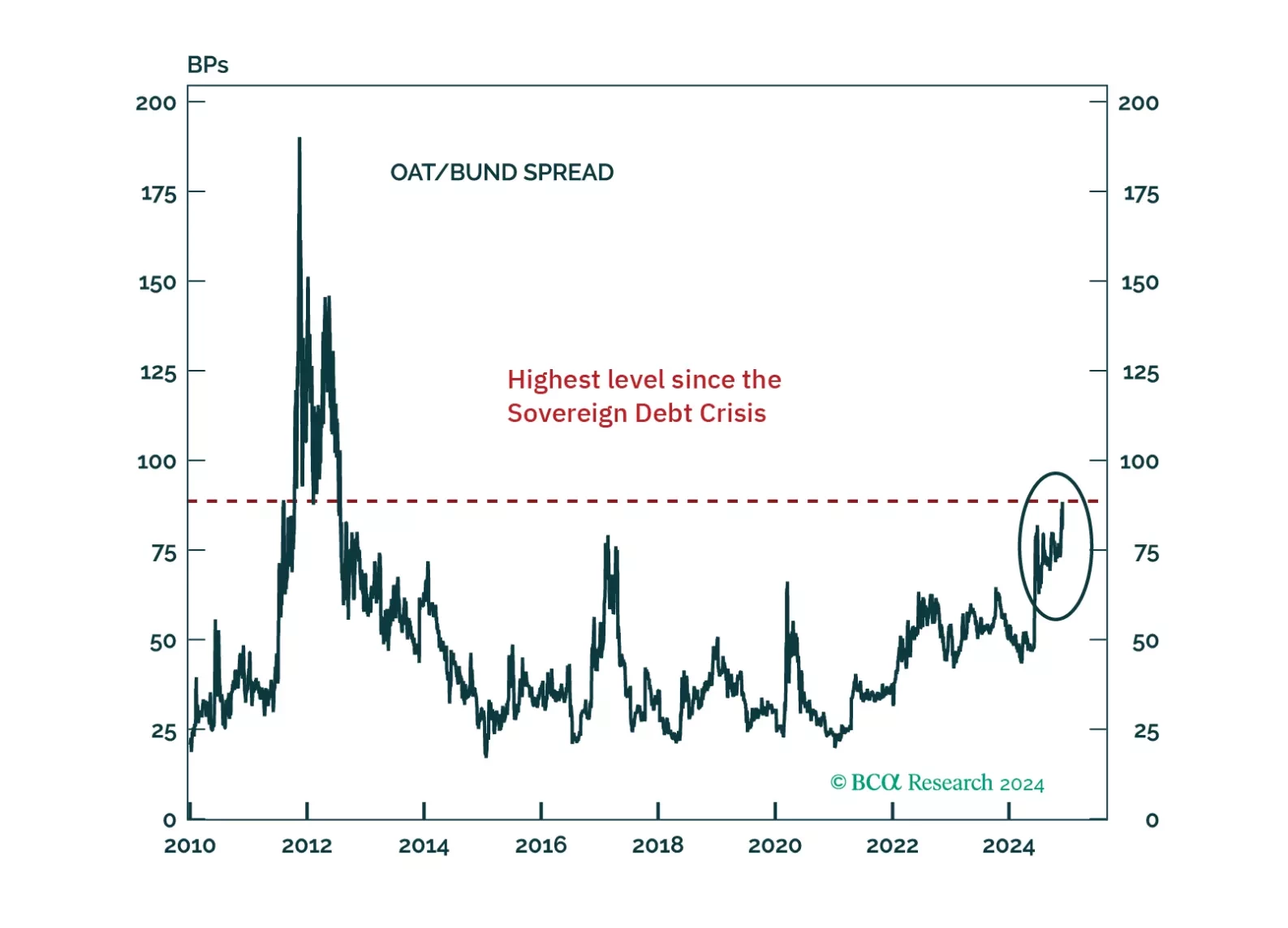

France

France’s political turmoil is far from over, and fiscal fears are growing. This is not a bond-friendly environment. In contrast, it is a good time to upgrade French equities. As the 2027 presidential race is about to begin in earnest, we make an early call on its outcome.

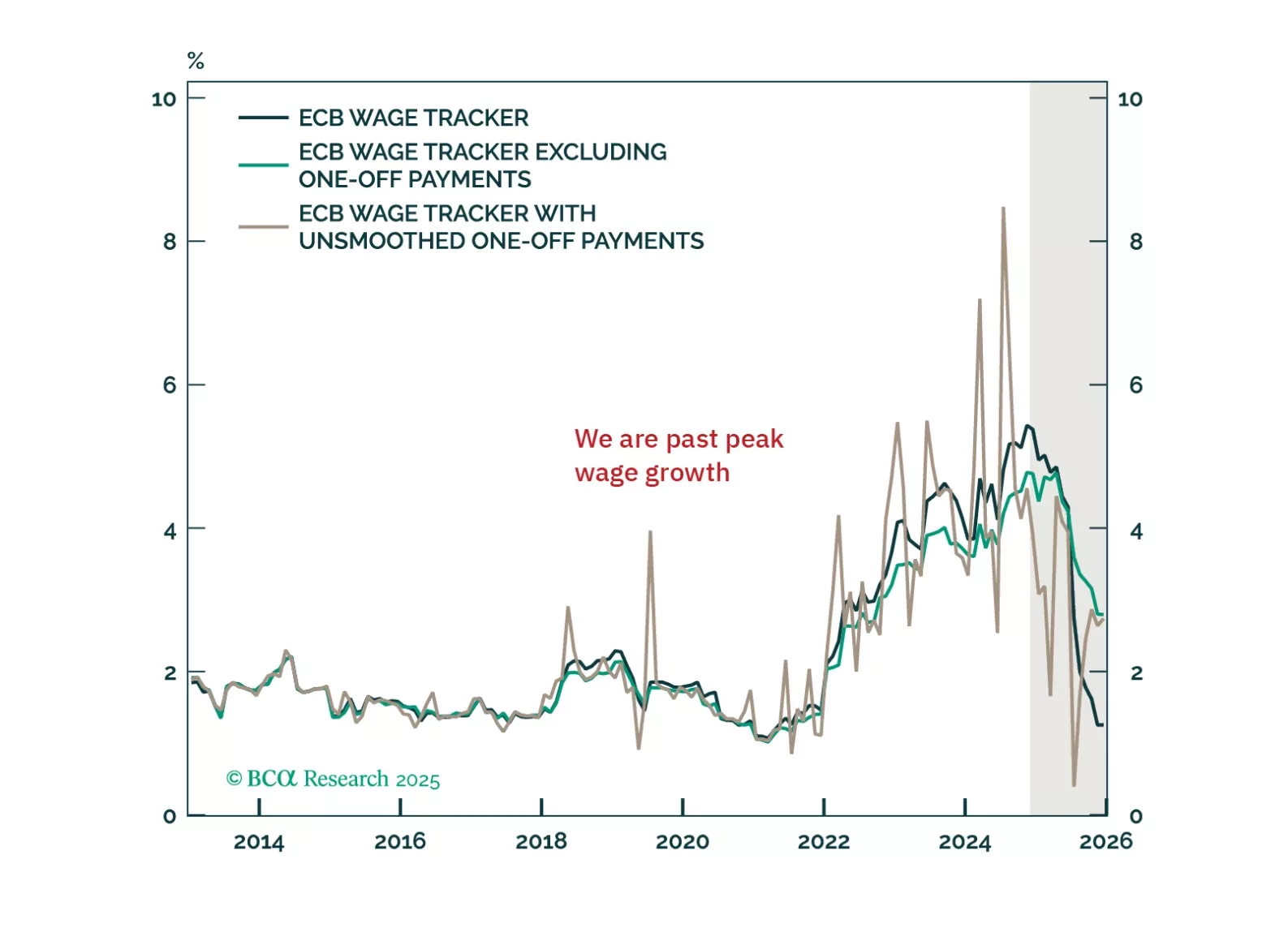

Europe’s deflation problem is getting harder to ignore. This week’s ECB cut is just the beginning — tariffs, the euro’s rally, and softening demand all point to more easing ahead. We explain what it means for yields, equities, and EUR/USD.

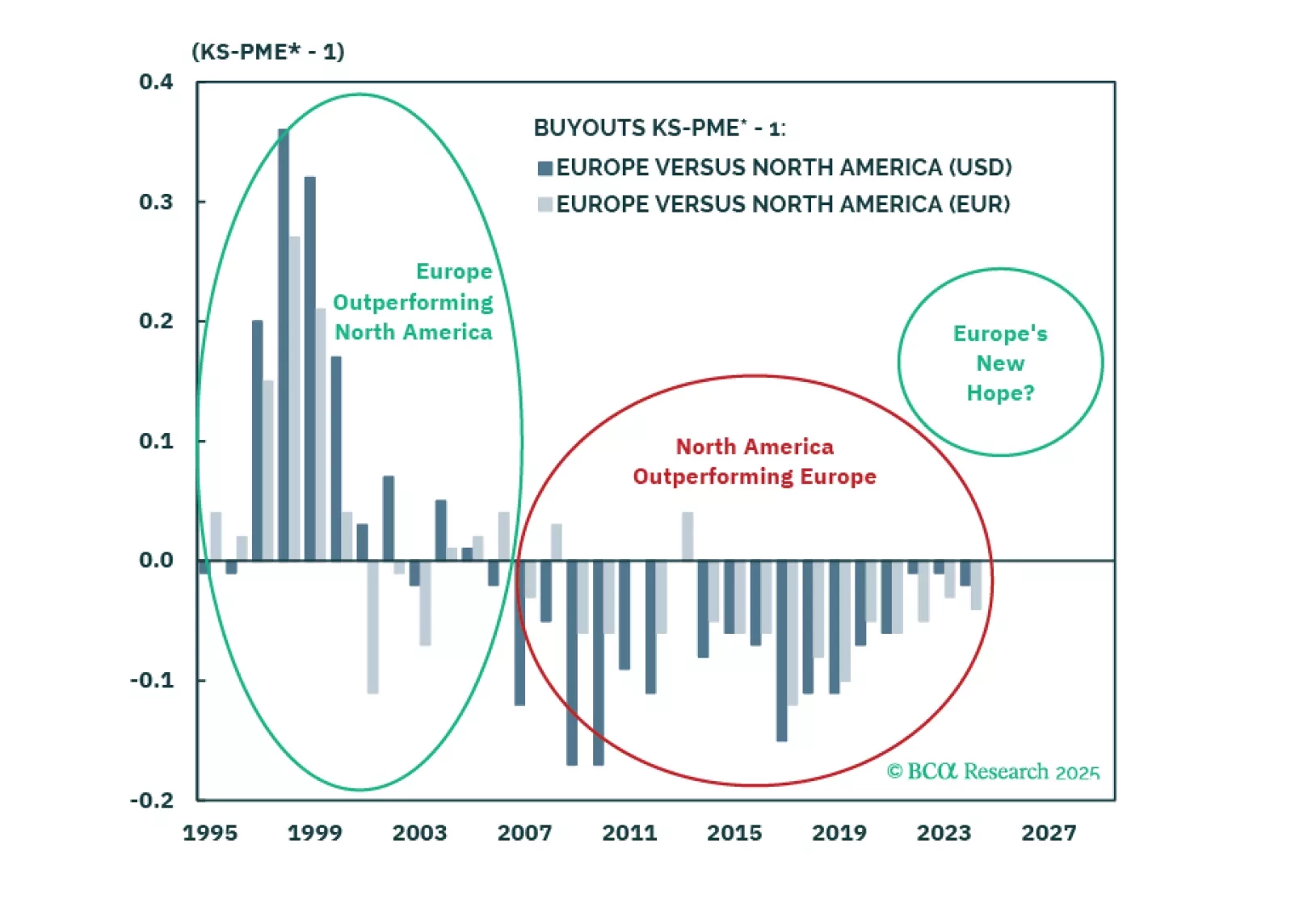

We are at a pivotal moment for Europe, supported by structural reforms and macro catalysts. While expanding credit markets and lower rates favor Private Equity over Private Credit, opportunities vary by segment. Large+ Buyouts are attractive as markets have priced in structural challenges. We downgrade Europe Private Credit, remain neutral on Europe Private Equity broadly but overweight Europe vs. North America in PE portfolios.

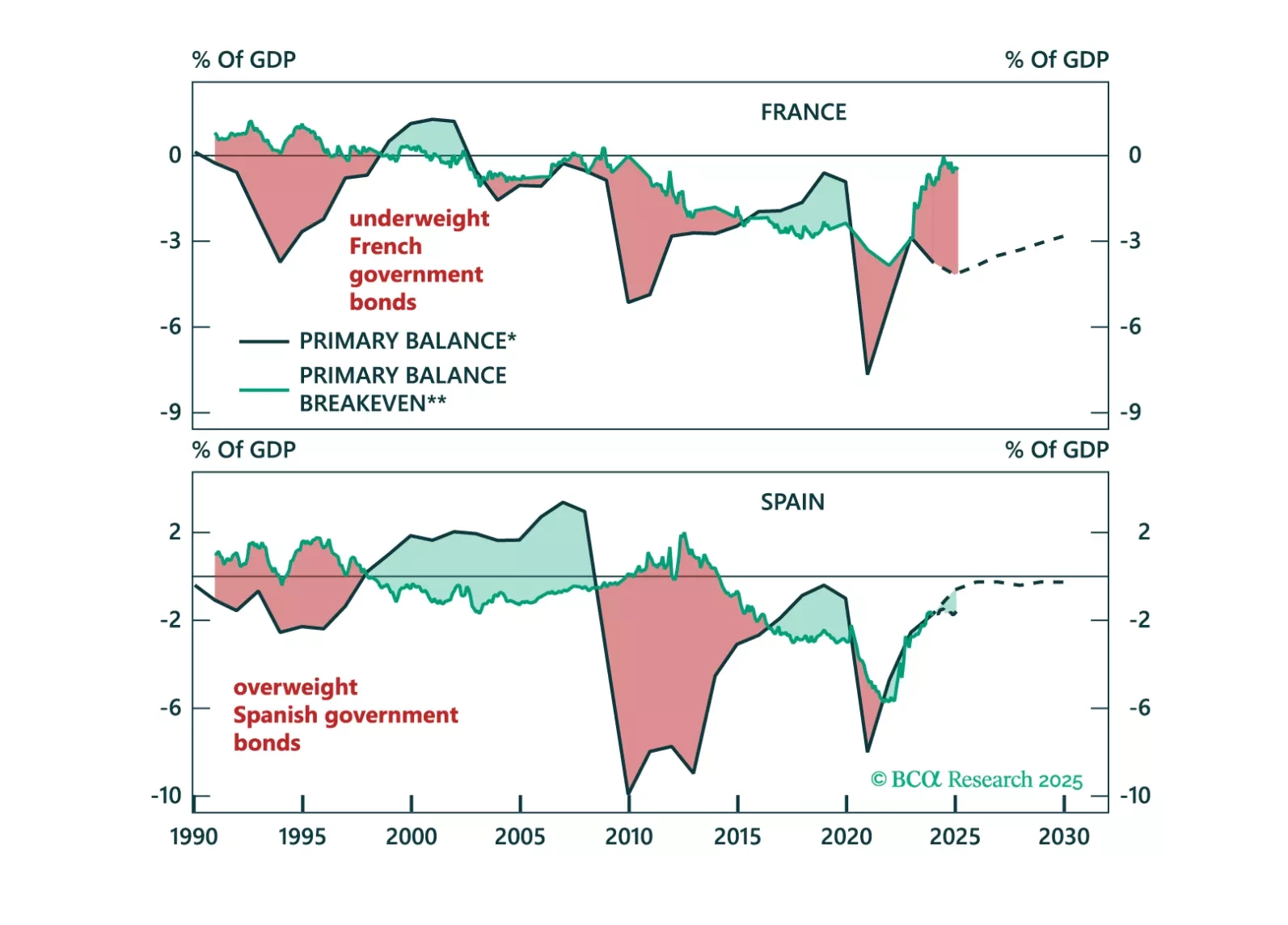

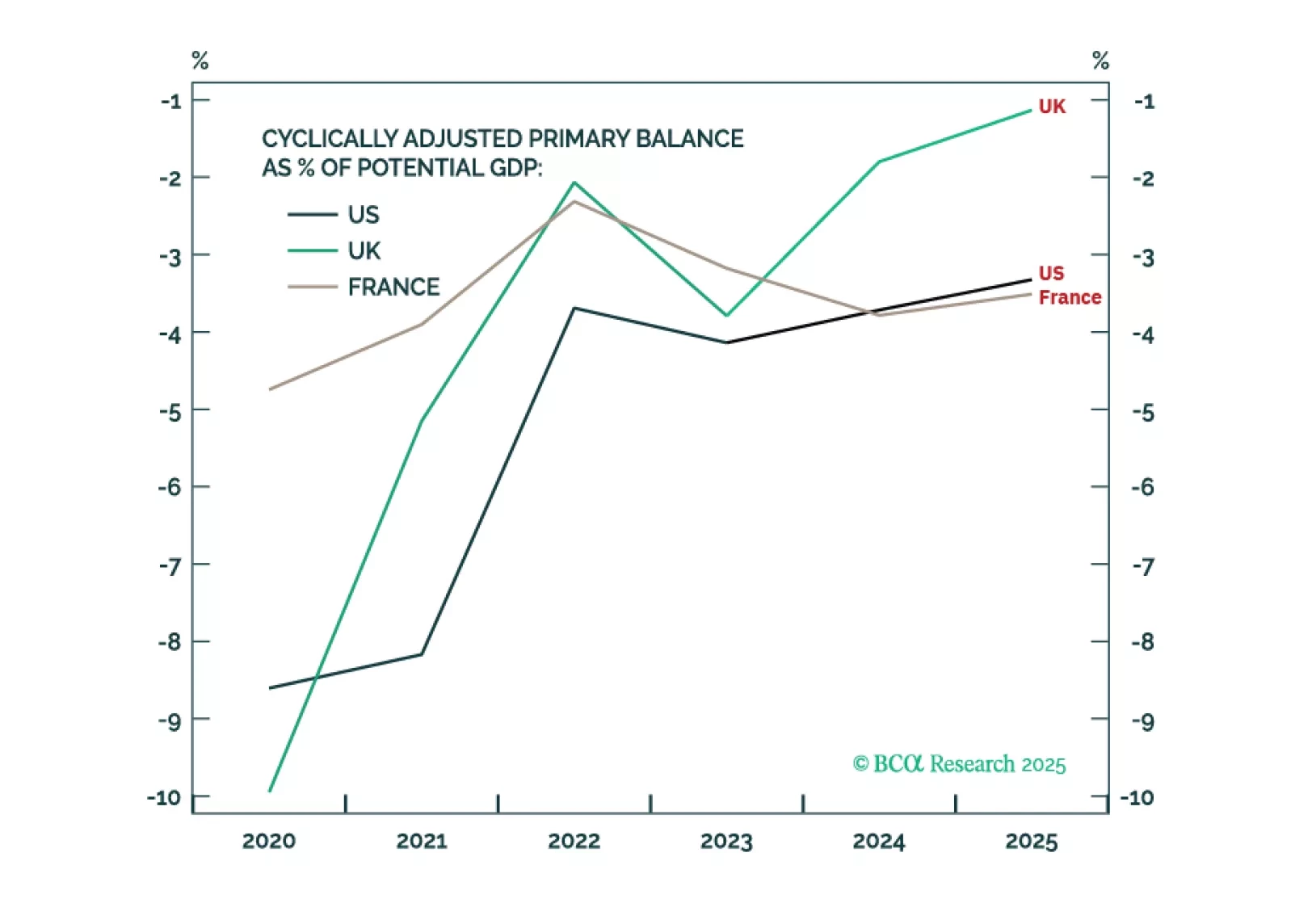

Questions about fiscal risks and their impact on bond markets have become more frequent in client conversations. This Special Report provides a framework to assess a country’s fiscal sustainability and how it affects its bond market outlook. On an individual country basis, Spain has shown a remarkable turnaround in its fiscal sustainability outlook while the fiscal outlook for France continues to deteriorate.

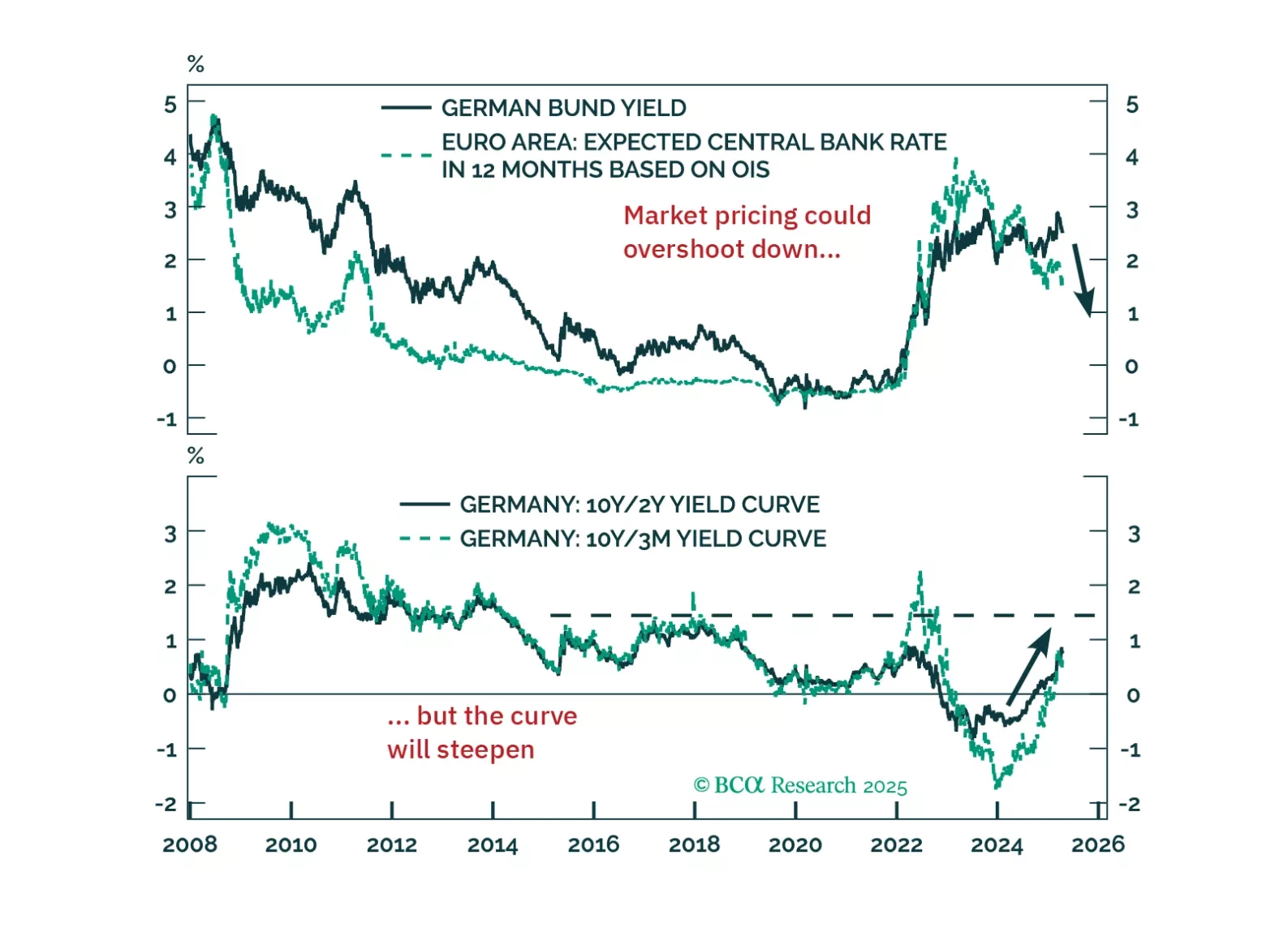

The ECB cut its deposit rate to 2.75%, as was widely anticipated. President Christine Lagarde did not provide any fireworks, but the Governing Council’s message was clear: Policy is restrictive, and inflation will fall further. As a result, if we combine our economic forecasts for the Eurozone with Frankfurt’s data dependency, we continue to expect the ECB’s deposit rate to settle below 2%. Consequently, German bond yields have downside, and the euro has yet to bottomed.

Political instability combined with the maths of debt sustainability is much more concerning in France than in either the UK or the US. Go long UK gilts versus French OATs and go tactically long GBP/USD.

France finds itself in a unique, thorny situation. Can it heave itself out of it? And what does it mean for investors?

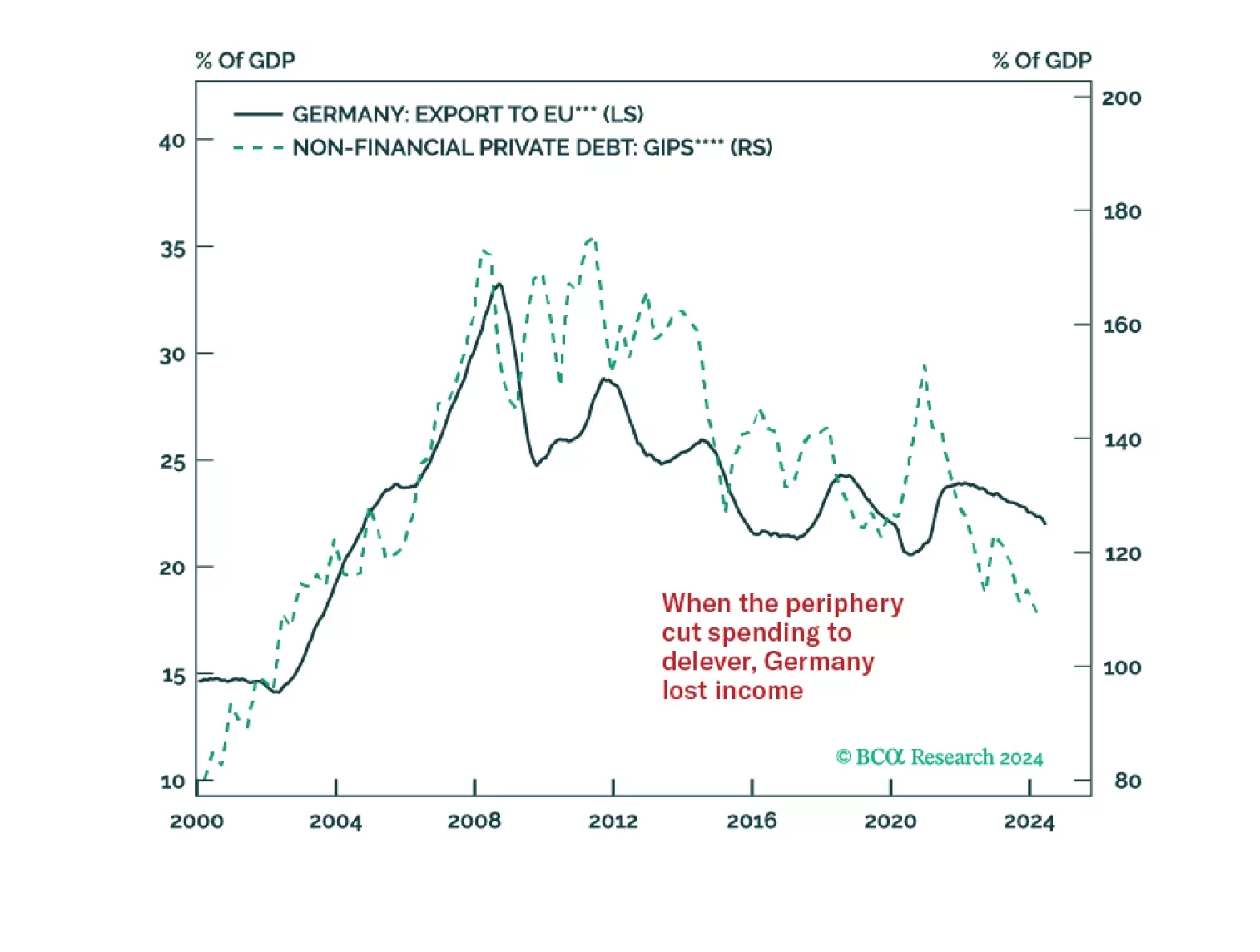

Germany’s economy has lagged that of the rest of Europe for nearly 10 years. So have German stocks. Investors are extrapolating these trends to bet on the country’s deindustrialization. Could Germany manage to beat dismal expectations?