Fixed Income

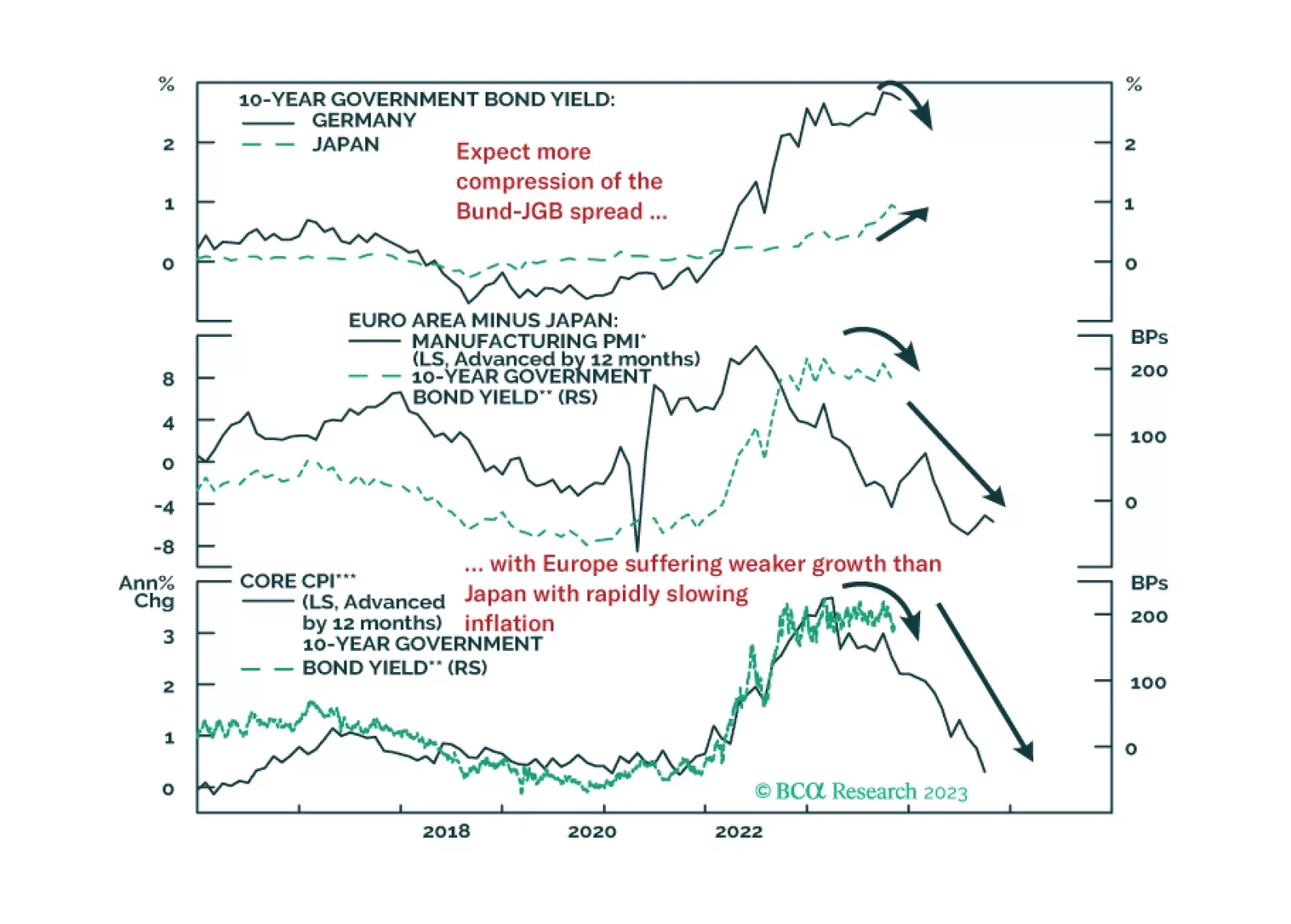

In this Insight, we review the performance and rationale for our current set of tactical fixed income trade recommendations. Our highest conviction positions also happen to be our most successful trades: positioning for a narrowing of the German bund-JGB spread and wider Japanese inflation breakevens.

China's money and credit data remained weak in October. New total social financing amounted to RMB 1.85 trillion – less than the RMB 1.95 trillion anticipated and below the prior month's increase of RMB 4.12 trillion. Similarly, loans extended by banks fell…

Our equally weighted global cyclical equity index has outperformed equally weighted defensives for most of this year. By October 17, this outperformance stood at about 12.6%. This outperformance is consistent with US Treasury market dynamics. The relative…

The preliminary release for the University of Michigan’s Consumer Survey sent a pessimistic signal about consumer sentiment on Friday. The headline index fell from 63.8 to 60.4 in November, below expectations of a marginal decrease to 63.7. Declines in both…

The UK economy stagnated in Q3 – a deterioration from the minor 0.2% q/q expansion in the prior quarter. Although the Q3 figure is slightly better than anticipations of a 0.1% q/q contraction, the details of the report are generally weak. Consumption dropped…

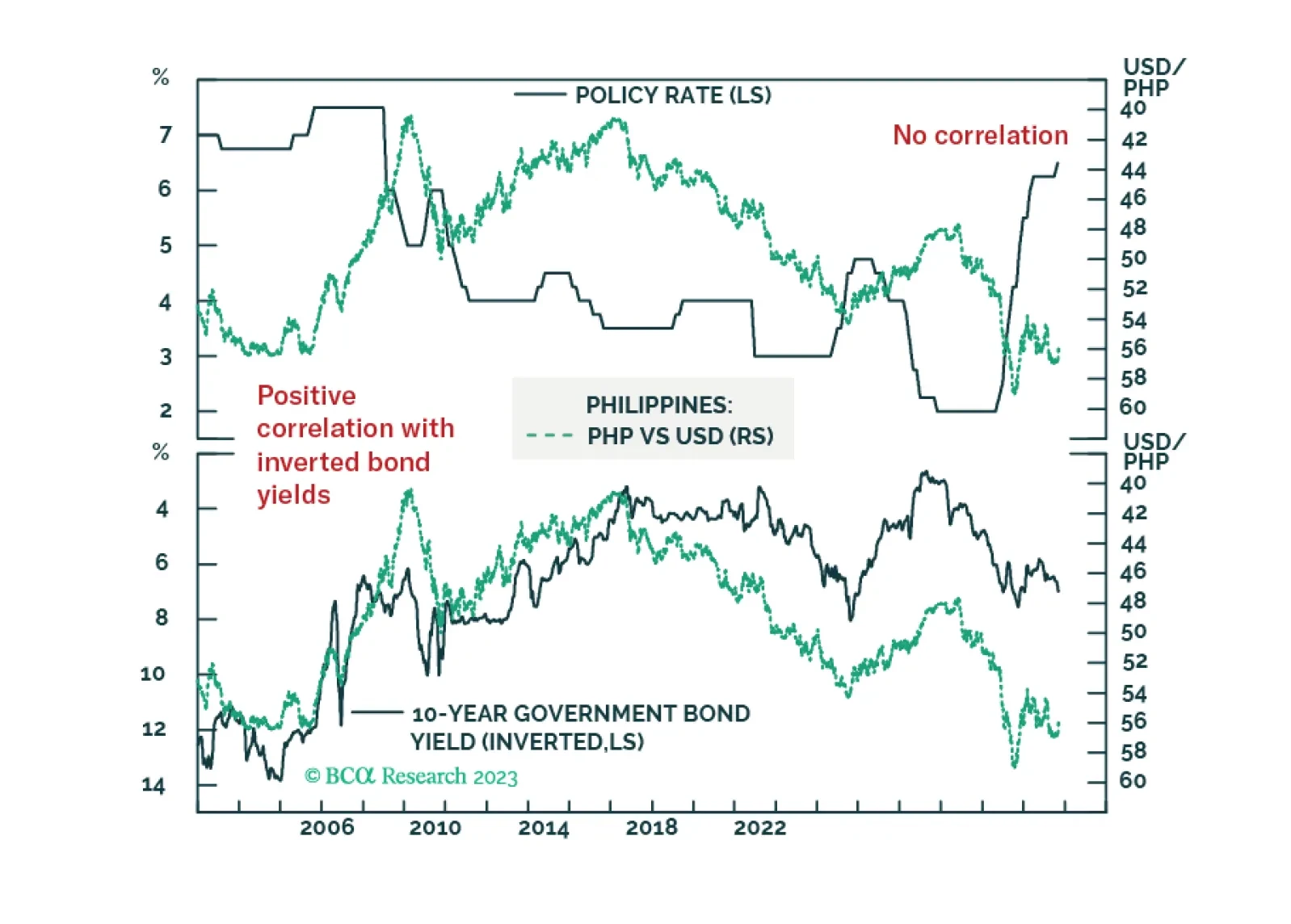

The recent rate hike by the Philippines central bank cannot control food inflation. Nor can it stem the currency slide.

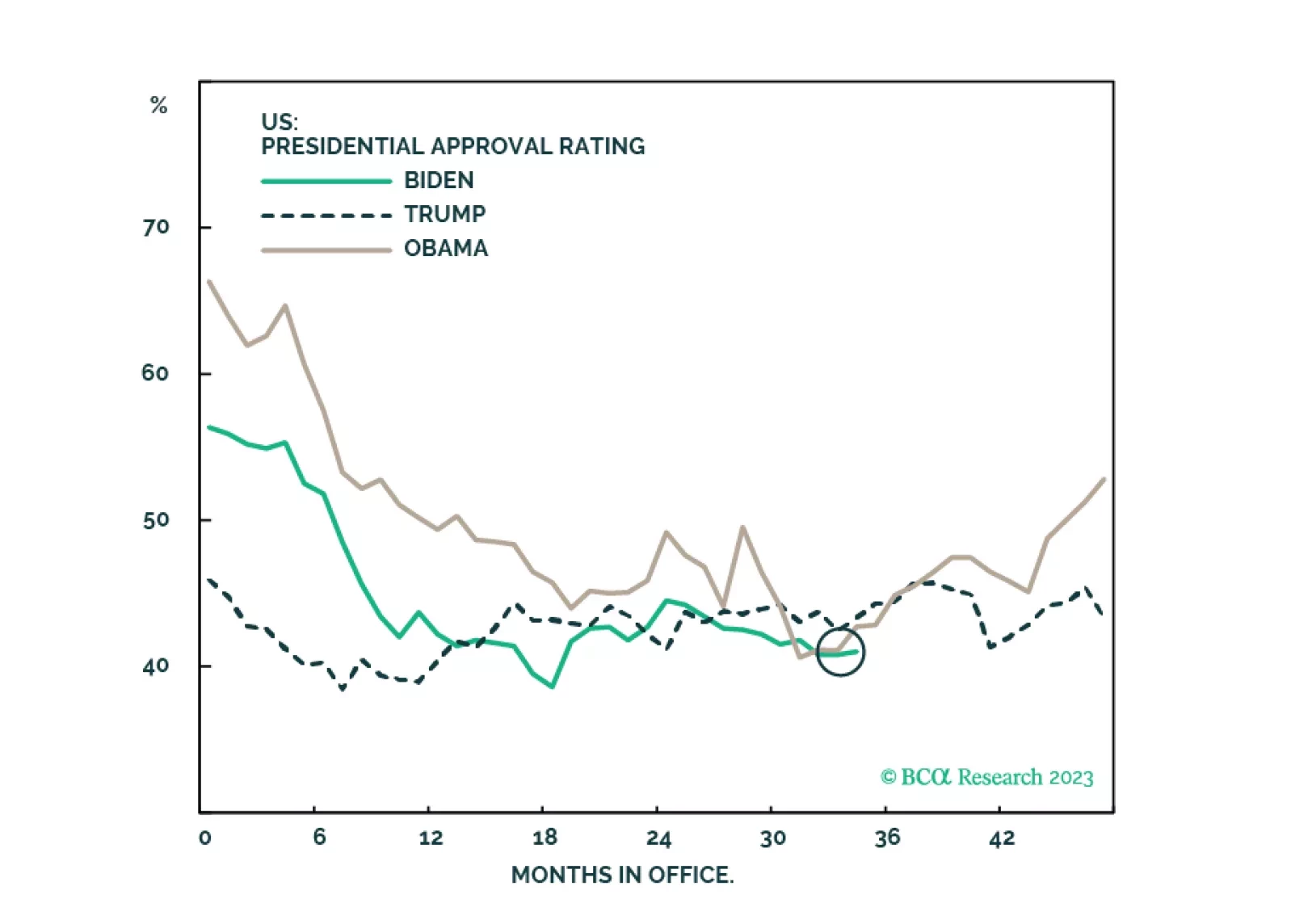

Results from Tuesday’s elections suggest that the Democrats are doing better than what their 2024 polling are showing. While the results are marginally positive for equities, investors should not overrate this off-year election, especially considering the slowing economy and the many foreign challenges facing the US.

According to BCA Research’s Counterpoint service, the ECB is the central bank that poses the lowest risk of repeating the mistakes of the 1970s and letting inflation expectations unanchor. One reason is the ECB’s inherited Germanic anti-inflation DNA. Even…

US small-cap stocks have underperformed significantly this year. While the S&P 500 price index is up 14.0% year-to-date, the S&P 600 has lost 2.5%. However, this underperformance has not been a straight line down. Small caps benefited from a…

The economies of Canada and Australia share many similarities. Both nations are major commodity exporters, but with overvalued housing markets and highly indebted consumers. Lately, however, a notable gap has appeared between the economic…