Fixed Income

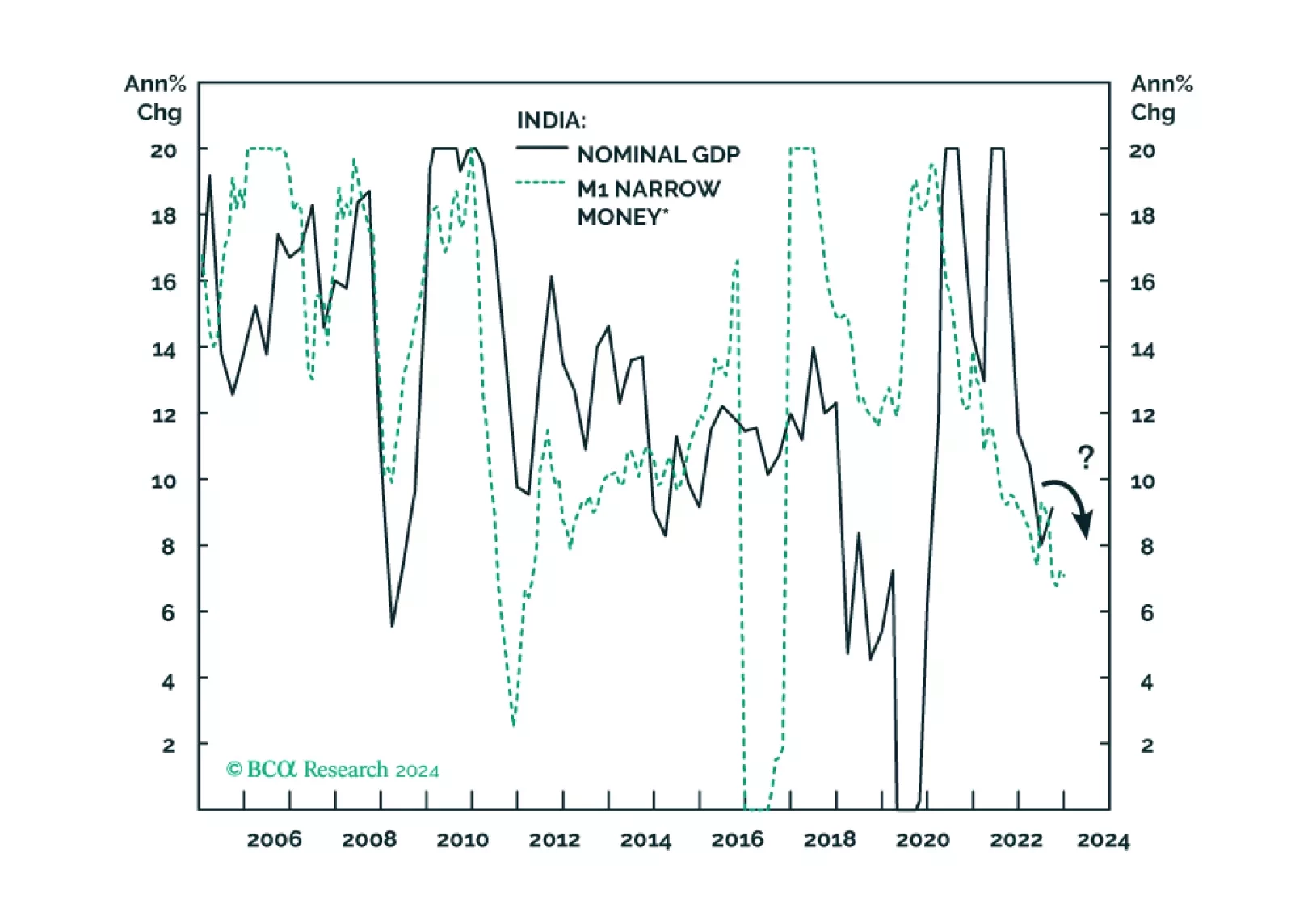

Decelerating nominal sales, a peaking credit cycle, and very high valuations - Indian stocks will not escape the carnage when risk assets globally begin to sell off.

The SEC has just approved bitcoin spot ETFs, but does bitcoin have any ‘intrinsic’ value? In this Special Report we explain why the answer is yes, how bitcoin compares with gold, and why the bitcoin price could ultimately head well north of $100,000.

The market will eventually be forced to react to rising odds of a sharp US national policy reversal. Investors should overweight government bonds and defensive equity sectors.

In light of the hotter-than-expected US CPI report, we look at what interest rate currency investors should focus on. Our conclusion largely keeps our existing trades in place, as published in our outlook, a few weeks ago.

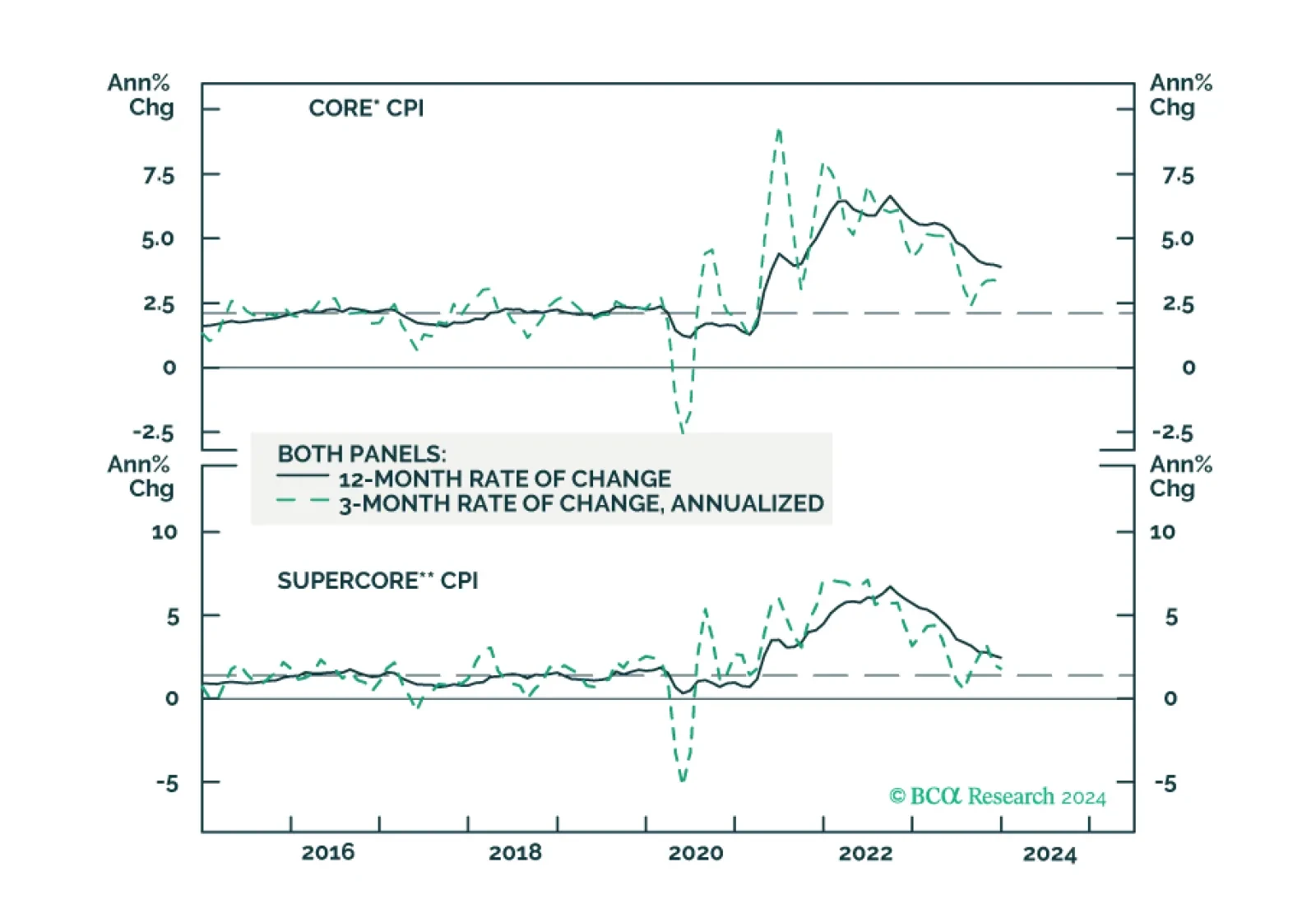

We update our inflation forecast following this morning’s CPI report.

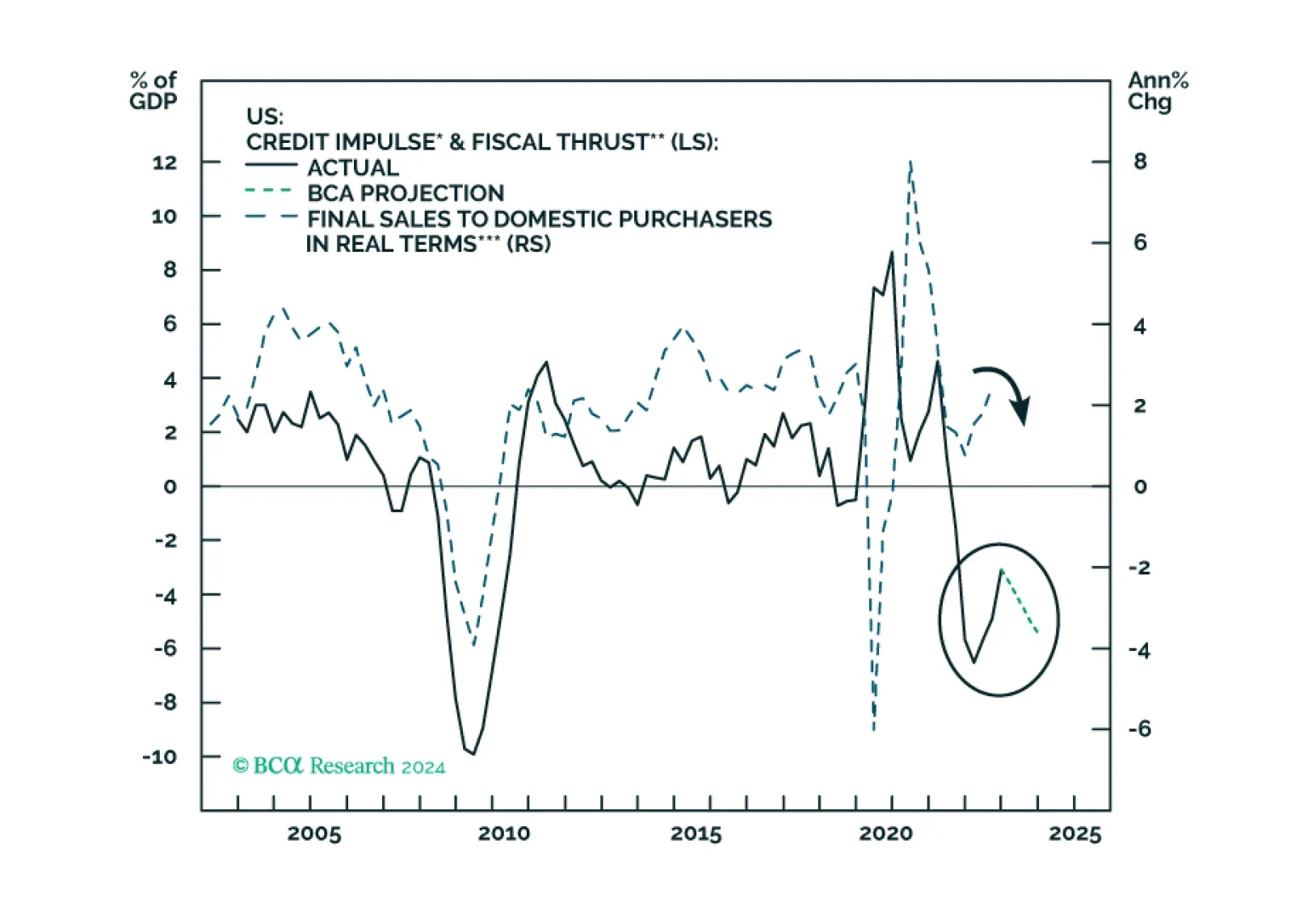

The combined US credit impulse and fiscal thrust indicator will likely relapse in 2024, heralding growth weakness. Stalling US sales volume and falling inflation, combined with sticky labor costs, will herald a non-trivial profit margin compression. The recent increase in Asian exports will likely prove to be a mid-cycle improvement rather than a cyclical recovery.