Fixed Income

Investors typically associate high-flying tech stocks with high sensitivity to interest rates. The rationale is simple: Given that most of their cashflows are further into the future, their value will be more sensitive to changes in their discounter. And…

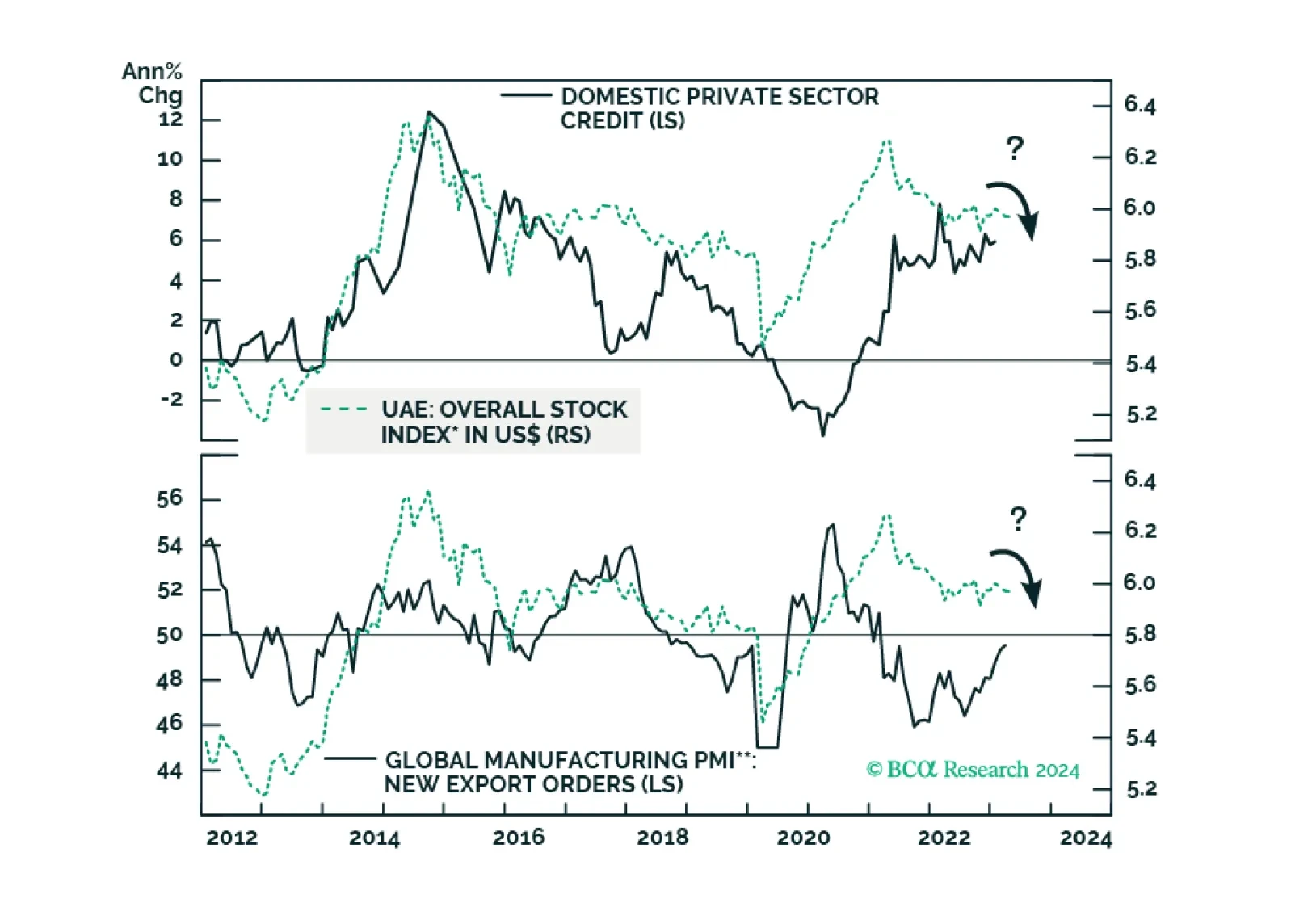

Subdued credit growth and weak global trade will remain headwinds for Emirati stocks. Surging property prices, which have led to a boom in real estate stocks, will also peak soon. Stay neutral on this bourse. Sovereign credit investors, however, should stay overweight UAE in EM credit portfolios.

The recent rise in market-based inflation expectations has caught the attention of market participants. Some investors have begun to worry that the Federal Reserve might be losing control of its inflation mandate by cutting rates sooner than it should. But…

Traditionally, equity managers have thought of oil equities as cyclical. This is because, in the past, oil equities had a strong positive correlation to the overall market. But US oil equities have increasingly become more defensive. Their 36-month rolling…

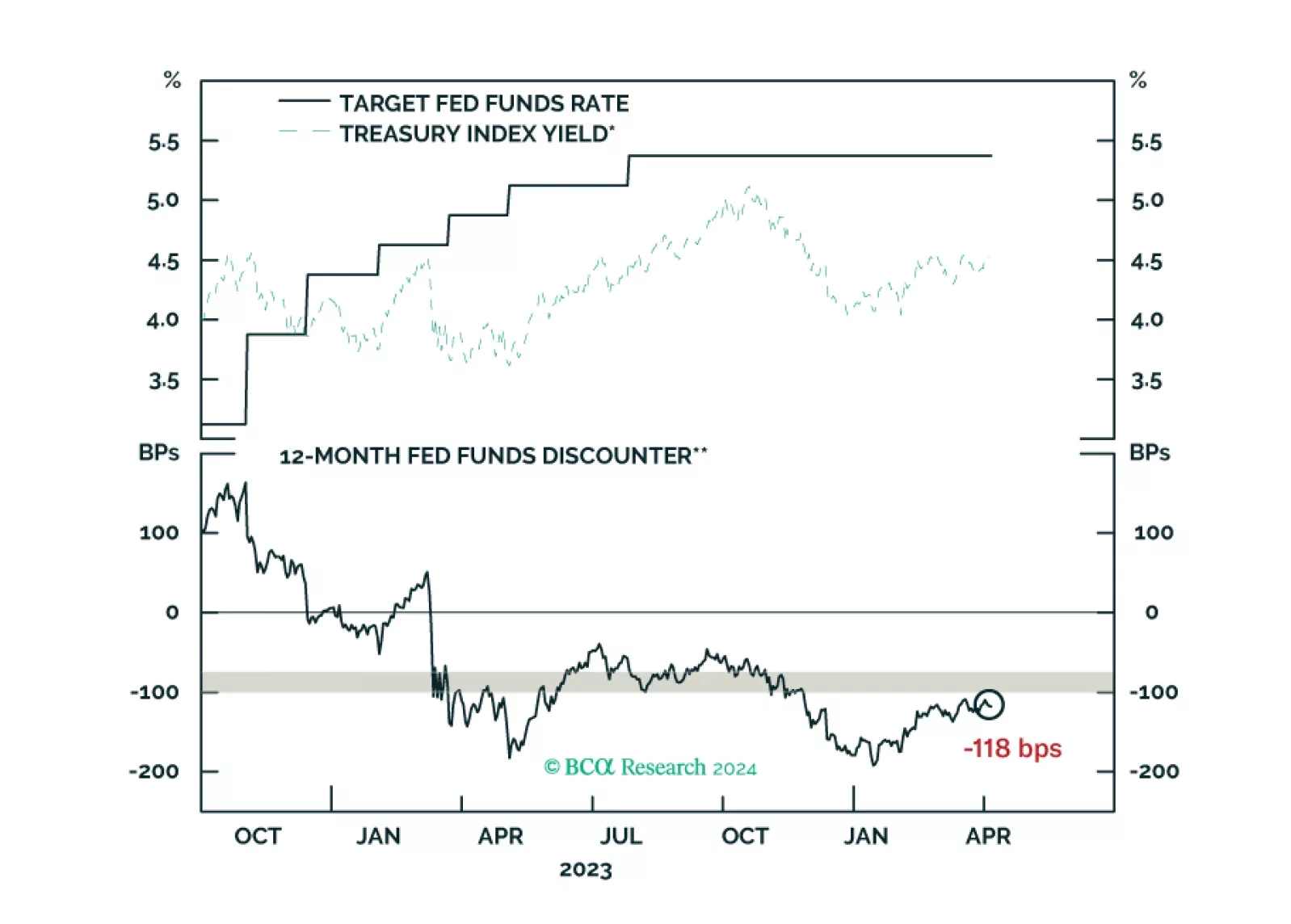

According to BCA Research’s US Bond Strategy service, until labor market cracks emerge, the path of least resistance for bond yields is probably higher, but the potential near-term upside in yields is limited. The team is monitoring three indicators that…

Gold prices reached $2300 per ounce for the first time on Wednesday. They have now rallied by more than 12% so far this year. To a degree the furious rally in gold has been puzzling. Who has been buying? It certainly has not been private investors. Global…

Our reaction to this morning’s employment report and bond market moves.

It is too early for the RBA to begin cutting rates. Inflation remains above target, with core CPI currently standing at 3.4%, one of the highest numbers amongst major economies. The labor market is also fundamentally strong. Australia’s unemployment rate…

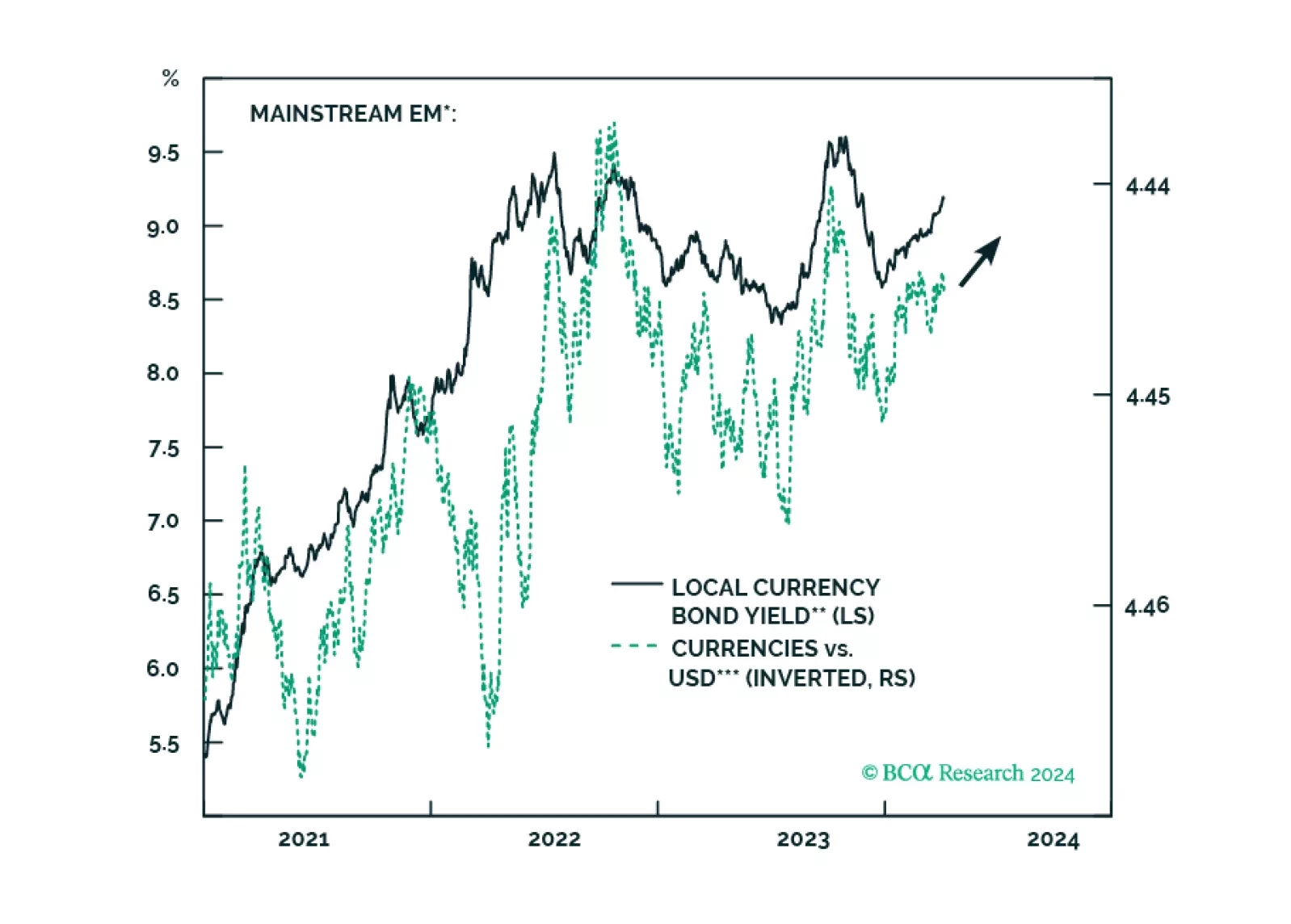

Climbing US bond yields, alongside higher oil prices, might spoil the party for global risk assets. There are budding cracks in EM domestic bonds, and even though we like this asset class in the long run, investors exposed to it should reduce their positions for now.

Flash estimates for Euro Area inflation in March surprised to the downside. Headline inflation slowed from 2.6% to 2.4% versus expectations of 2.5% and core inflation eased from 3.1% to 2.9% versus expectations of 3%. While the stickiness of services…