Fixed Income

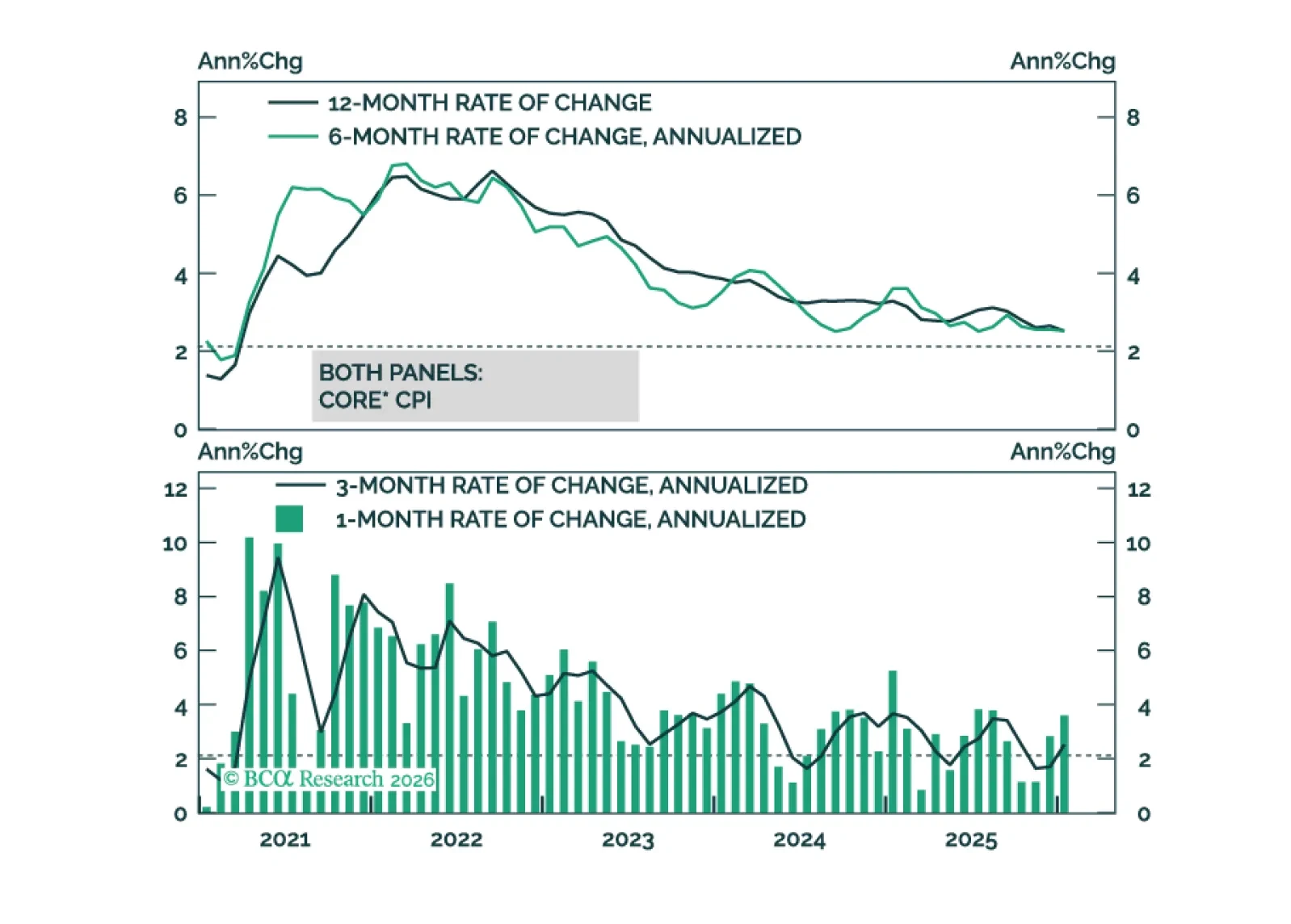

Core inflation will get close to the Fed’s 2% target by the end of this year.

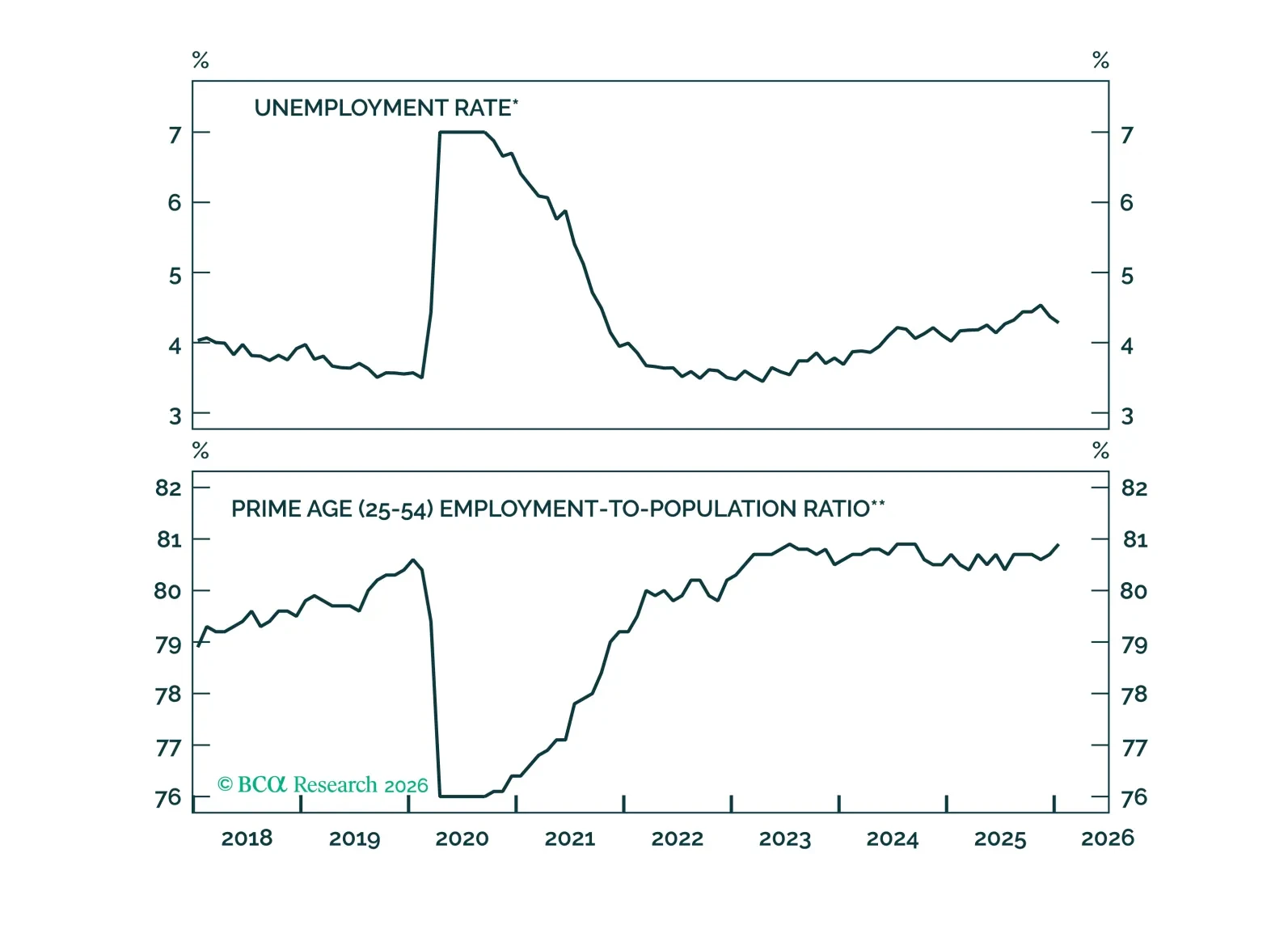

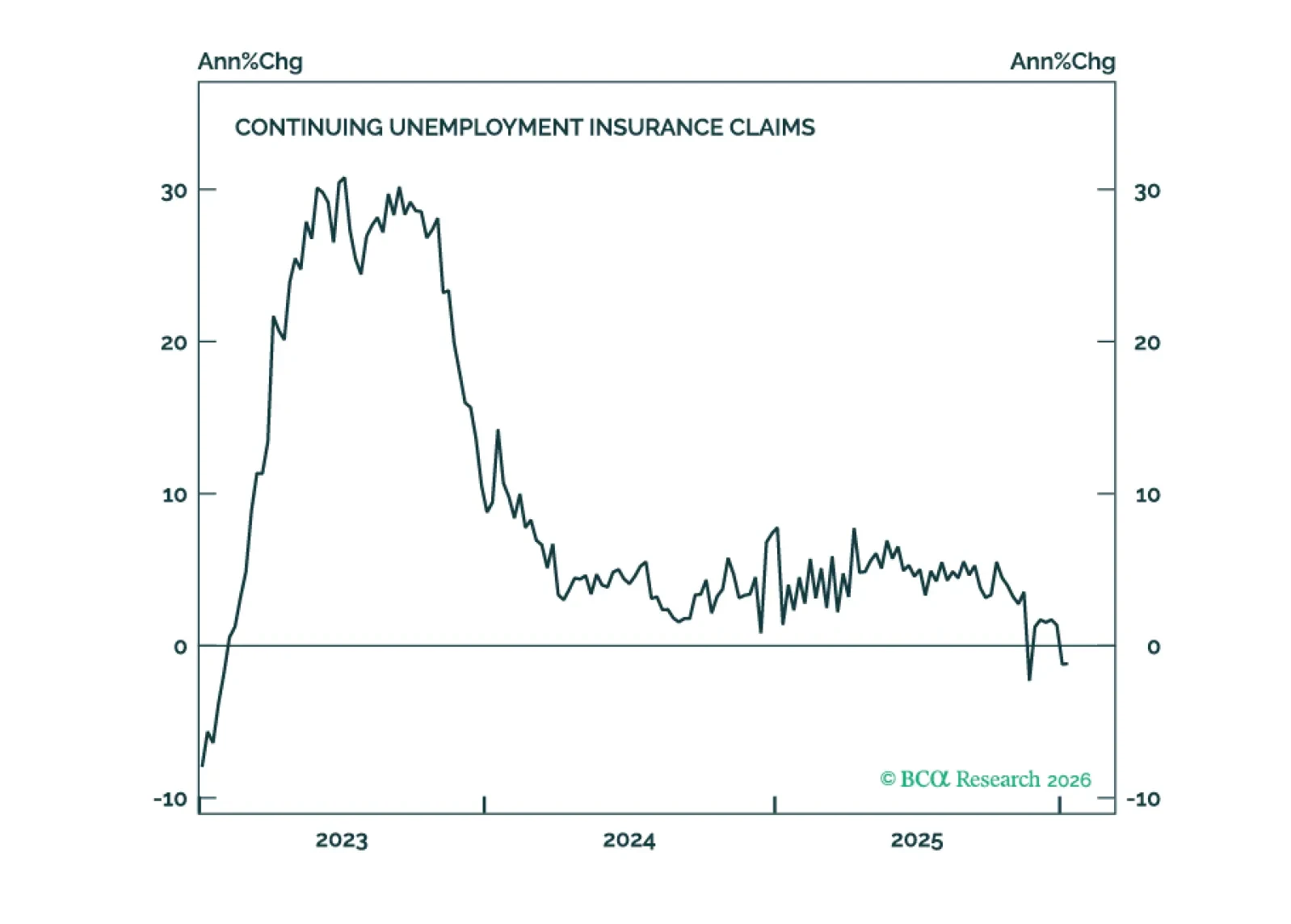

The labor market tightened in January, significantly lowering the odds of a H1 2026 rate cut. Rate cuts driven by lower inflation are still likely in H2 2026.

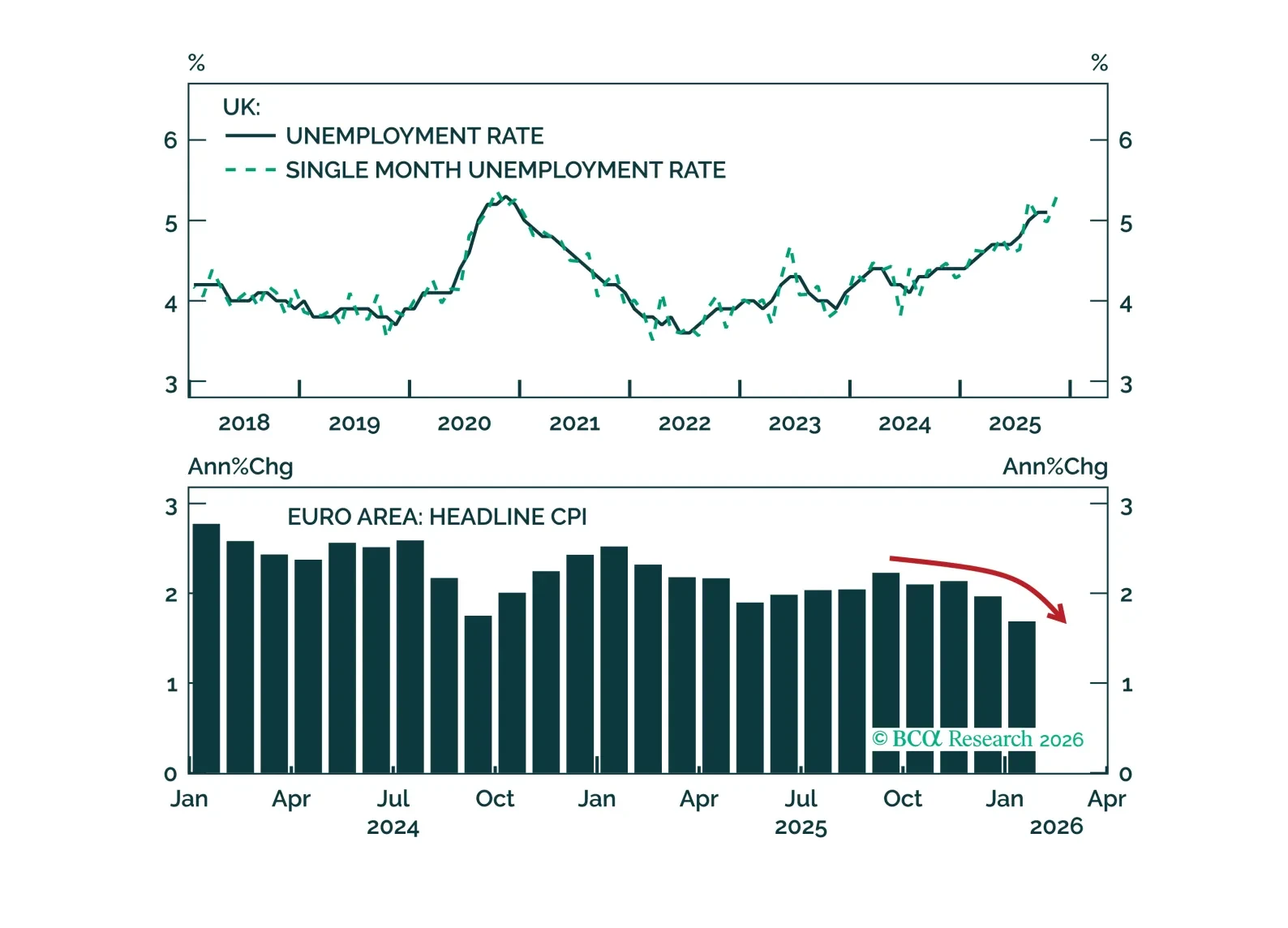

This week’s central bank meetings are a good reminder that monetary policy can still surprise. The Bank of England sounded more dovish, and the European Central Bank sounded complacent about the inflation undershoot. Meanwhile, the Reserve Bank of Australia hiked rates earlier this week. Investors should remain overweight UK Gilts, position for more ECB easing by going long the September 2026 3-month Euribor futures, and fade further rate hikes priced in Australia.

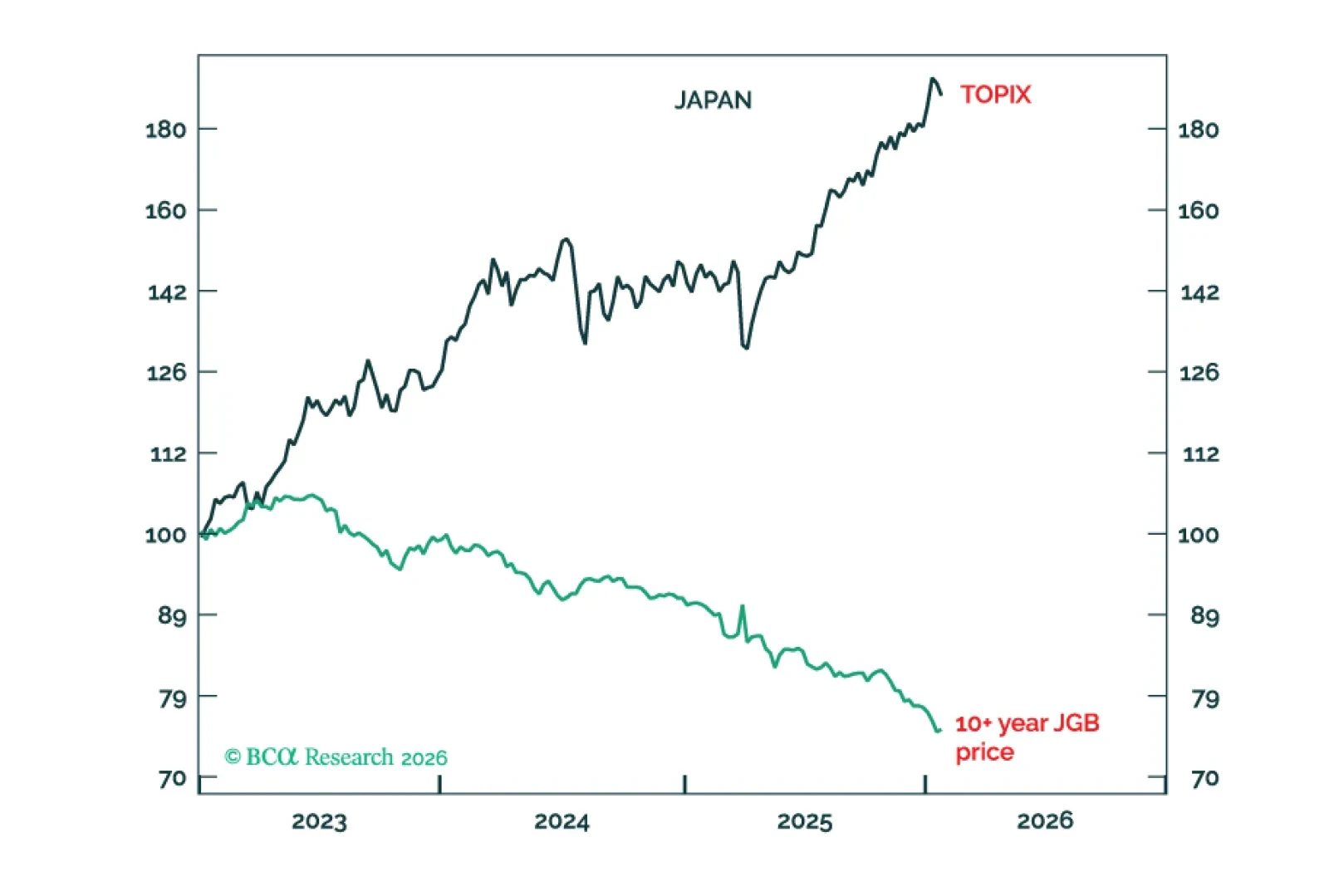

The US and Japan are in the same predicament: save the bond market or save the stock market? How this predicament will be resolved is the biggest global macro call of 2026-27. Plus: a new tactical trade is to go short AUD/JPY.

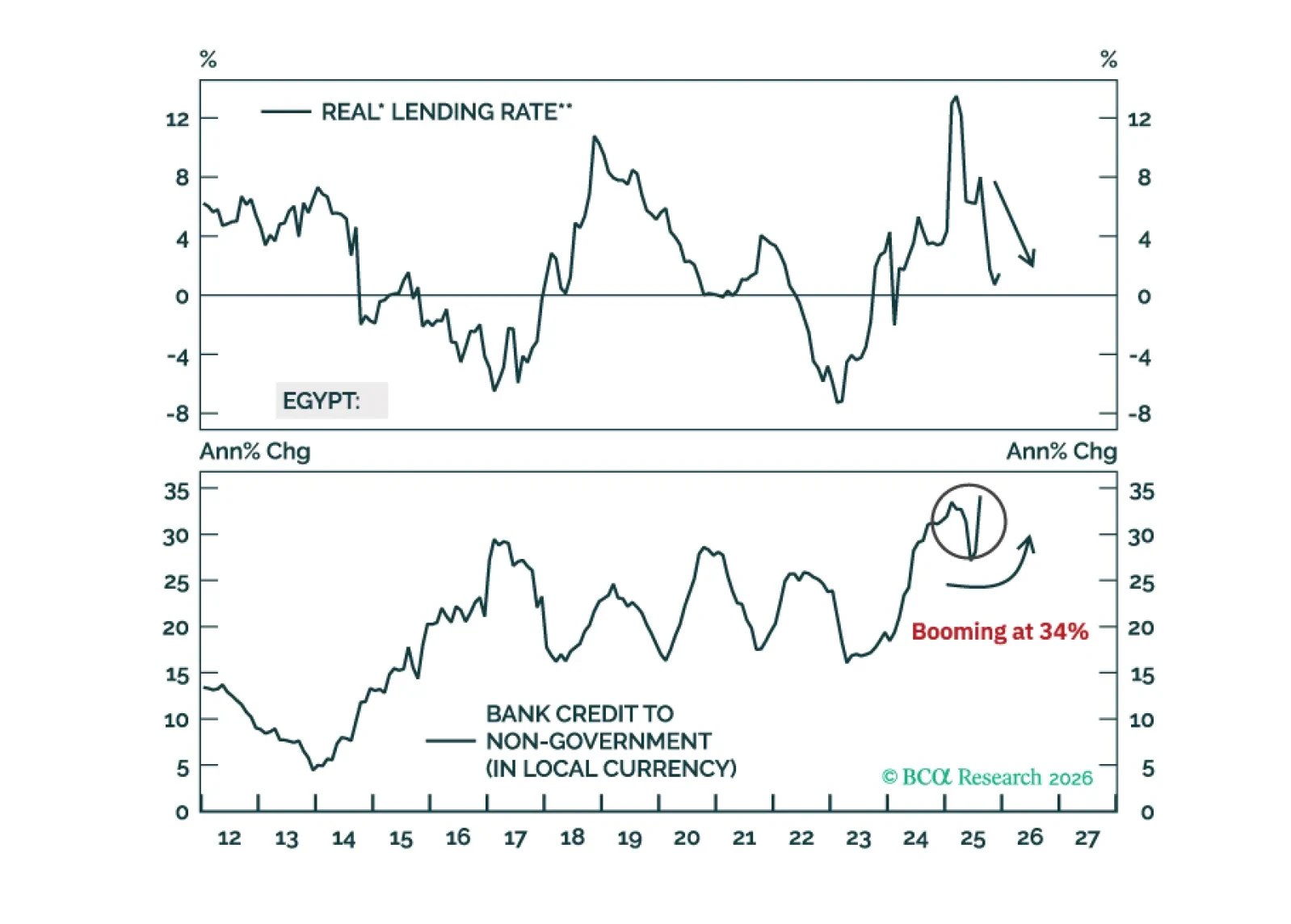

Egypt’s underlying inflation pressures are much higher than the headline CPI numbers imply. Real interest rates have plunged. As such, domestic bond yields have stayed high for a reason. Steer clear.

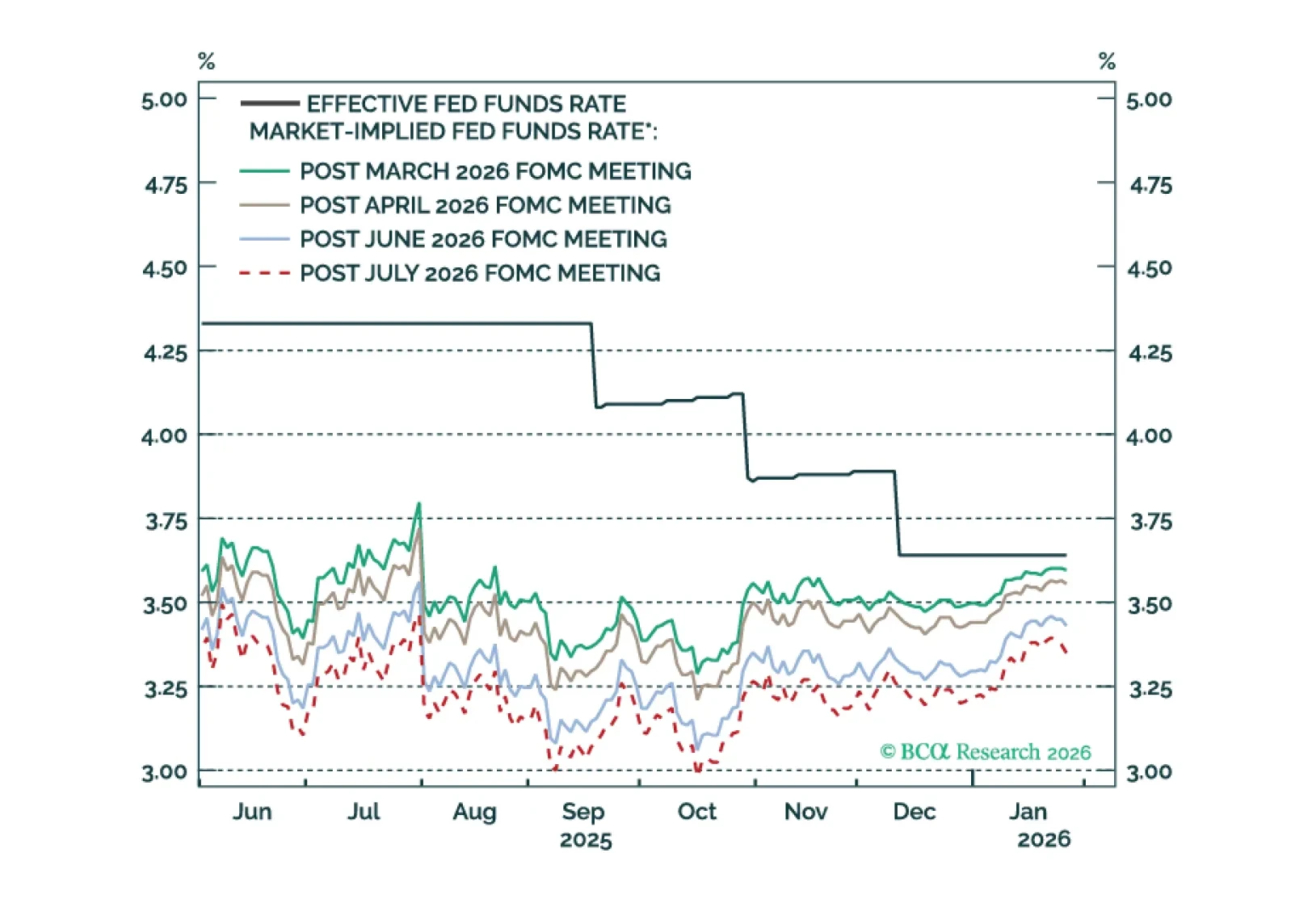

The Fed will keep rates on hold in H1 2026, but dovish policy surprises are likely in the second half of the year.

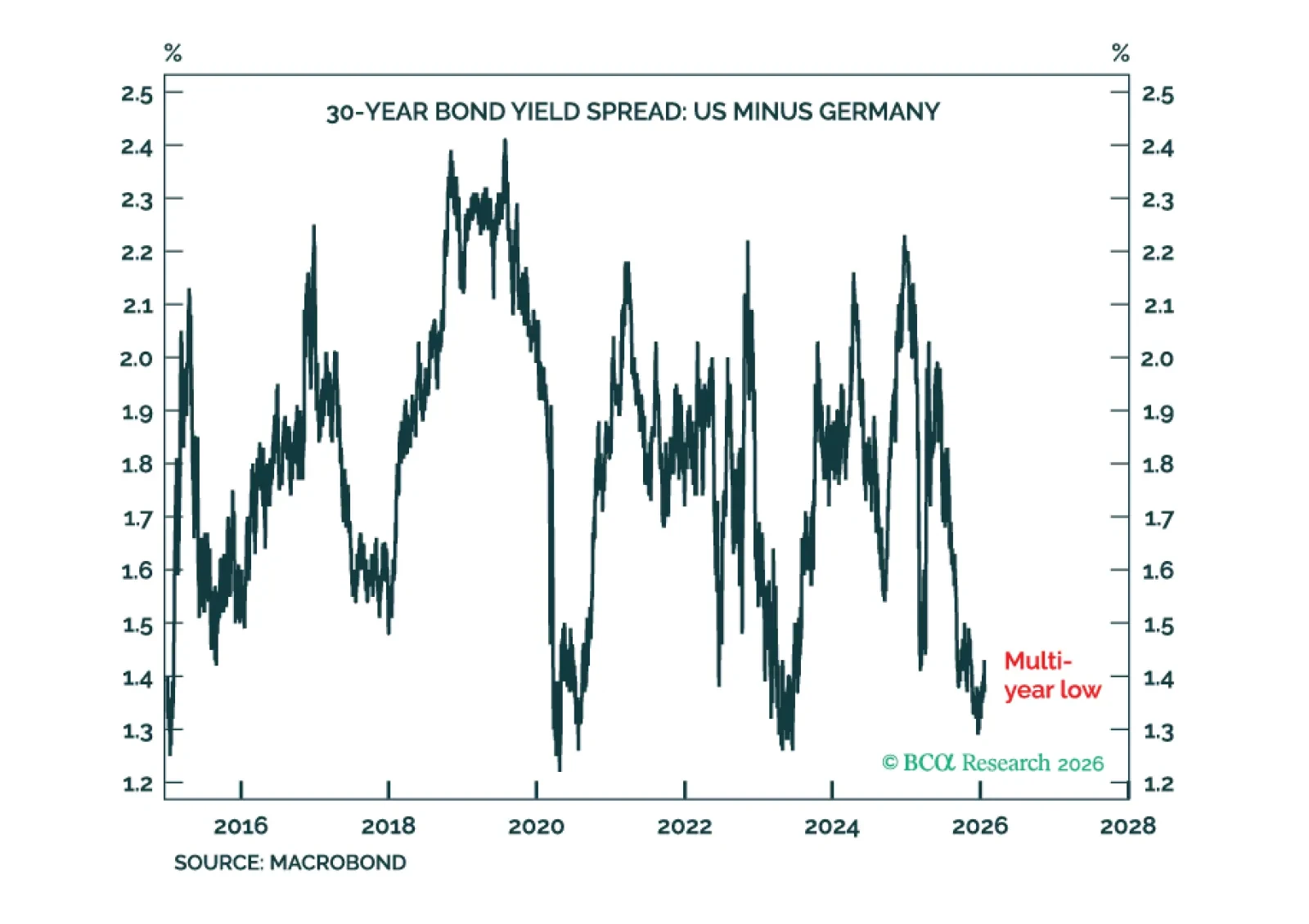

US Treasury yields require a higher premium for both geopolitical risk and inflation risk, but higher bond yields are not necessarily bad for stocks.

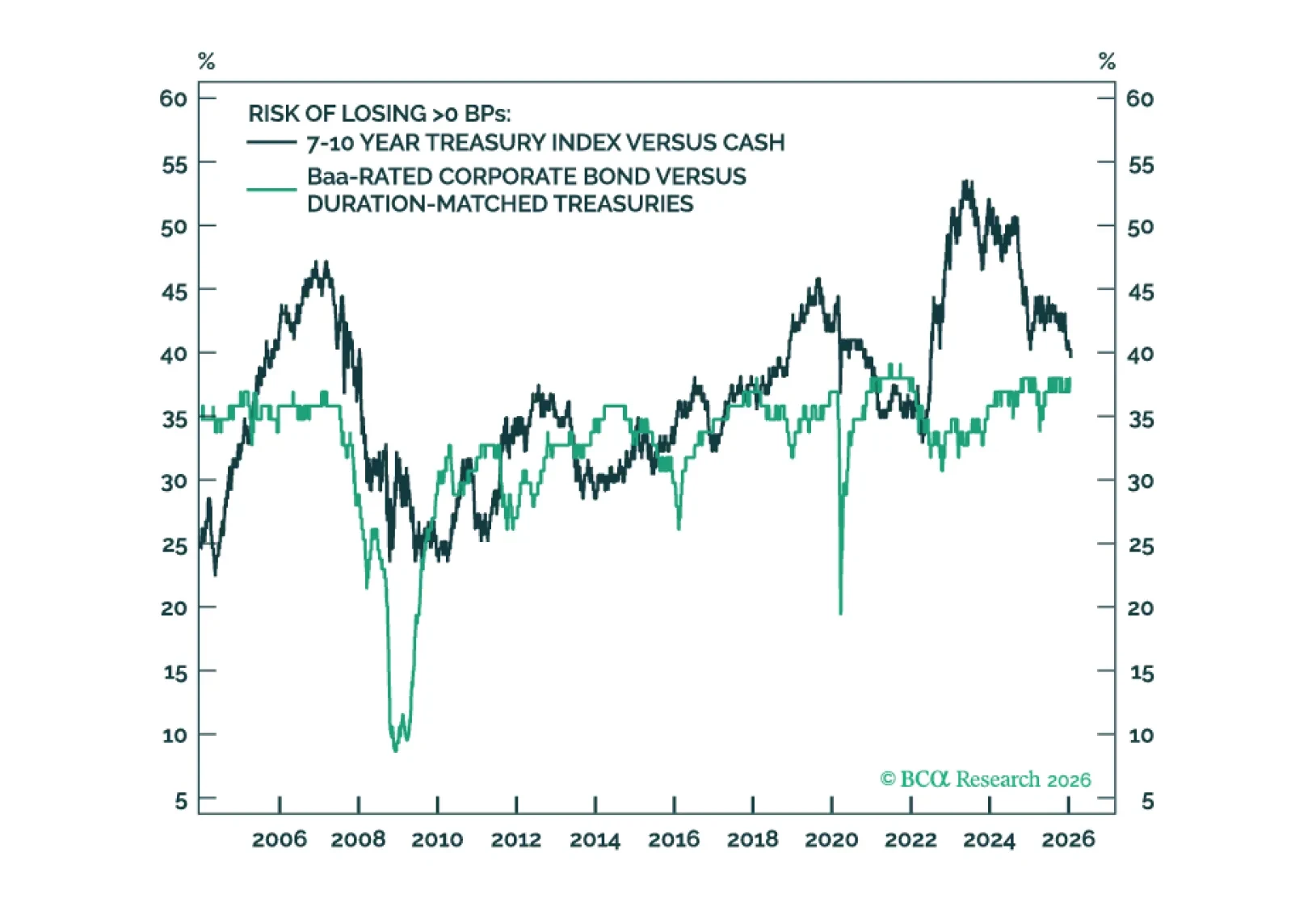

The 10-year Treasury term premium is now competitive with Baa- and Ba-rated credit spreads. Even without term premium compression, duration carry trades could outperform credit carry trades in a low rate vol environment.

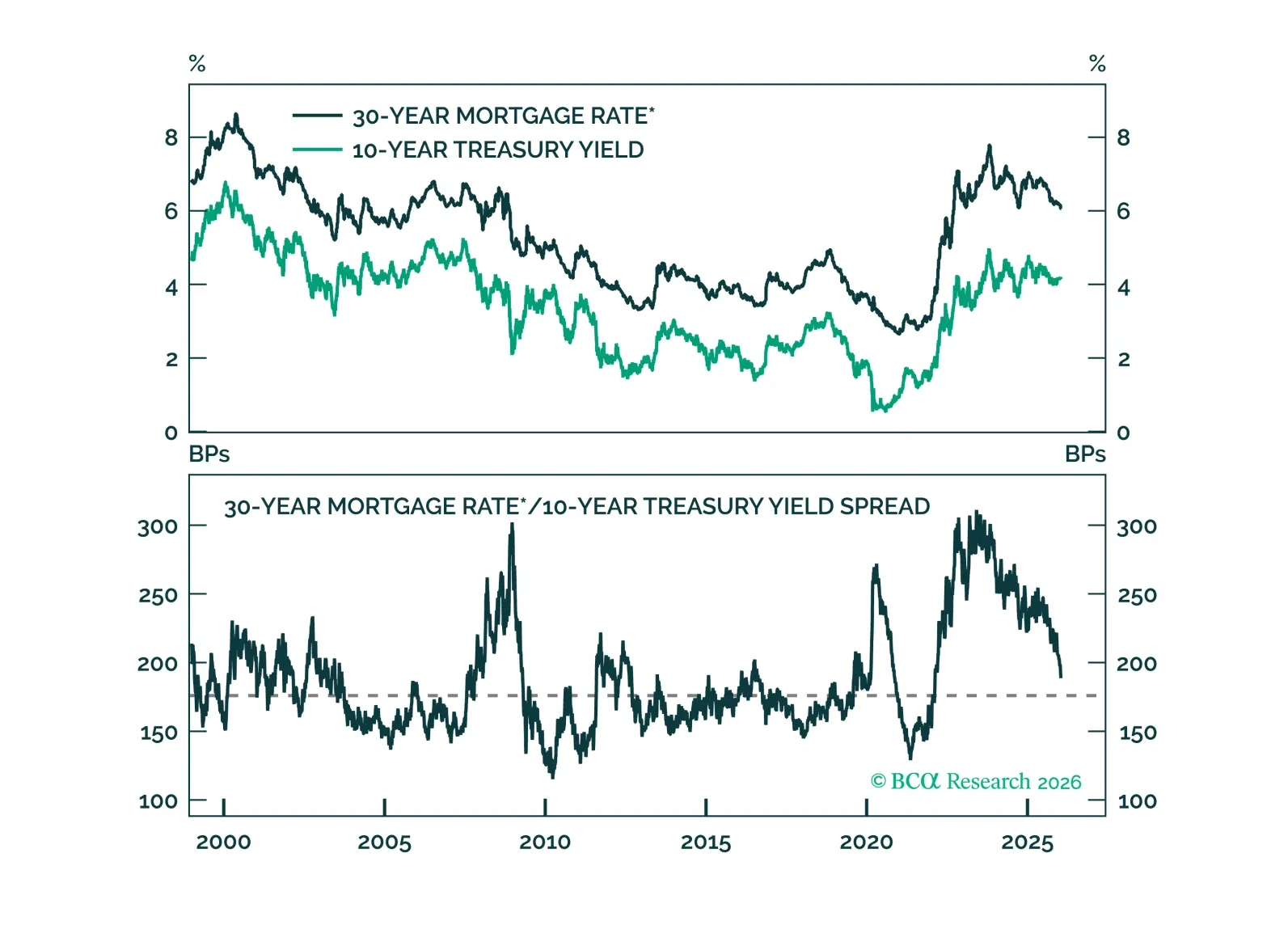

Mortgage spread tightening has run its course. Any further drop in mortgage rates will necessitate lower Treasury yields.