Fixed Income

The market backdrop changed a lot between the preparation and the publication of our equity downgrade report. We publish this companion Insight to help investors navigate the new environment.

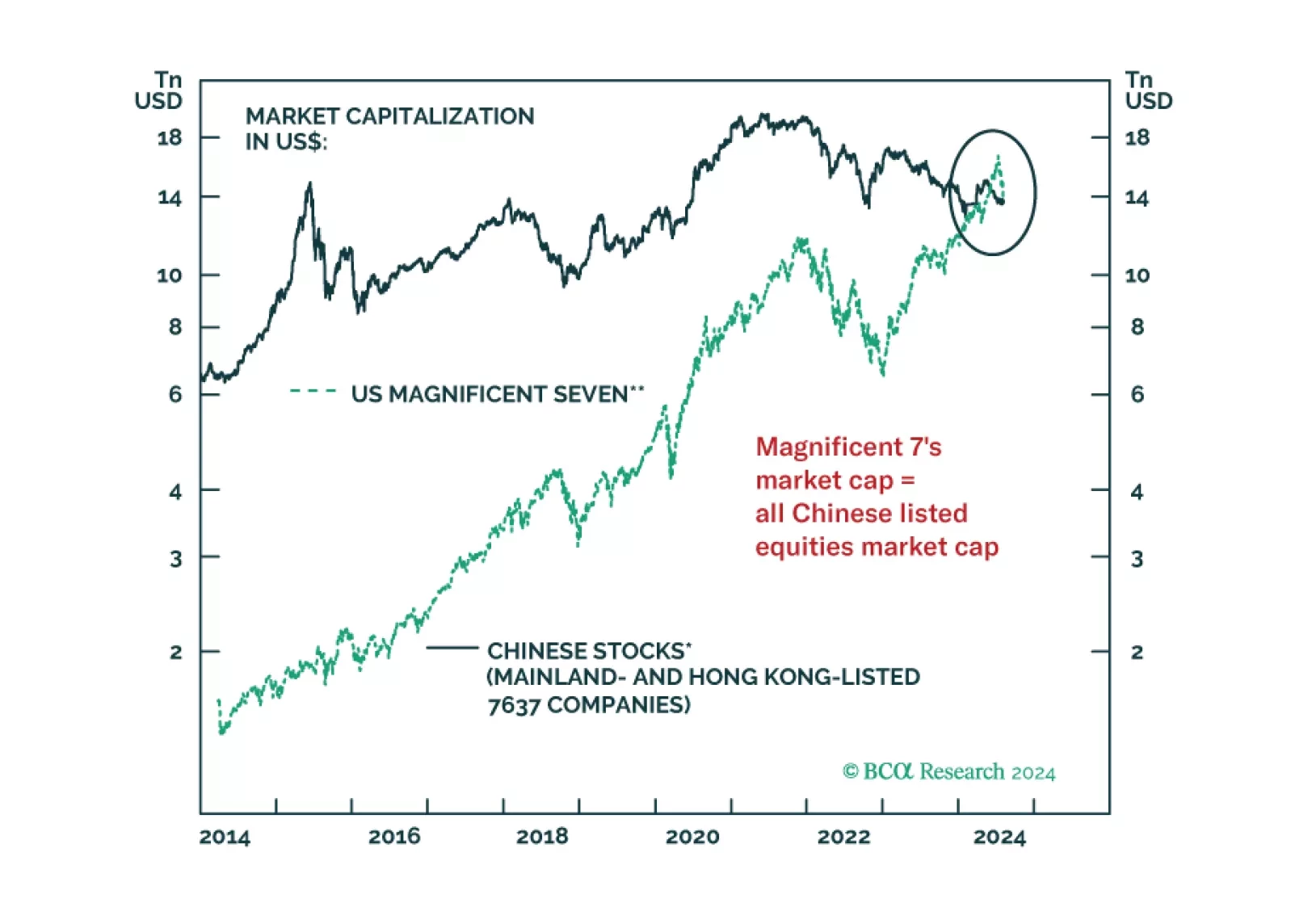

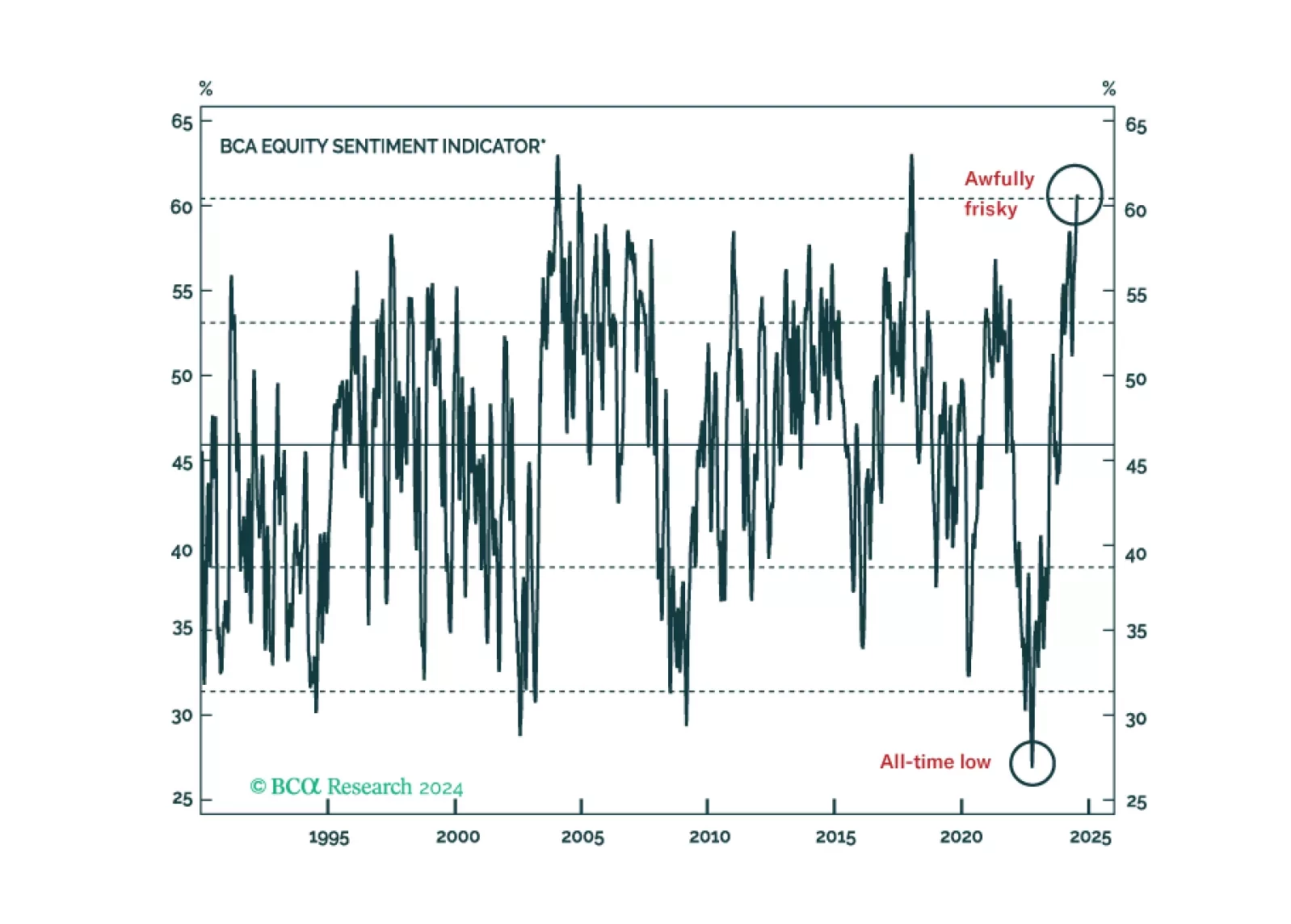

The prices of multiple financial assets have failed to break above their technical resistances. When this occurs, a breakdown ensues. In brief, global risk assets remain vulnerable. We are upgrading Chinese onshore stocks from neutral to overweight and offshore ones from underweight to neutral within EM and global equity portfolios.

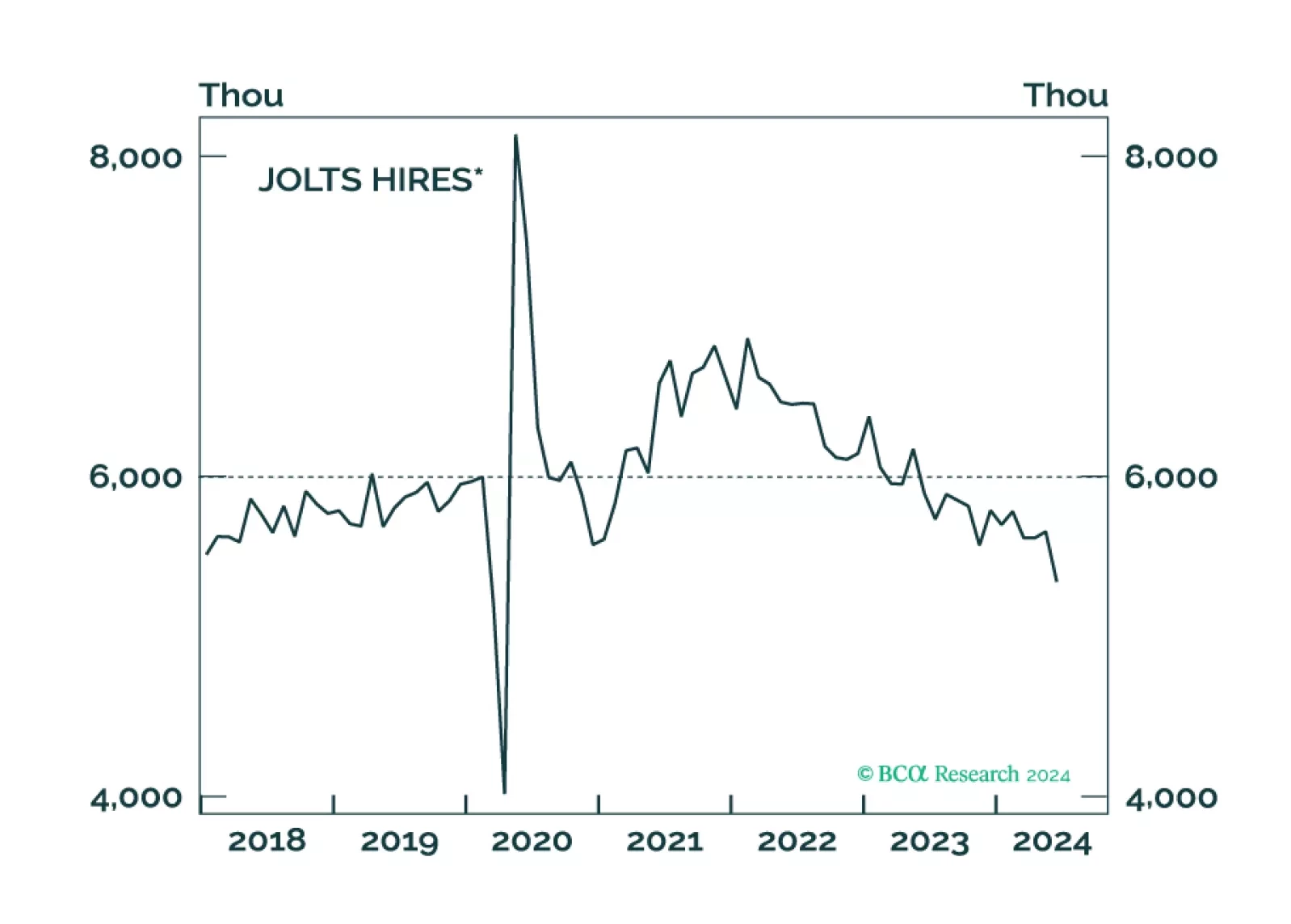

Mounting evidence that the labor market is on its way to cracking checked two more boxes on our checklist, driving us to tactically downgrade equities to underweight while upgrading fixed income to overweight. Our tactical and cyclical (6-12 months) views are now aligned as our conviction that a recession will begin before year-end has increased.