Fixed Income

Preliminary estimates suggest that activity continued to slow across DM economies in September. Manufacturing PMIs contracted at a faster pace in the US, Eurozone, Germany, France and Australia, and grew at a slower pace in the UK. Services PMIs continued…

The PBoC lowered the 14-day reverse repo rate by 10 bps on Monday, a move that follows a string of easing measures in late July when the central bank lowered the 7-day reverse repo rate, several maturities of the loan prime rate and the 1-year medium-term…

The European Central Bank (ECB) cut rates by 25 bps in September. It did not signal consecutive rate cuts and we highlighted that the short inter-meeting timeframe between September and October provides little scope for ongoing data releases to move the…

According to BCA Research’s European Investment Strategy, the low rate of innovation in Europe is a major problem for the economy. Not only does it prevent Europe from standing at the technological frontier, but it also contributes to the low rate of…

The Bank of Japan’s policy normalization has been accompanied by exceptional outperformance by Japanese banks. Japanese banks have outperformed both the country’s broader market as well as the MSCI ACW Banks index by 10.3% and 2.6%, respectively, so far this…

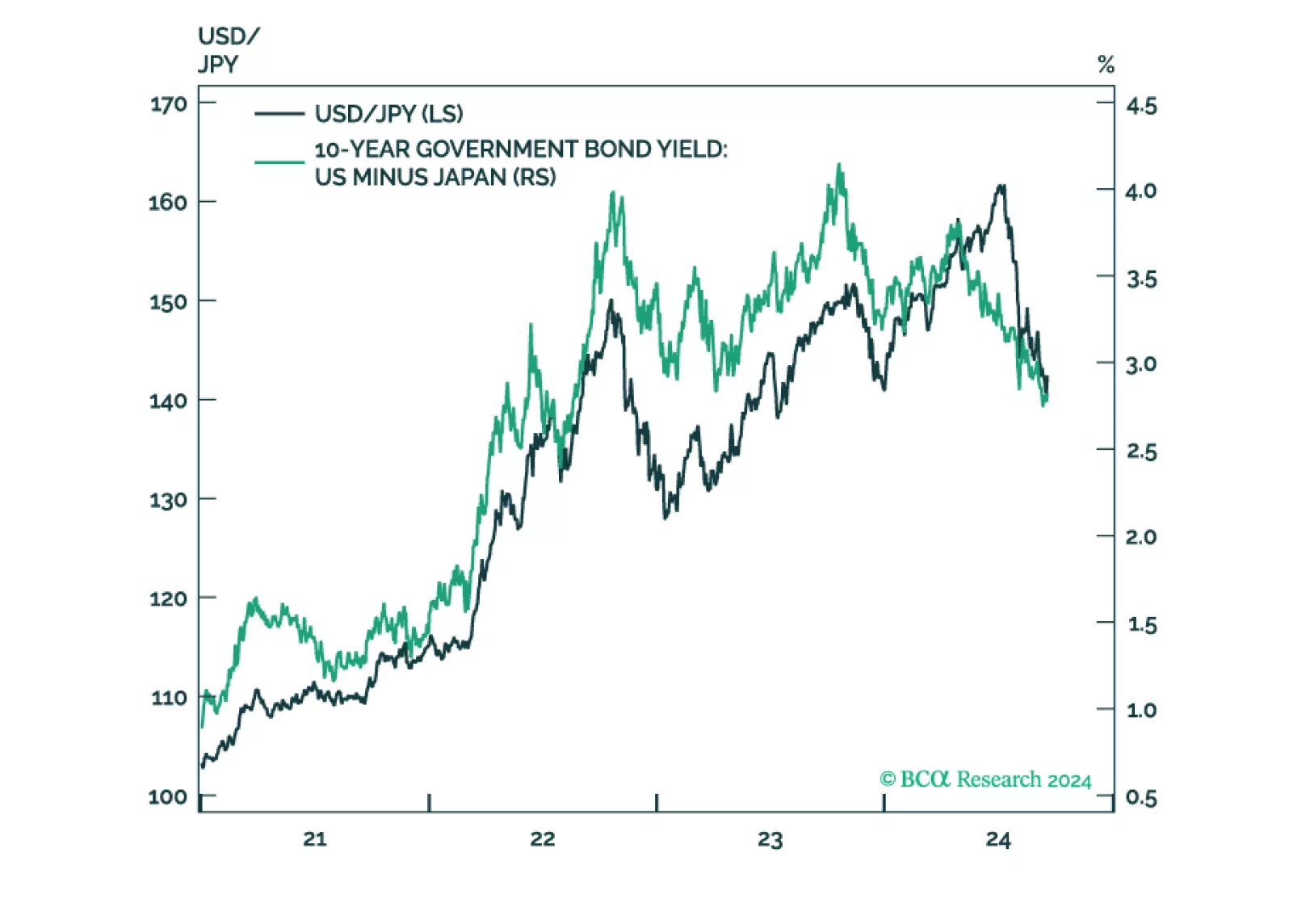

According to BCA Research’s Foreign Exchange Strategy and Global Investment Strategy services, most carry investors have covered their positions. Away from day-to-day noise, the longer-term trajectory of yen exchange rates will be driven by fundamentals. …

In this report, we argue that the Bank of Japan is unlikely to hike interest rates this week, but the relative trajectory of bond yields in Japan is higher. This warrants an underweight position in JGBs and a leveraged bet on a higher yen. The positioning for equity investors is murkier, as progress on corporate reforms is necessary for a rerating in Japanese shares. That is not yet very clear. The bottom line is: Stay long the yen.

UK headline CPI grew at a stable 2.2% y/y in August, though the core measure accelerated from 3.3% to 3.6%, in line with expectations. An 11.6% annual increase in airfare largely drove core CPI higher, while offsetting contributions from food and alcohol led…

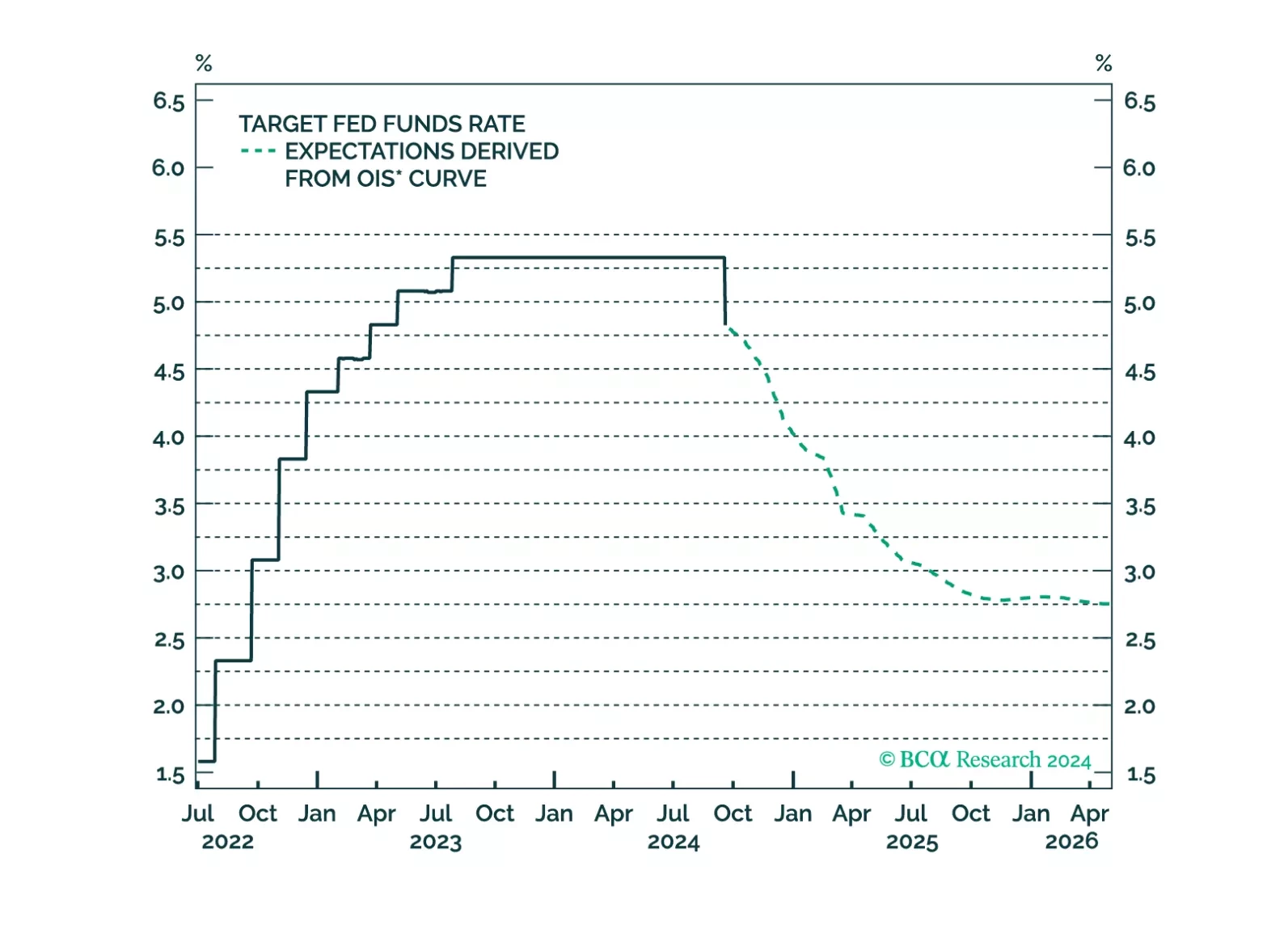

The Fed started its easing cycle with a bang, cutting the policy rate by 50 basis points in September, above consensus expectations but in line with odds embedded in the futures and OIS curves. Our US Bond strategists had highlighted it is unusual for the…