Fixed Income

A falling stock market and sticky bond yields represent the worst of both worlds for investors. We interrogate why bond yields haven’t dropped more given the large selloff seen in equities.

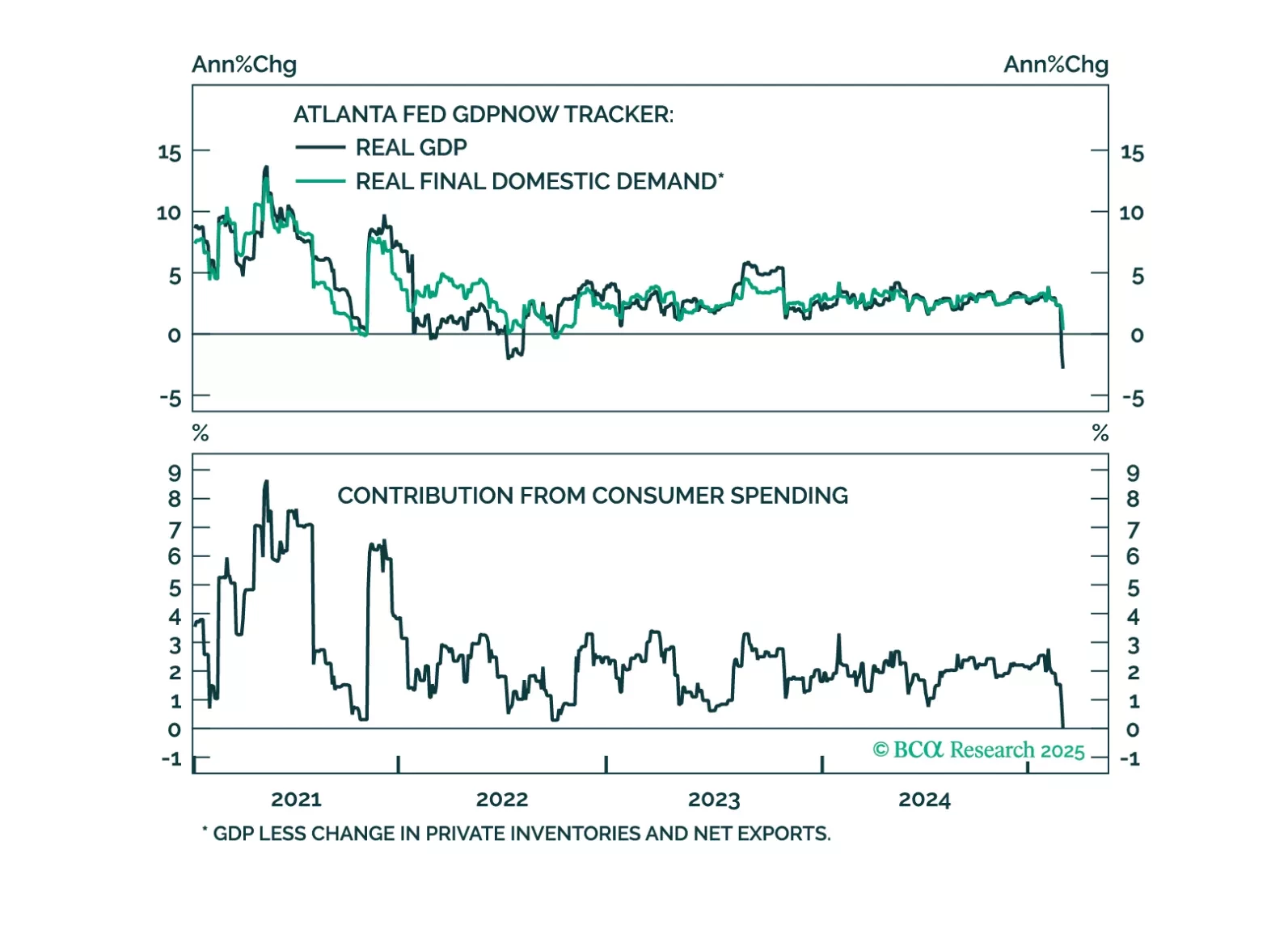

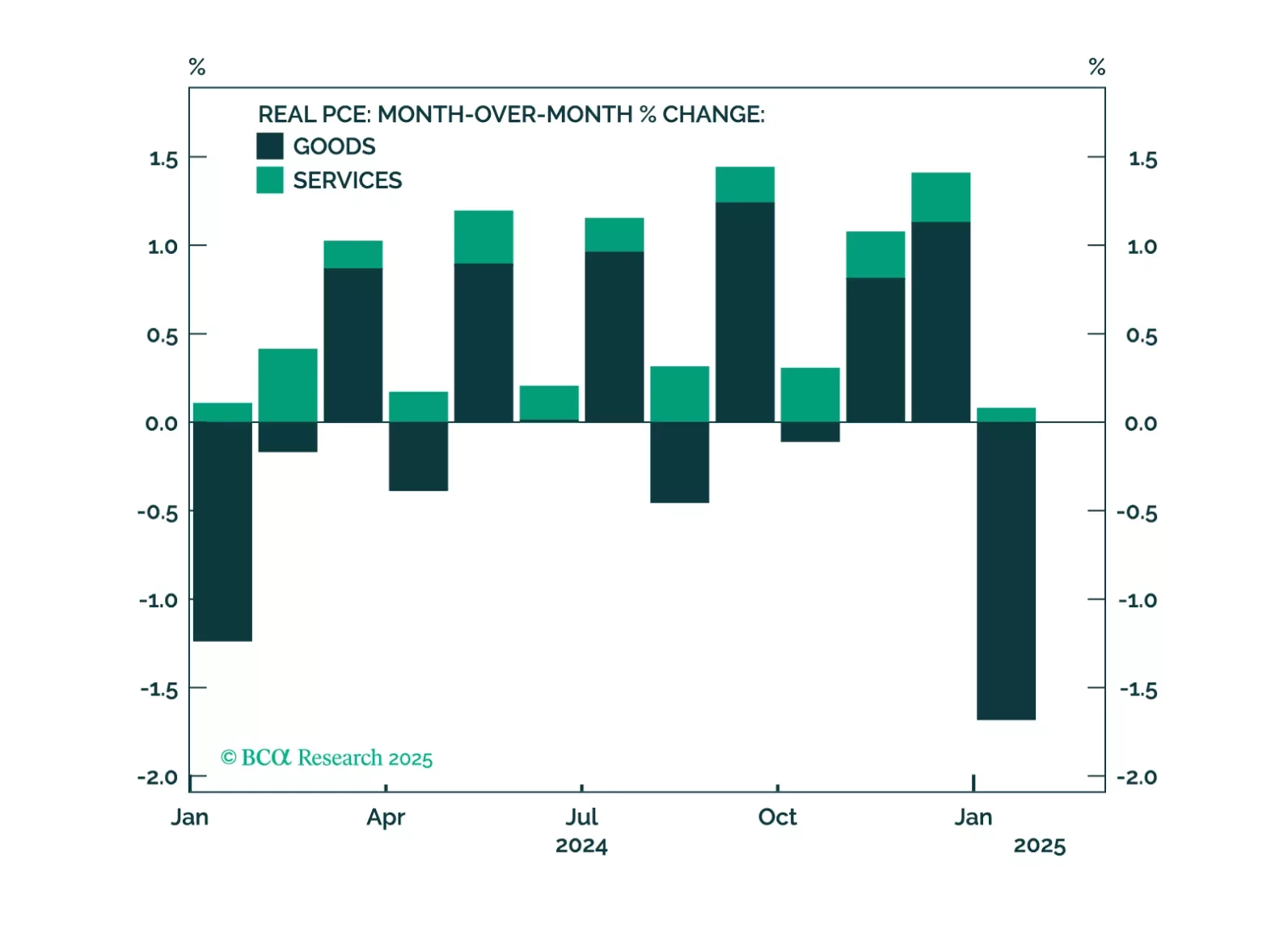

This morning’s employment report showed solid job growth, but recent consumer spending indicators are more concerning. The risk of recession starting within the next few months has increased. We suggest some important indicators for investors to track in the current environment.

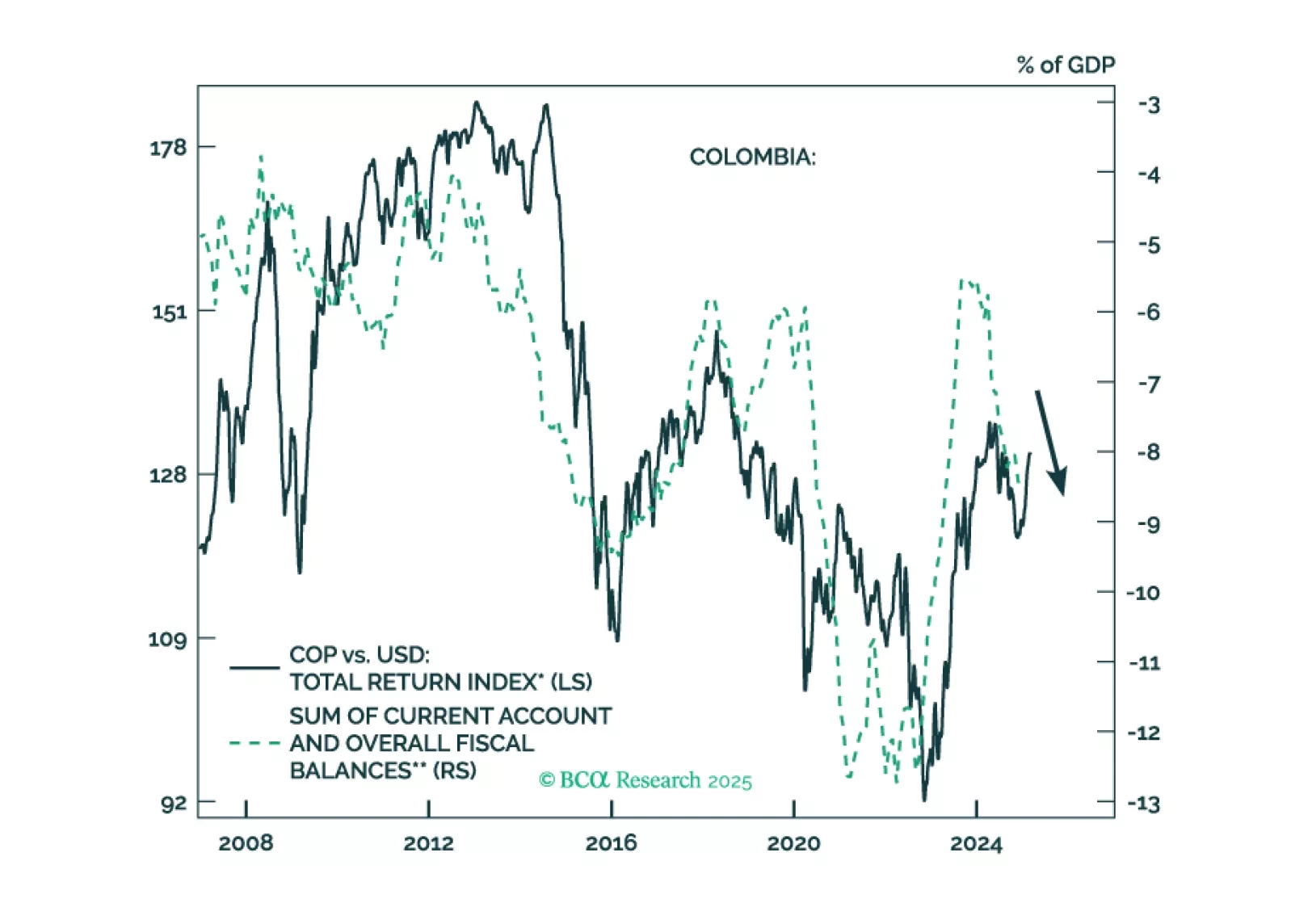

Colombian financial markets have rallied on the expectation that a right-wing government will be elected in 2026. We take a contrarian bearish stance on the nation's financial markets. Colombia is suffering from two structural macro issues – unsustainable public debt and plunging energy exports – that will not be easily solved by a conservative administration in 2026. Continue underweighting Colombia within EM equity and fixed-income portfolios, continue shorting the COP versus the USD and the CLP, and bet on yield curve steepening.

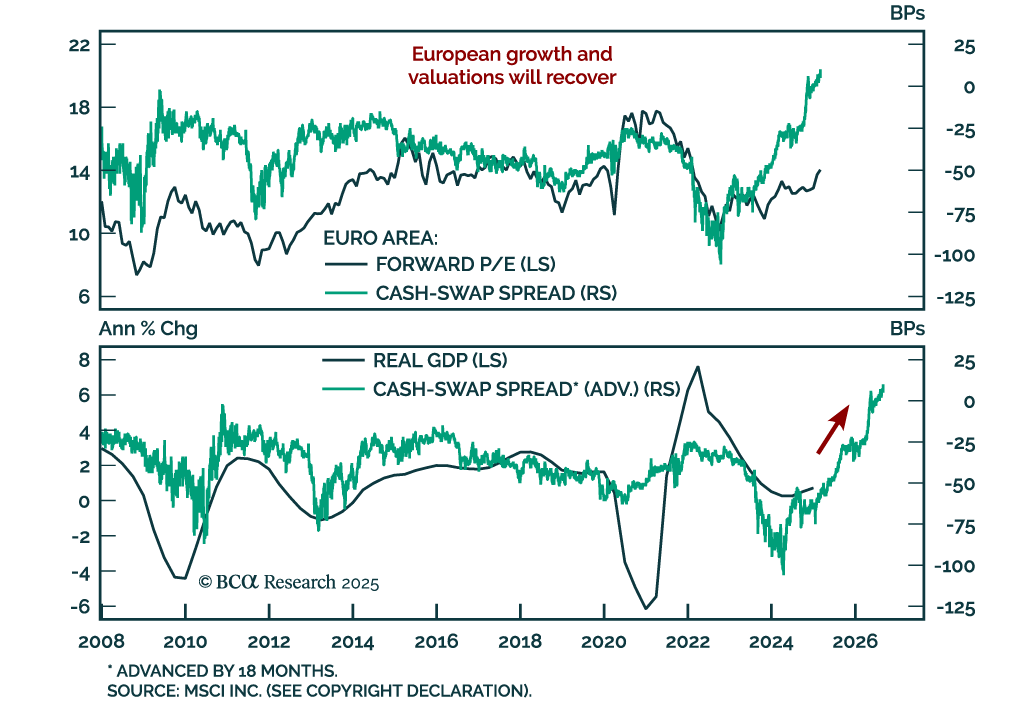

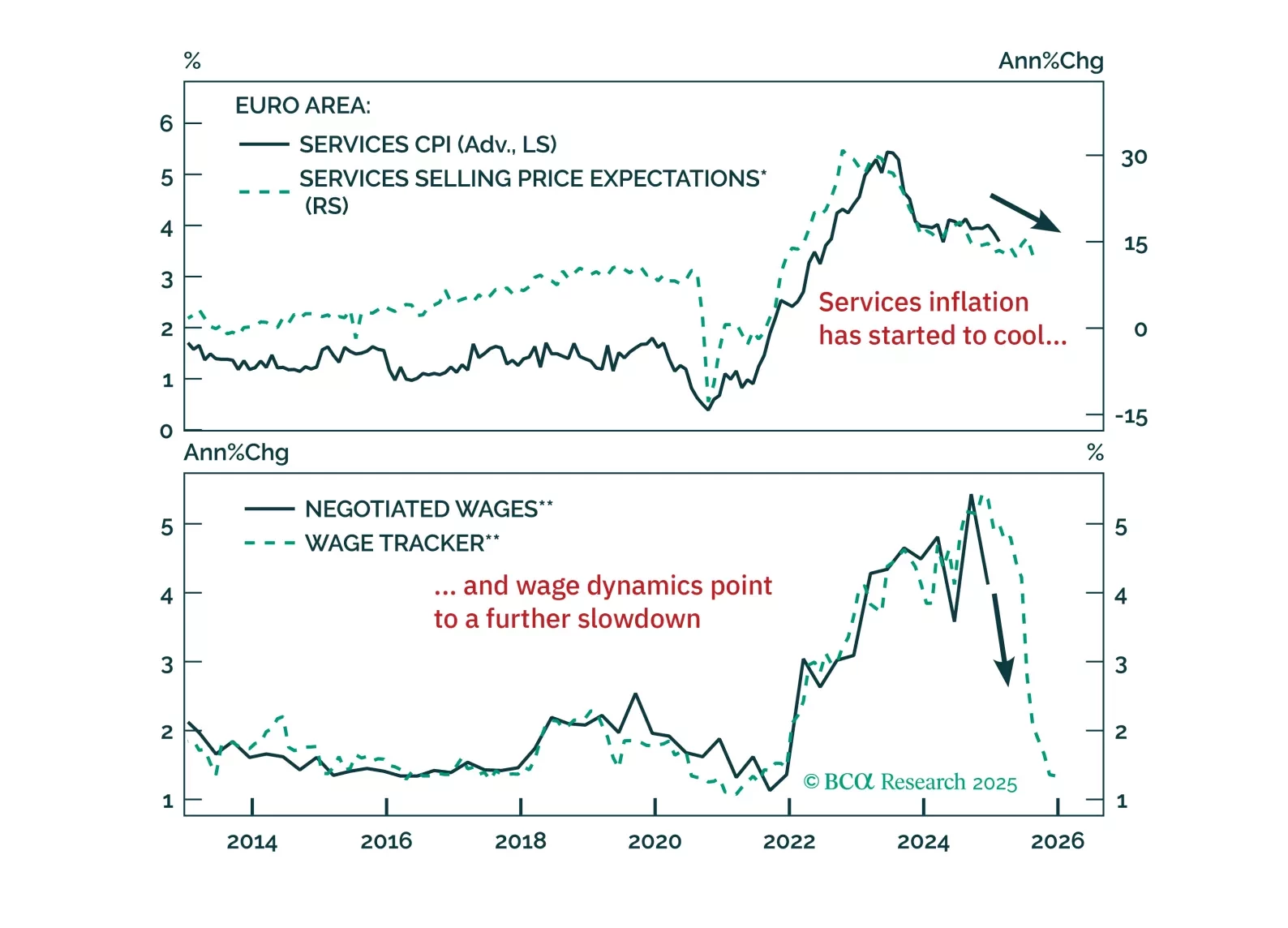

The ECB cut rates as expected, but rising yields and a stronger euro are tightening financial conditions just as fiscal policy shifts the macro landscape. With more rate cuts ahead and market positioning stretched, we outline the key risks, investment opportunities, and our updated call on the ECB’s terminal rate. Read our full report for actionable insights.