Fixed Income

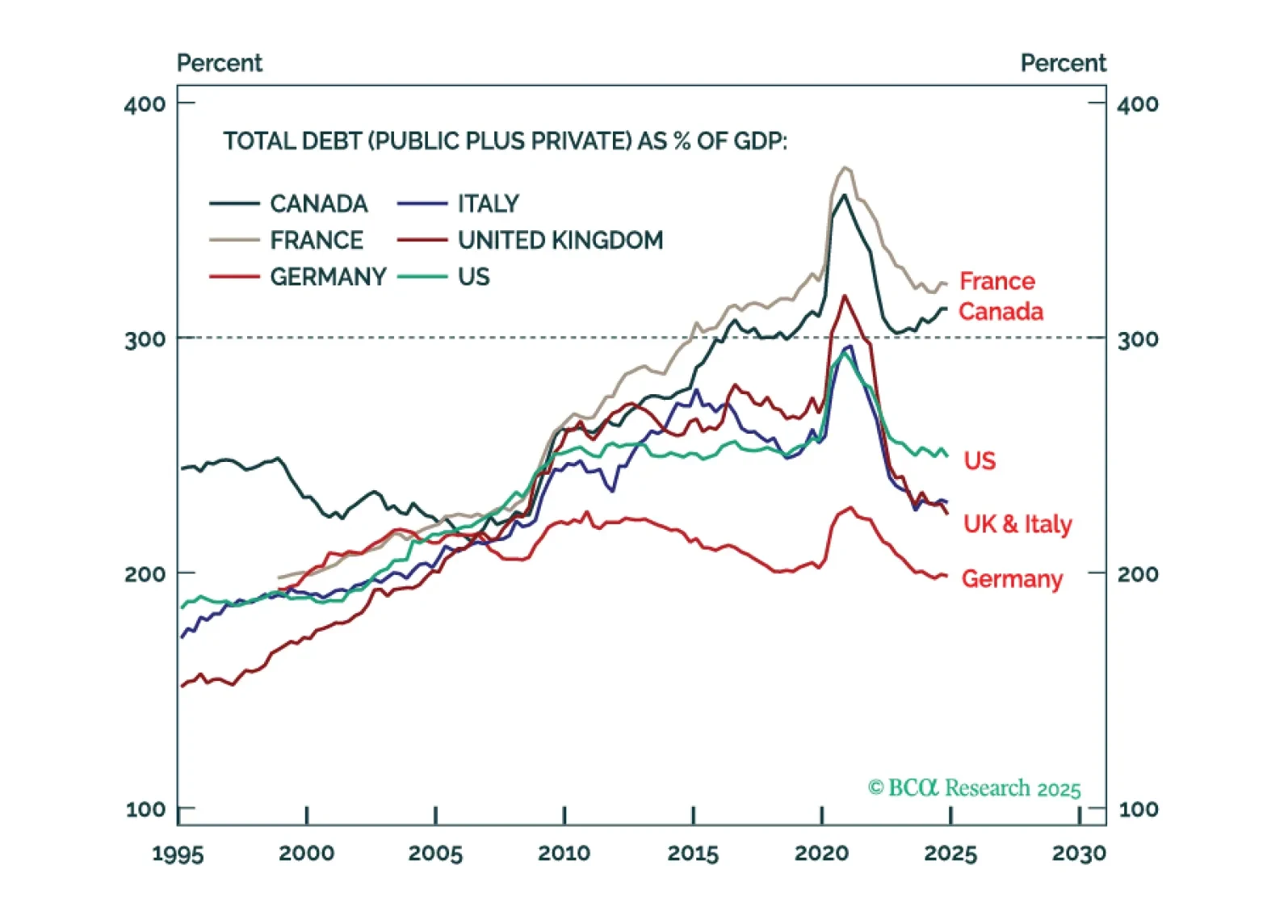

The bond vigilantes are circling over several targets right now: France, the UK, and Japan. But France is the most vulnerable because of a toxic combination: a total debt ratio well above 300 percent plus the worst primary deficit in the G7 plus political gridlock, which will get even worse if Prime Minister Francois Bayrou loses the September 8th vote of confidence in his minority government. We explain why the ECB cannot save France, and the investment implications. Plus, we unveil our brand-new complexity ‘heat map’ for global asset allocation which leads to a new tactical trade to underweight world communication services (WTEL).

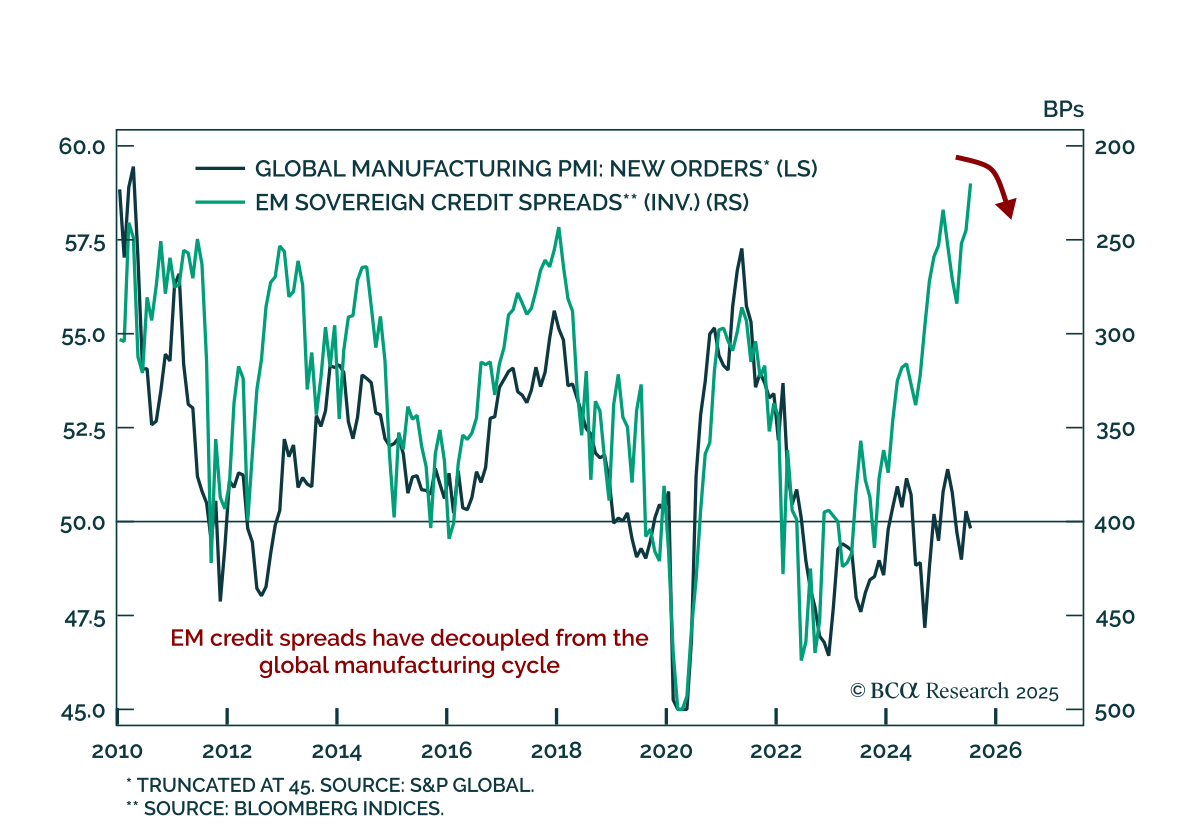

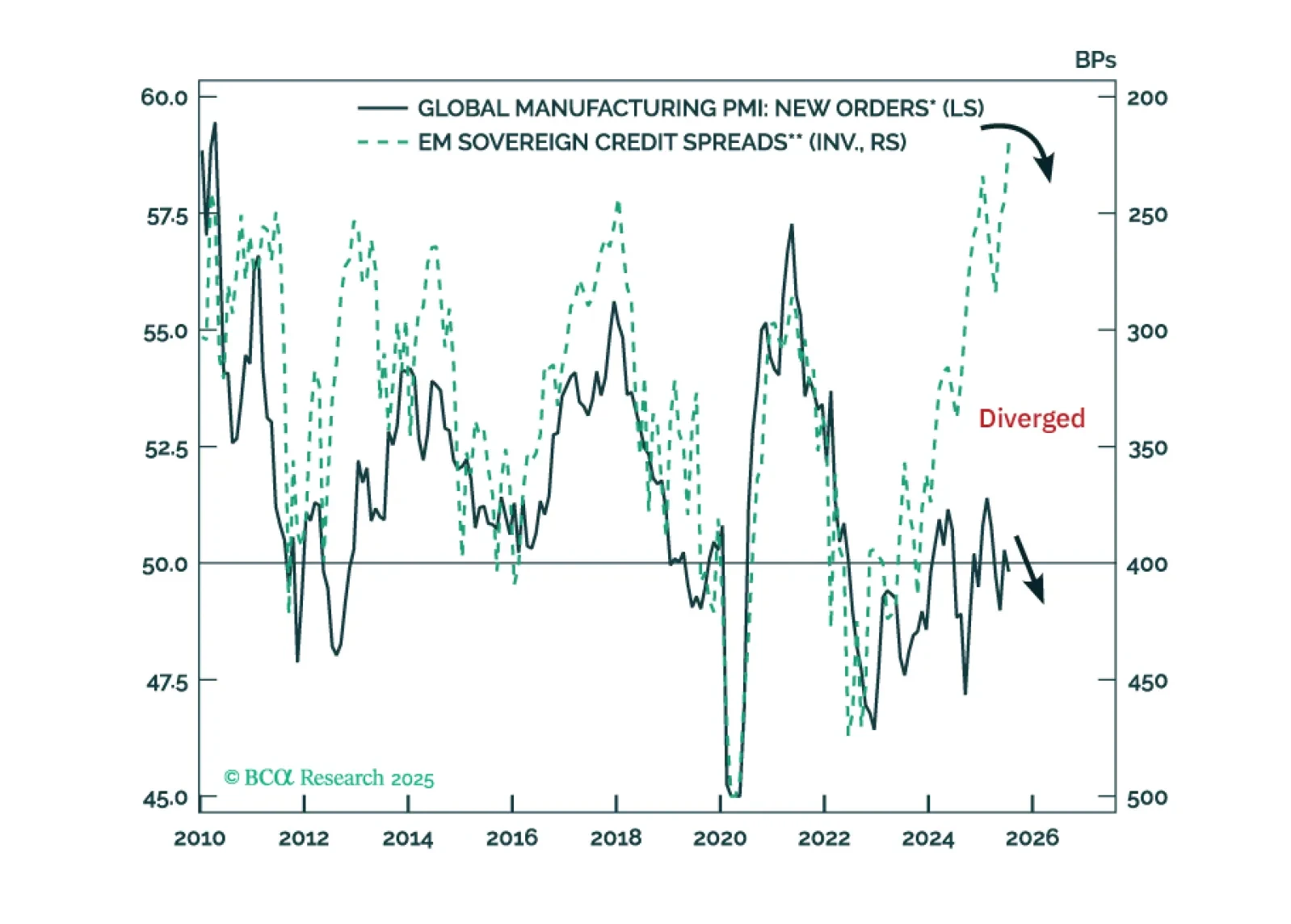

EM sovereign and corporate credit spreads are set to widen. Within a global credit portfolio, maintain a neutral allocation to EM credit markets versus US corporate credit. Favor EM local currency bonds over EM USD bonds.

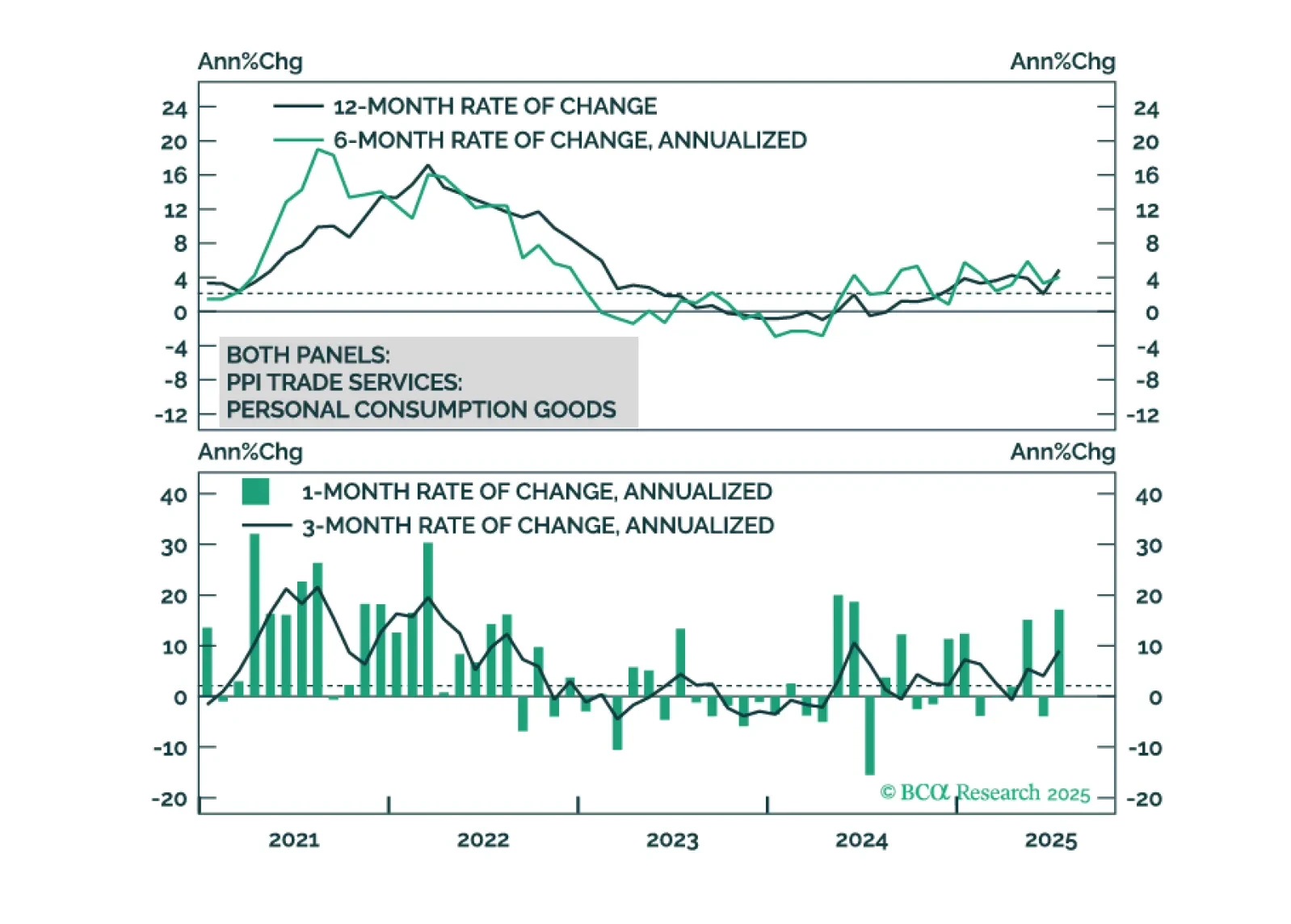

The cost of tariffs is falling on the US consumer, not foreign exporters or US firms.

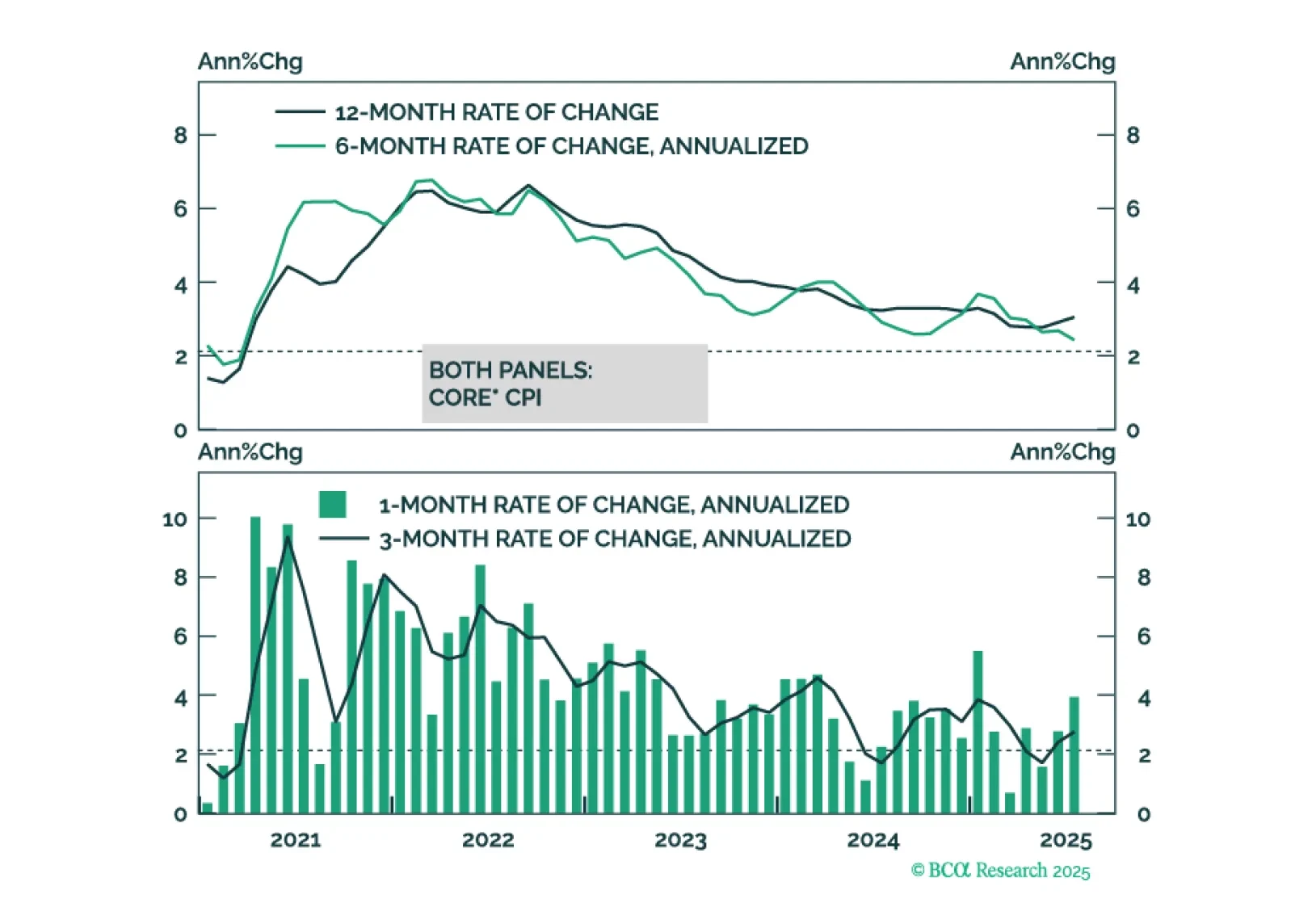

This morning’s CPI report marginally tips the scales in favor of a September rate cut.