Fixed Income

Most Fed and pundit assessments of inflation expectations are overly narrow, focusing too much on long-term market-based measures. We favor a more qualitative approach that asks whether the inflation outlook is influencing household and business decision making.

Goldilocks, with fault lines underneath. Our first joint FICC outlook lays out where growth, inflation, and policy are headed this quarter and where the calm could crack.

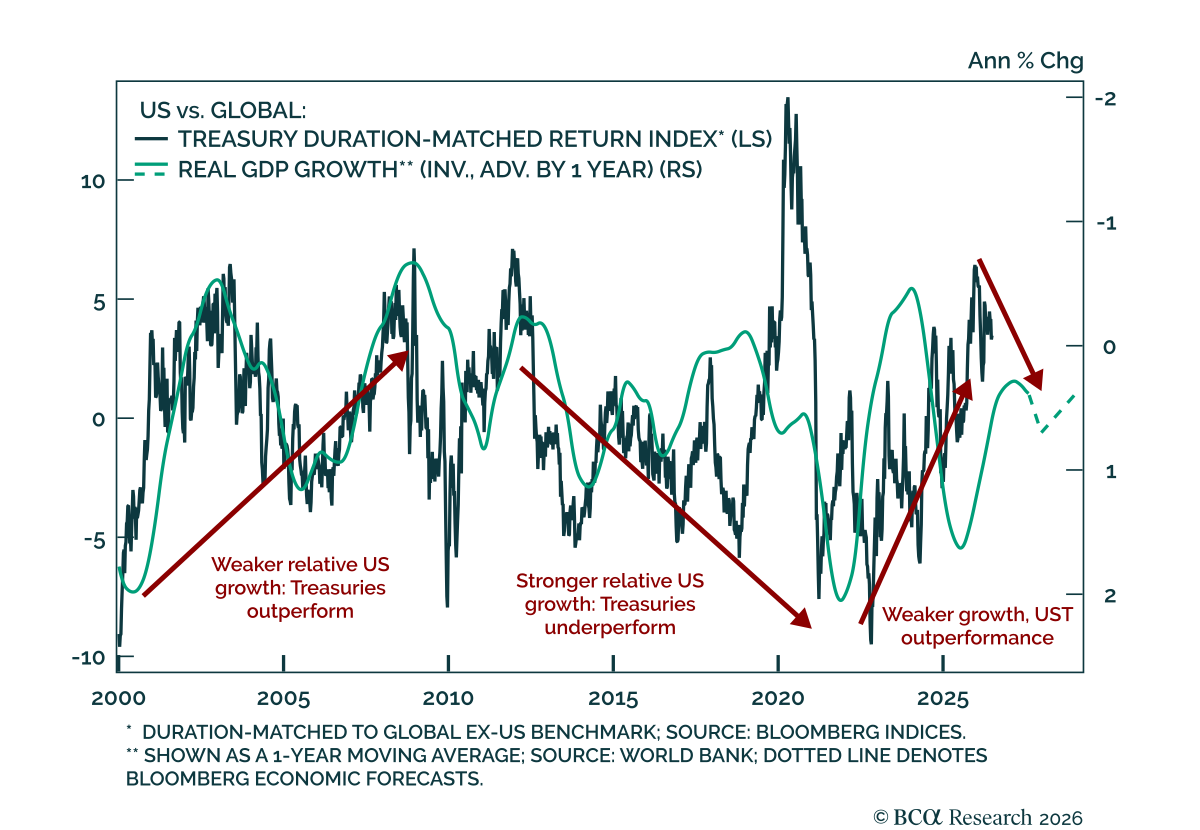

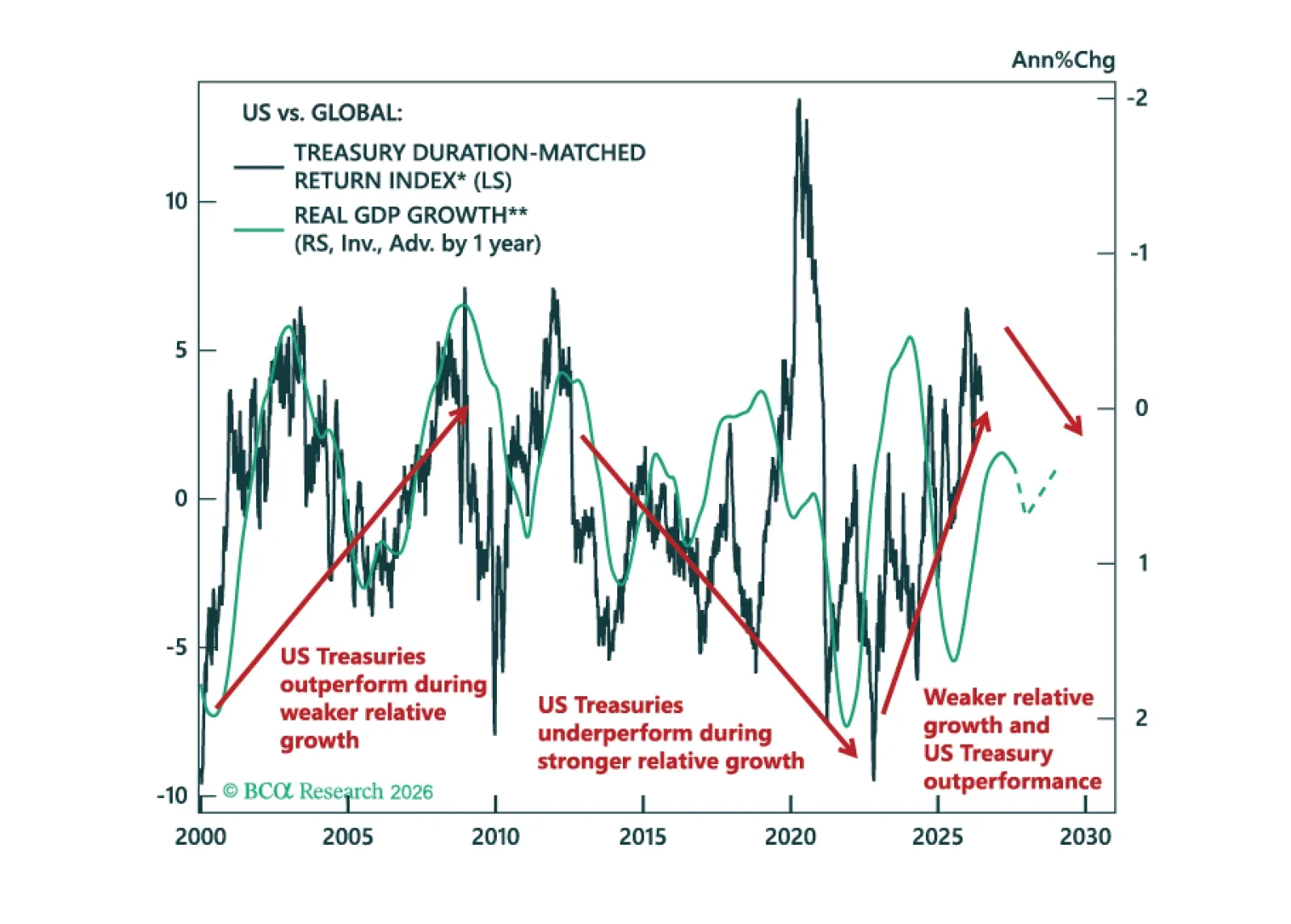

We review our Model Bond Portfolio performance for Q2 and look ahead as fixed income markets move beyond the US-Iran conflict, which is finding its kinetic equilibrium. Valuations and growth differentials are moving against continued US Treasury outperformance.

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

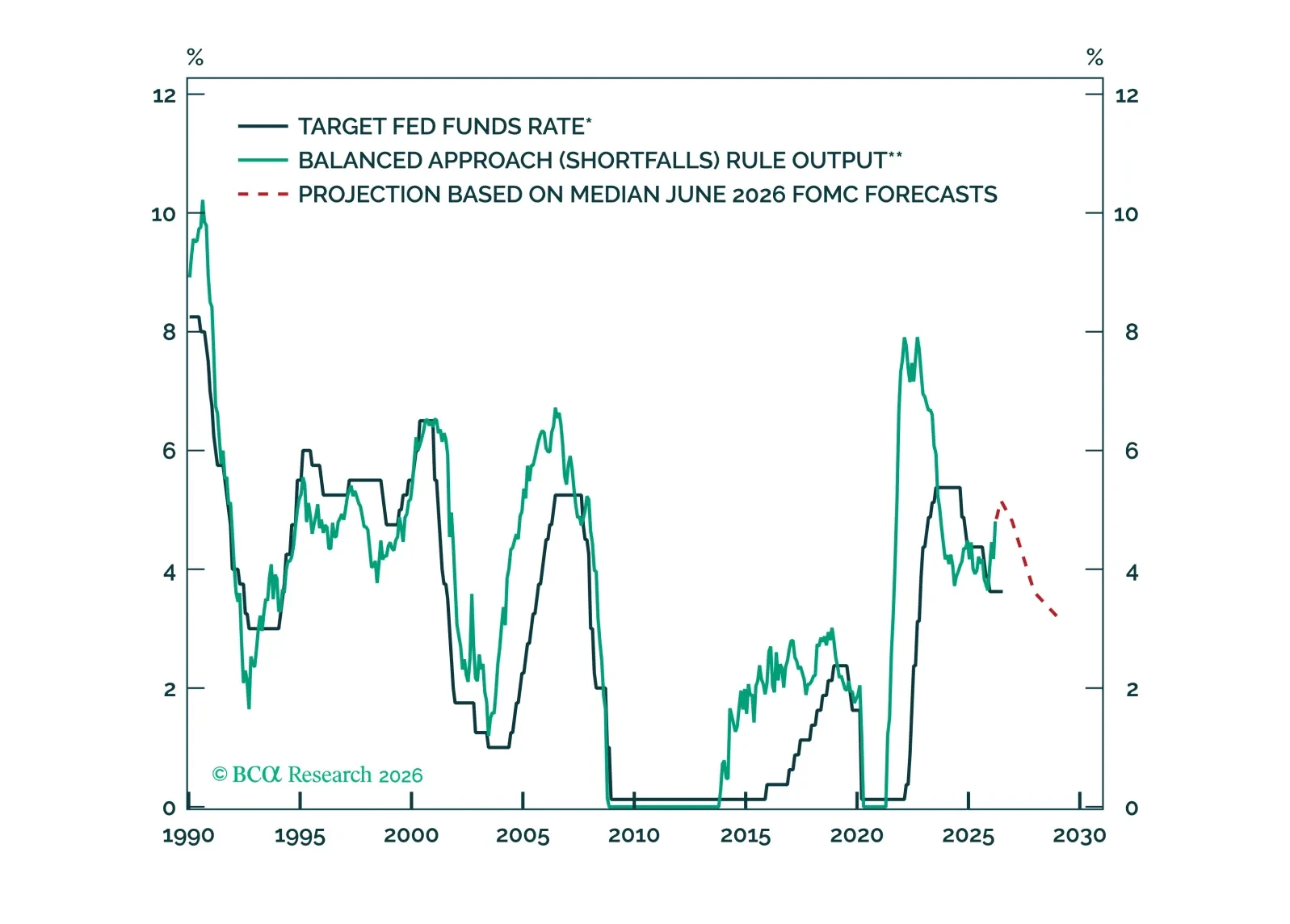

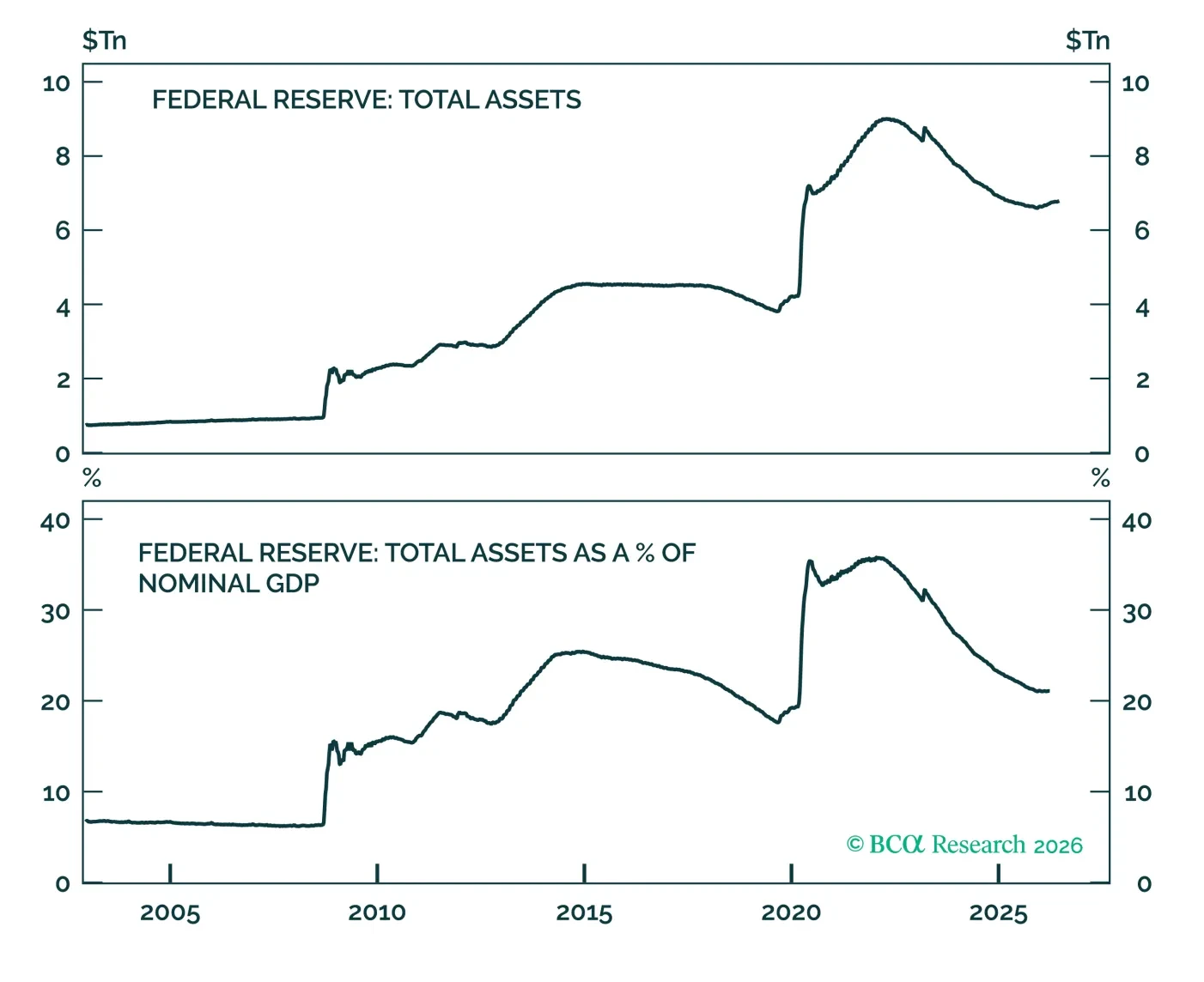

We discuss what recommendations to expect from the Fed’s balance sheet task force. We conclude that any future balance sheet consolidation will be smaller than many anticipate.