Fiscal

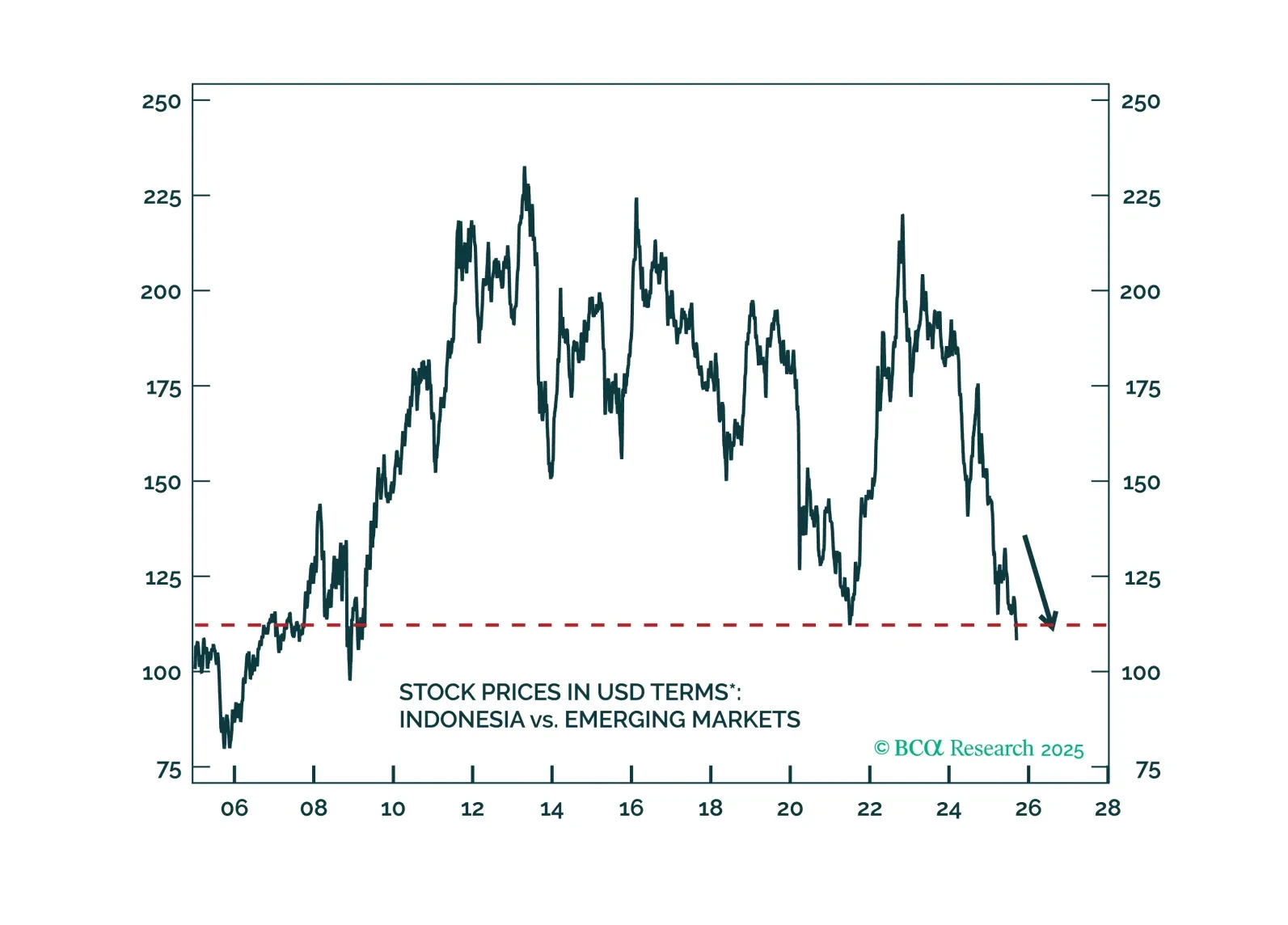

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.

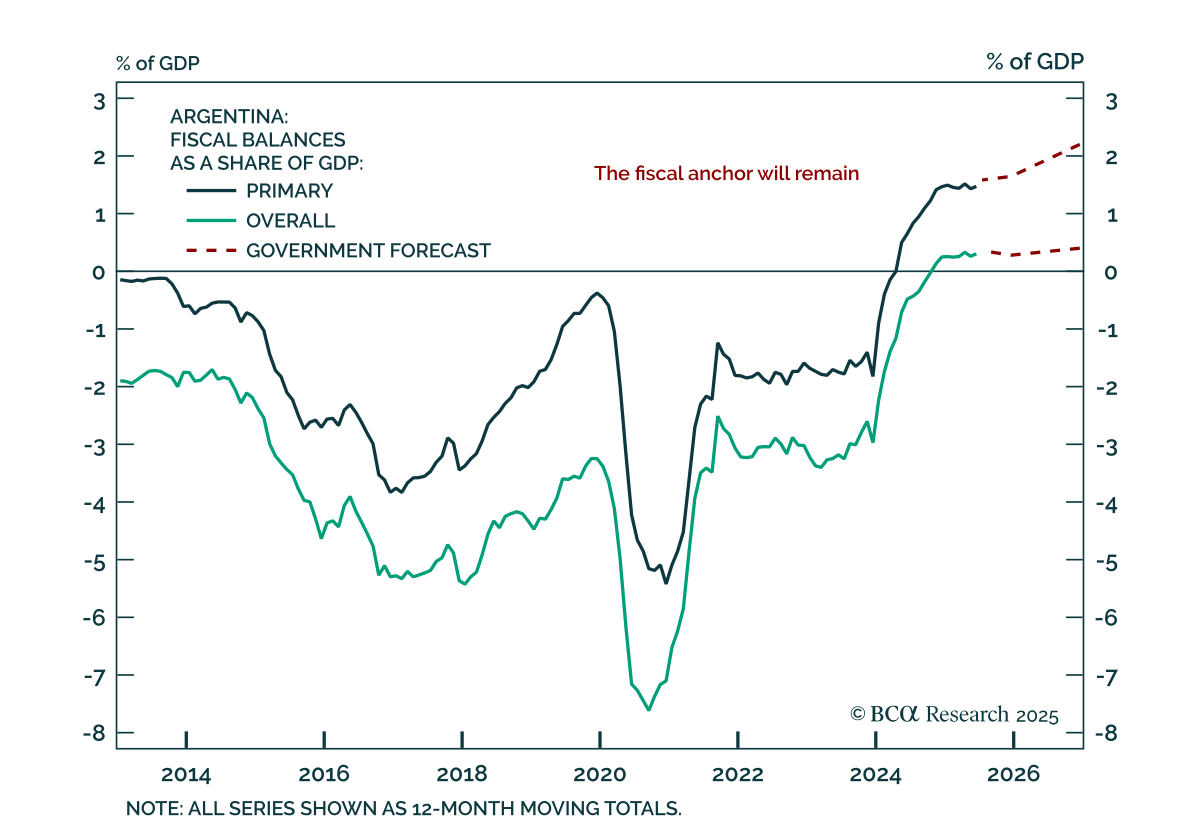

Despite the post-election selloff, investors should continue buying Argentine assets on weakness. Argentine markets sold off sharply after President Milei’s party suffered a crushing defeat in Sunday’s Buenos Aires election. Investors did not expect the…

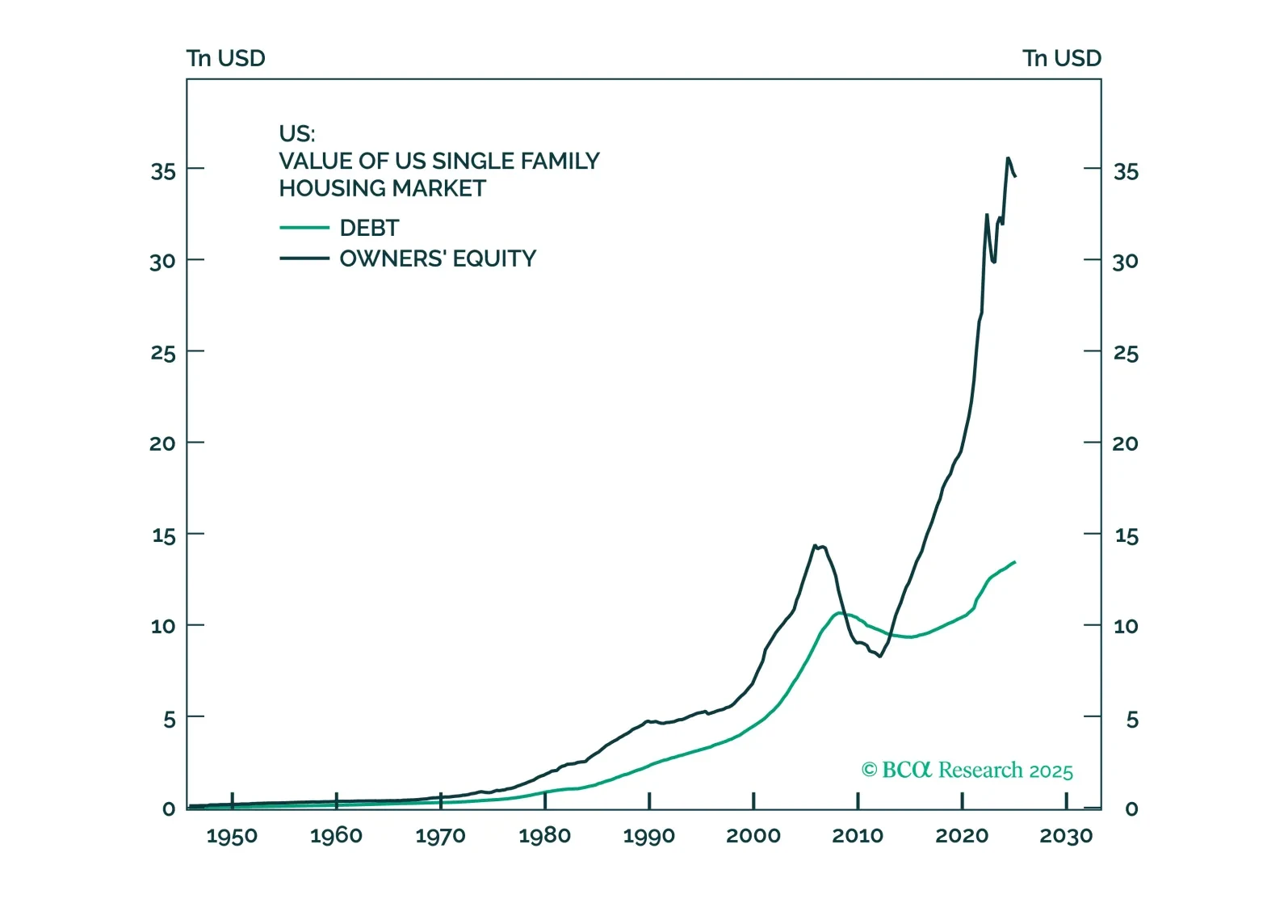

In the Alpha report, we maintain our bullishness on the equity market. We are optimistic that the cash-fueled cycle will evolve into a leverage-driven one, with the AI capex cycle acting as the "bridge" between the two. Our view is easily falsifiable. If the 10-year yield starts moving against us, we will pull the plug on the cycle. One reason to fret is that tariff revenue has now become critical to the equity bull market. Without it, bonds could riot.

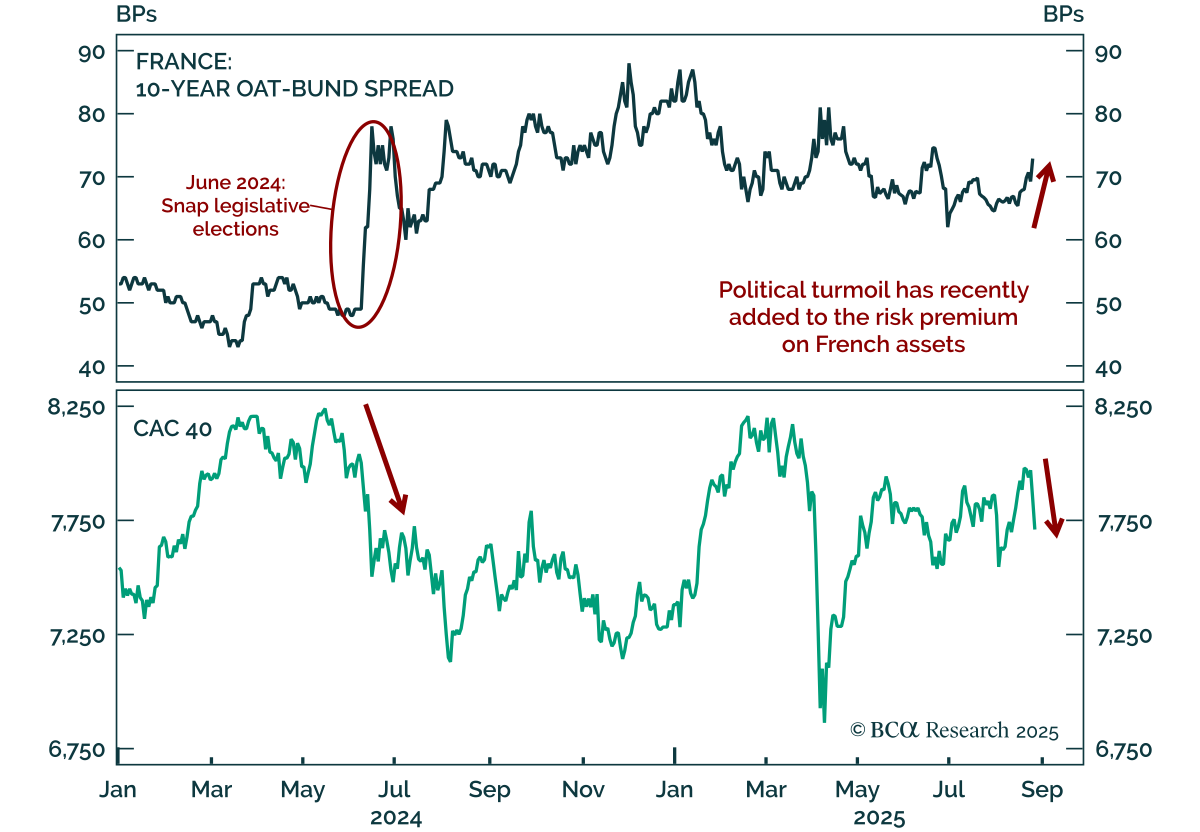

France’s renewed political turmoil highlights fiscal risks for OATs, but creates opportunities to buy French equities on dips. PM Bayrou has called a September 8 confidence vote over his deficit-cutting budget proposals, triggering a selloff in the…

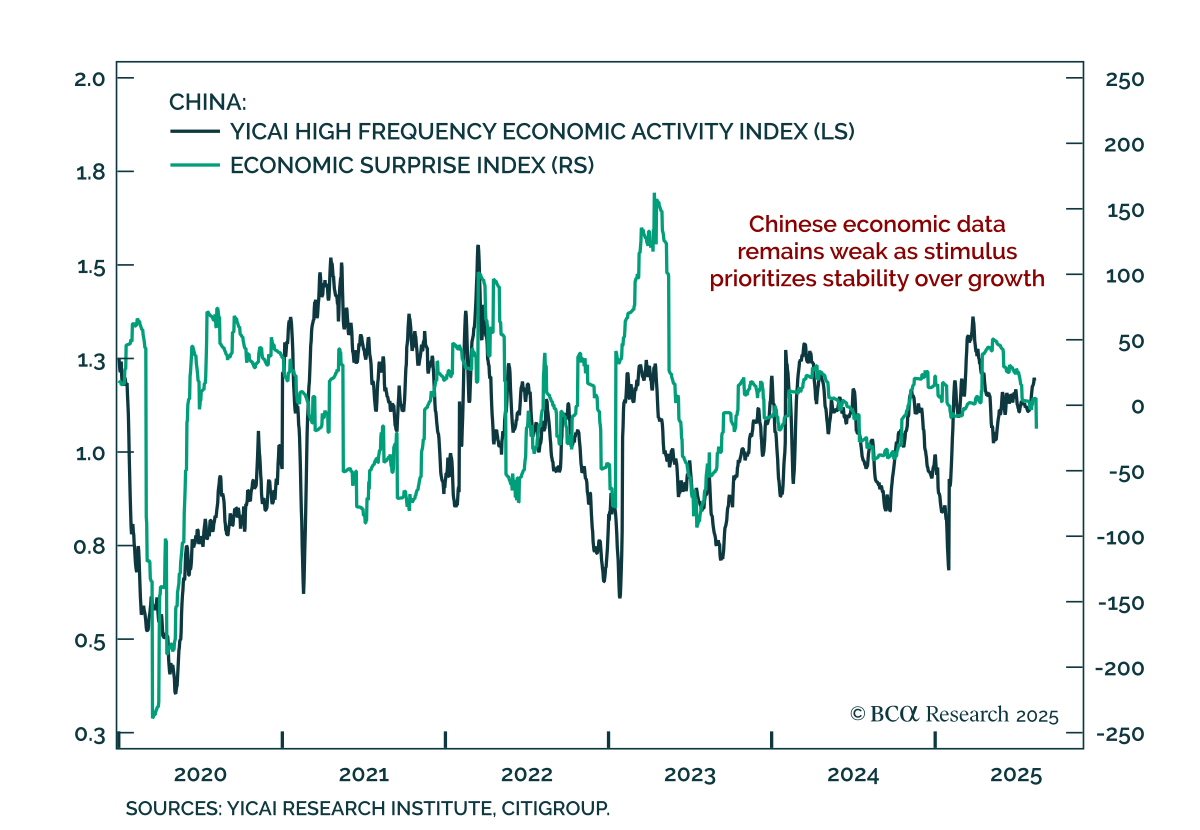

July data confirm China’s weak growth, with no near-term shift toward meaningful stimulus. New home prices fell 0.31% m/m, retail sales slowed to 3.7% y/y from 4.8%, and industrial production eased. Flooding in July disrupted infrastructure spending…

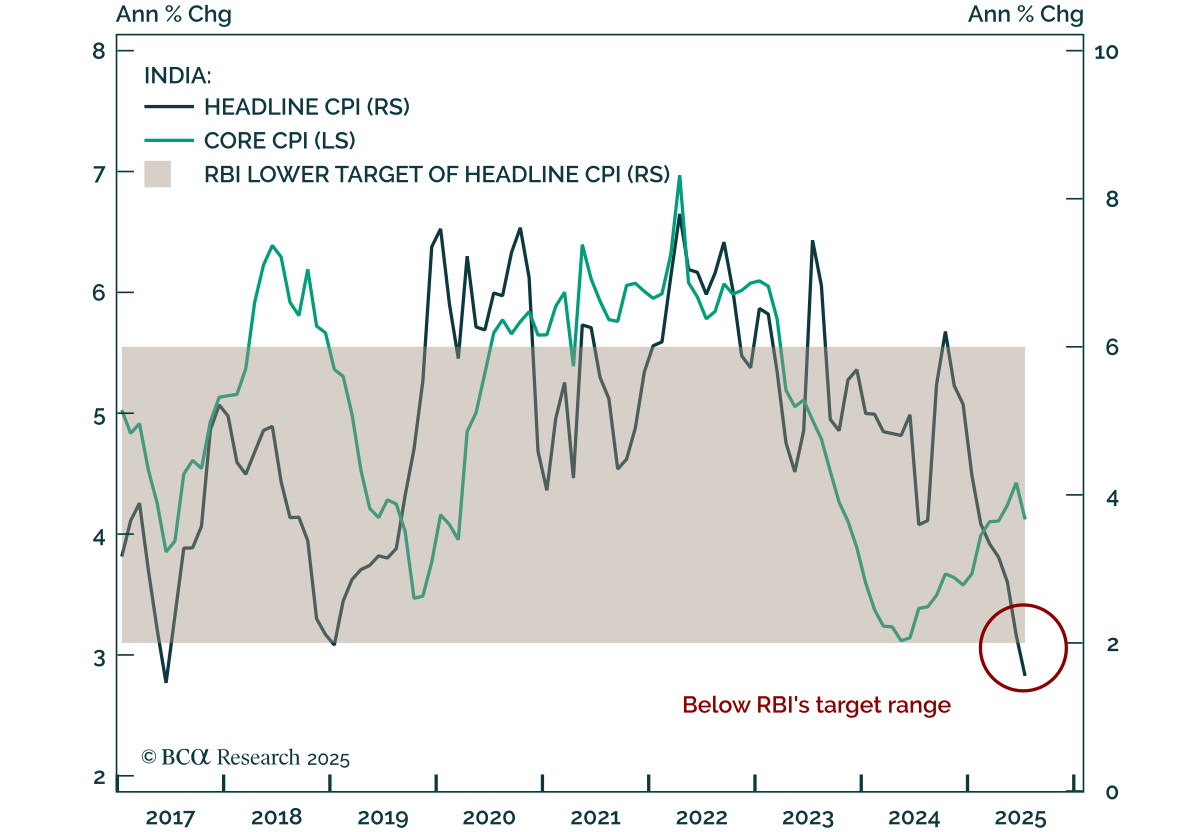

India’s sharp CPI undershoot will bring forward rate cuts, supporting a long on local bonds. Headline CPI fell to 1.55%, well below the RBI’s 2-6% target range, pointing to earlier and deeper easing than markets price. Our Emerging Markets strategists…

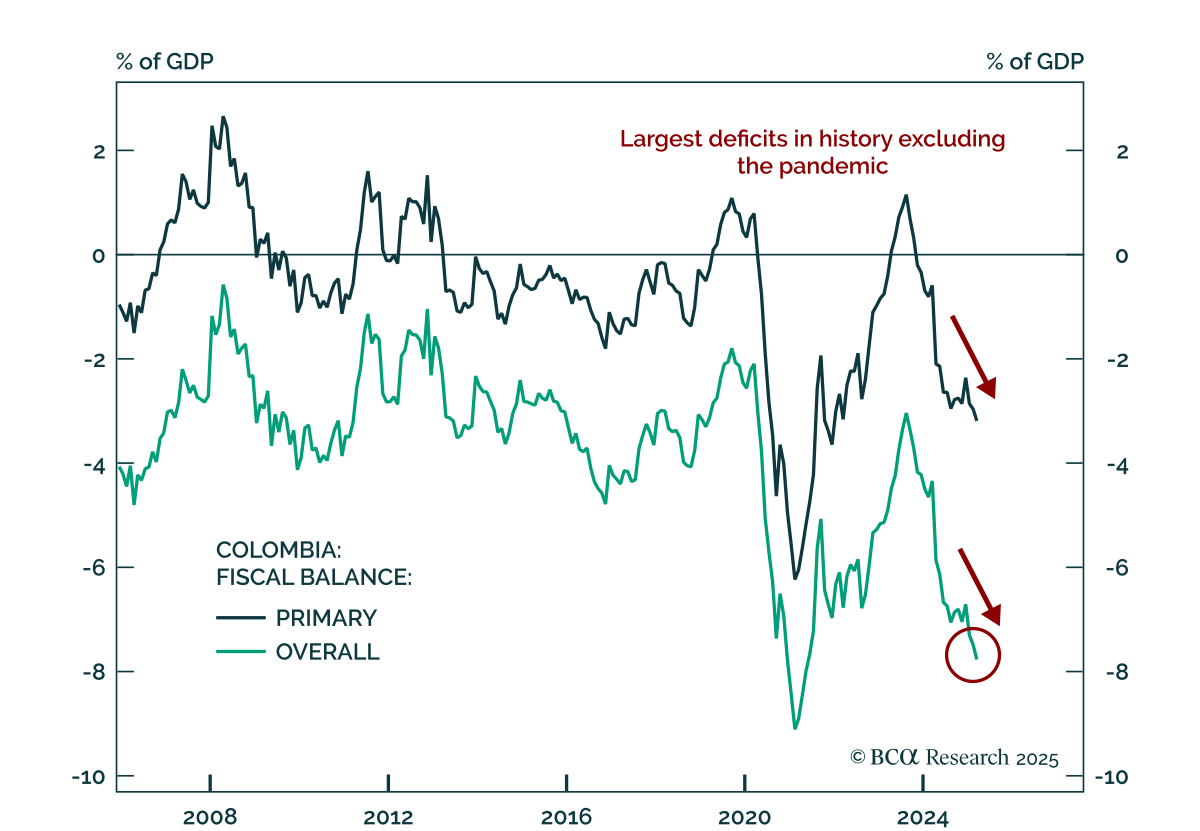

Our Emerging Markets strategists have upgraded Colombian equities, local bonds, and sovereign credit from underweight to neutral relative to EM benchmarks. Markets are caught between optimism about a potential rightward policy shift in 2026 and a…

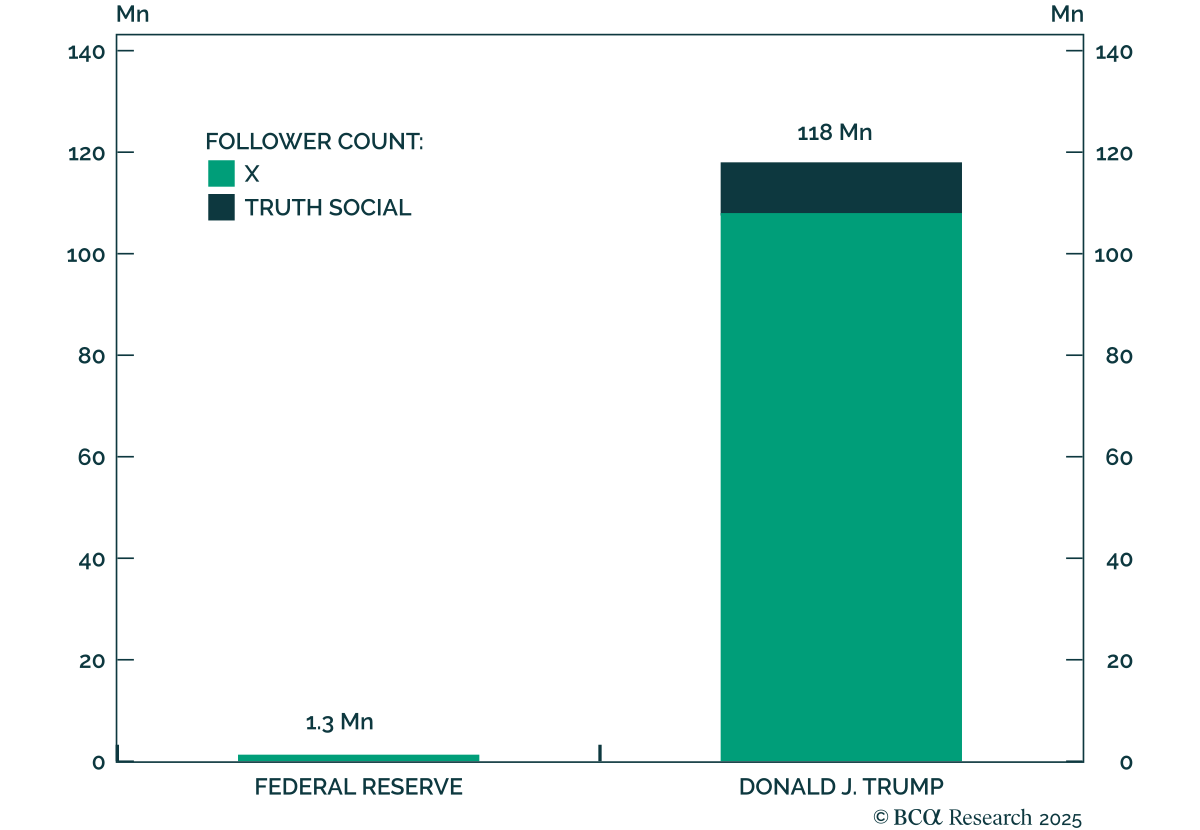

The Fed is losing its independence just as the macro environment demands a dovish pivot. Our GeoMacro strategists see it as a setup bullish for equities and bonds but bearish for the dollar. Our Chart Of The Week comes from Marko Papic, Chief GeoMacro…

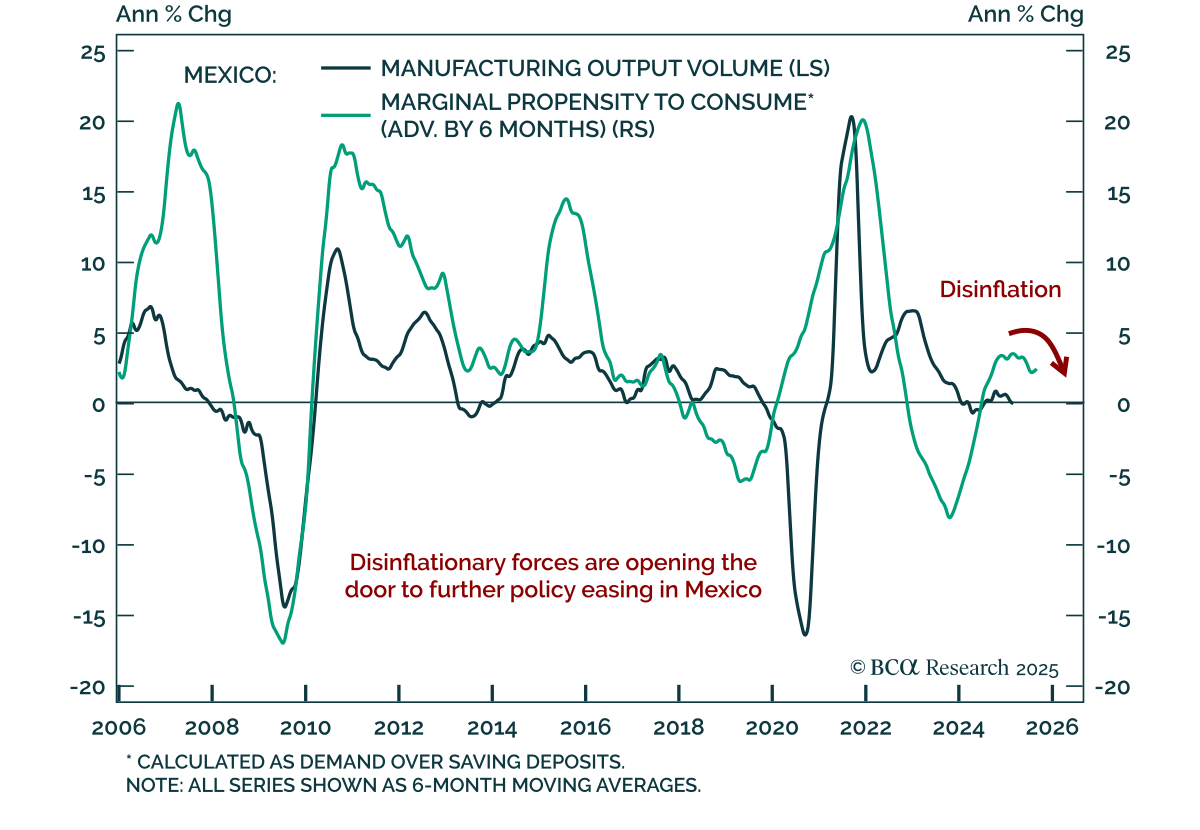

Banxico’s latest rate cut reinforces our bullish view on Mexican domestic bonds. Mexico’s central bank eased policy by another 25 basis points to 7.75%. Investors should bet on further easing. Inflation will continue falling within the target range…

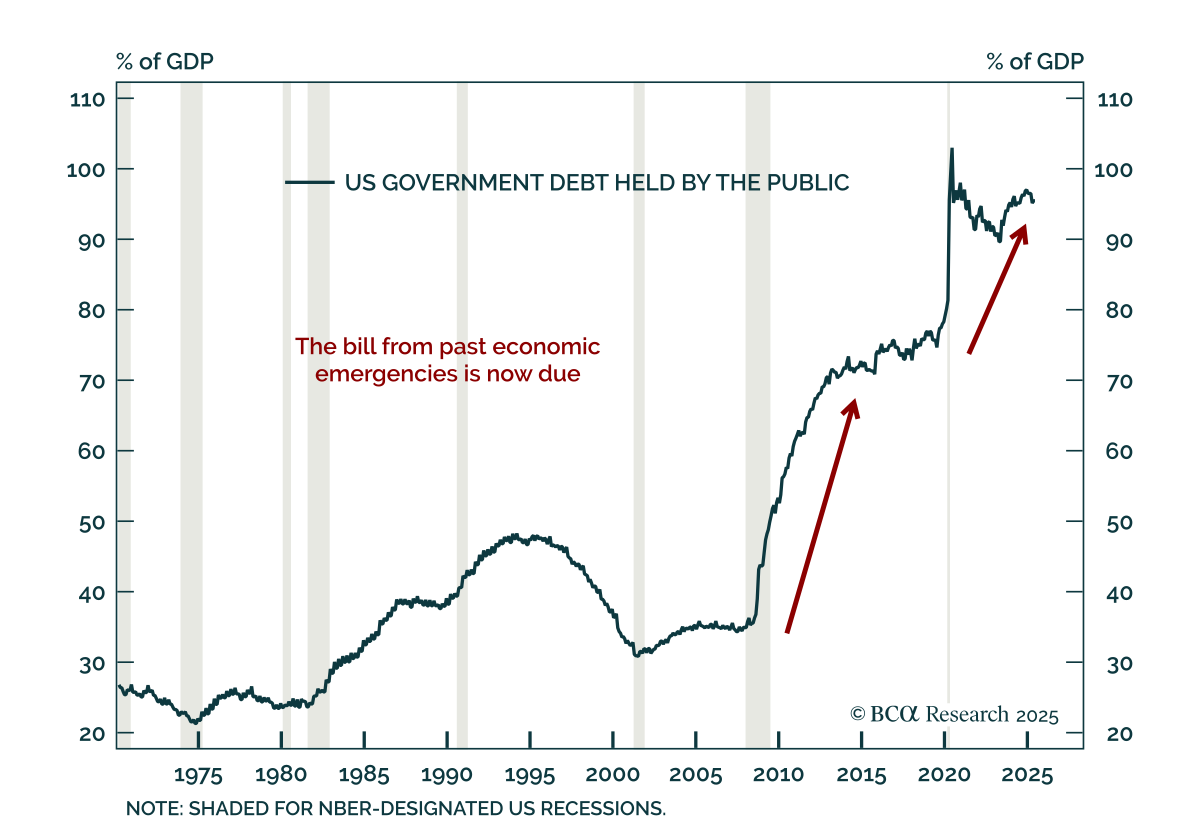

Our Bank Credit Analyst strategists argue that a US fiscal crisis should be treated as a base case over the next decade, not a tail risk. The ballooning US budget deficit reflects higher interest rates, demographic pressures, and the lingering effects of past…