Europe

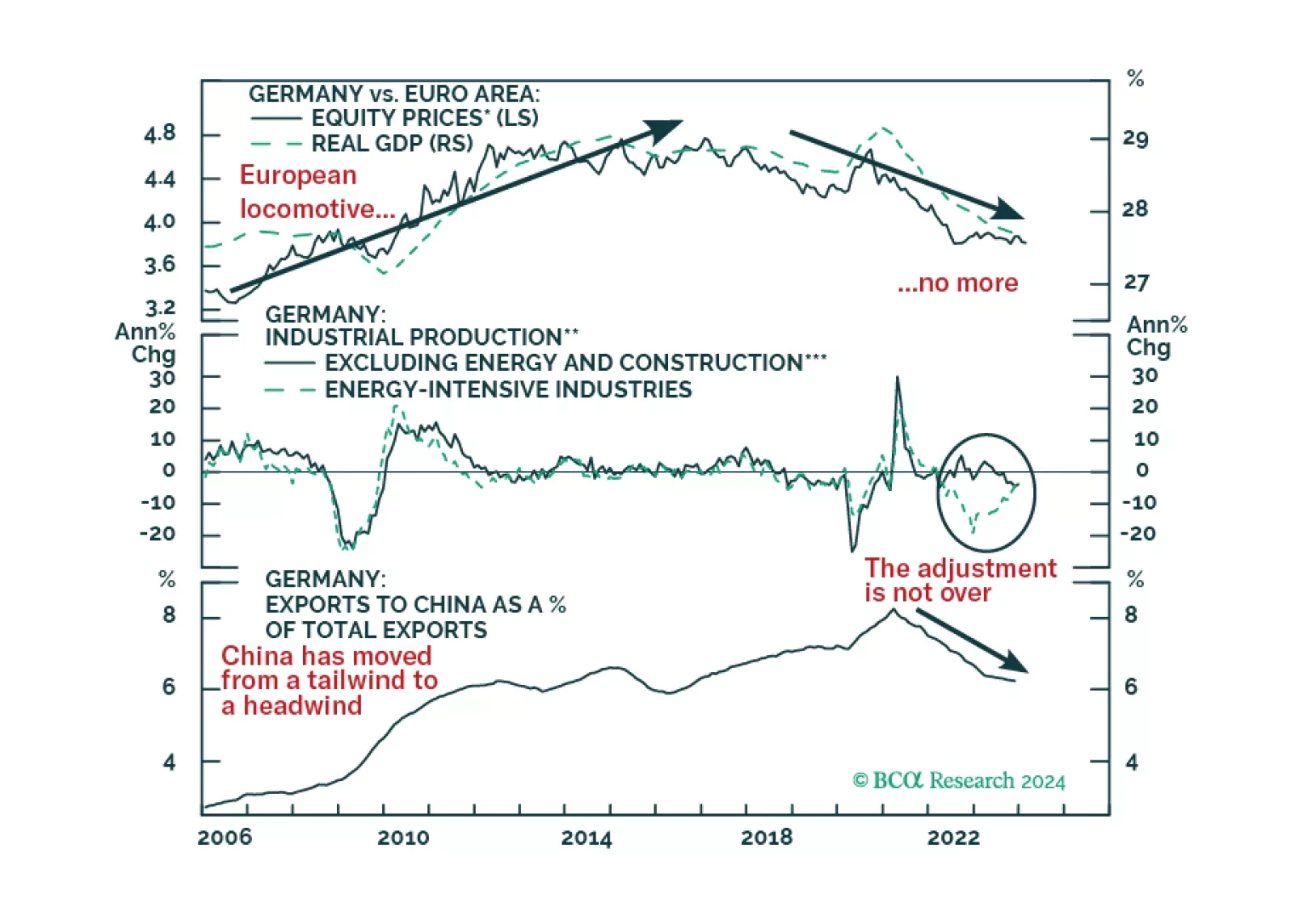

The German economy has lagged that of Europe. This trend will continue, but does it mean German equities will underperform further?

German factory orders delivered a positive surprise on Tuesday, unexpectedly increasing on both a monthly and annual basis. The 8.9% m/m increase in December came in well above consensus estimates of a 0.2% m/m decline. This translated to a 2.7% y/y rise,…

Euro area small-cap stocks are attractively valued compared to their large-cap counterparts. They have underperformed by 20% since April 2022, but small caps’ earnings have kept pace with those of large-cap firms. Hence, valuation indicators, including…

BCA Research’s European Investment Strategy service upgrades Swedish government bonds to neutral from underweight within European fixed-income portfolios. The Riksbank kept its policy rate steady at 4% last week. Governor Erik Thedéen and the Riksbank…

As expected, the Bank of England voted to keep its bank rate unchanged at 5.25% on Thursday – maintaining policy on hold for the fourth consecutive meeting. Two of the nine MPC members voted in favor of a 25bps rise (one less than in December) while one…

When will the US also buckle under high rates? We expect a US recession to begin around mid-year. Stay defensive.

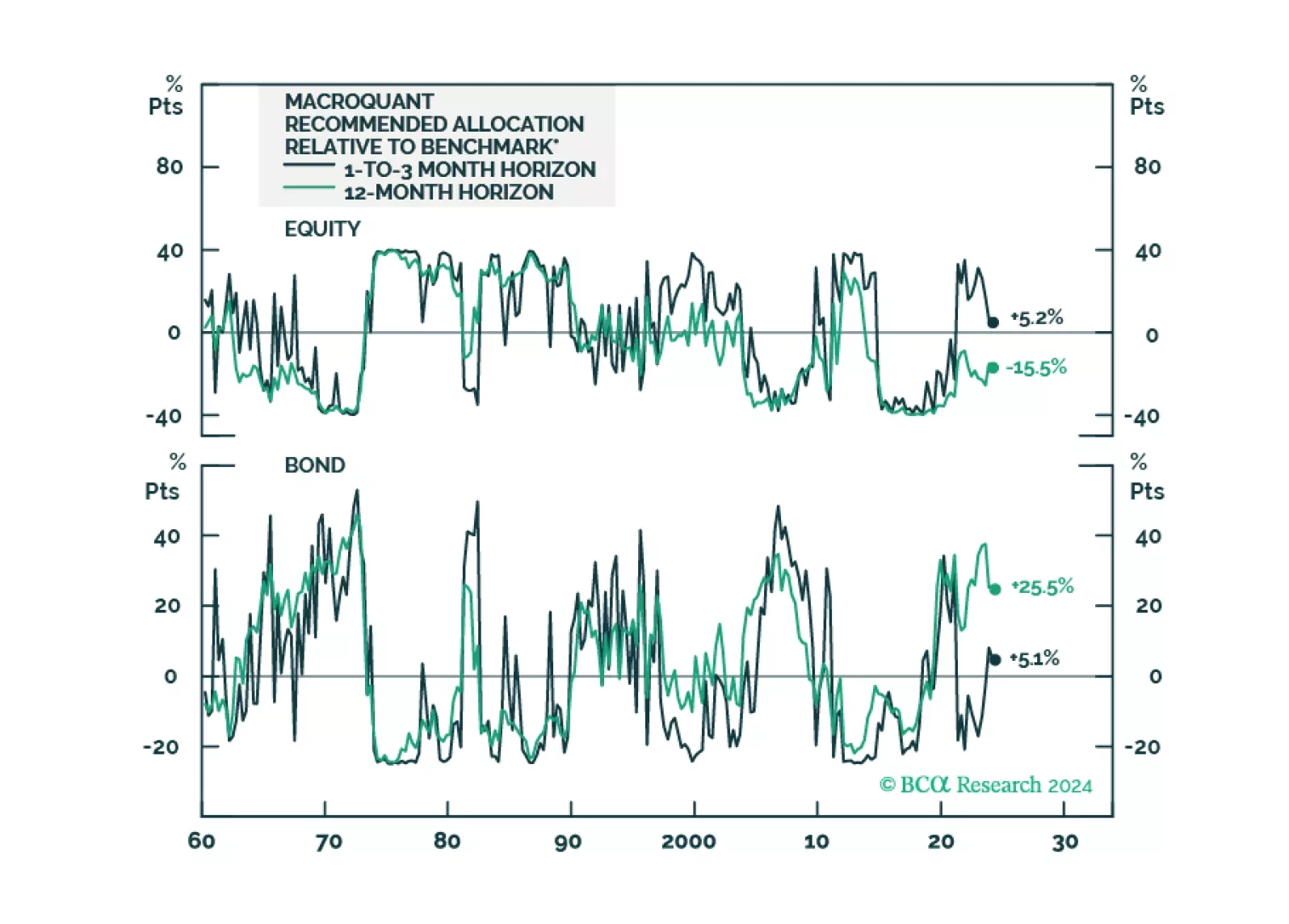

Following the release of the white paper yesterday, today we are sending you the inaugural issue of the MacroQuant Monthly, a report summarizing the output of our next-generation MacroQuant 2.0 model.

The strong H2/2023 rally in global credit markets can be attributed to lower global inflation and the associated reduction in global interest rate volatility. However, our colleagues at BCA Research’s Global Fixed Income Strategy service argue that credit…

According to BCA Research’s Foreign Exchange Strategy service investors should remain long NOK/SEK. The Norges Bank kept policy on hold last week, but the bullish case for the NOK (albeit over the short term) remains in place. There were no major…

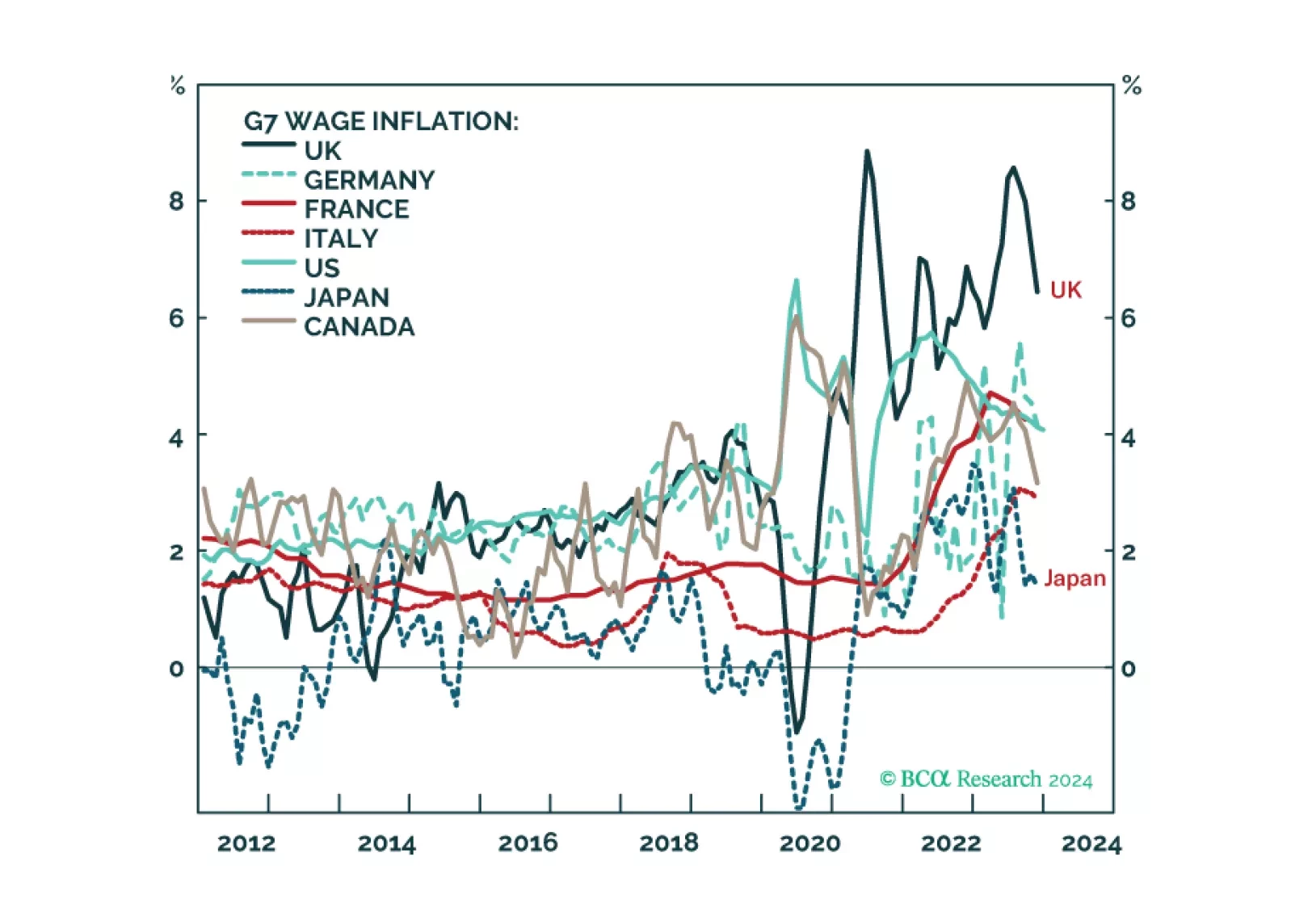

We describe and explain the wide disparity of wage inflation across G7 economies, and discuss what it means for the Fed, ECB, BoE, and BoJ policy moves in the coming year. Plus: we highlight two investments ripe for reversal, and two investments ripe for rebound.