Europe

MacroQuant recommends a slight underweight in equities, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, has upgraded oil and copper to overweight, and is bullish on gold.

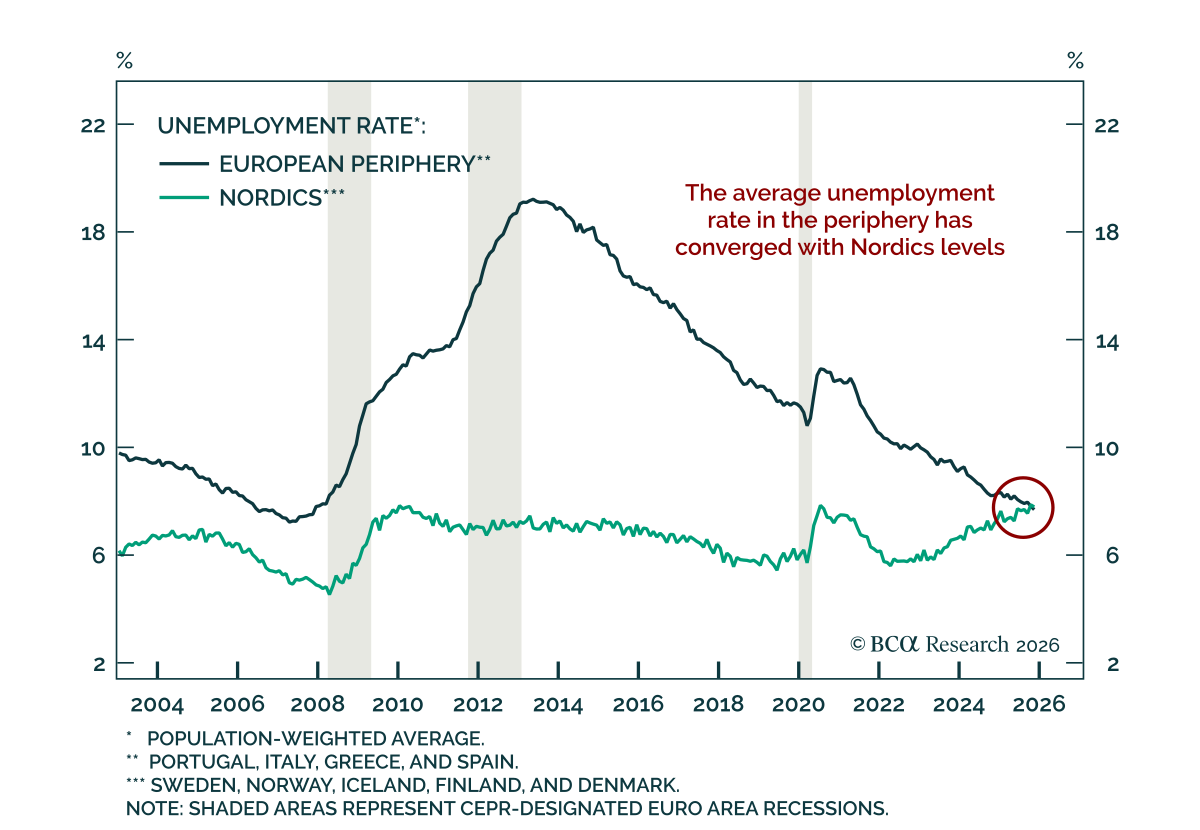

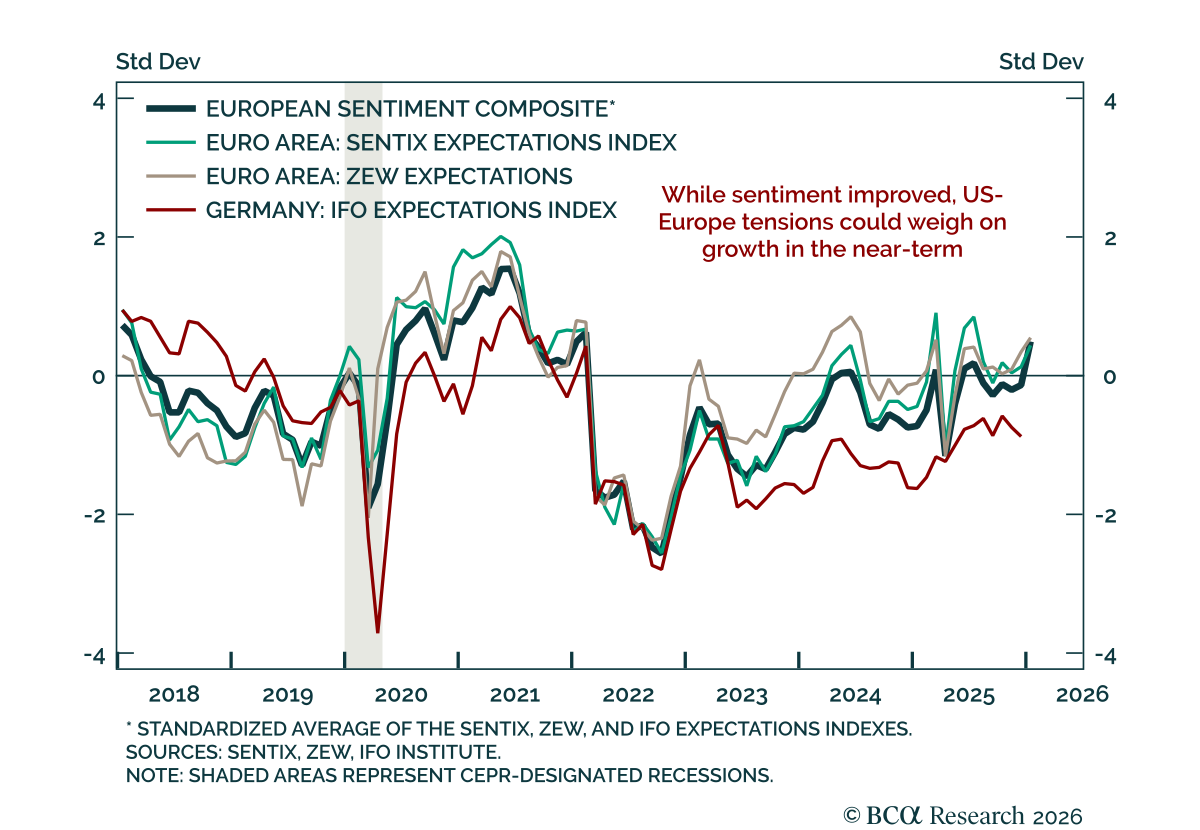

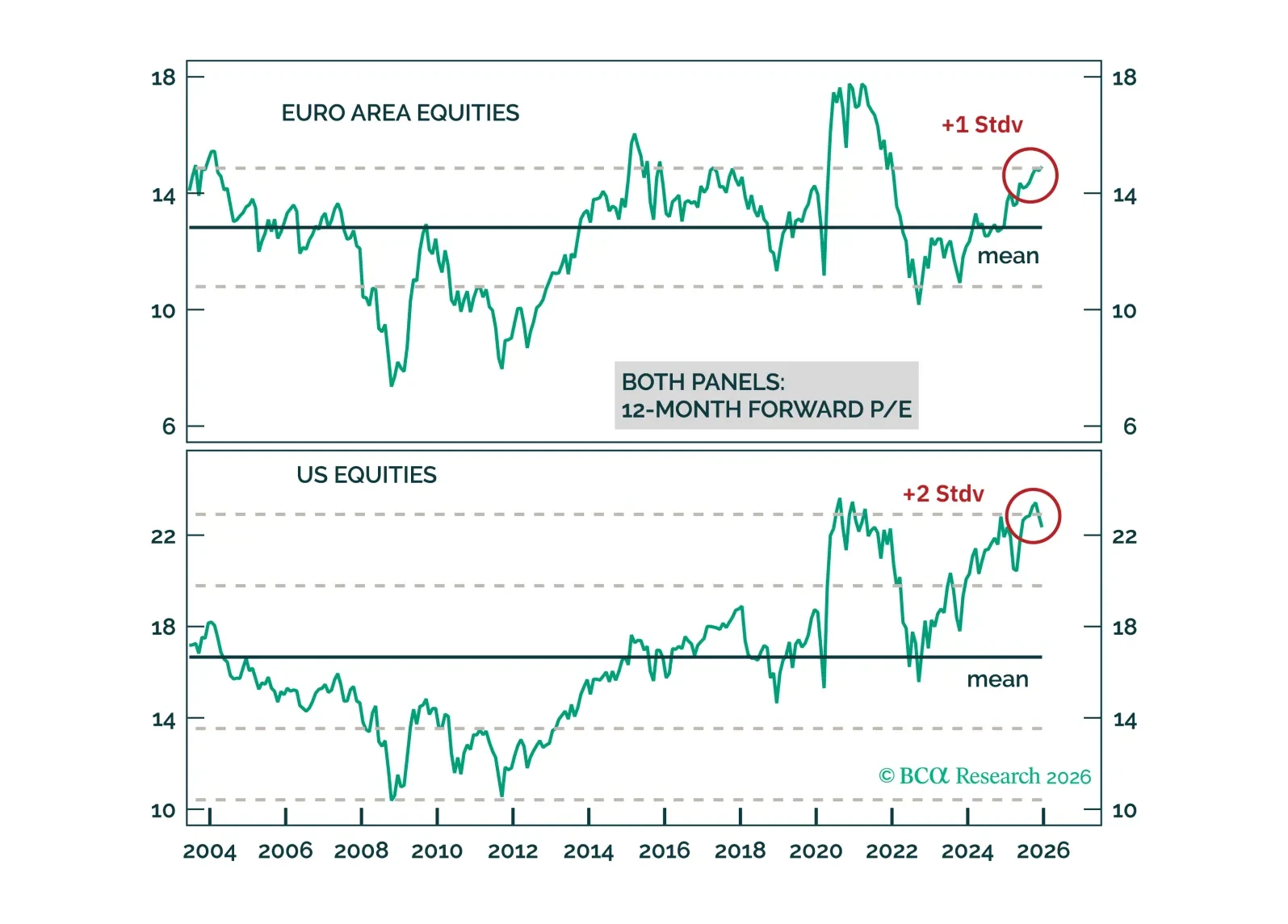

Europe is in a geopolitical sweet spot. Exaggerated fears of Russian military aggression and abandonment by the United States, as well as increased competition from China, create a geopolitical imperative to stimulate, reflate, and reform. Taken together with fading cyclical headwinds, it suggests that European risk assets can continue to outperform US ones on a cyclical investment time horizon. Remain long European stocks, in particular industrials, and EUR/USD.

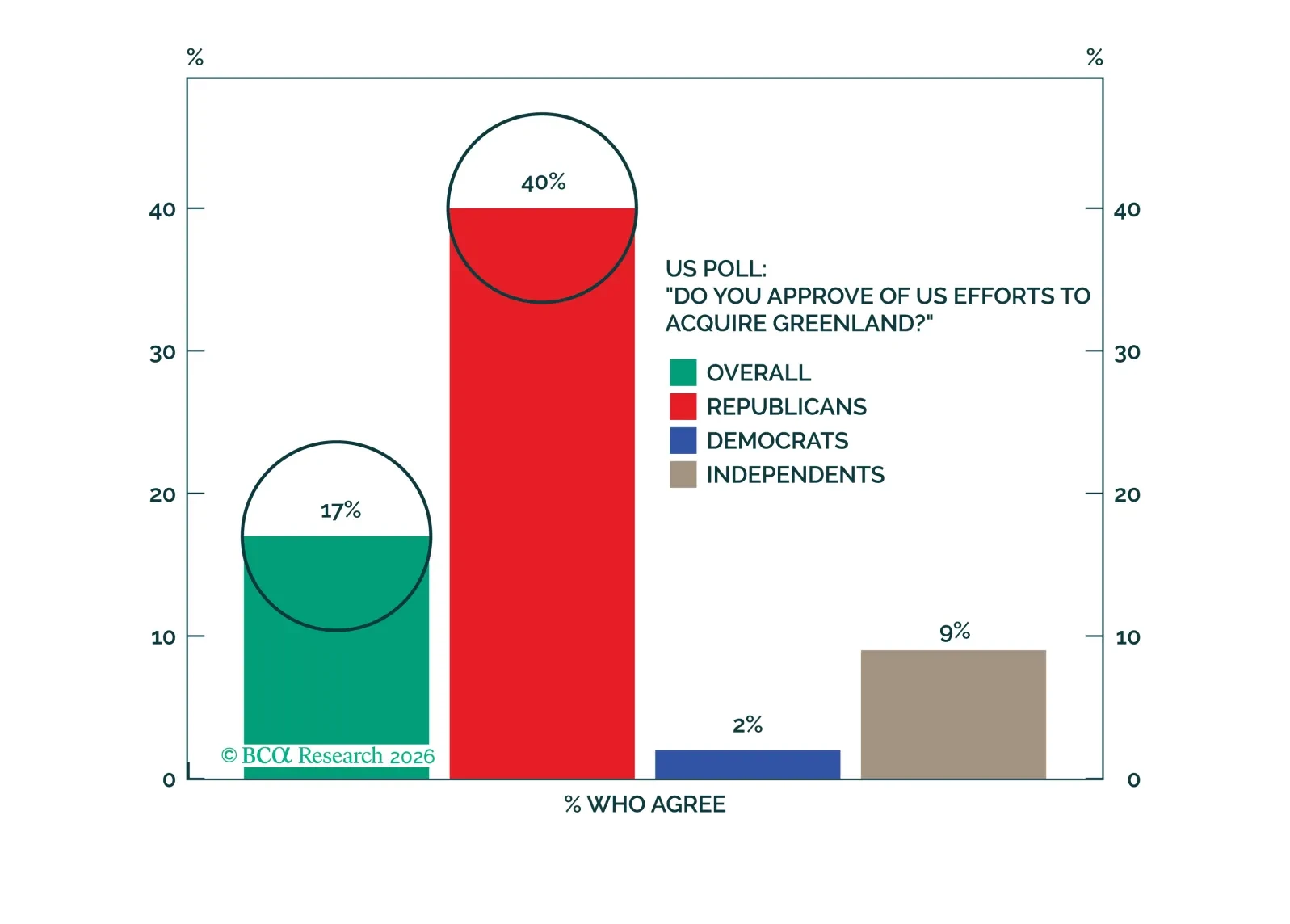

Investors should bet against the US seizing Greenland by force and collapsing NATO. But stay tactically defensive anyway.