Europe

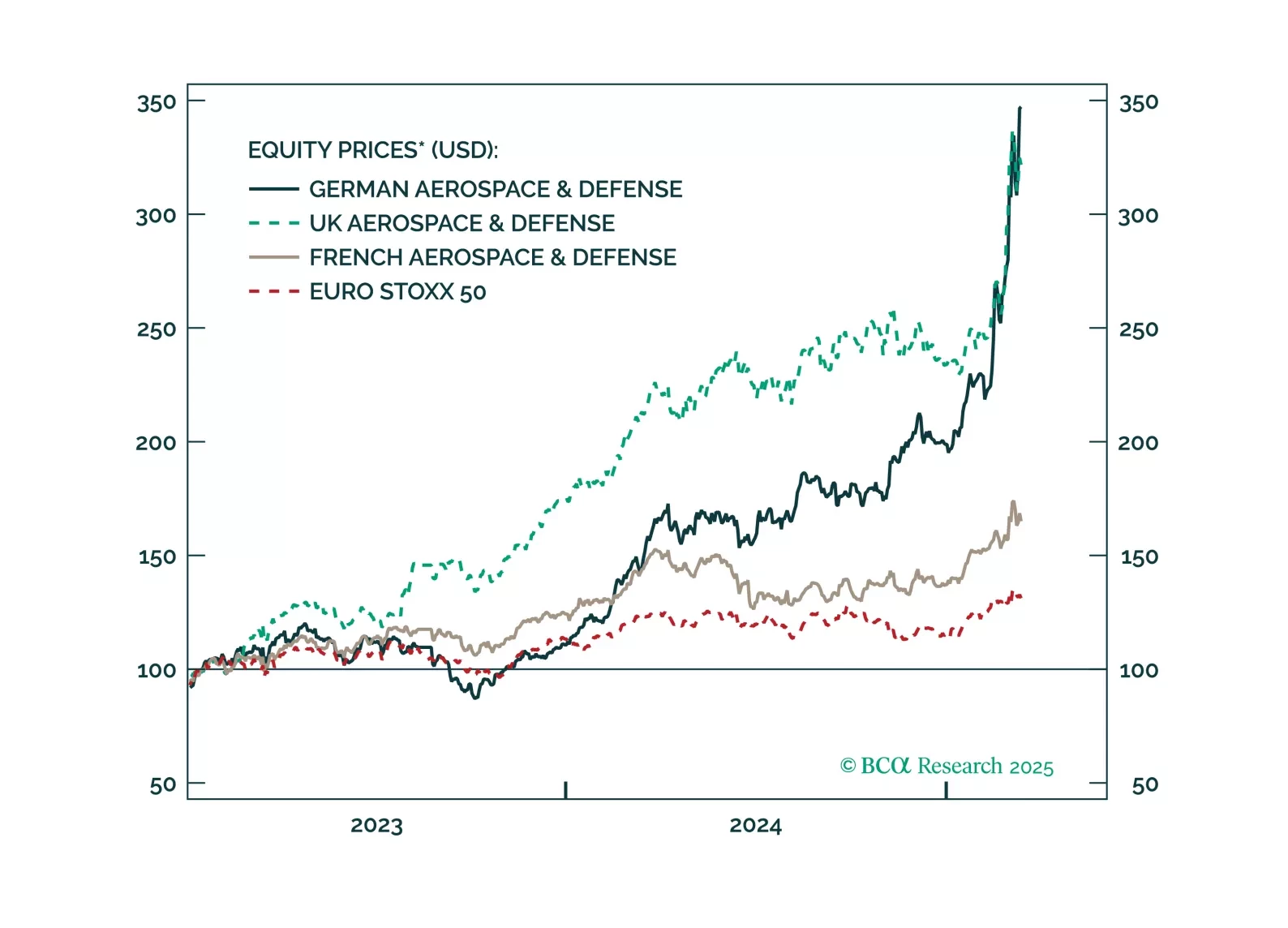

Investors should not chase the rally in European defense names any further. Too much good news has been priced in too quickly.

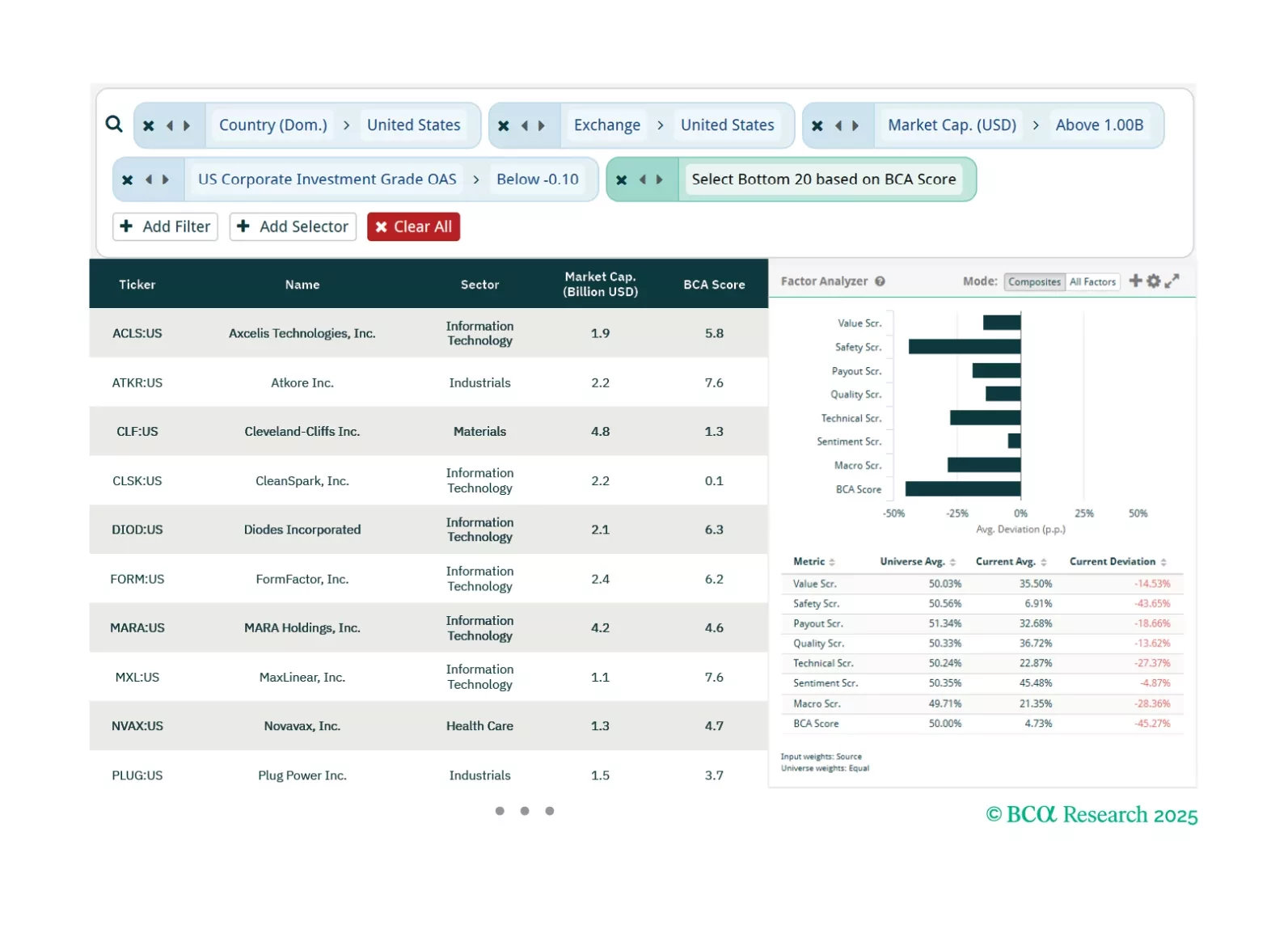

This week, our three screeners cover equity plays in US OAS Spreads, US Exceptionalism, and “DIVE”.

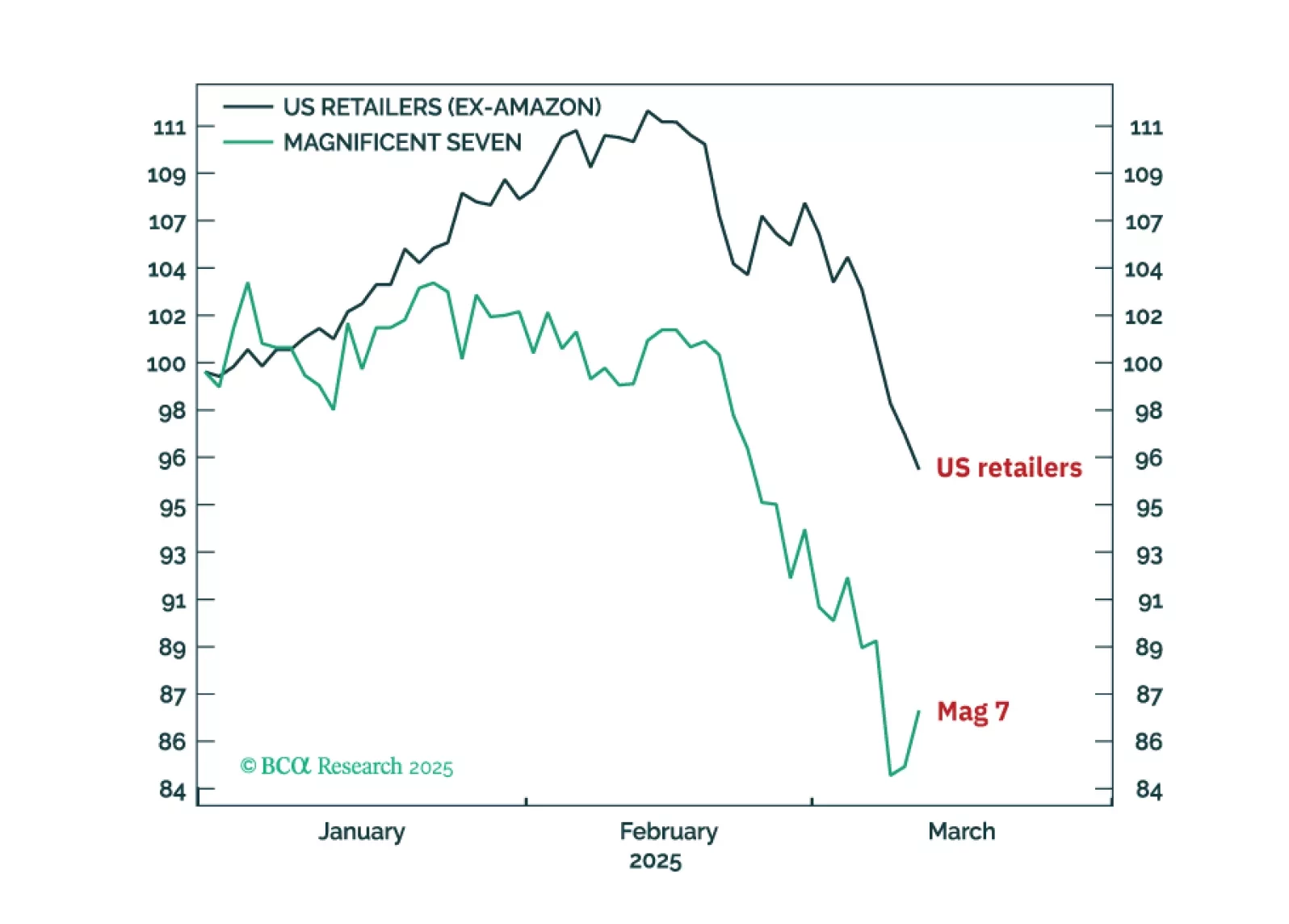

The Trump slump is nearing a temporary reprieve, with a playable countertrend rally in stocks and a tactical rebound in the dollar. Go tactically long USD/SEK. For long-term investors though, the AI bubble still has a lot of air to come out.

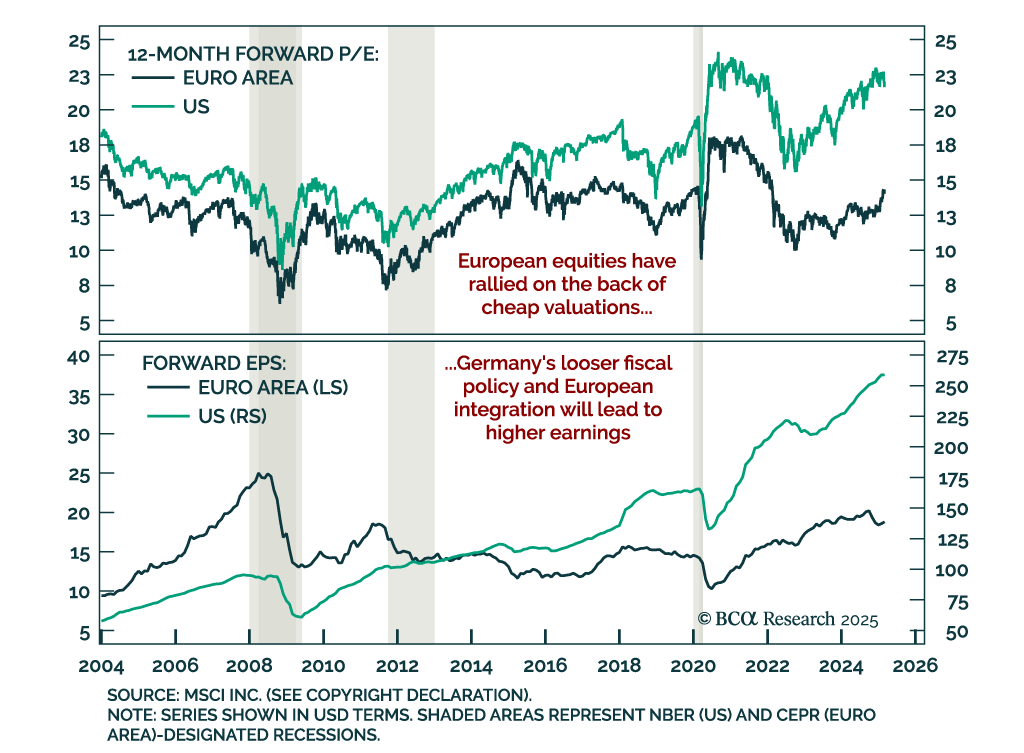

There is an alternative to investing in US stocks: Do it via Europe (DIVE). Allocate to European sectors or stocks that are highly and positively correlated with the Magnificent 7 but do not suffer stretched valuations.

This week, our three screeners cover equity plays in US defensives, US Tech, and European Small Cap Value.

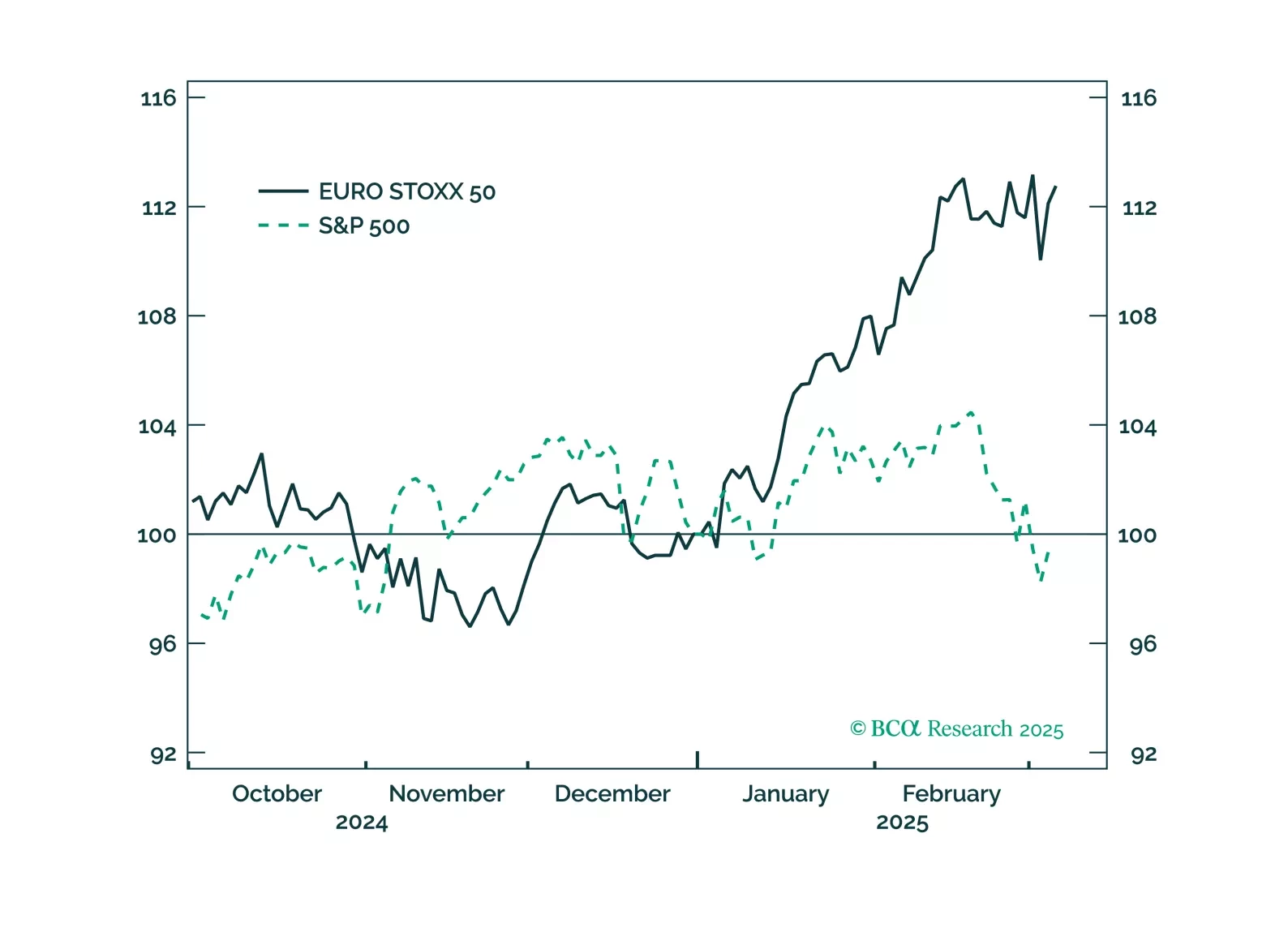

The US economy is set to enter a recession within the next few months. Stay underweight equities and overweight cash. Look to increase fixed-income duration exposure over the coming months. The euro is likely to strengthen and European stocks should outperform US stocks over the next month or so, but these trends will reverse by the middle of this year.

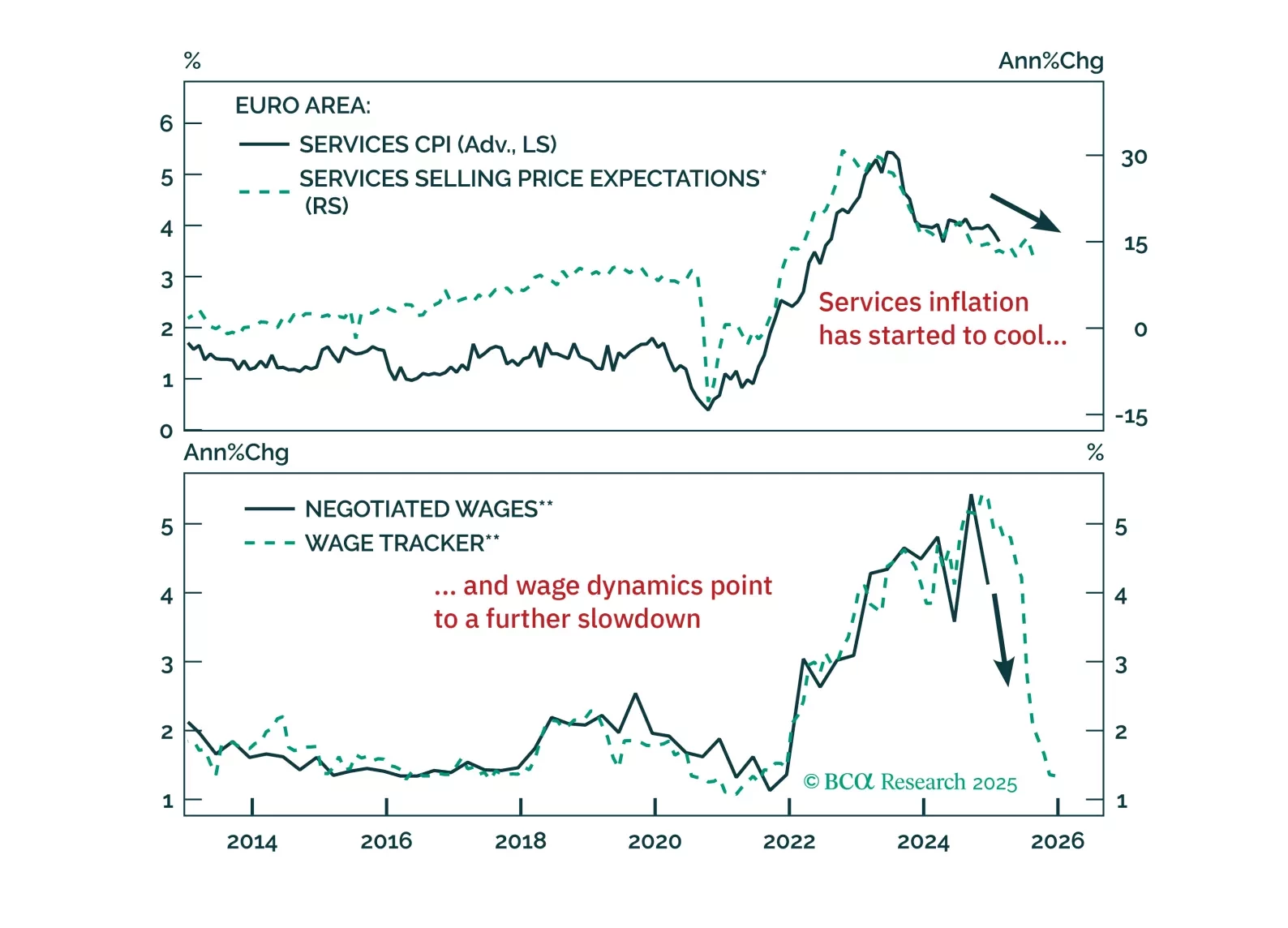

The ECB cut rates as expected, but rising yields and a stronger euro are tightening financial conditions just as fiscal policy shifts the macro landscape. With more rate cuts ahead and market positioning stretched, we outline the key risks, investment opportunities, and our updated call on the ECB’s terminal rate. Read our full report for actionable insights.