Europe

Our European and FICC strategists remain tactically constructive on Europe while urging investors to prepare portfolios for a more challenging medium-term environment. Rather than issue a single house forecast, our colleagues present two credible but…

Europe faces a difficult macro backdrop, but whether it slips into recession remains finely balanced. We present two perspectives before translating them into investment implications.

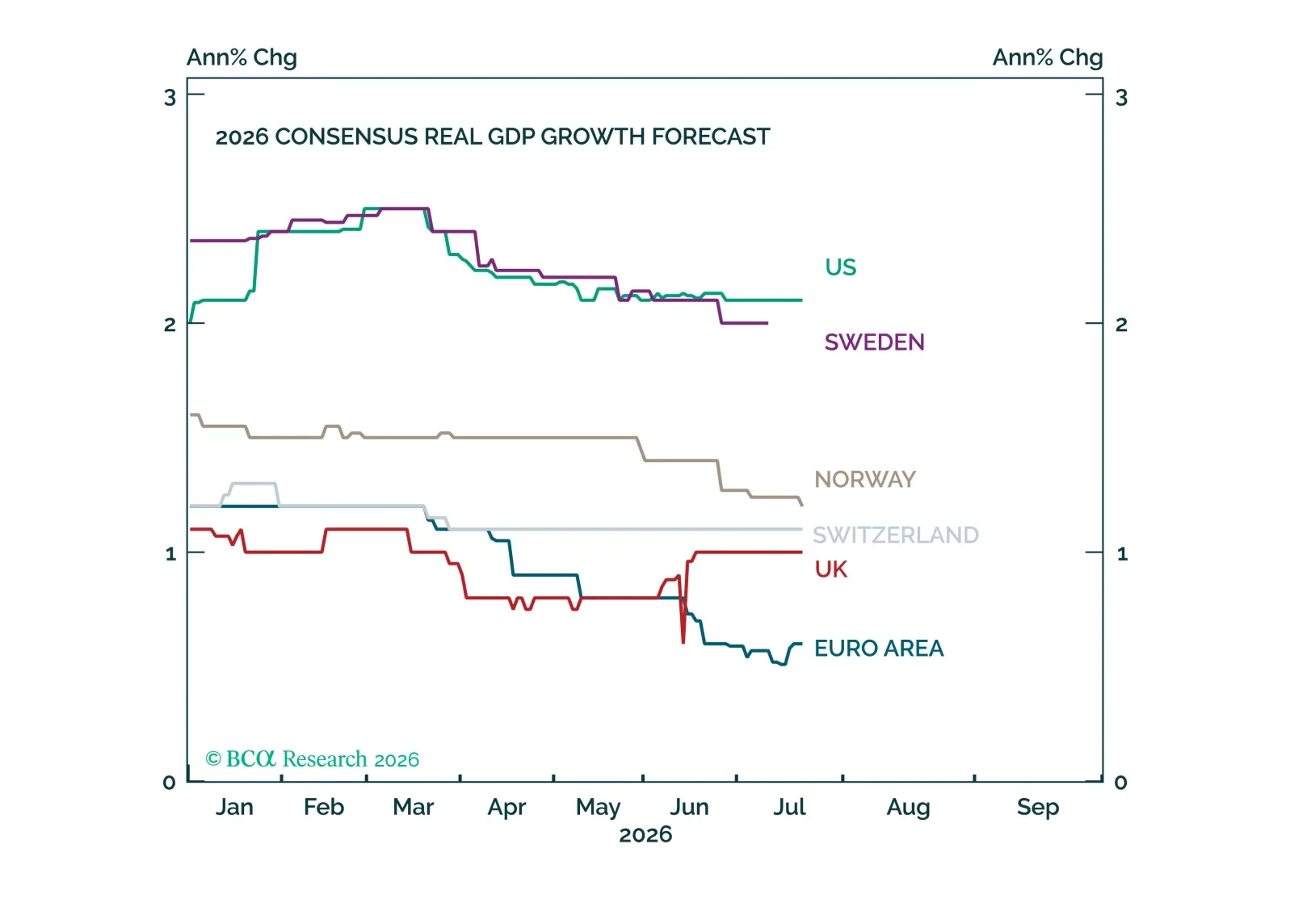

July marked the end of de minimis exemptions in Europe, pointing to the inflationary consequences of the retreat from globalization. Starting July 1st, the European Union imposed a flat €3 customs duty on all parcels valued under €150, ending a duty-free…

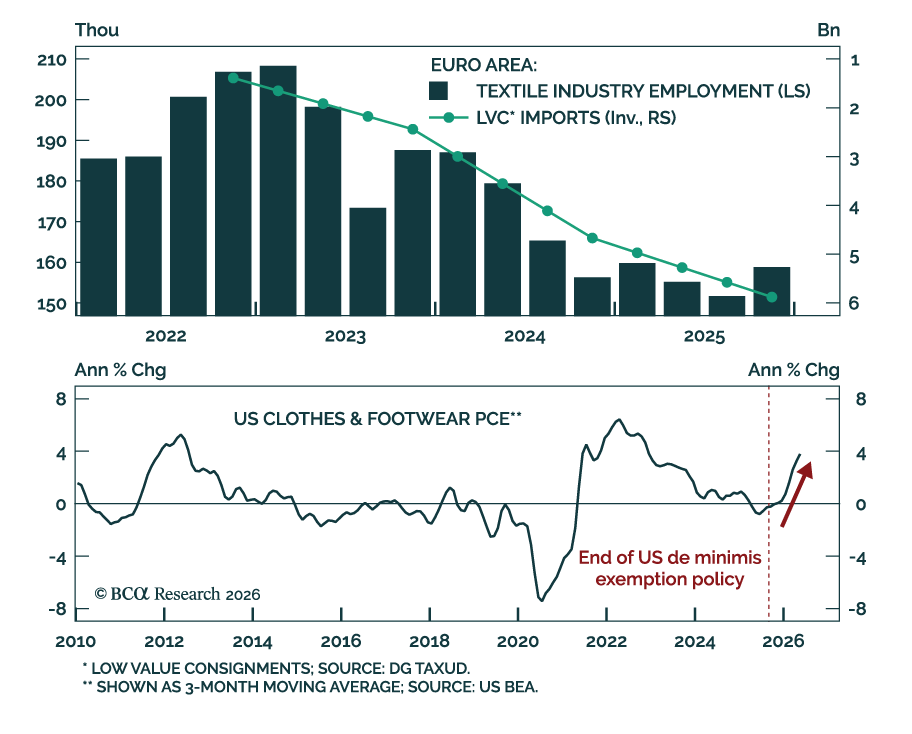

Our European investment strategists recommend reducing exposure to French risk assets as France heads into its most consequential election in decades. A strained budget, a paralyzed political system, and a turbulent geopolitical backdrop are pushing voters…

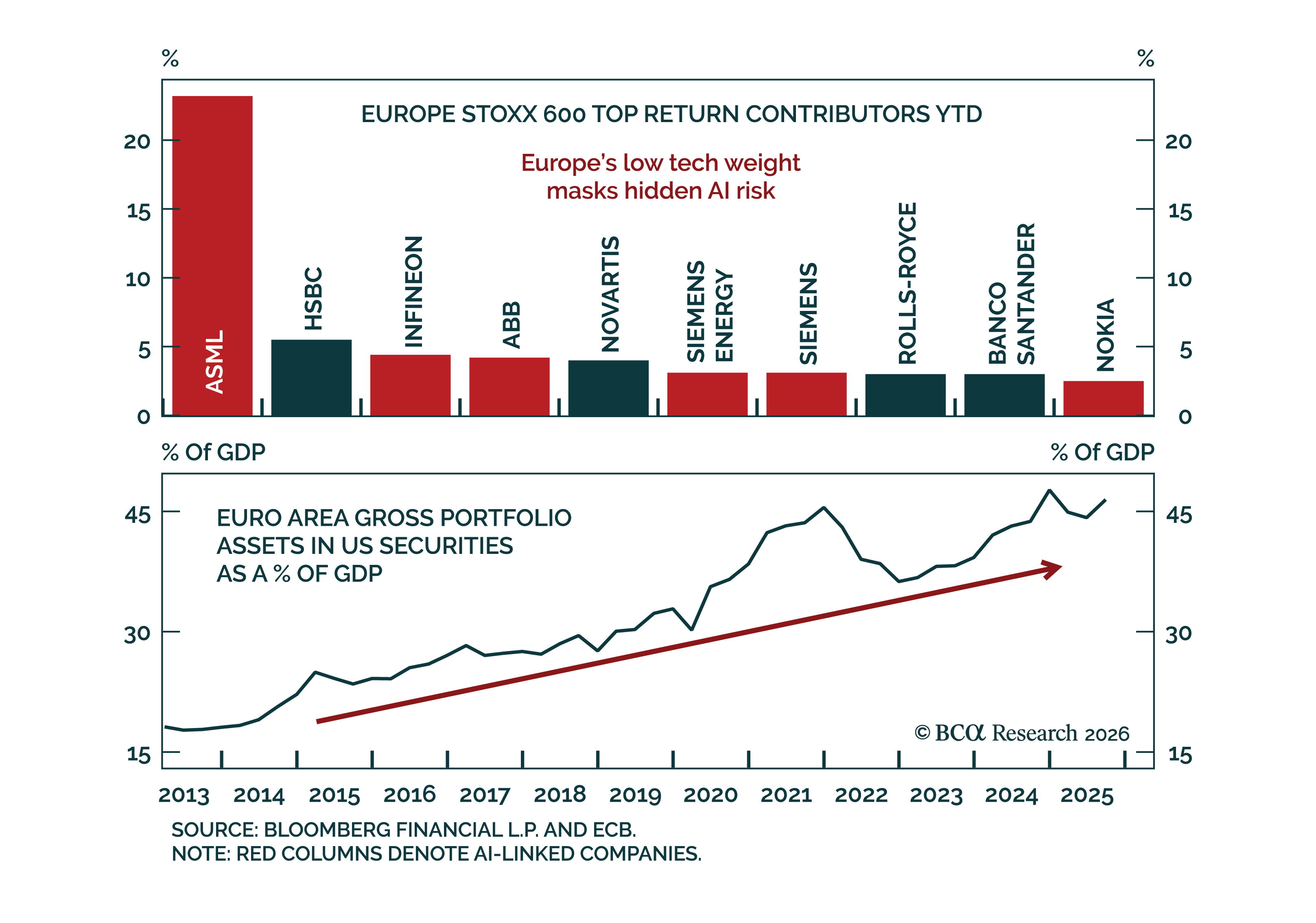

Europe is far less insulated from the AI trade than sector weights suggest. The Stoxx 600 has hit record highs on the back of earnings upgrades, improving macro data, and a rotation into laggards like healthcare, staples, financials, and domestic…

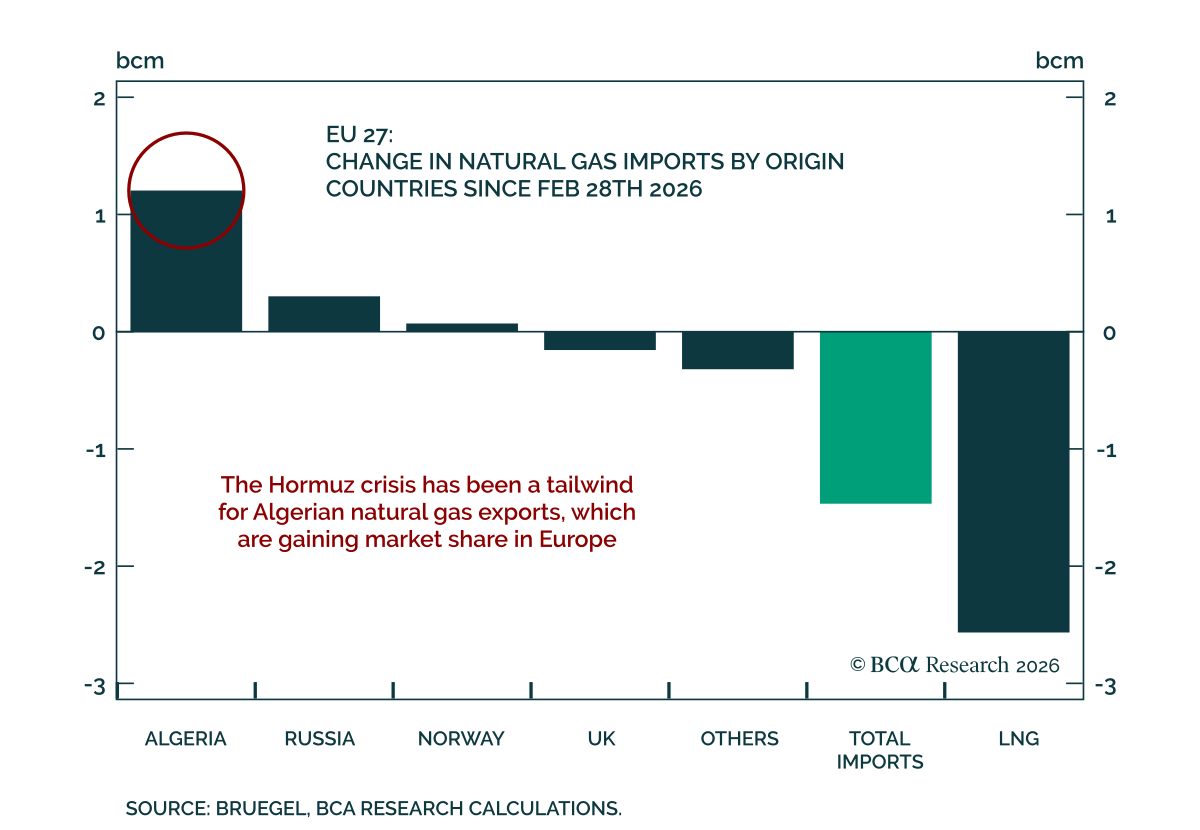

Algeria may offer the European Union some relief from its natural gas supply squeeze. Algeria has become the EU’s third-largest natural gas supplier, delivering around 40 billion cubic meters in 2025, accounting for roughly 14% of total EU imports. The timing…

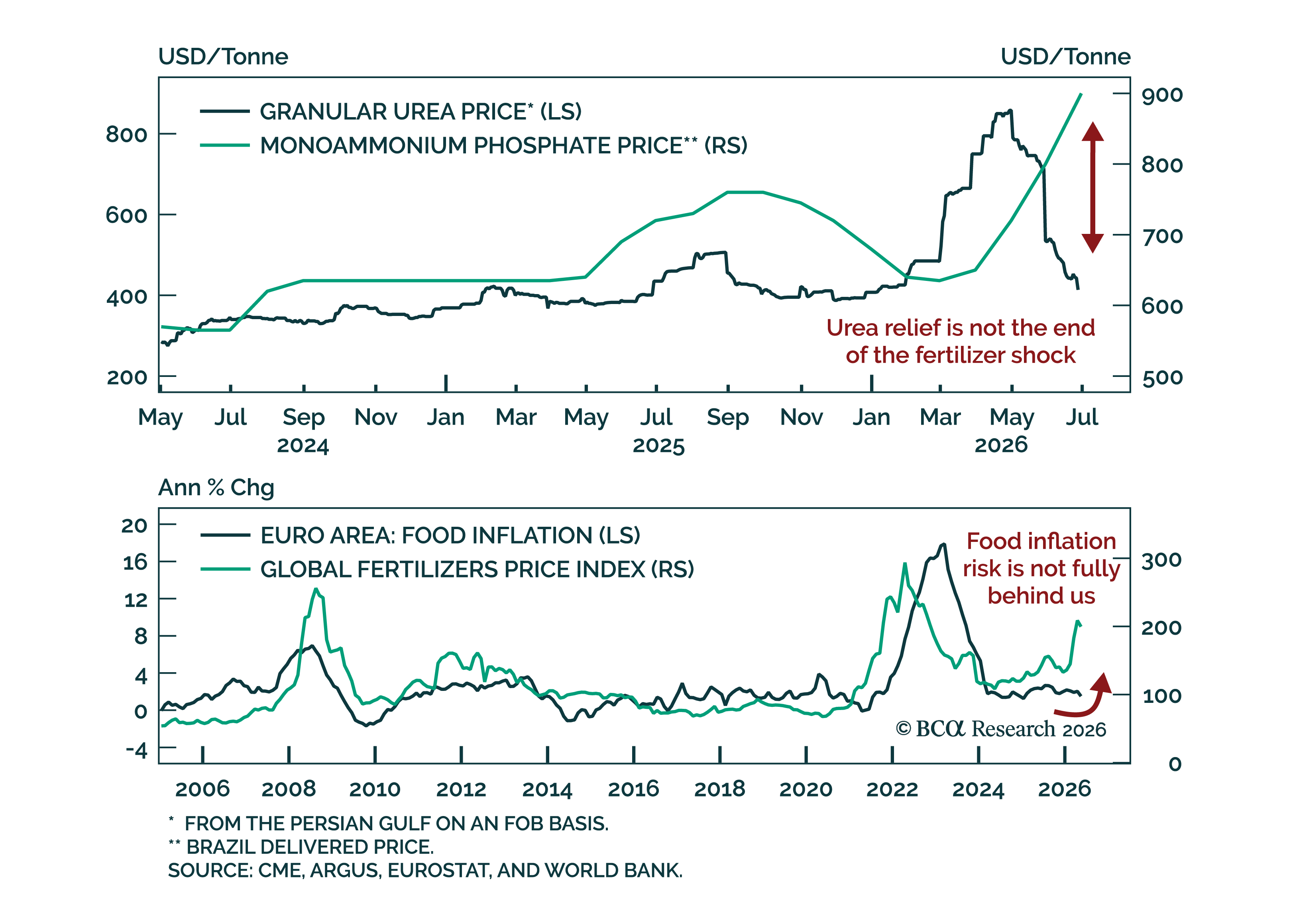

The collapse in urea prices is giving markets a false sense of relief; Europe should not assume the food shock is over. Granular urea price has fallen back to prewar level of $440/Tn, but only after farmers had already faced the worst of the Iran-driven…

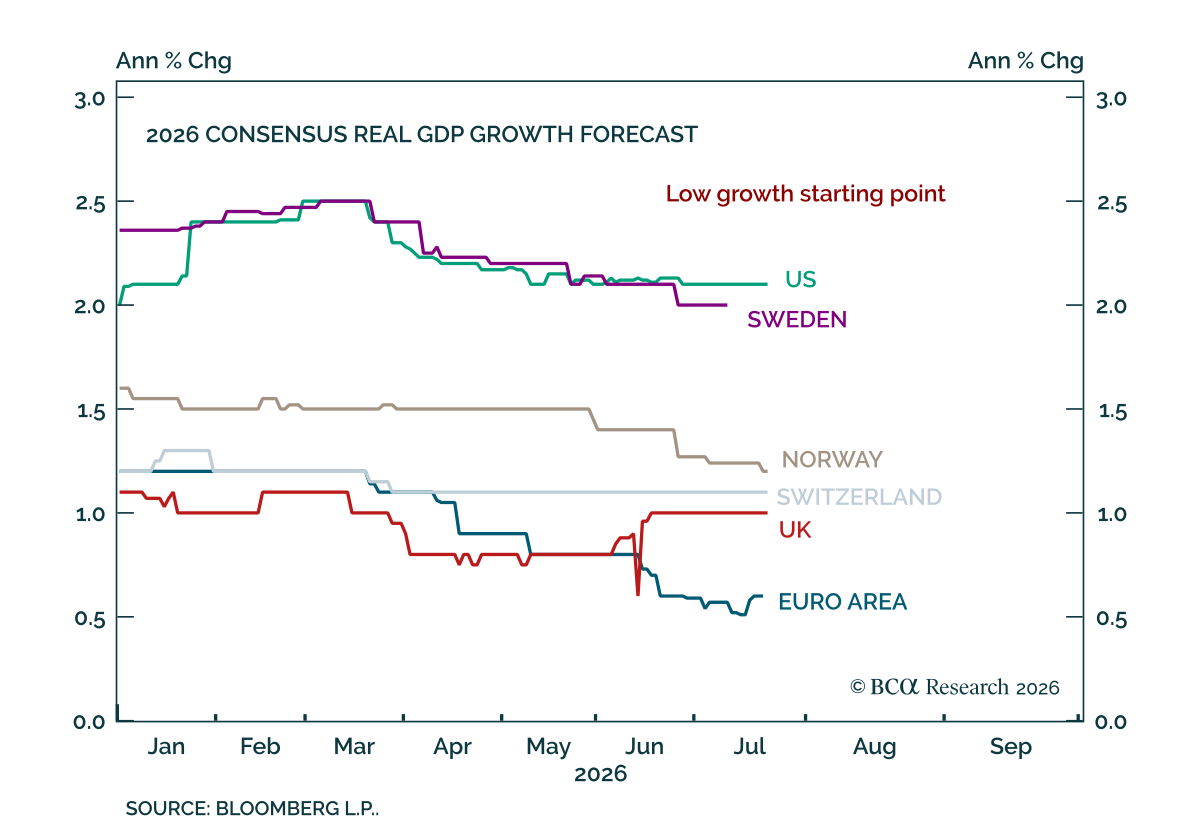

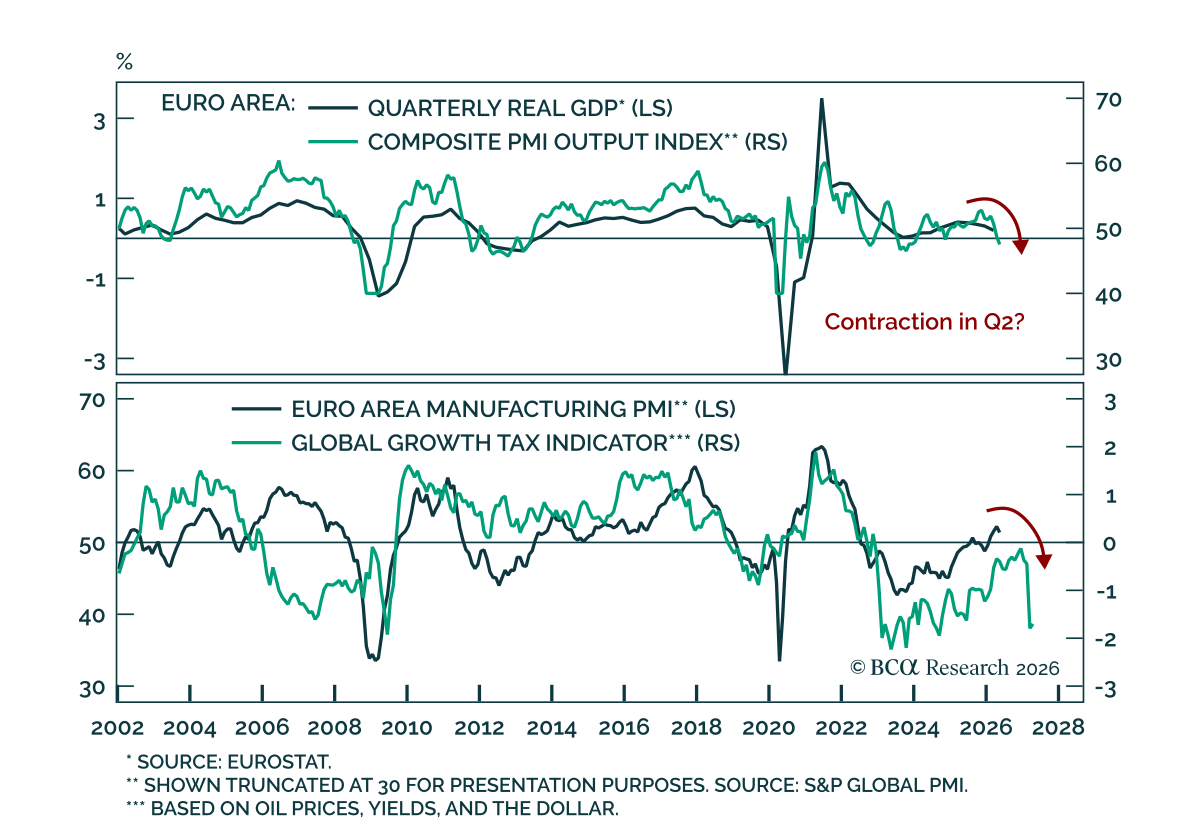

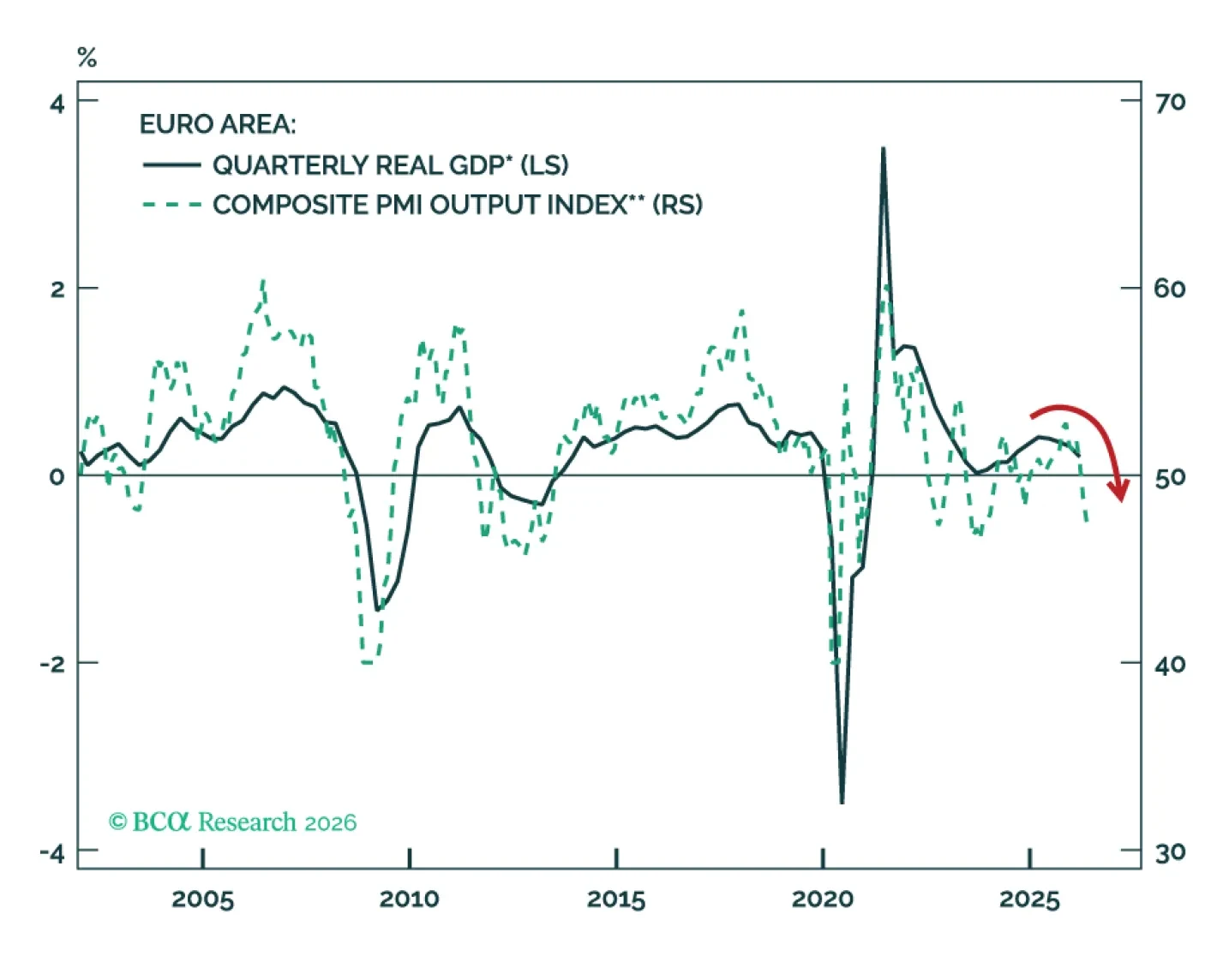

Our European strategists argue Europe is shifting from stagflation toward recession. Growth is weakening rapidly, labor markets are softening, and limited fiscal space leaves the economy exposed to renewed inflationary pressures, especially…

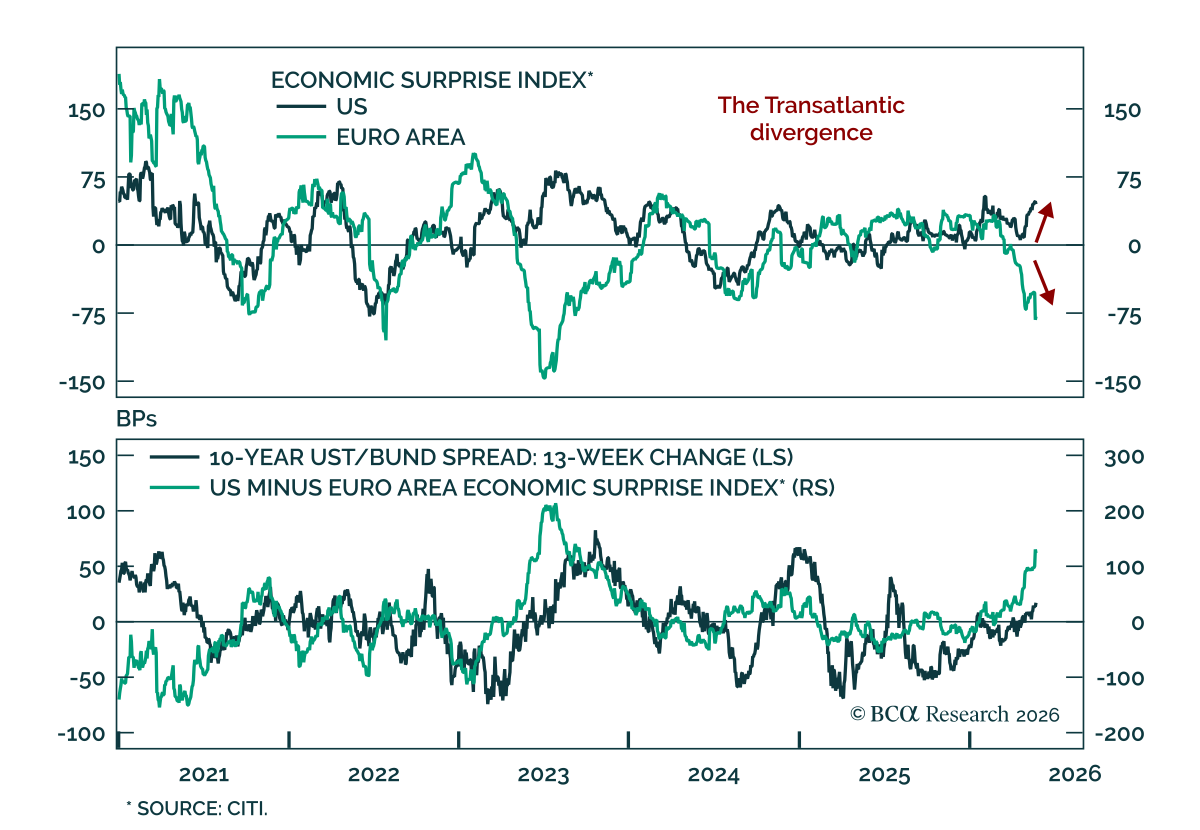

Go long German 10-year Bunds versus US 10-year Treasuries as US resilience diverges from euro area weakness. The trade is backed by a widening growth gap, with the US better insulated from rising oil prices and the euro area losing momentum. The US…

Europe is sliding from stagflation toward recession as prolonged disruptions in the Strait of Hormuz weaken growth, labor markets, and supply chains while keeping inflation elevated. Even if a US-Iran deal is reached, limited fiscal support and rising food inflation leave the Euro Area increasingly vulnerable to a deeper economic downturn.