Euro Area

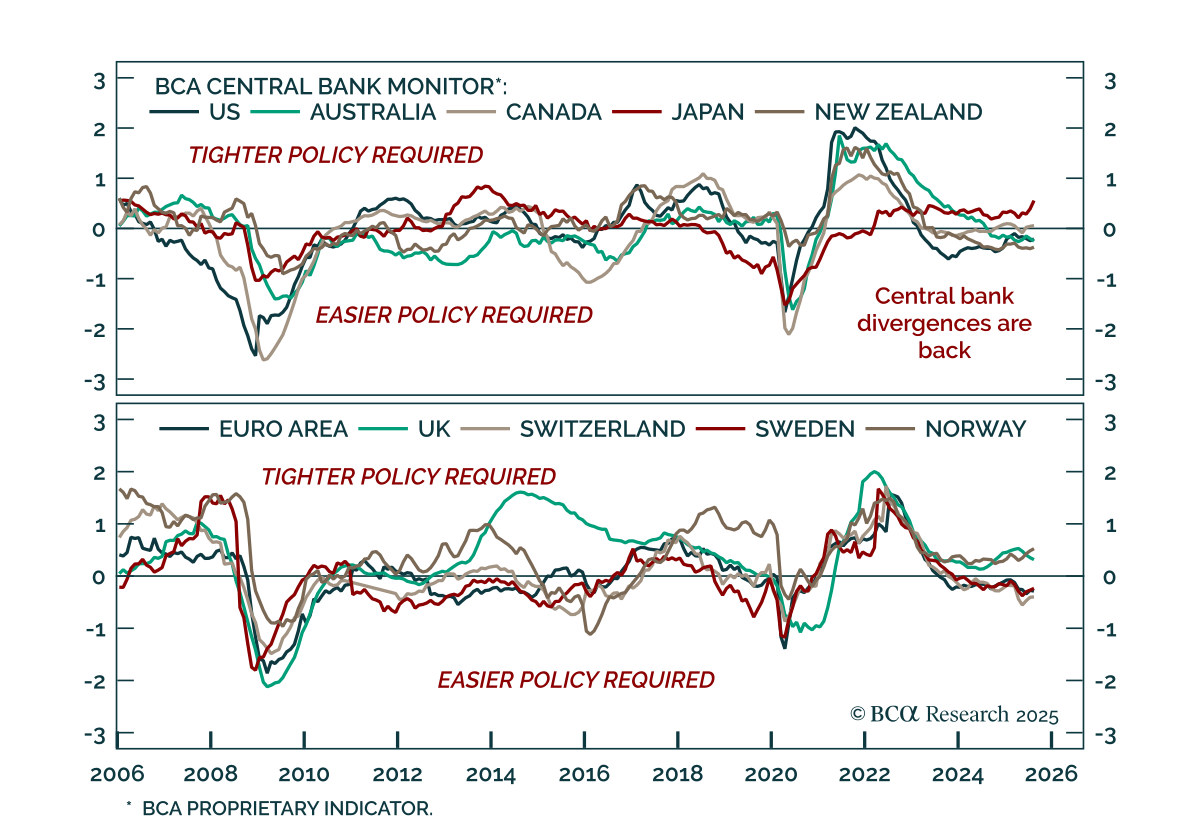

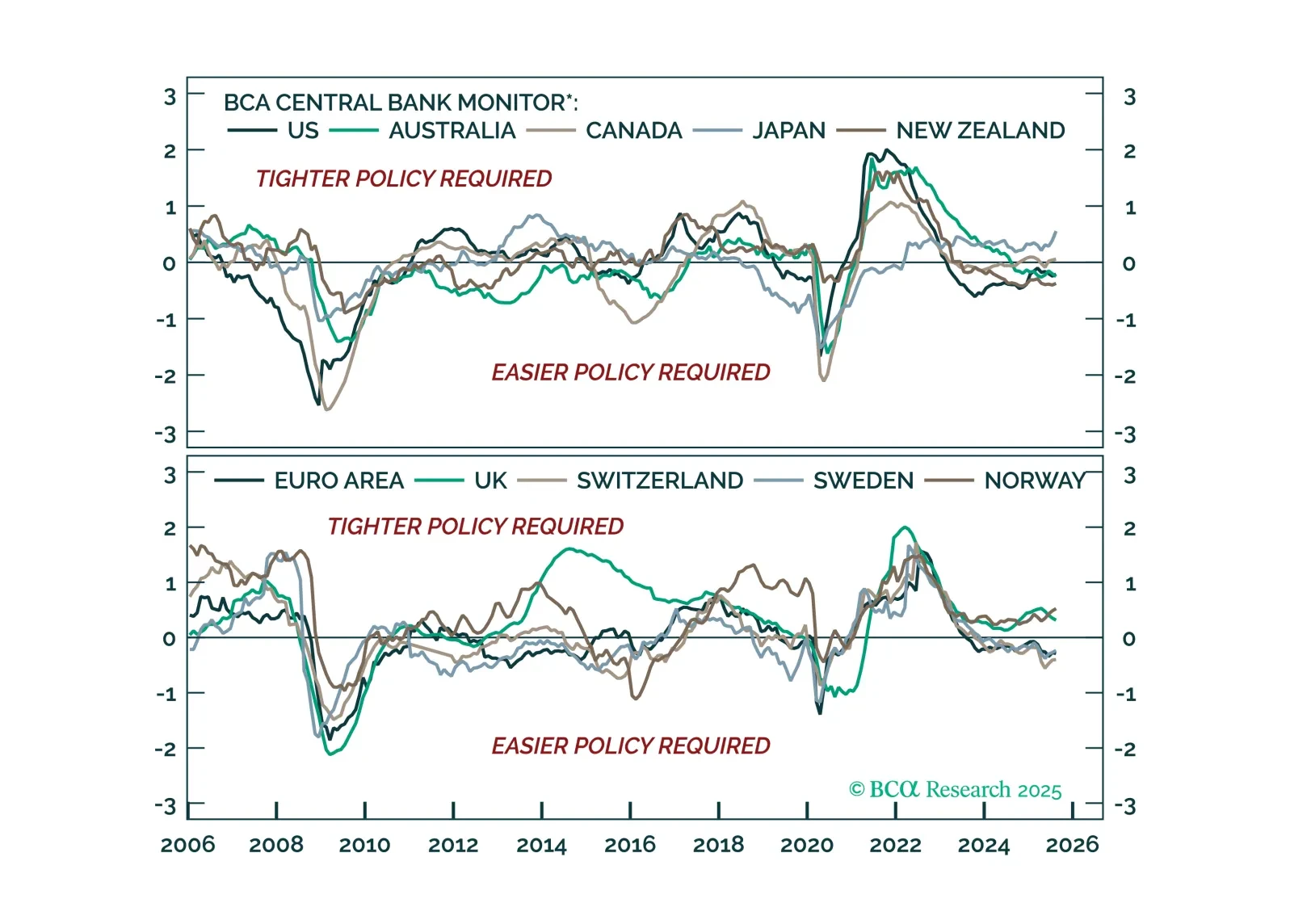

Monetary policy divergences are re-emerging. We rely on BCA’s Central Bank Monitor to assess the current policy stance of major central banks, and highlight the tactical opportunities across bond markets and currencies.

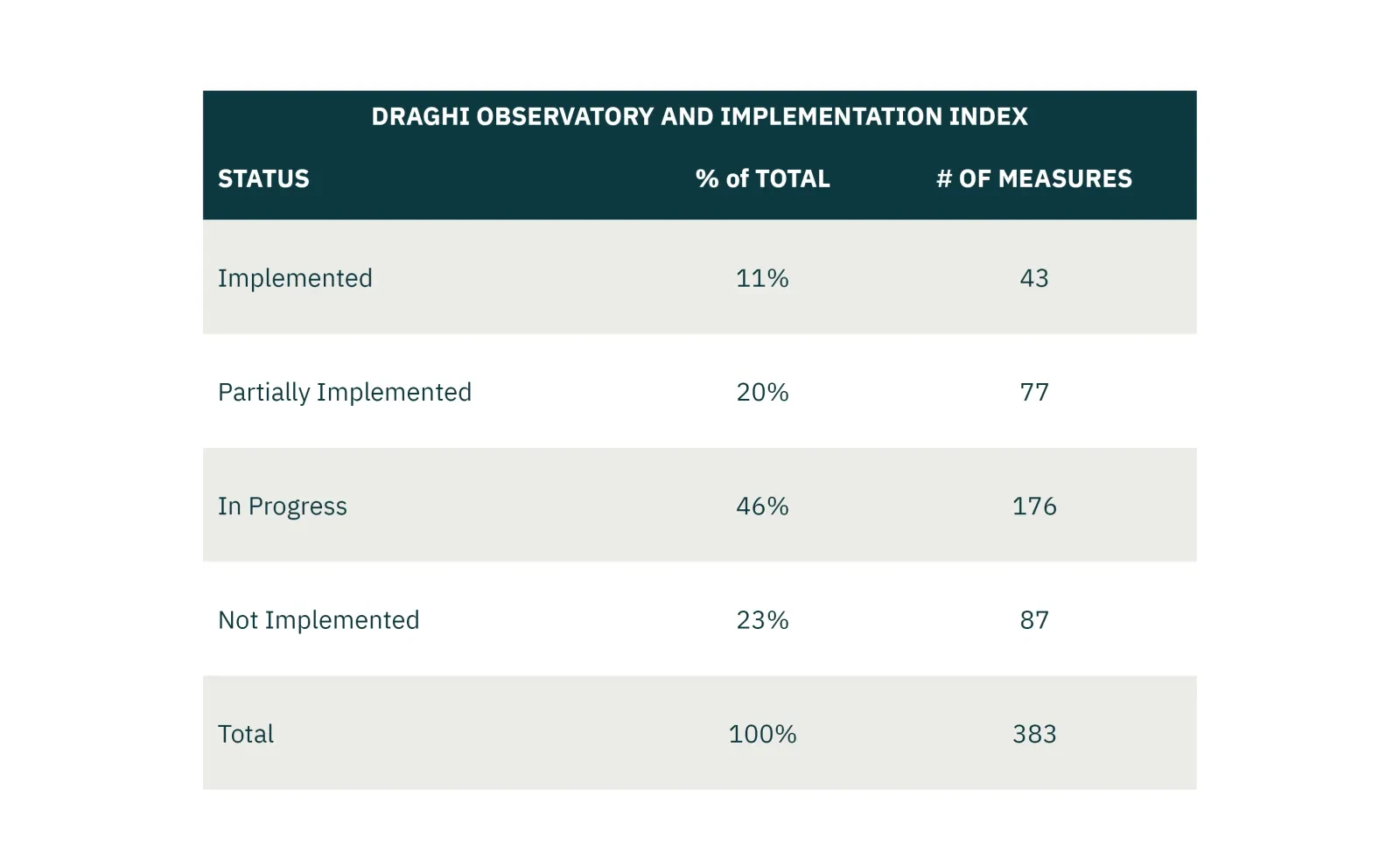

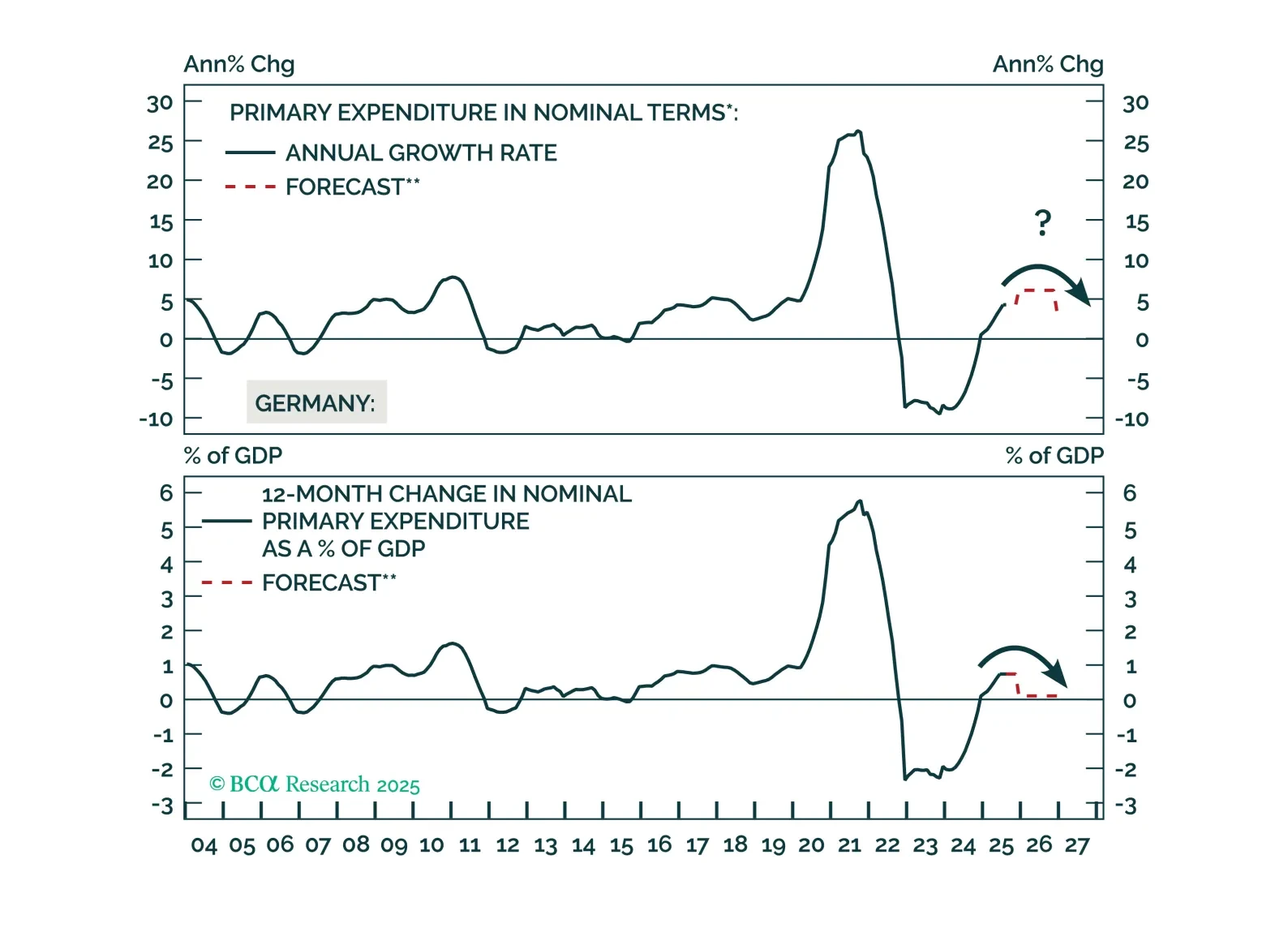

One year in, the EU is progressing slowly in implementing Mario Draghi's recommendations to restore Europe’s competitiveness. The lack of progress is due more to the various pushbacks from European capitals and the lack of proper funding than a lack of ambition. Our overall assessment remains positive, given the EU is adopting many of the priorities from Draghi’s report.

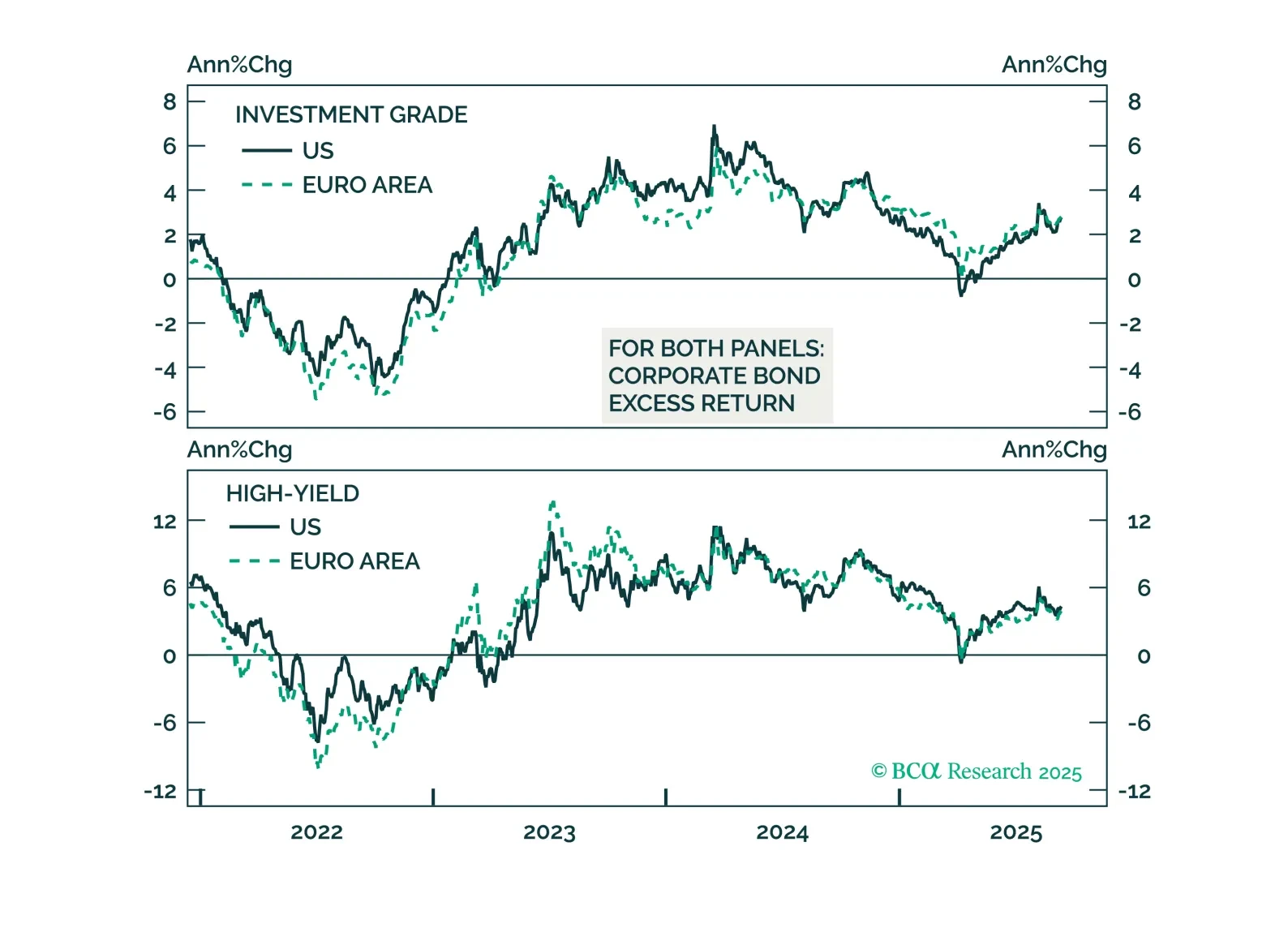

Structural tailwinds help explain tight credit spreads. In Europe, we see room for further tightening. Stay underweight US credit amid cyclical risks, but upgrade Euro Area IG to overweight and HY to neutral.

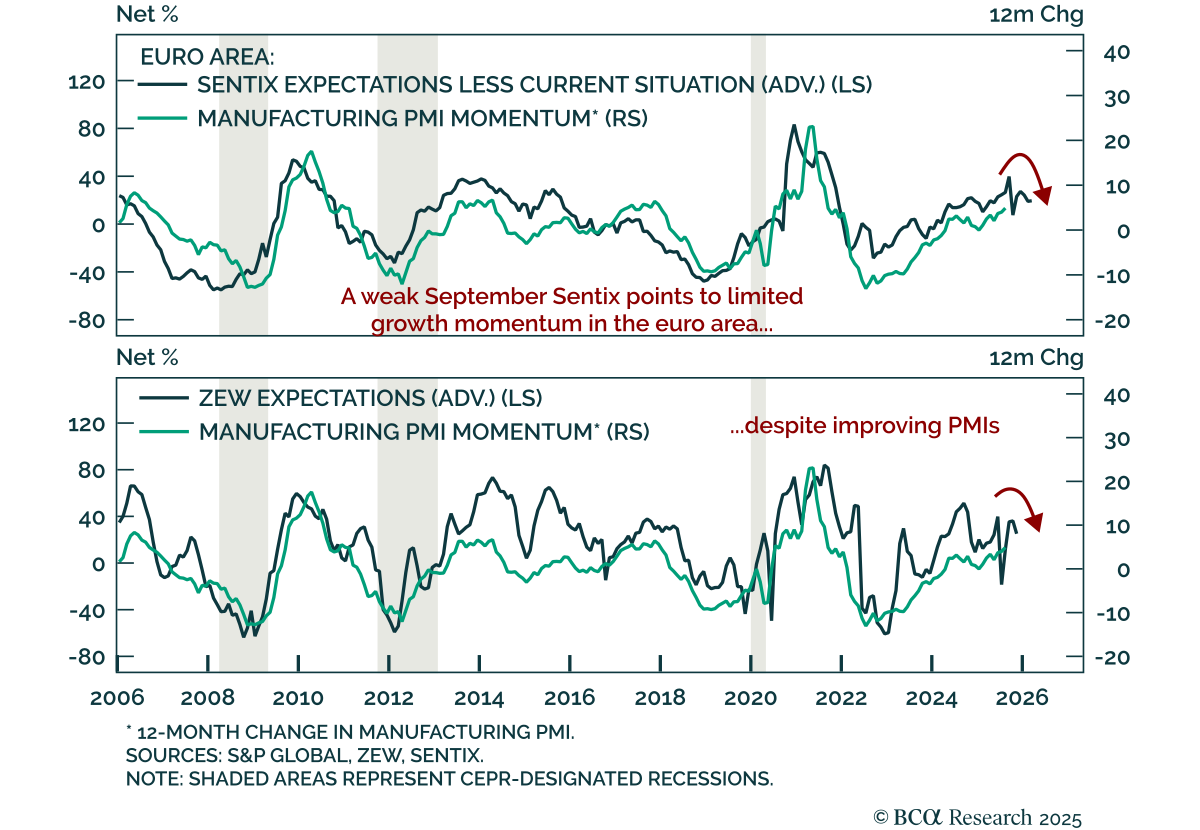

Core Europe’s industrial sector will relapse in the coming months due to US tariffs and a strong euro. Investors can play the imminent deflationary shock by being long Central European bonds. They should, however, hedge the currency risk vis-à-vis the euro.

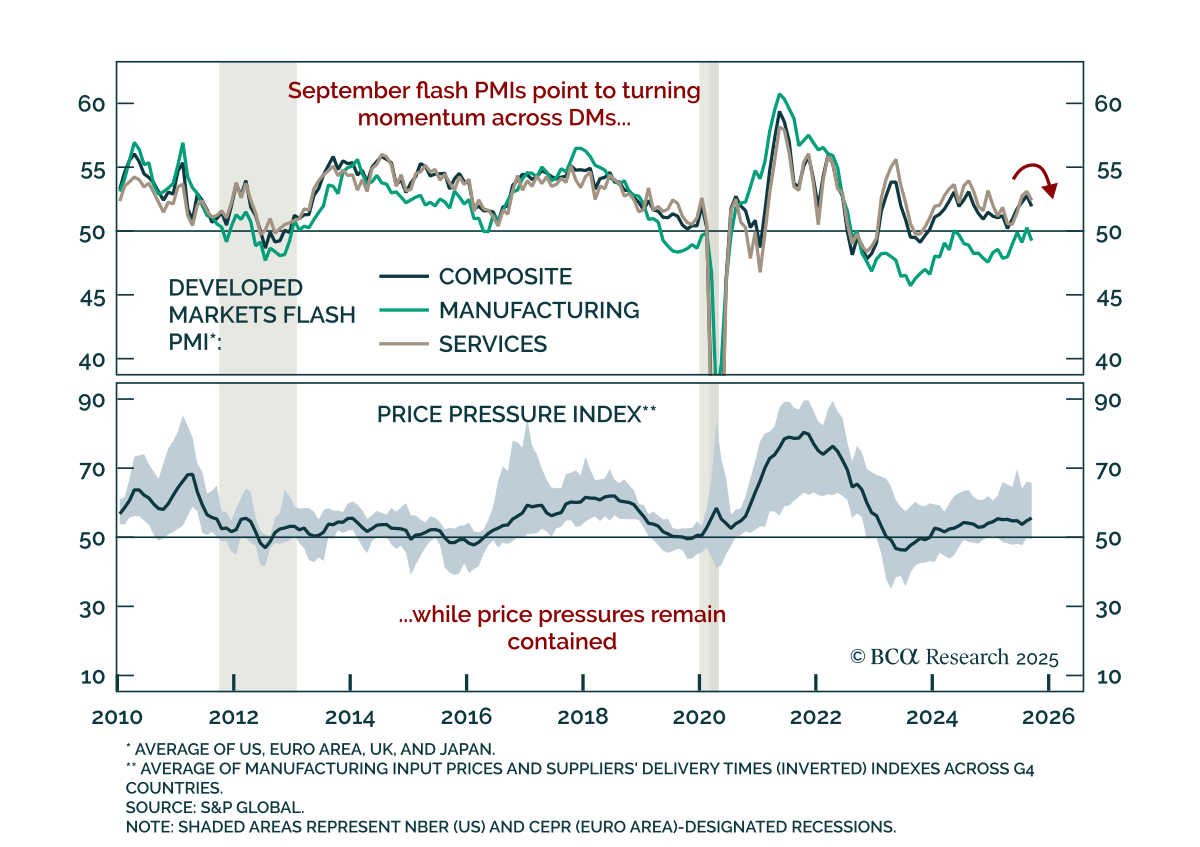

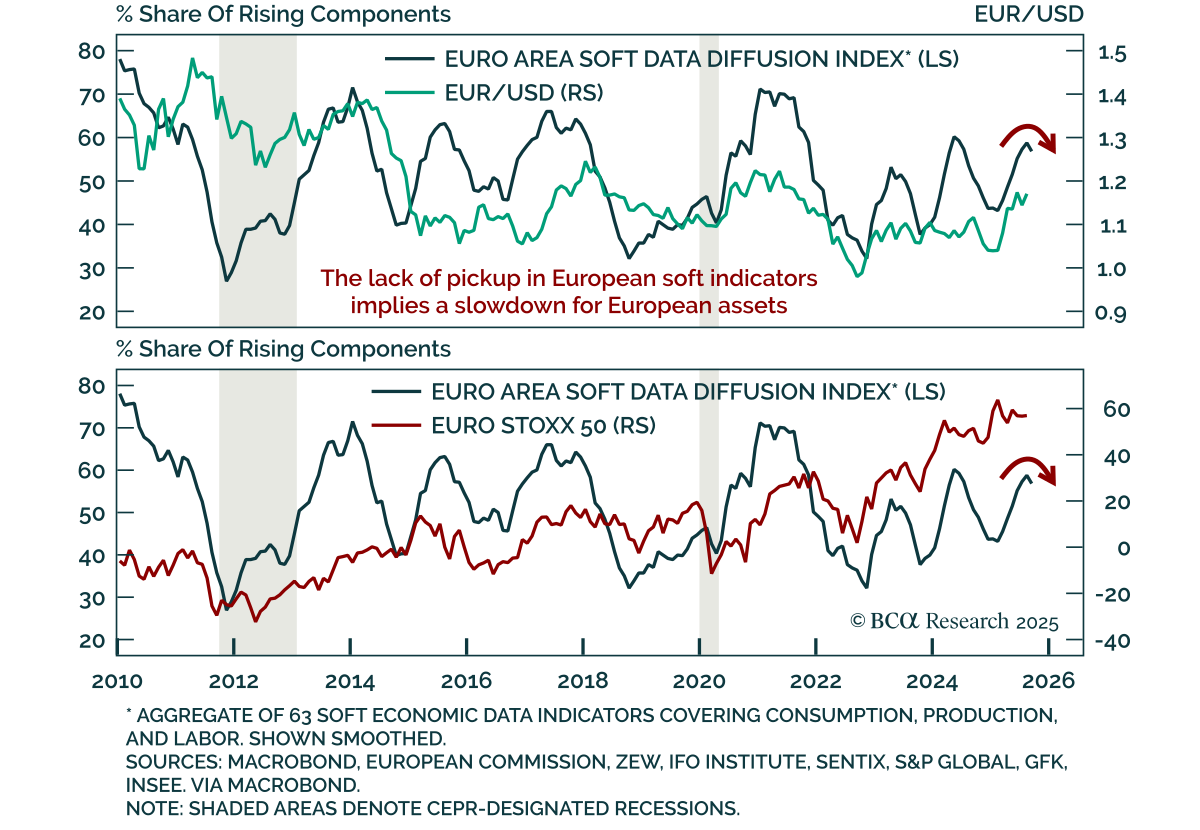

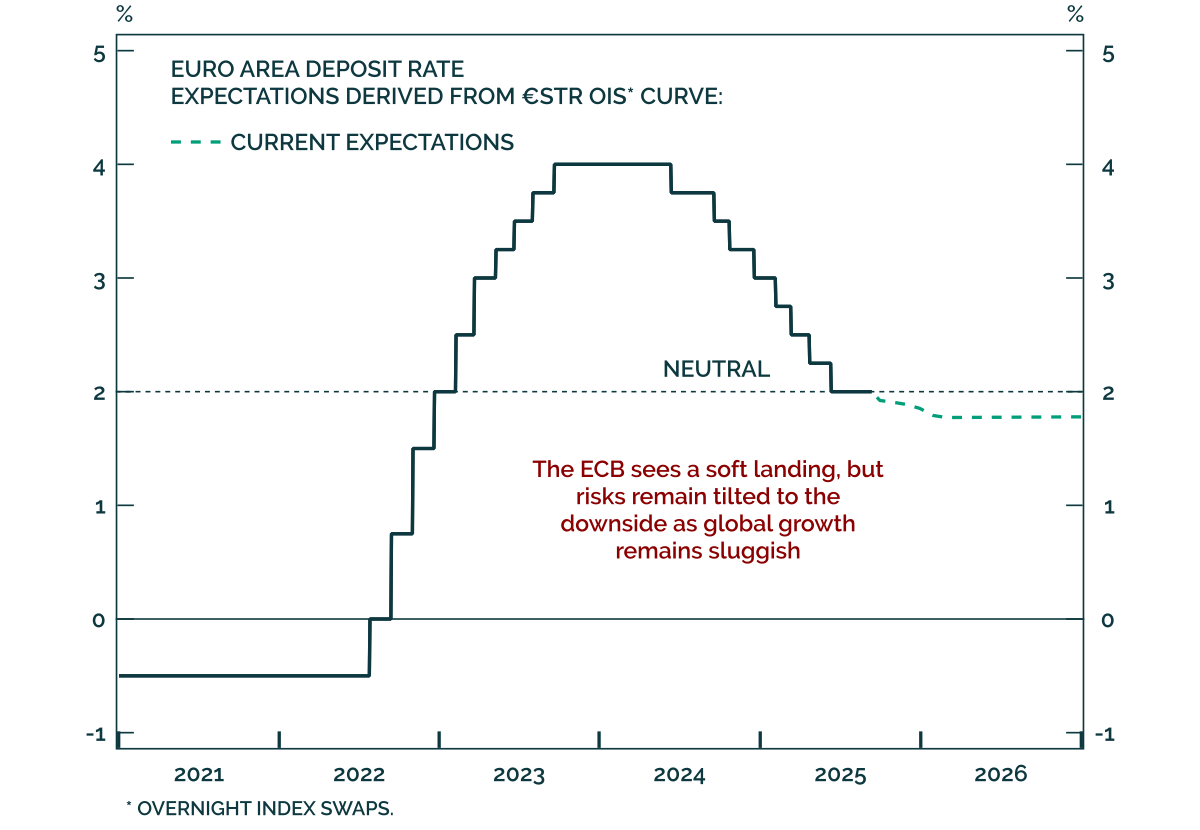

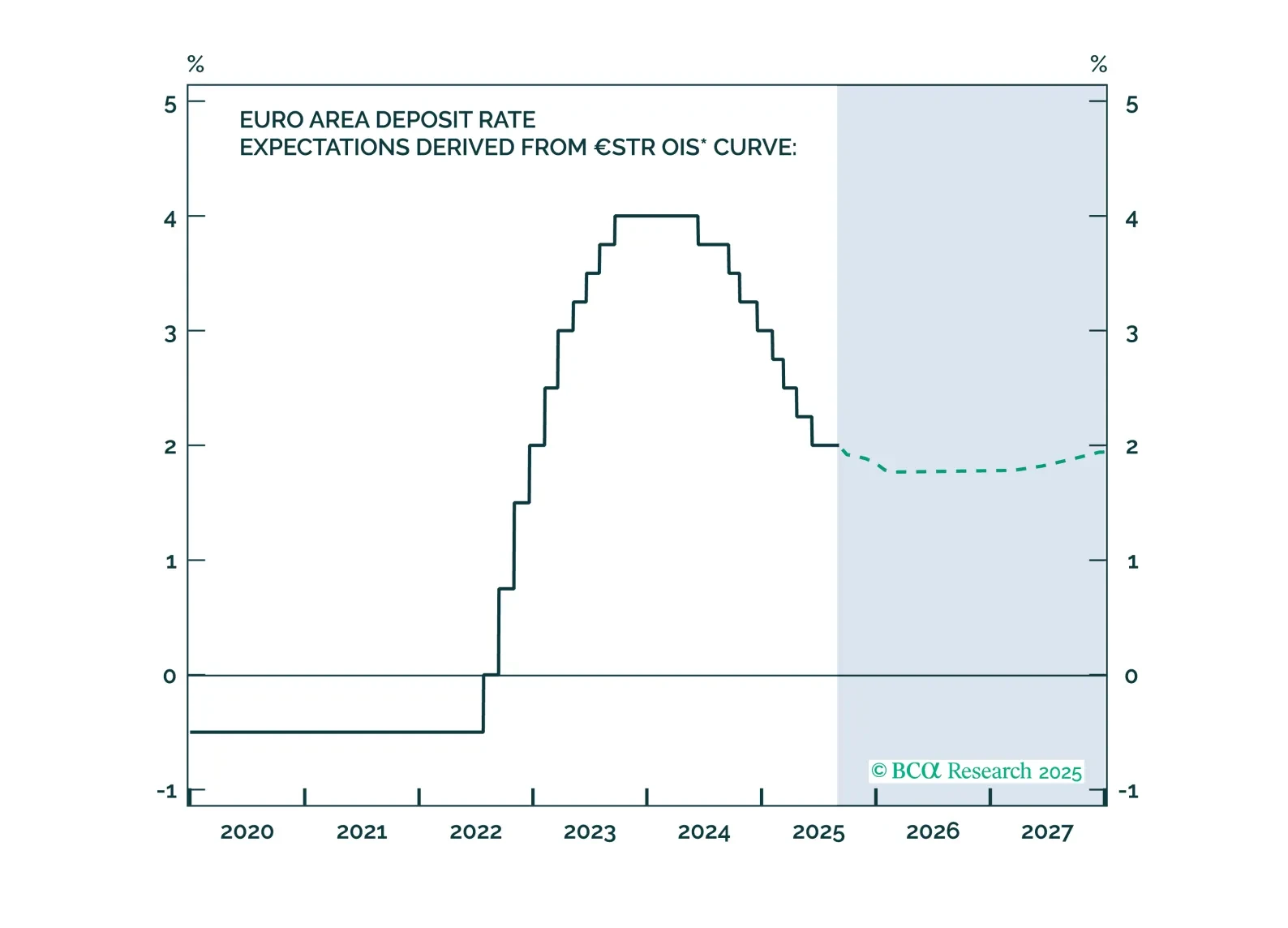

The European Central Bank has achieved a soft landing. Inflation is back to target, with well-anchored inflation expectations. The unemployment rate is historically low, and real economic growth is stable, albeit weak. Given that little to no additional easing will come from the ECB, investors should underweight government bonds relative to equities.