Euro Area

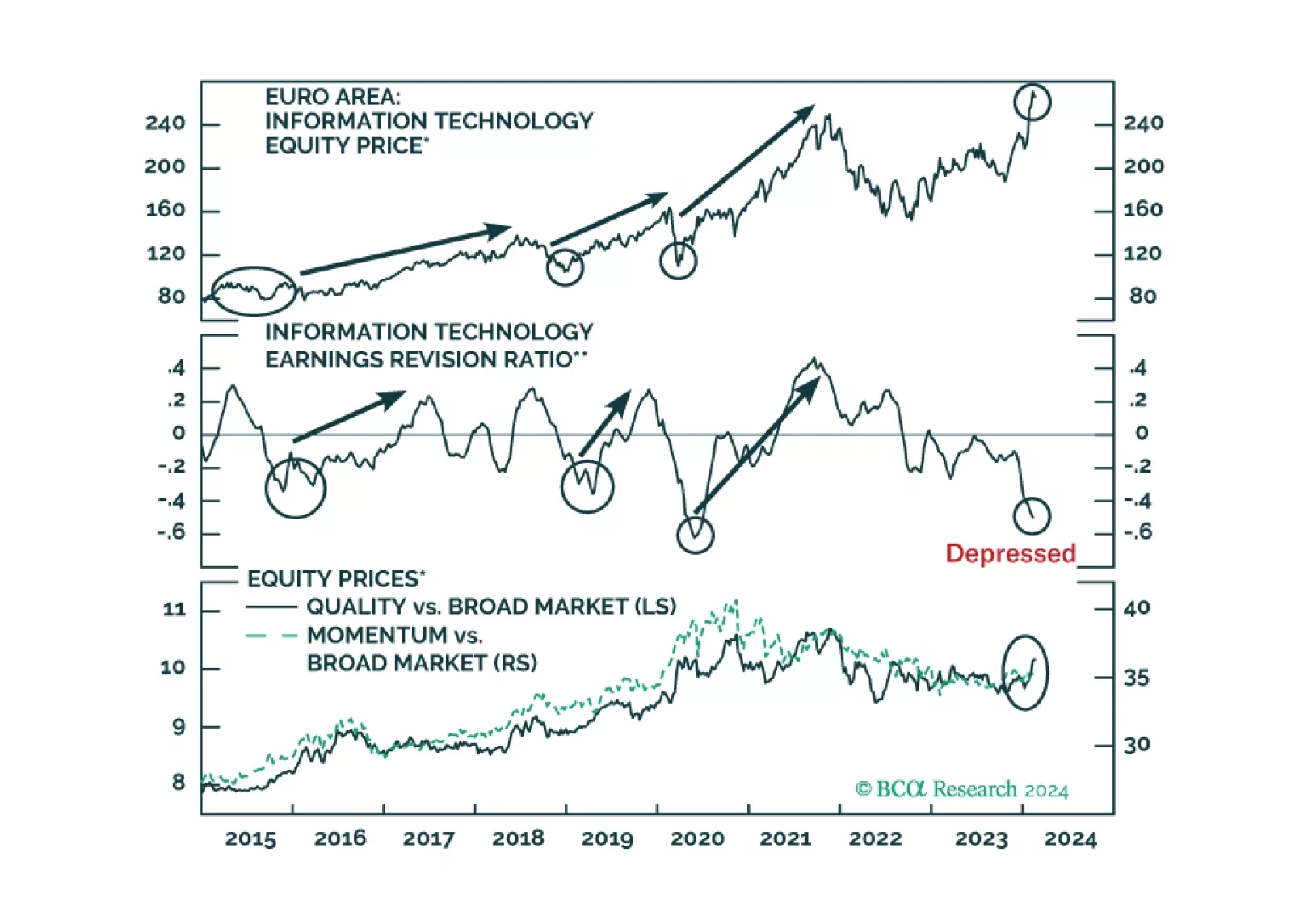

Signs that we are entering the last phase of a bubble are building up. Can European equities benefit from a new tech mania?

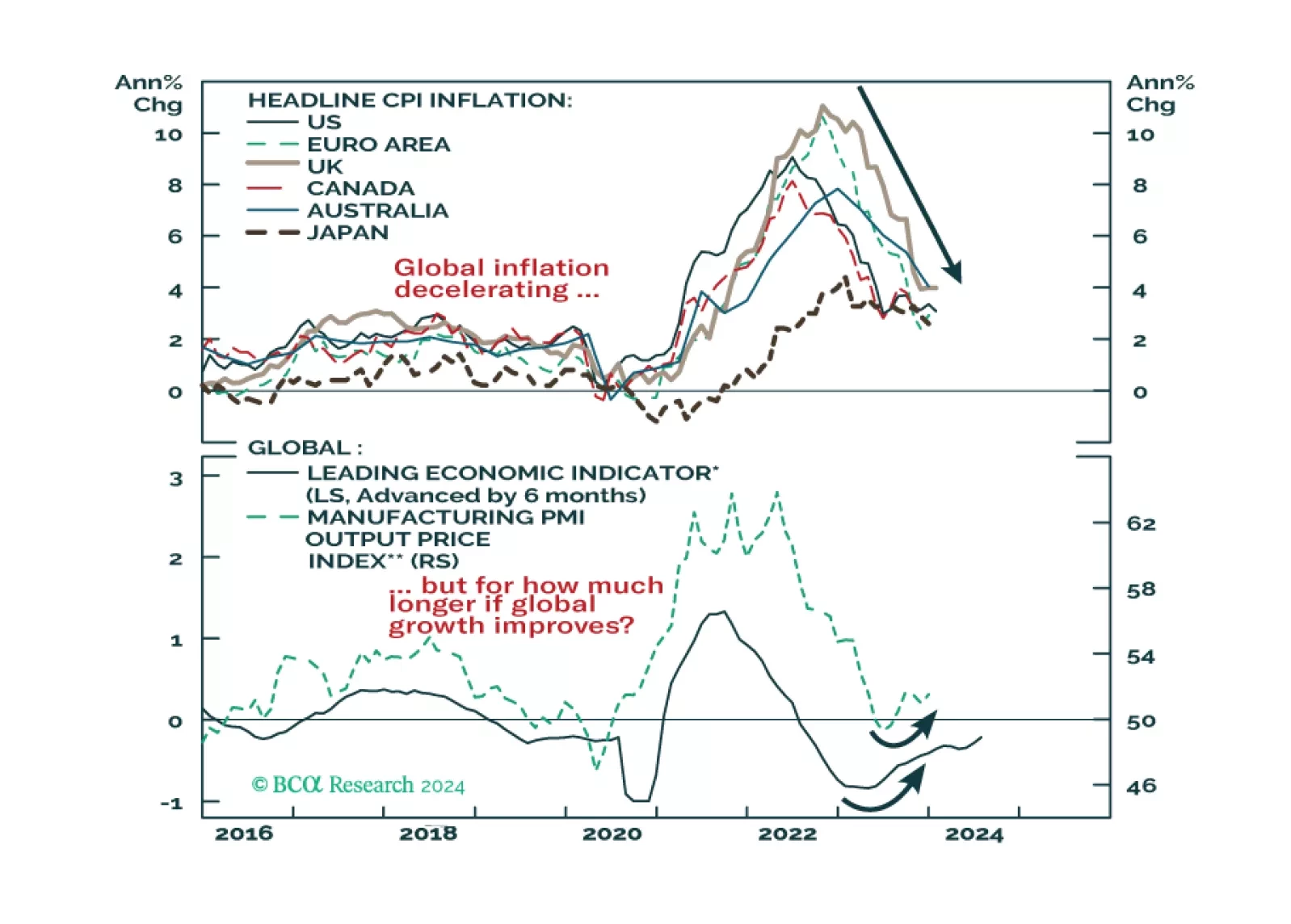

Could a second wave of global inflation be underway? The latest inflation prints in the US and UK showed upside surprises, while there is evidence of increased price pressures in global manufacturing. Combined with the improvements seen in economic sentiment measures and leading economic indicators in the US and Europe, and potential upside risks to oil prices, we see a strong case for owning more inflation protection in global bond portfolios. Inflation-linked bonds look attractive in this environment, especially in the US.

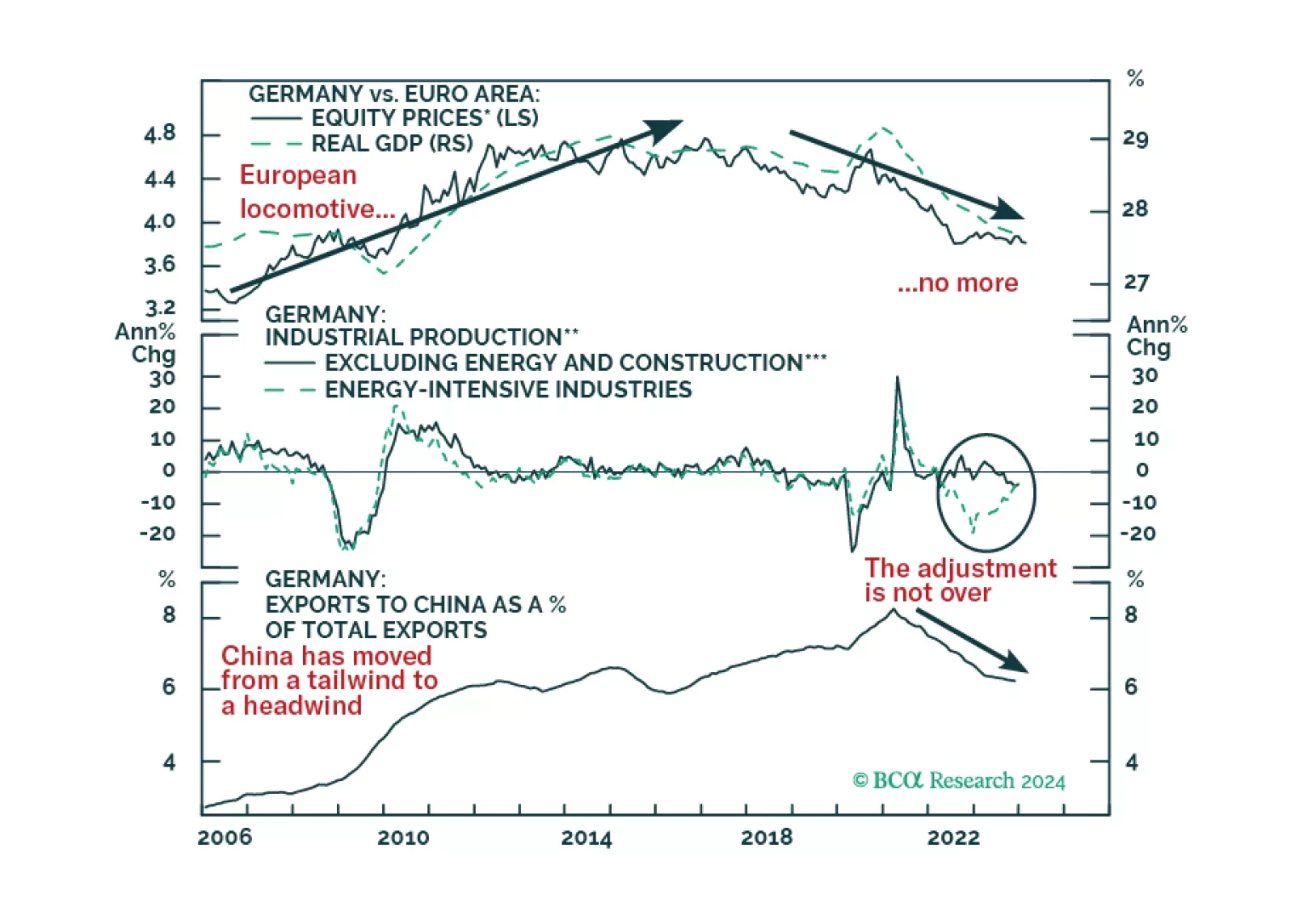

The German economy has lagged that of Europe. This trend will continue, but does it mean German equities will underperform further?

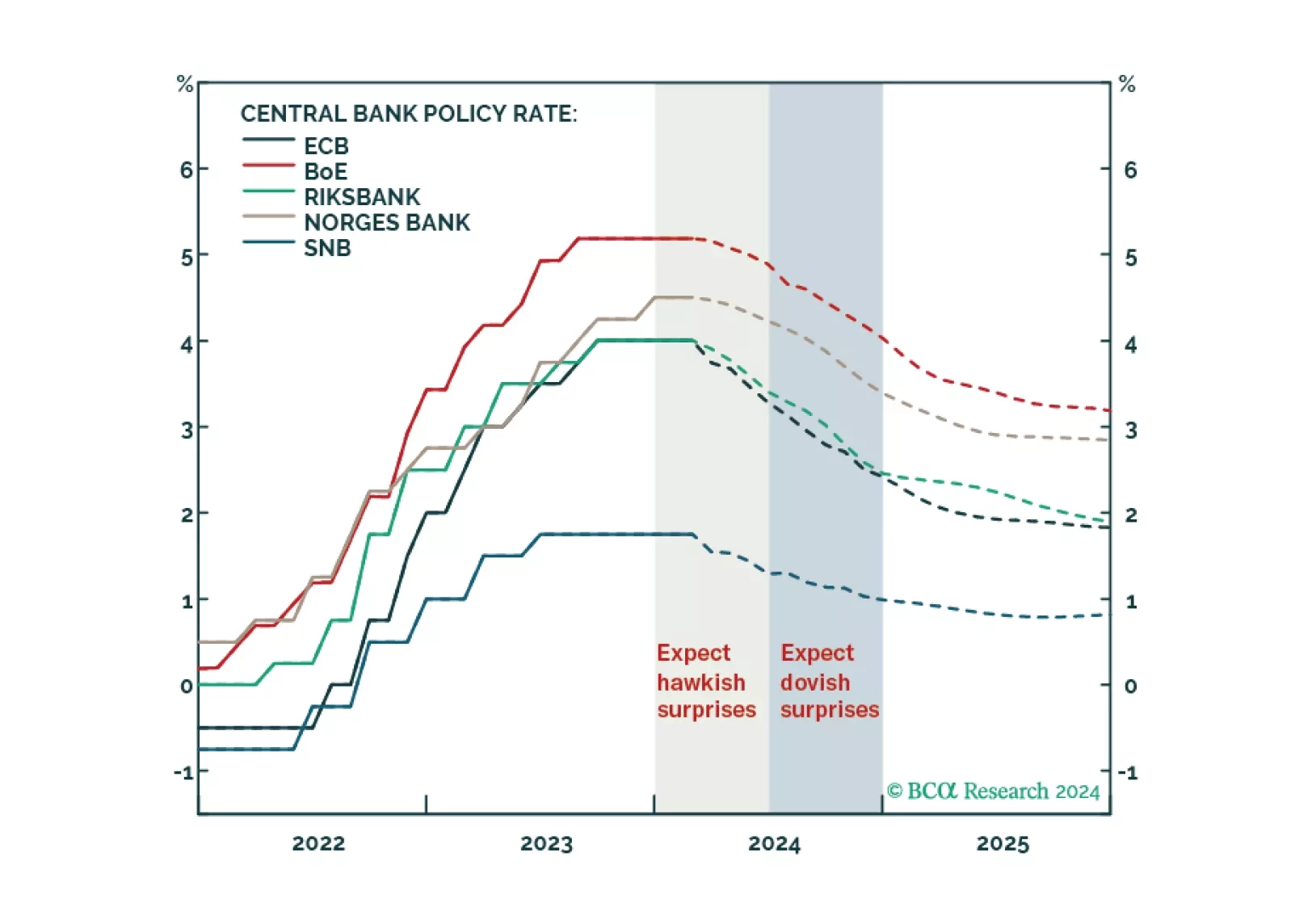

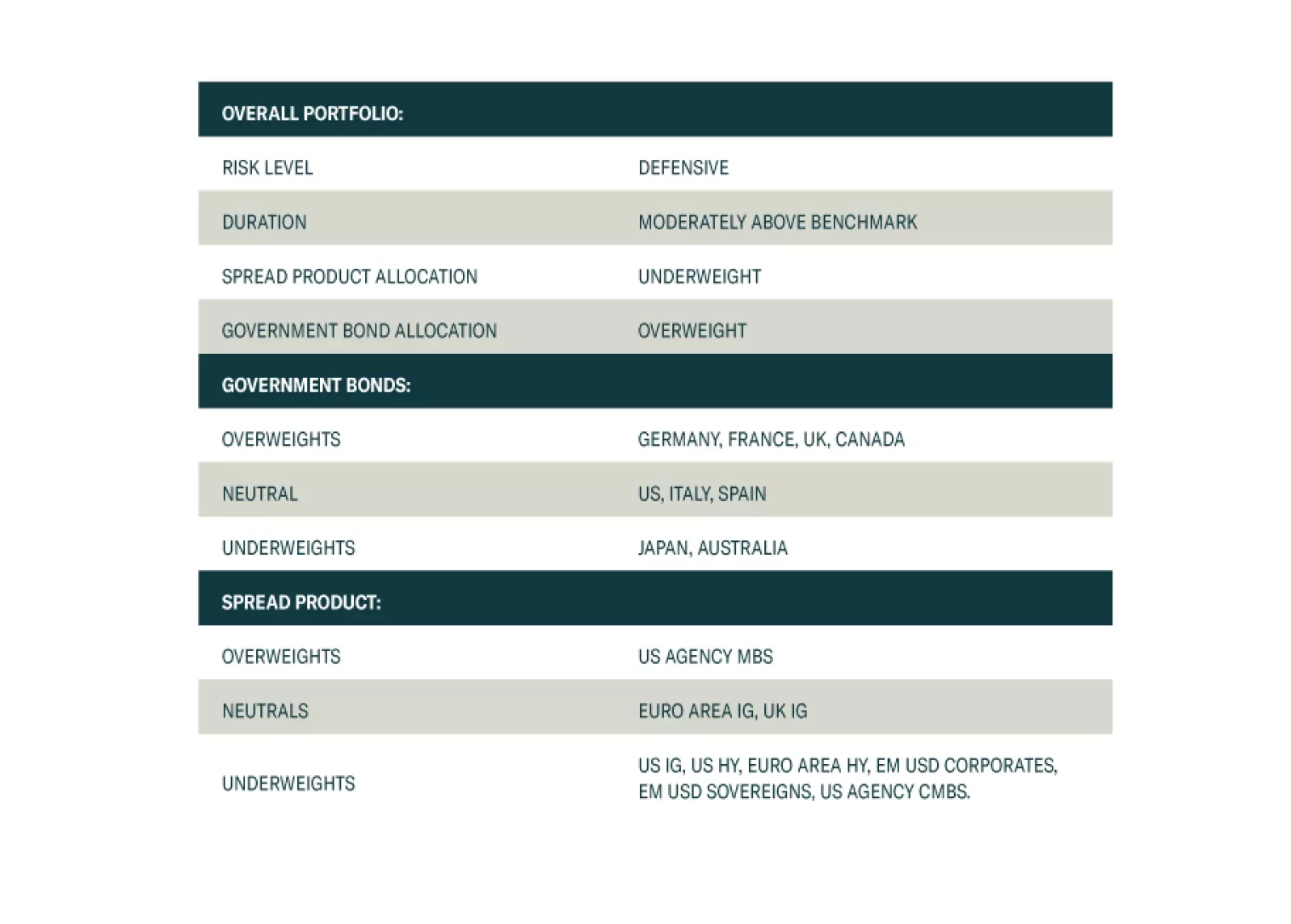

Our Central Bank Monitors support European central bankers’ decision to hold rates steady. Find out what it means for European fixed-income portfolio allocation.

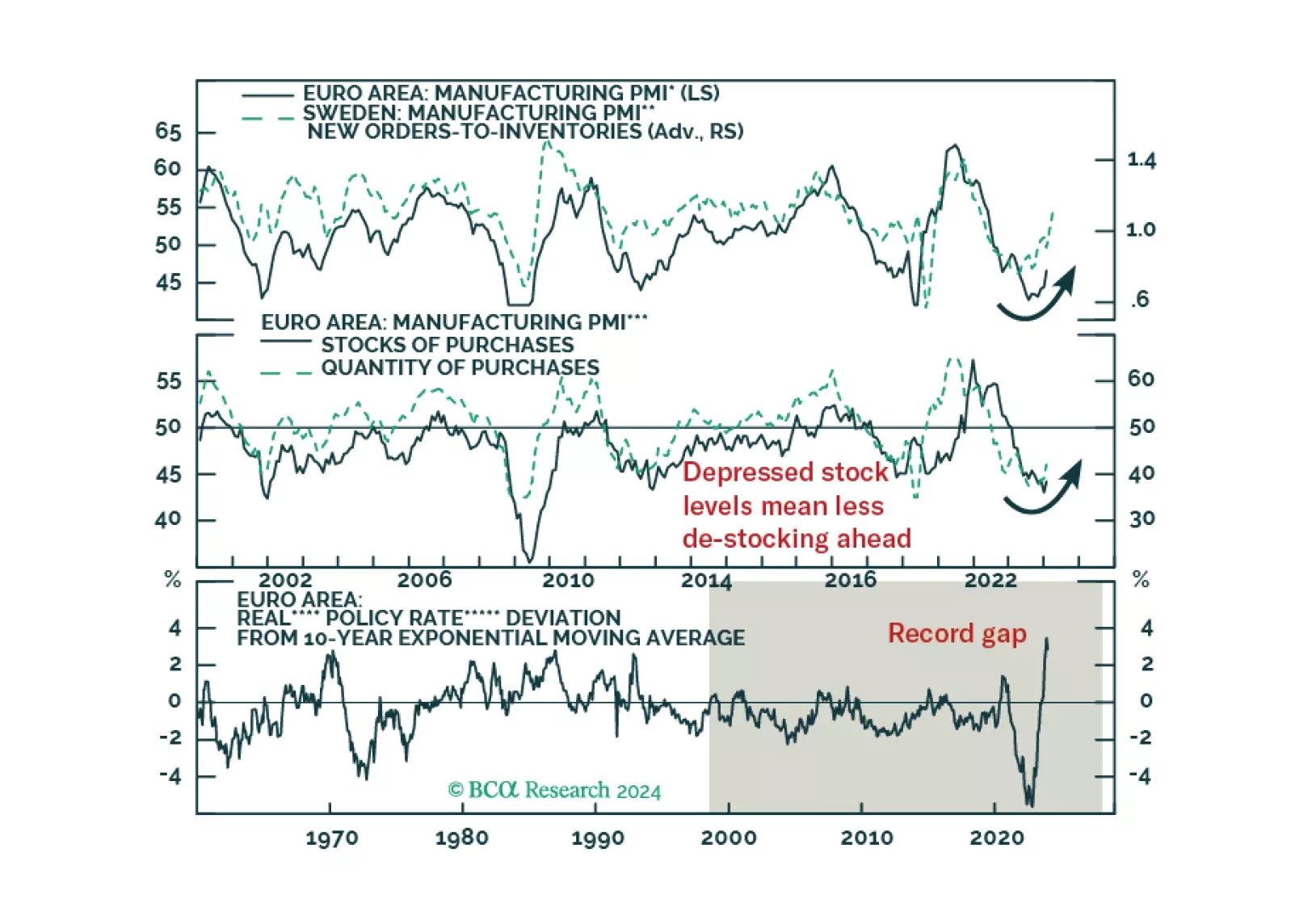

Is the rebound in European PMIs enough to boost the appeal of European risk assets?

We present the performance review of the Global Fixed Income Strategy Model Bond Portfolio for 2023. We also discuss the outlook for 2024 performance based on our Key Views for the year. The portfolio is positioned to benefit from a year where the global backdrop will be one of weak growth and further declines in inflation, leading central bank to begin cutting interest rates.