Equities

Over the last weeks, US semiconductor stocks have plunged by over 17%. In a way, this correction should be expected. Semiconductor stocks had skyrocketed this year. Even after the recent pullback, semi stocks are still up over 20%…

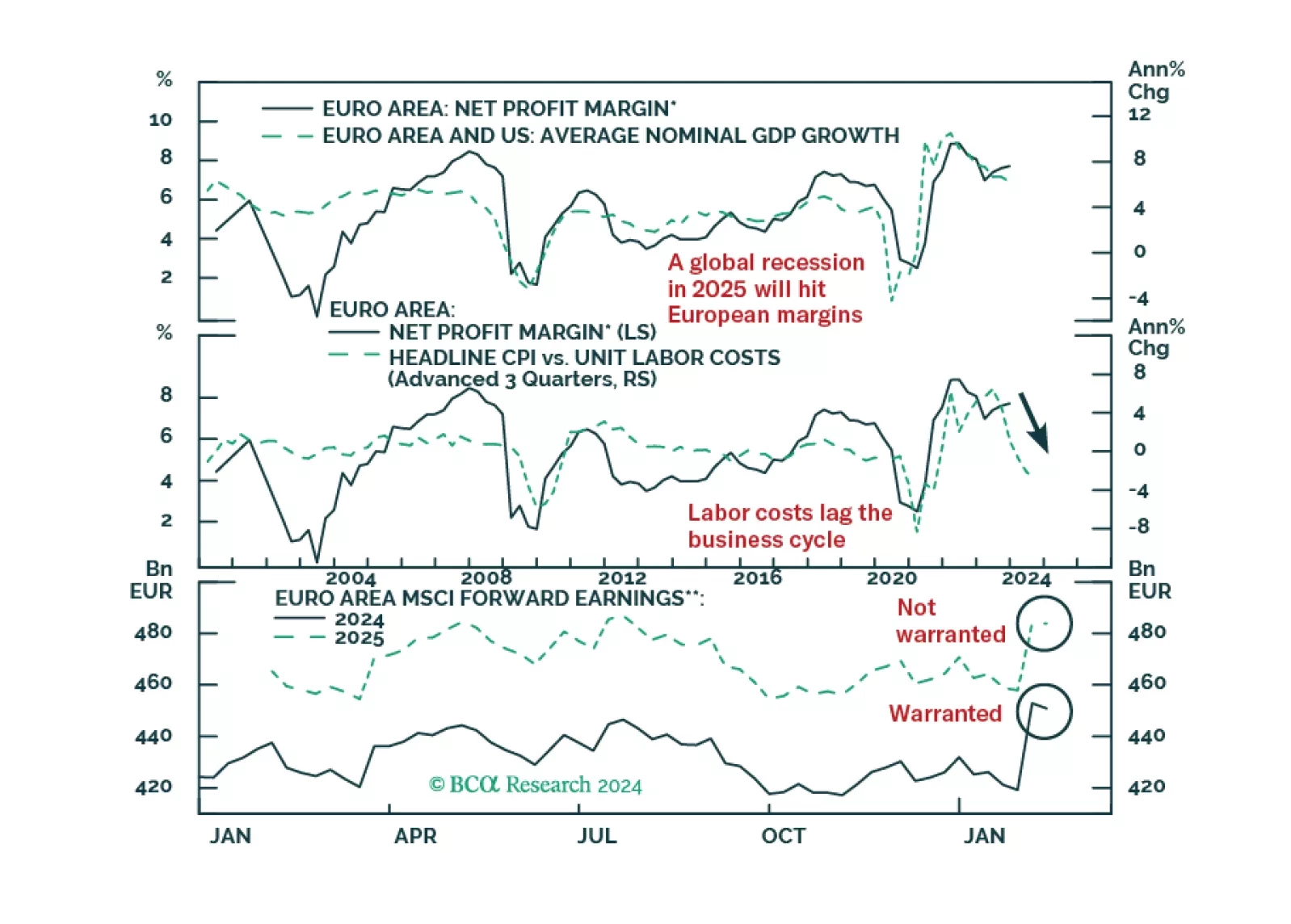

According to BCA Research's European Investment Strategy service, European profit margins have downside because they are both elevated and procyclical. European net margins stand at 7.7% above their long-term average of 5%. Analyst expectations…

European profits margins are elevated. Will a mild recession be enough to bring them down?

BCA’s US Beige Book Monitor – an indicator we use to gauge changes in the language of the Fed’s Beige Book report and which historically tracks US GDP growth – has improved in April. Nevertheless — and despite March's hot retail sales and February's…

The headline Philadelphia Fed manufacturing survey for April delivered a positive surprise on Thursday, increasing from 3.2 to a twelve-month high of 15.5 and beating expectations it would soften to 2.0. Measures of demand improved with new orders and…

The equity risk premium – calculated as the 12-month forward earnings yield minus the 10-year real rate – continues to drop both for US and global stocks, standing at 2.7% and 3.7% respectively. The compression of the equity risk premium has been the result…

Nvidia has amassed staggering sales from AI. Last year its data center revenues exploded, going from just over $4 billion in 2023 Q1, to over $18 billion in 2023 Q4. That said, its competitors have not done as well. In the same time frame that Nvidia added…

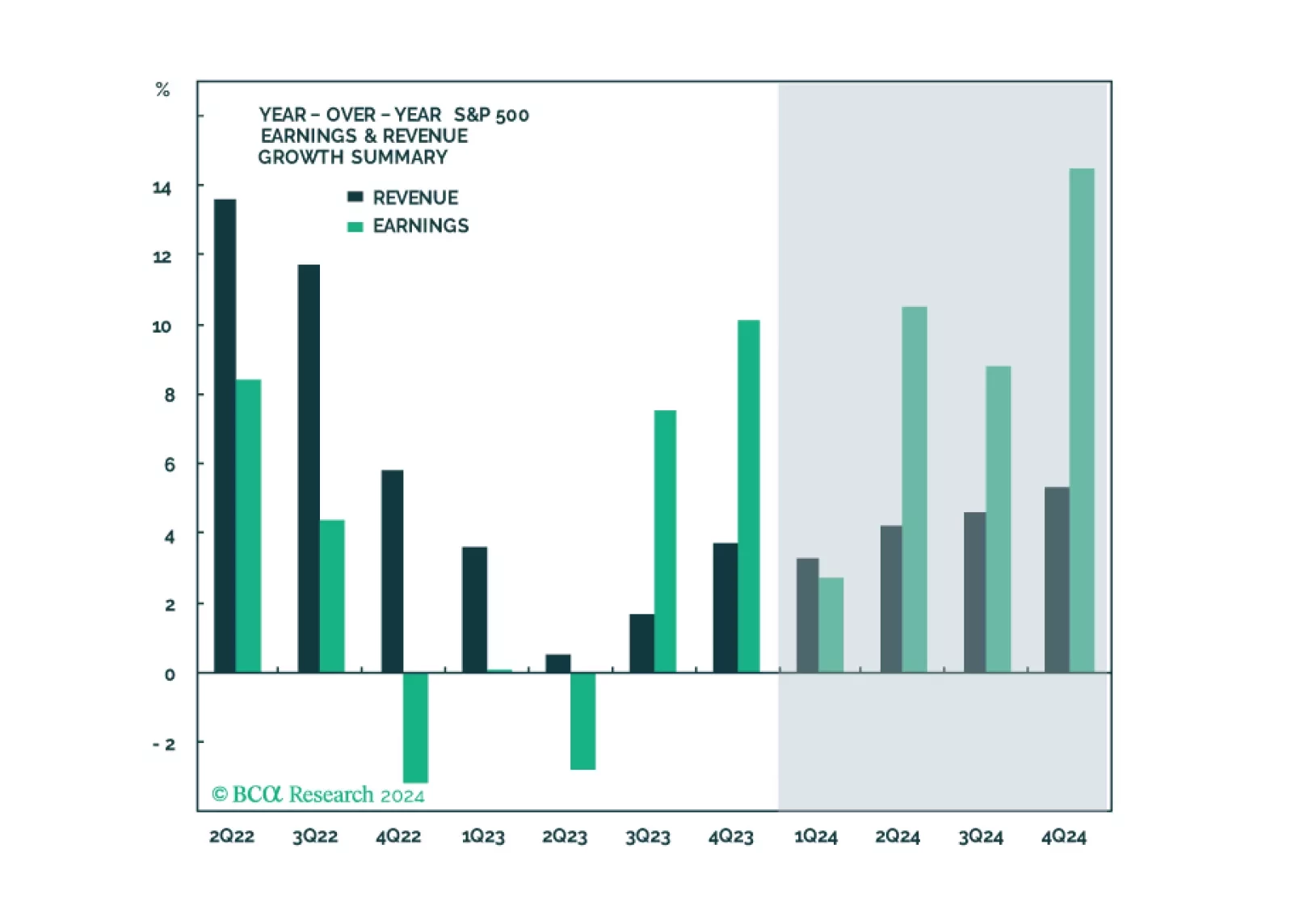

BCA Research’s US Equity Strategy service provides its take on US Q1-24 earnings expectations. Room for surprise? Positive earnings surprises have been a fixture of nearly every earnings season since the darkest days of the pandemic. This quarter will…

The US Energy sector has shifted from a capex and growth obsessed industry to one that is more focused on shareholder returns. ESG as well as the collapse in oil prices during the 2010s were the main culprits. Divesture due to ESG mandates on portfolios…

In this note, we preview the Q1-2024 earnings season, give our take on expectations and share what we will be watching.