Equities

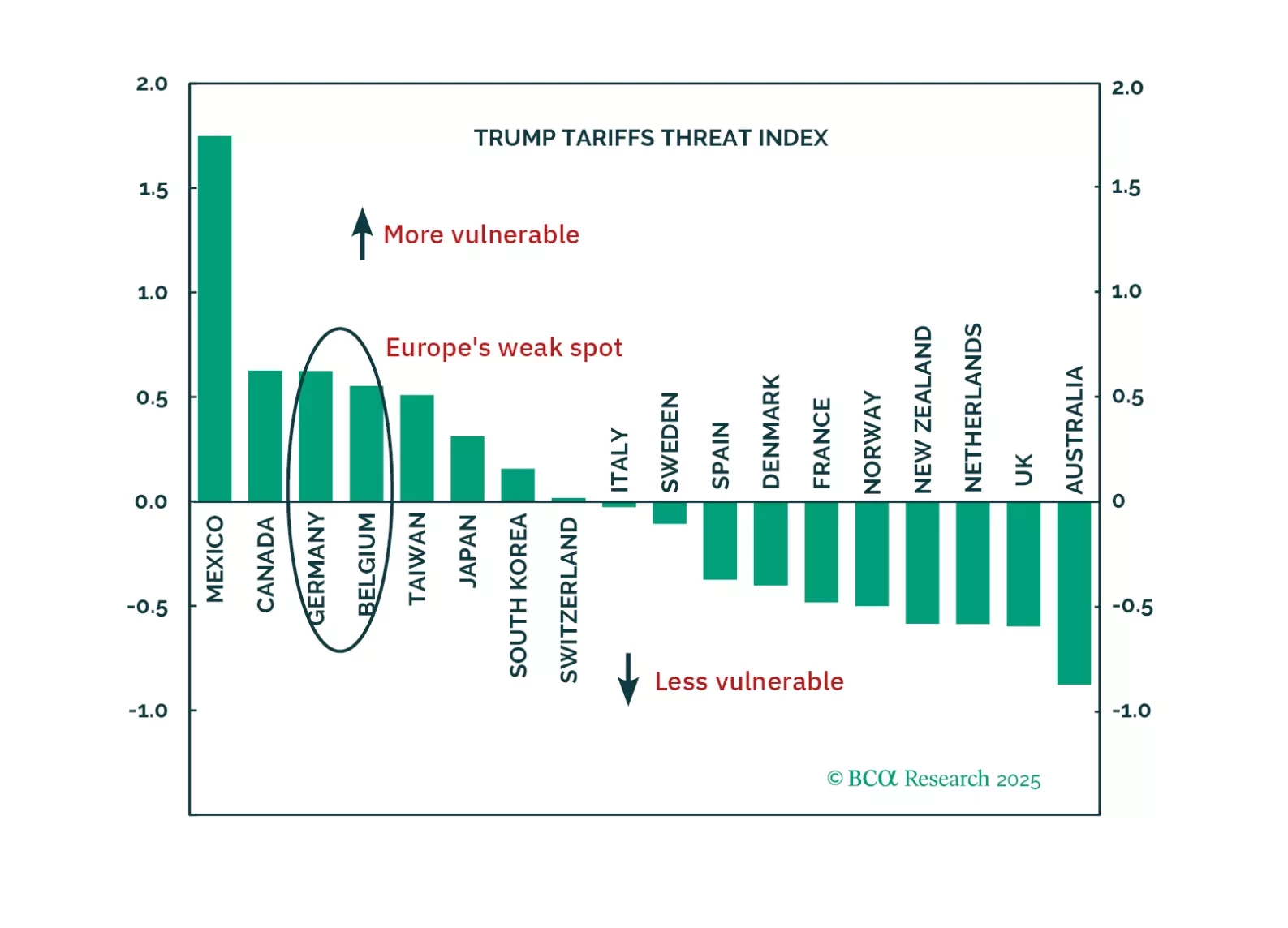

President Trump is about to be inaugurated. Investors often assume all his policies will hurt Europe, but the reality is more nuanced.

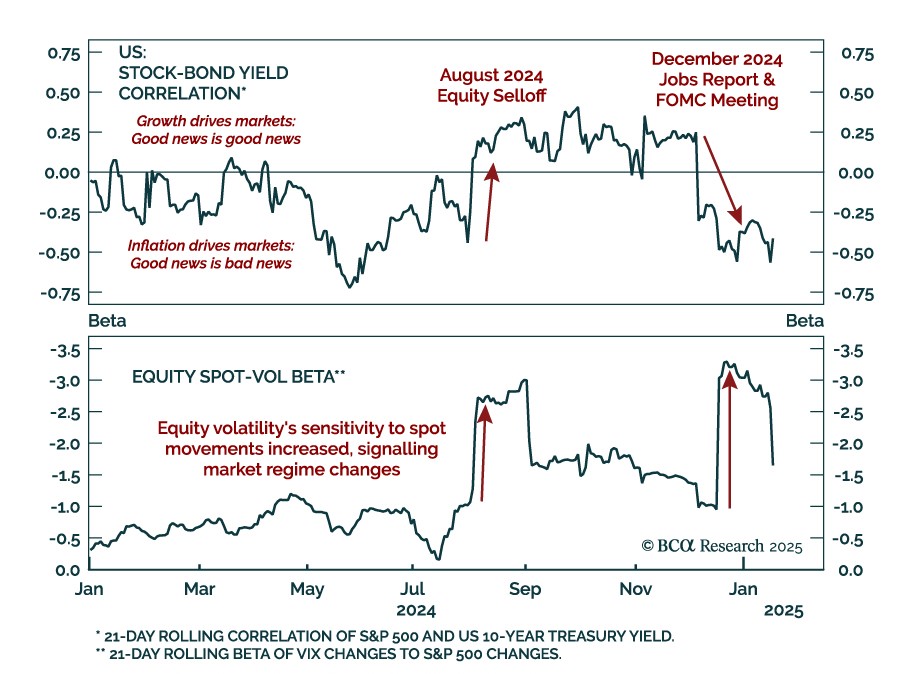

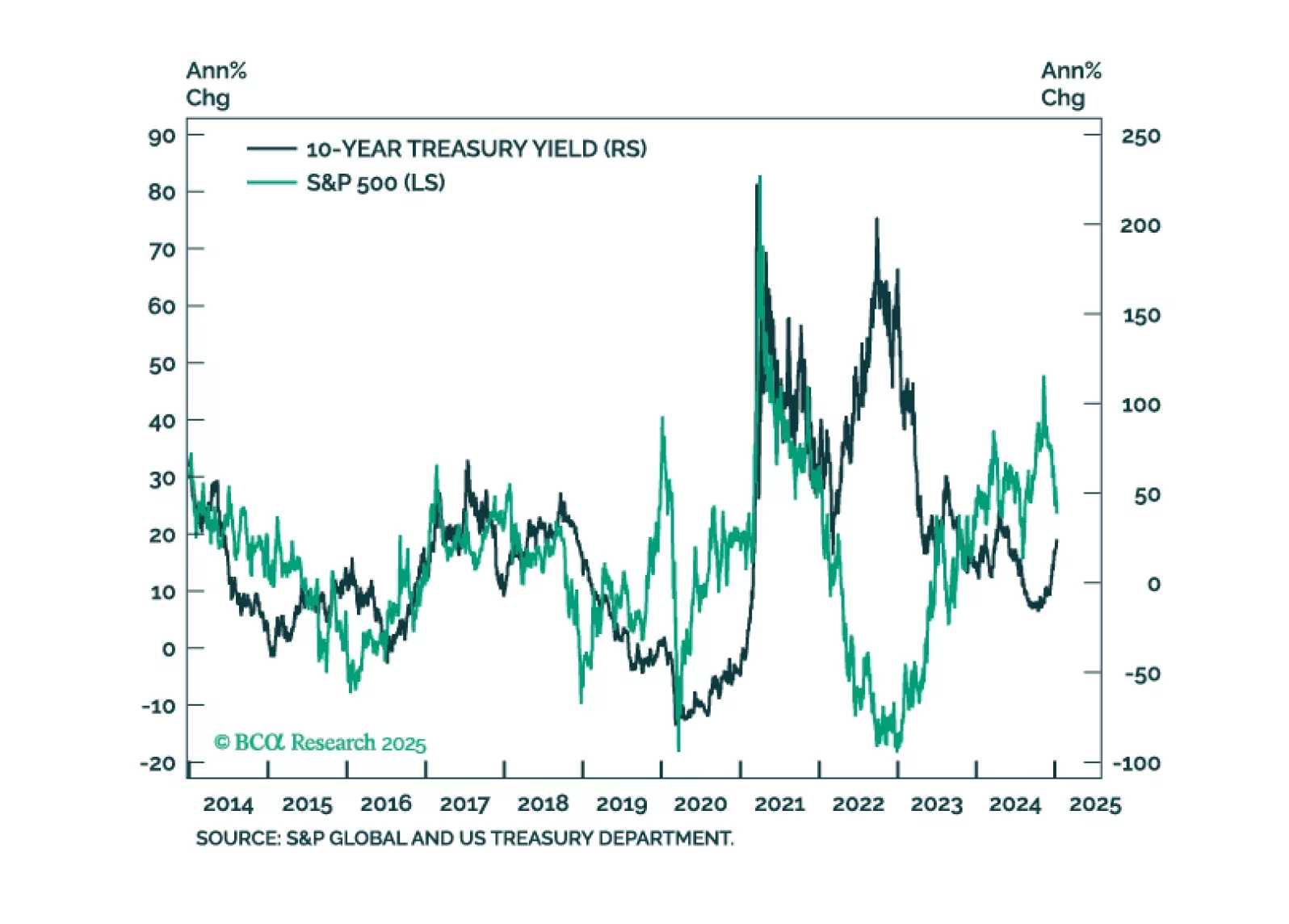

In this first presentation of 2025, we start with an overview of the 2025 outlook webcast polls, and a brief post-mortem of the 2024 market performance. Then, we shift gears and examine what is behind the recent surge in bond yields and its implications for equities. We also review market technicals and positioning and conclude with a list of trades to prepare our portfolio for continued moves in yields.

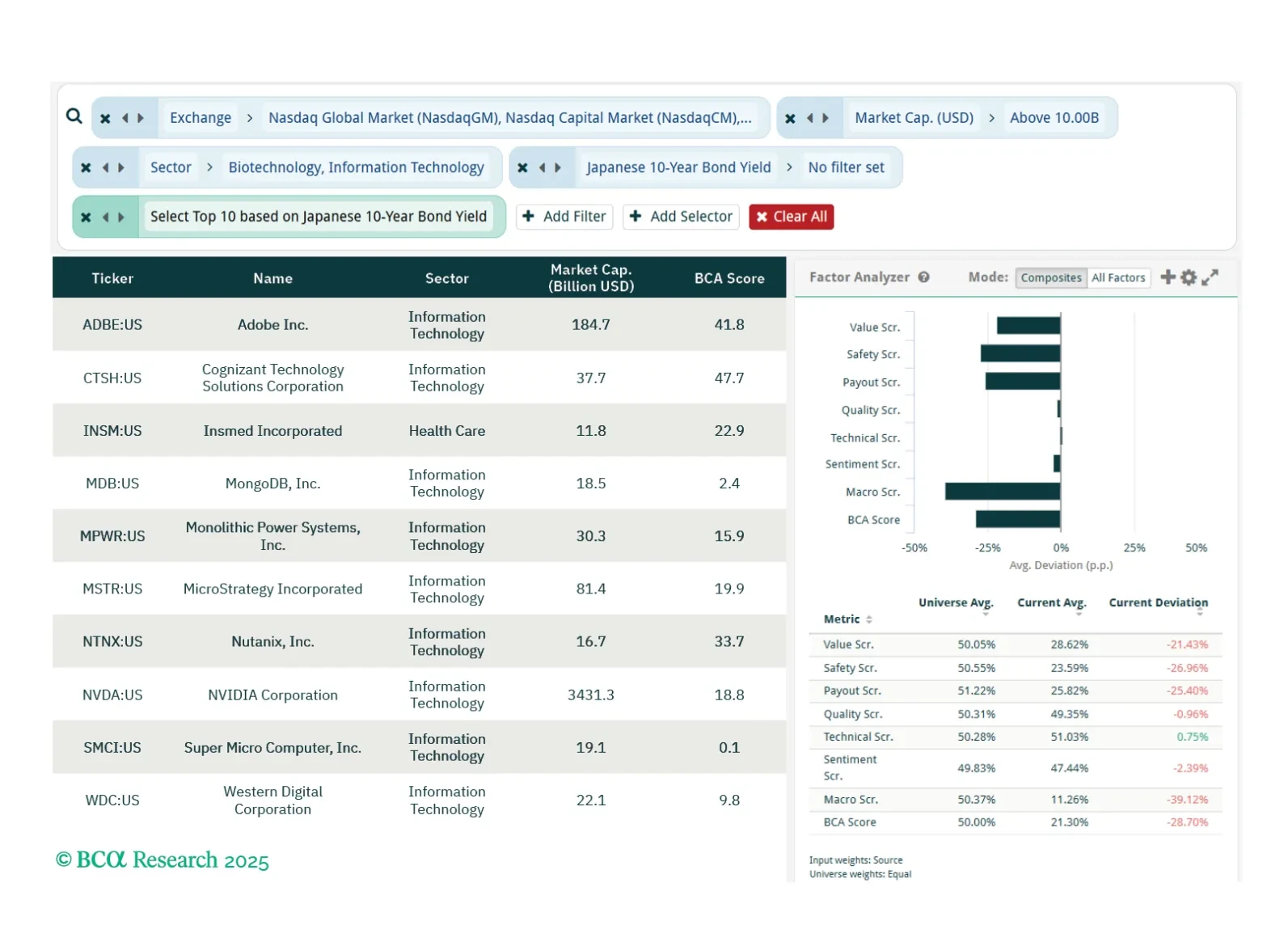

To kick start our new research agenda at Equity Analyzer, we welcome you to our weekly screener report. Each week we will deliver three screeners highlighting stocks exposed to various macro and investment views and themes, that have either been suggested by various BCA strategies, such as the Global Investment Strategy, or are based on research by the Equity Analyzer team. In our first installment, we take a look at US Tech stocks, equity sentiment, and quality "bubble" stocks.

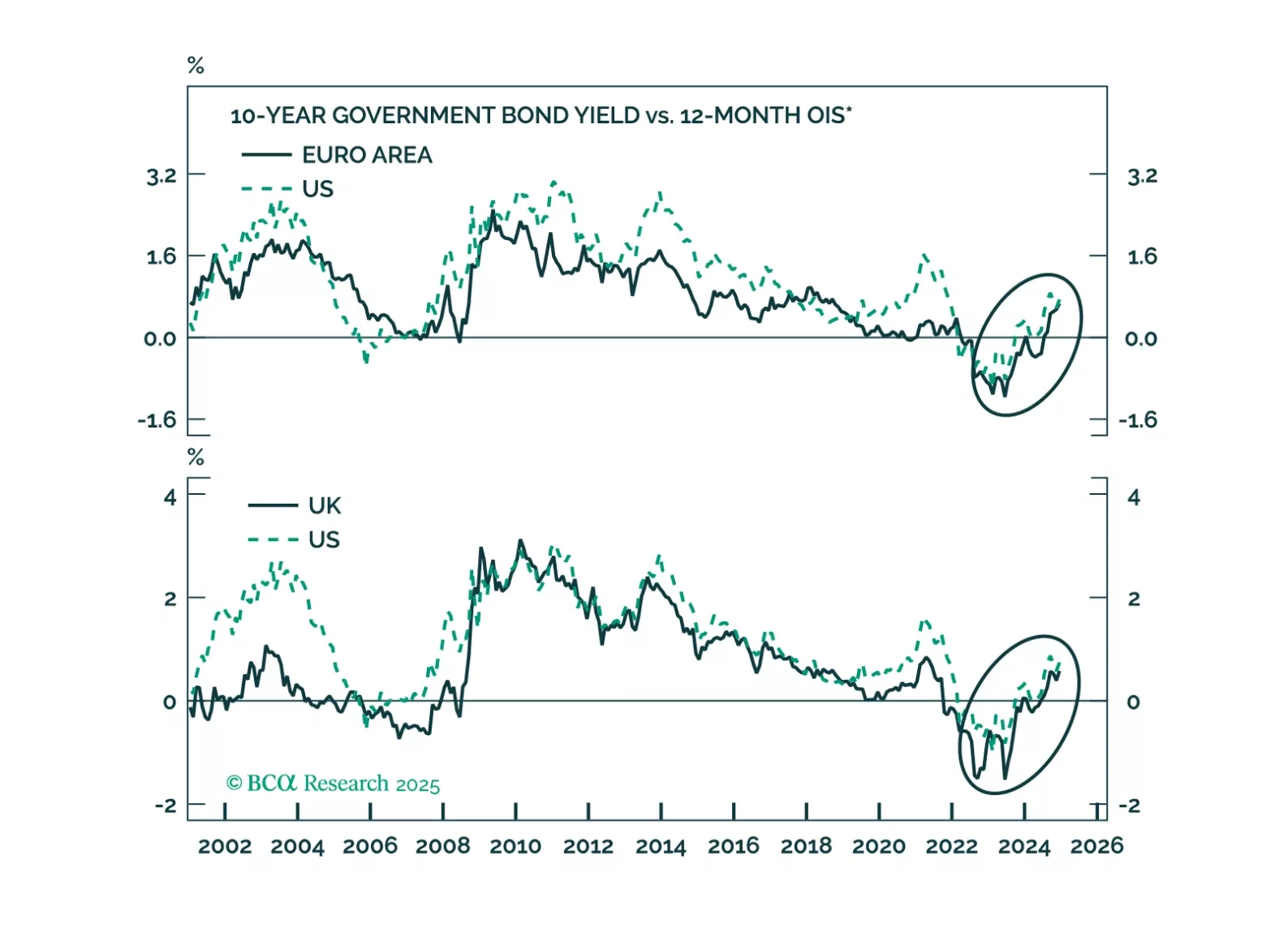

UK and German bonds are victims of the global bond market riots. Will European yields continue to move higher and will the euro and the pound find a floor anytime soon?