Equities

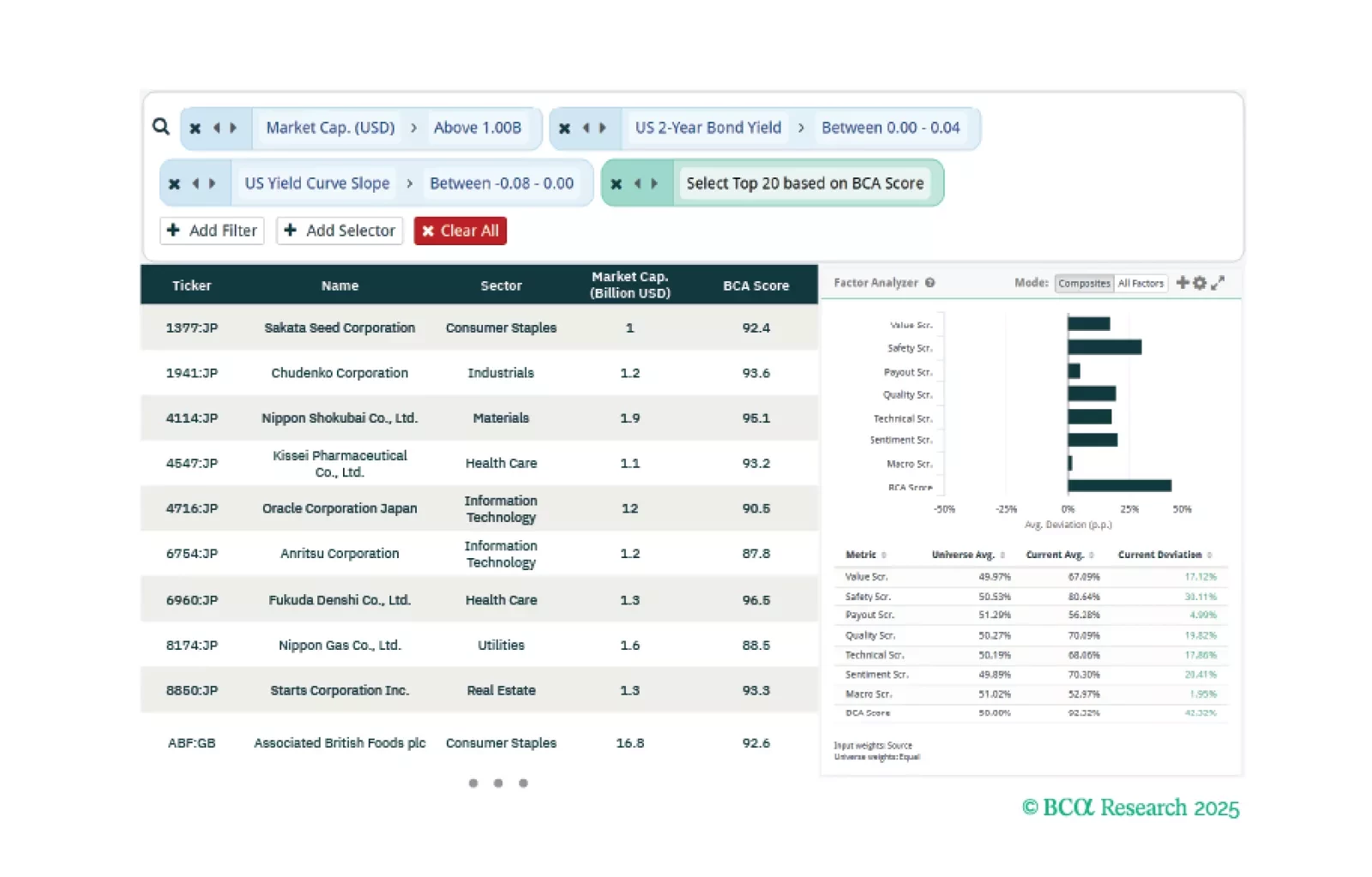

This week, our three screeners focus on providing equity insights based on the impact of tariffs, and trade policy uncertainty in general, helping clients identify stocks exposed to these shocks.

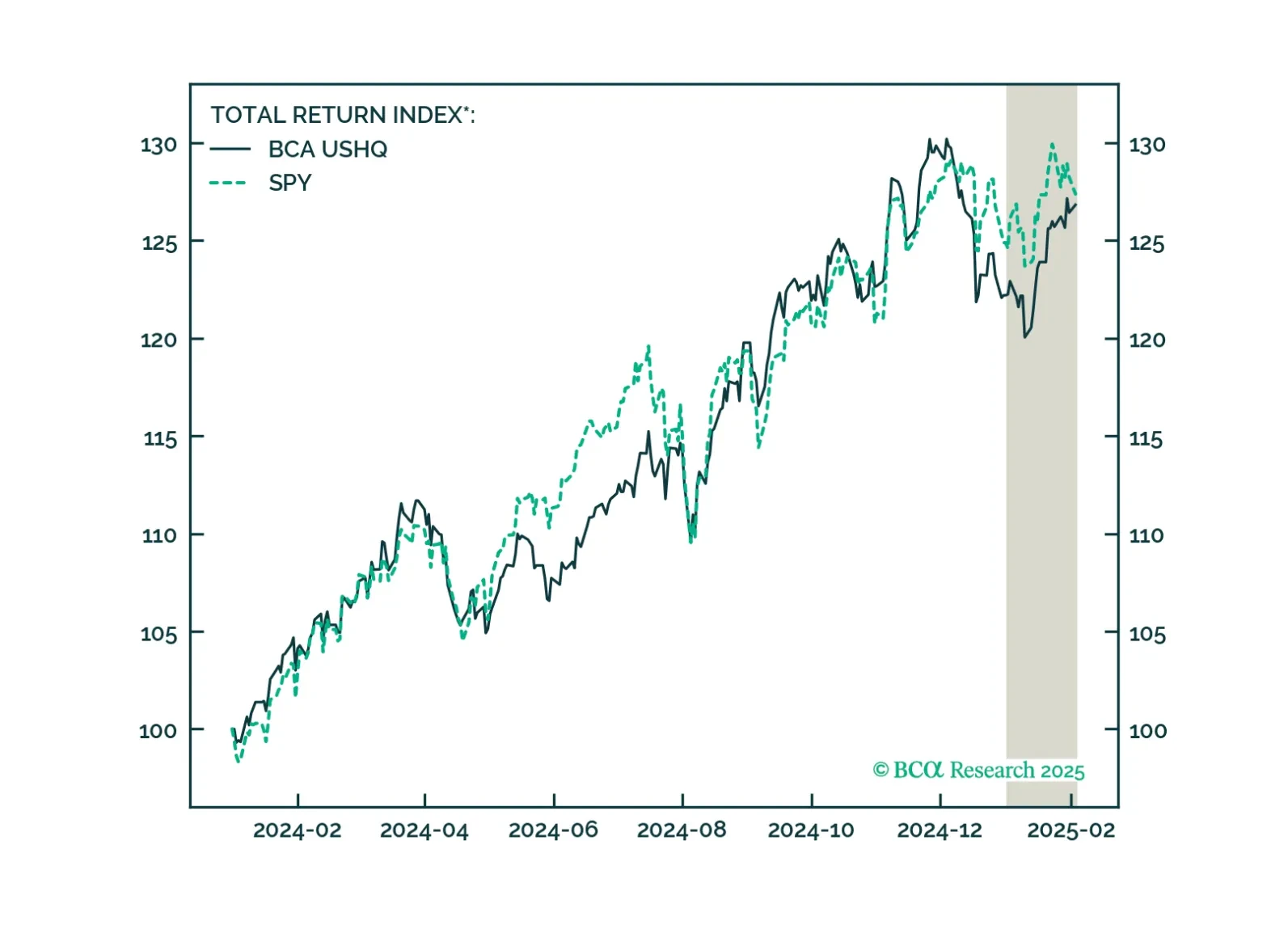

The US High-Quality (USHQ) portfolio slightly outperformed in January, returning 3.4%, whilst its SPY benchmark returned 2.9%. That said, we think the USHQ portfolio will have a solid run through the first half of 2025, benefitting from rising market risk on the back of President Trump’s tariff agenda. USHQ’s underlying Quality and Safety Score factor tilts will be increasingly favored as market uncertainty grows.

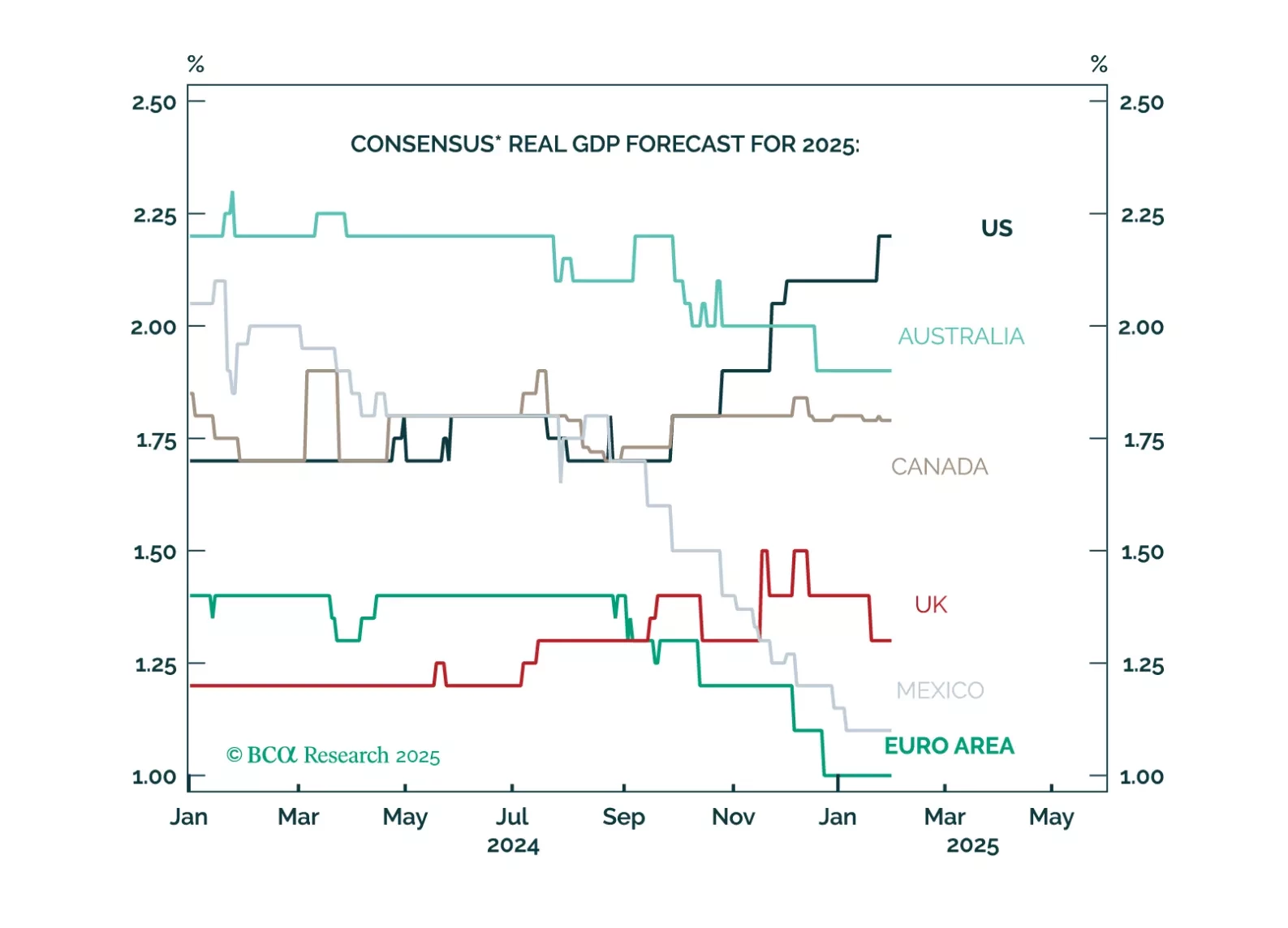

Markets and forecasters anticipate a “Golden Age” for Trump’s America, with US growth expectations soaring while the rest of the world lags. However, this extreme optimism means that there is a lot of room for disappointment. Cooling income growth, weak housing and less deficit spending than expected will result in US growth underperforming expectations. Maintain a modest underweight to equities and modest overweight to fixed income. US markets have become more expensive relative to the rest of the world even as quality differentials have stabilized. Prepare to downgrade US equities to underweight and to upgrade Euro Area and China to overweight. We will wait to pull the trigger until we have more clarity on trade policy and when the dollar's momentum turns negative.

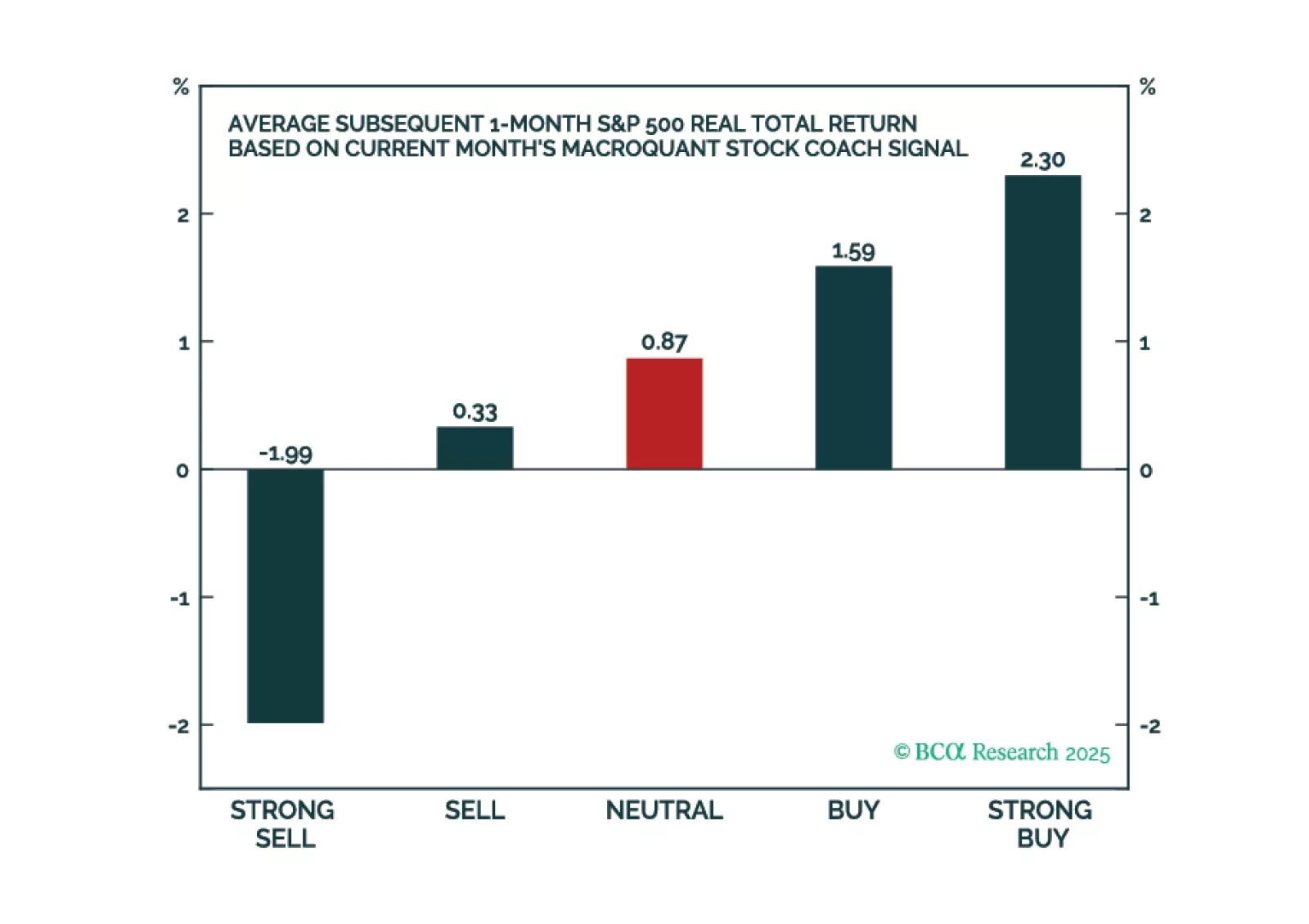

The latest version of the MacroQuant model suggests that the bull market in US stocks is winding down. The model expects Treasury yields to fall later this year but is not ready to go long duration just yet.