Equities

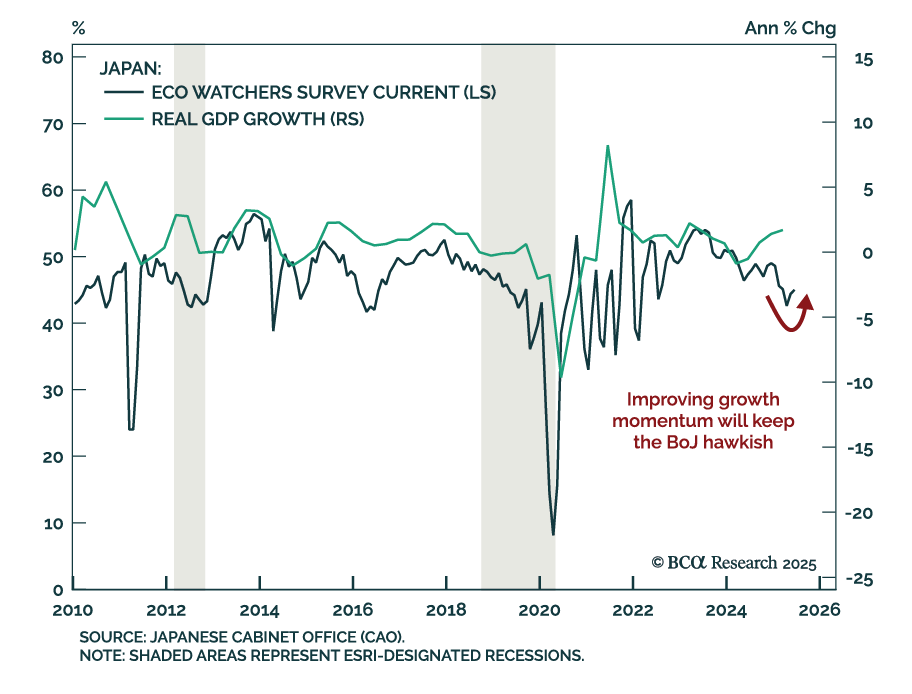

Japan’s improving growth momentum and structural inflation shift support an underweight in JGBs and long JPY positioning. The June Eco Watchers Survey was broadly in line with expectations, with current conditions ticking up to 45.0 and expectations modestly…

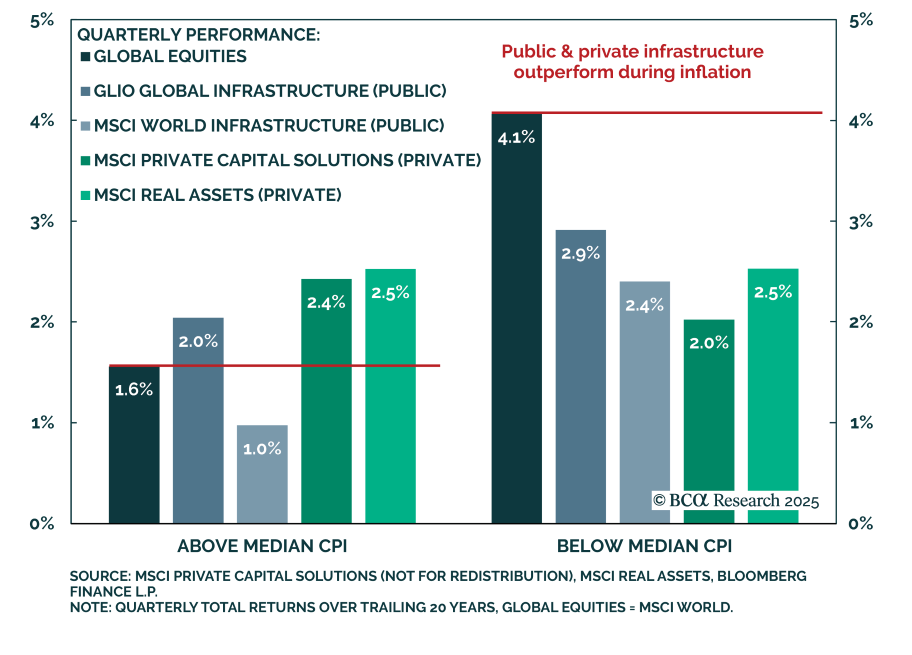

BCA’s Private Markets & Alternatives strategists recommend a balanced allocation across Public and Private Infrastructure, with near-term valuation favoring Public. Structural differences in index construction, sector mix, and regional exposure drive…

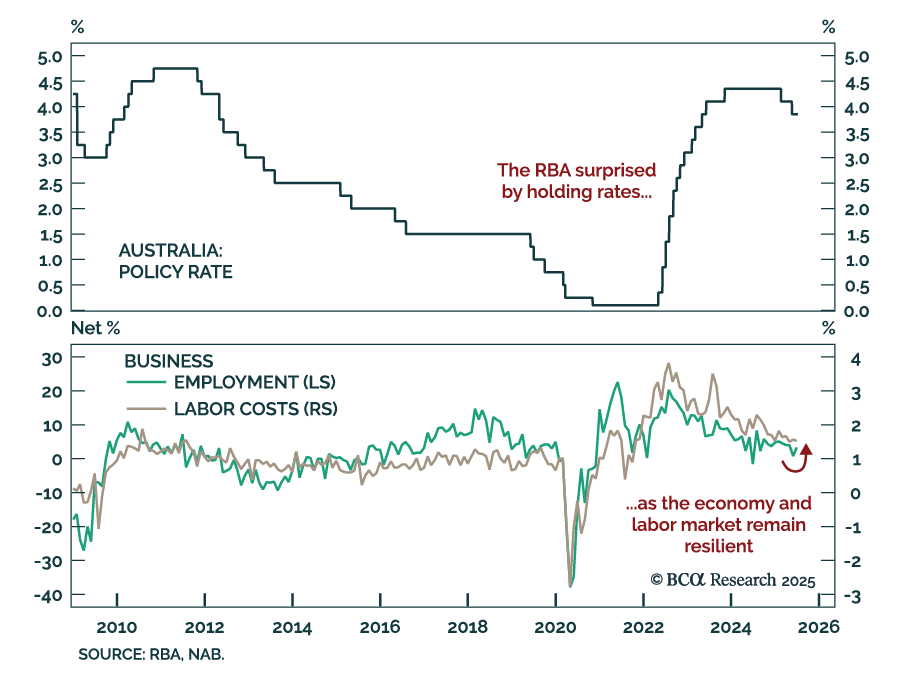

The RBA’s surprise hold reinforces a slower easing path, warranting an underweight on Australian bonds. Markets had priced in a 25 bps cut, but the central bank opted to keep rates at 3.85%. Governor Bullock characterized the decision as a matter of timing,…

全球市场正从疫情后的刺激与错配中走出。“宿醉” 初醒,各类资产进入新一轮定价周期。在结构变化加速之际,小莉将讨论如何在全球 “宿醉期” 中稳健前行、寻找超额回报。

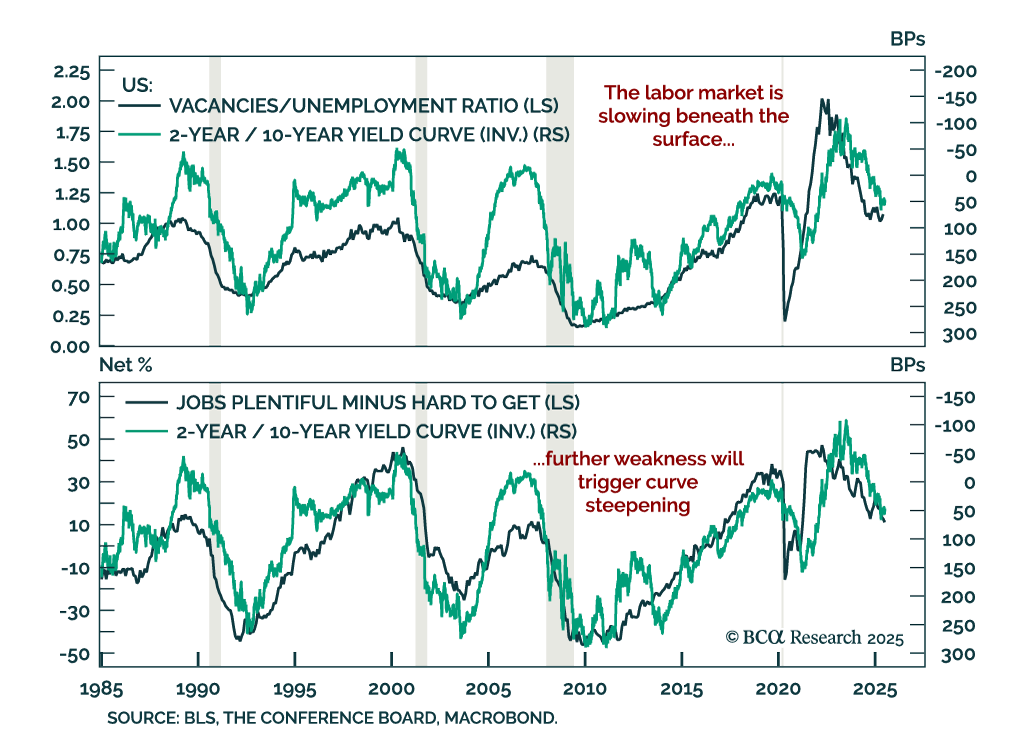

Labor market cracks reinforce long duration and steepener positioning as growth risks mount. Job market data has looked strong on the surface, but the details of the June employment and JOLTS reports confirm a slowing trend within the “low hiring, low firing”…

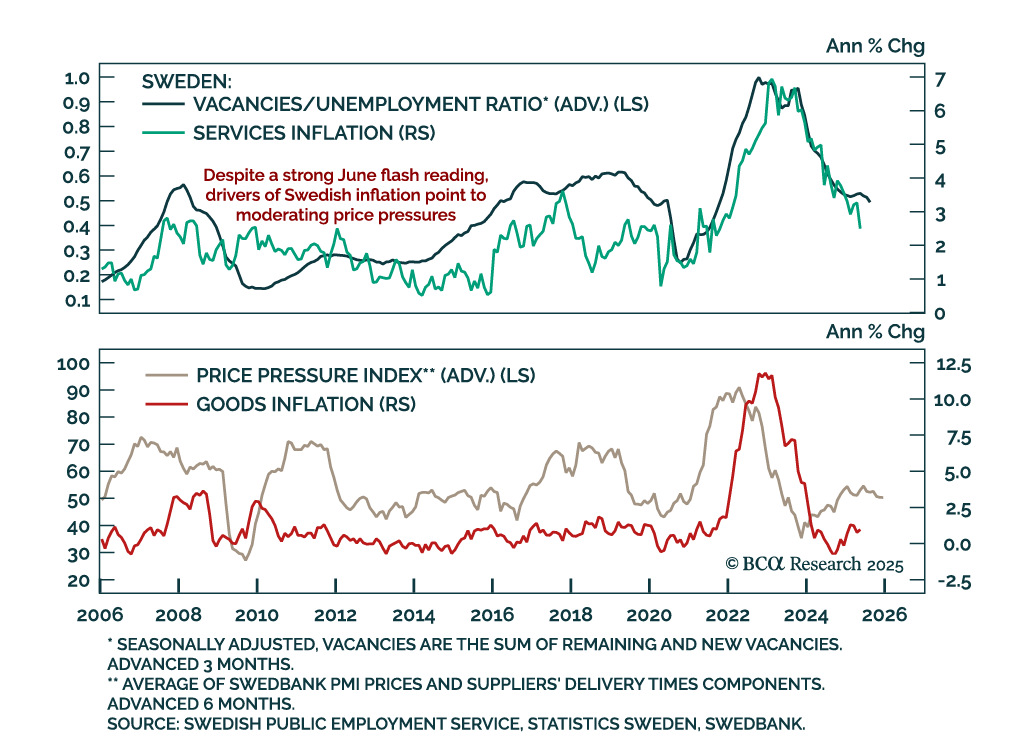

Stronger-than-expected June inflation will likely keep the Riksbank on hold in August, despite soft underlying trends. Headline inflation accelerated more than expected to 0.5% m/m (0.8% y/y), while CPI ex-housing rose to 2.9% y/y and core inflation to 3.3%…

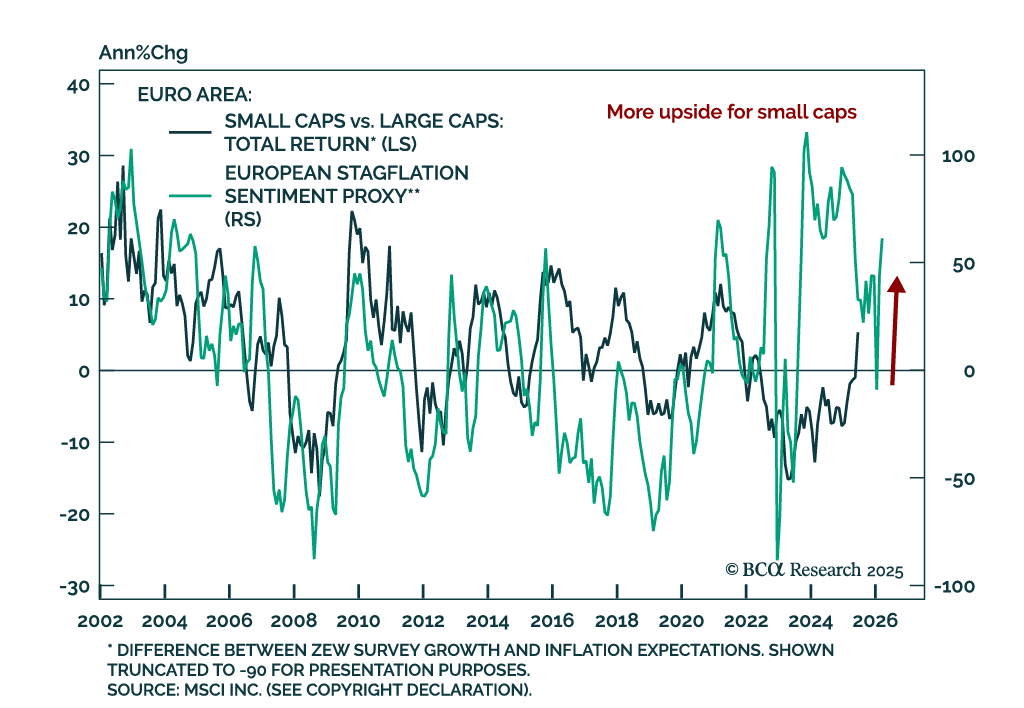

Our European Investment strategists upgrade small caps to maximum overweight, citing improving margins, supportive macro trends, and attractive valuations. They expect small caps to continue outperforming large caps over the next 12 to 18 months. With…

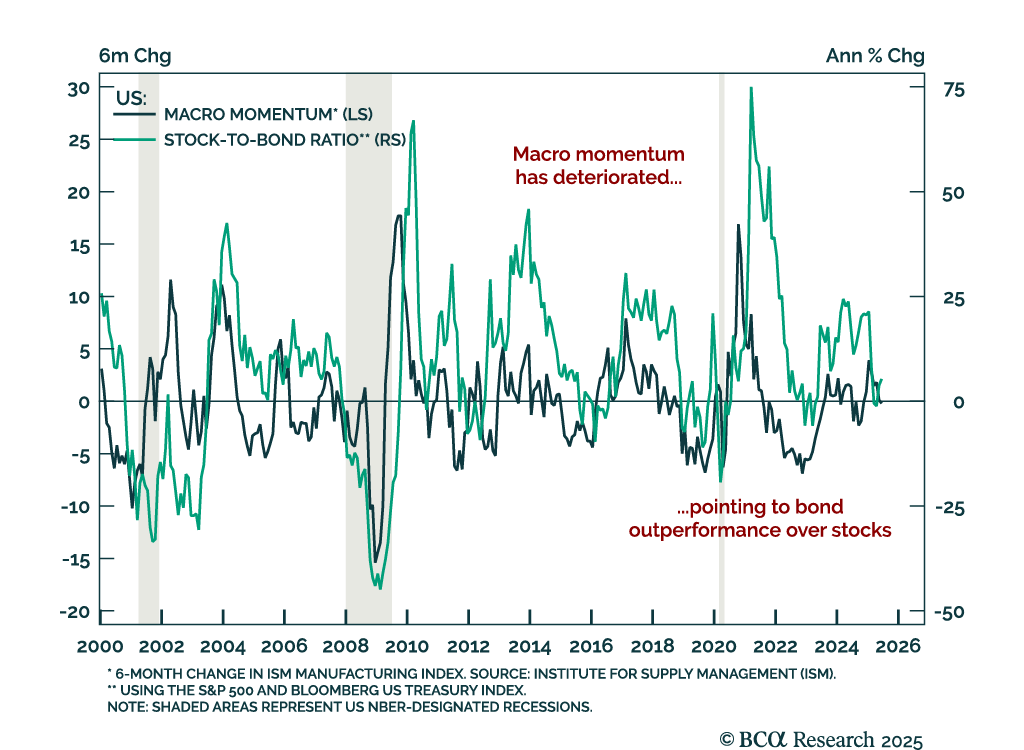

Deteriorating macro momentum supports a defensive asset allocation stance as hard data deteriorates. Last week’s ISM Manufacturing and Services PMIs confirmed that growth is slowing and price pressures are easing from a high level. The ISM Manufacturing index…

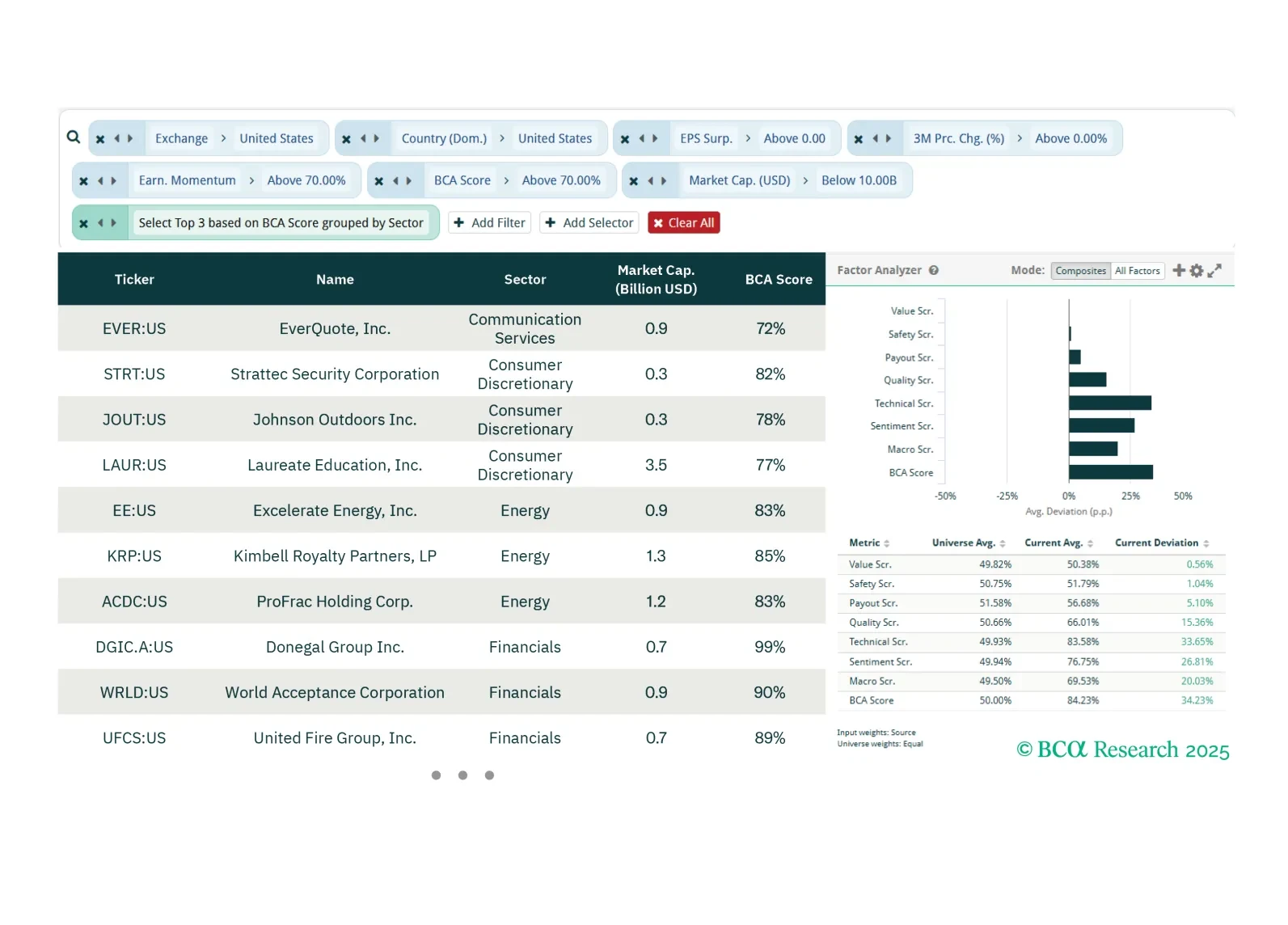

This week our three screeners identify stocks that are likely to keep delivering deliver earnings surprises in the US, European small caps that are high quality and mean reverting, and Japanese large caps picks across GICS 1 sectors.

Earnings growth should continue to support equity performance this year. However, after blockbuster gains, some profit-taking is likely. We recommend booking profits and increasing exposure to Defensives.