Equities

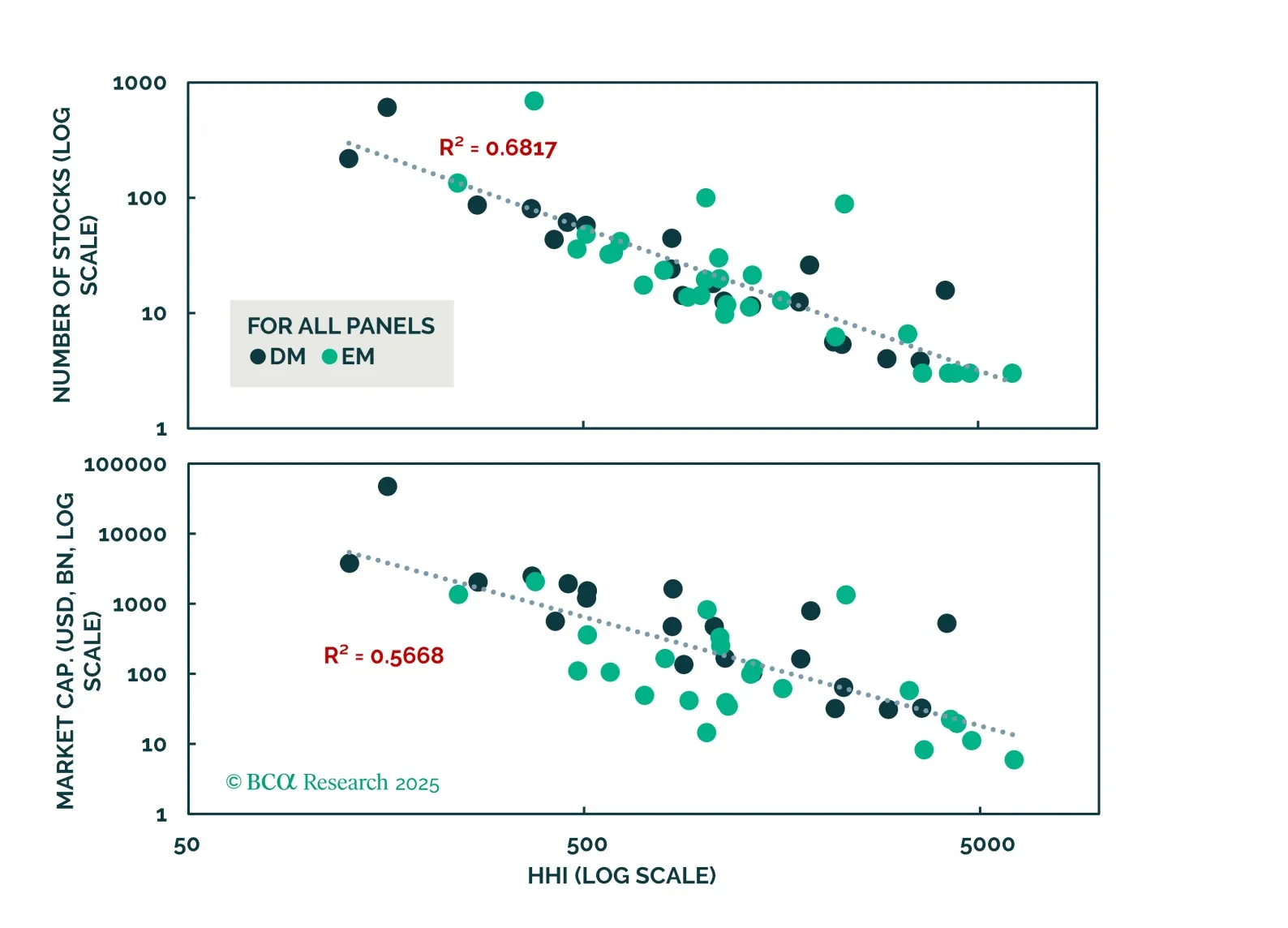

Using stock-level data for MSCI ACWI country indices going back to 1984 for Developed markets and 1988 for Emerging markets, we find that market concentration adds little predictive power for long term forward returns. Whatever predictive power it has disappears once we include traditional metrics like value and size. The same is true for idiosyncratic index risk. Index concentration is just not very important for determining risk and return in equity markets.

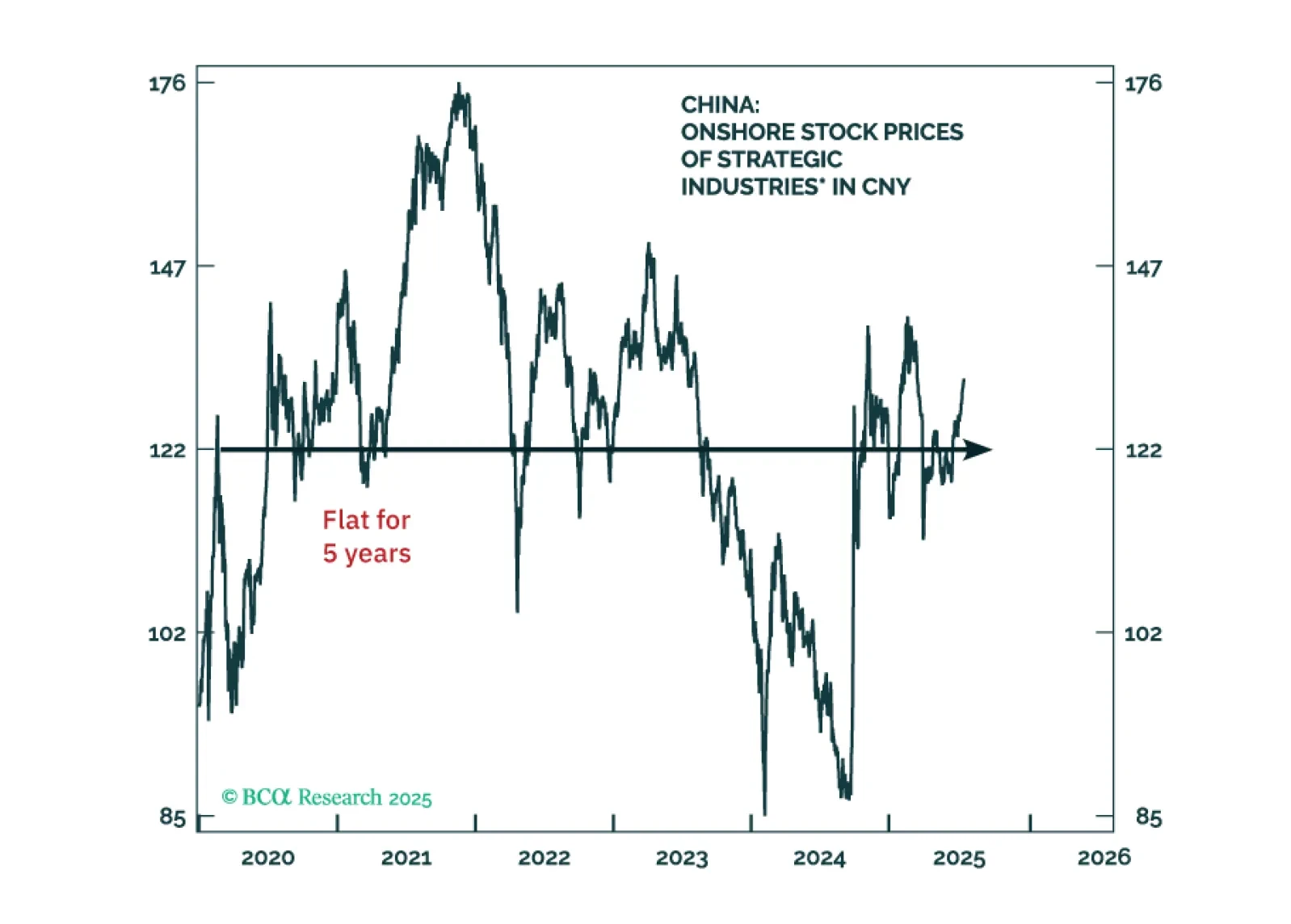

Investors often ask us which industries the Chinese government is prioritizing for expansion. The assumption is that investing in sectors hand-picked authorities will produce solid investment returns. Yet, this assumption has not held over the past decade.

We will only move to a fully defensive stance if the “whites of the recession’s eyes” appear. So far, they have not. We will be increasingly looking to our MacroQuant model for guidance on when the next turning point in markets may come.

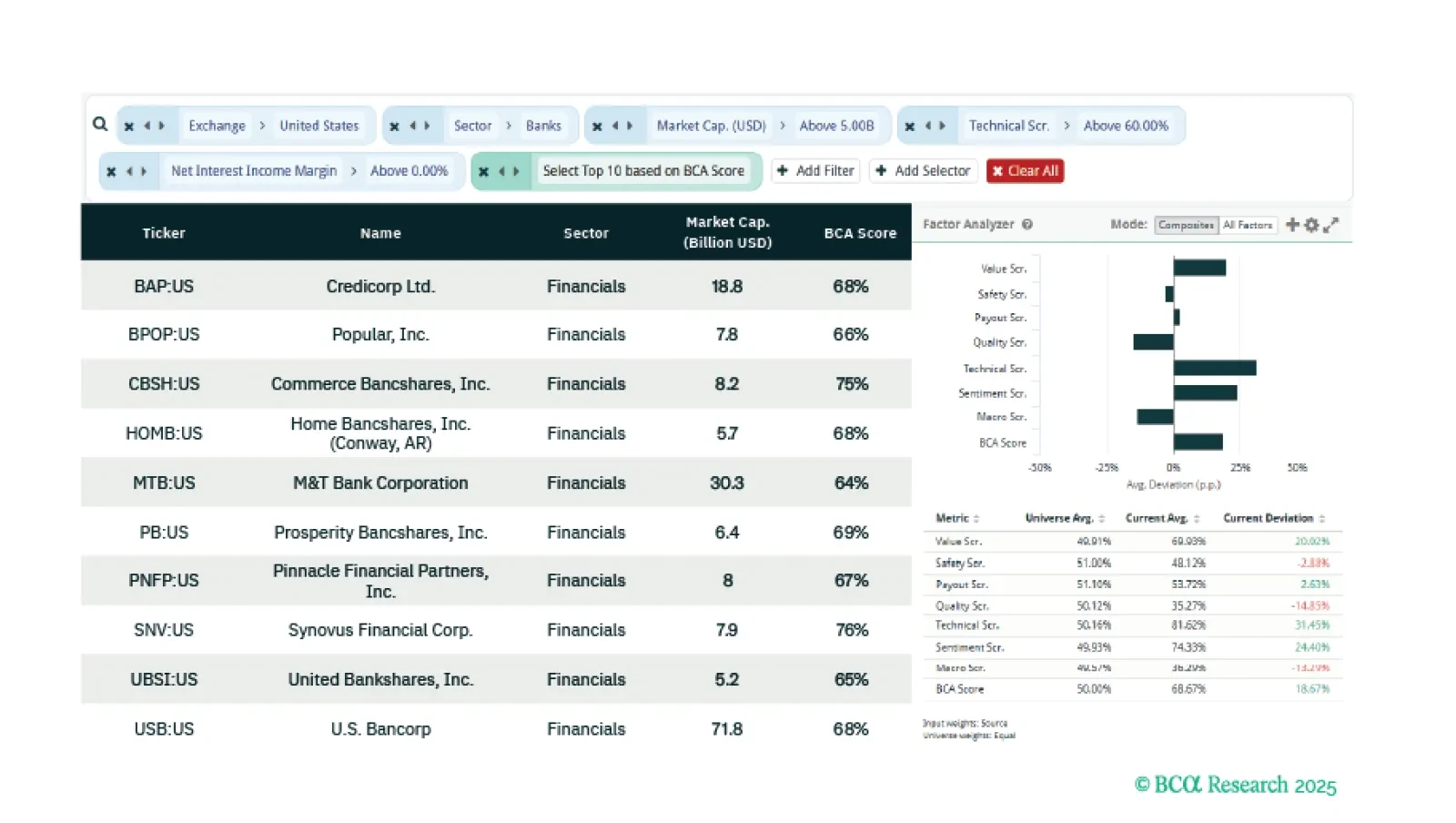

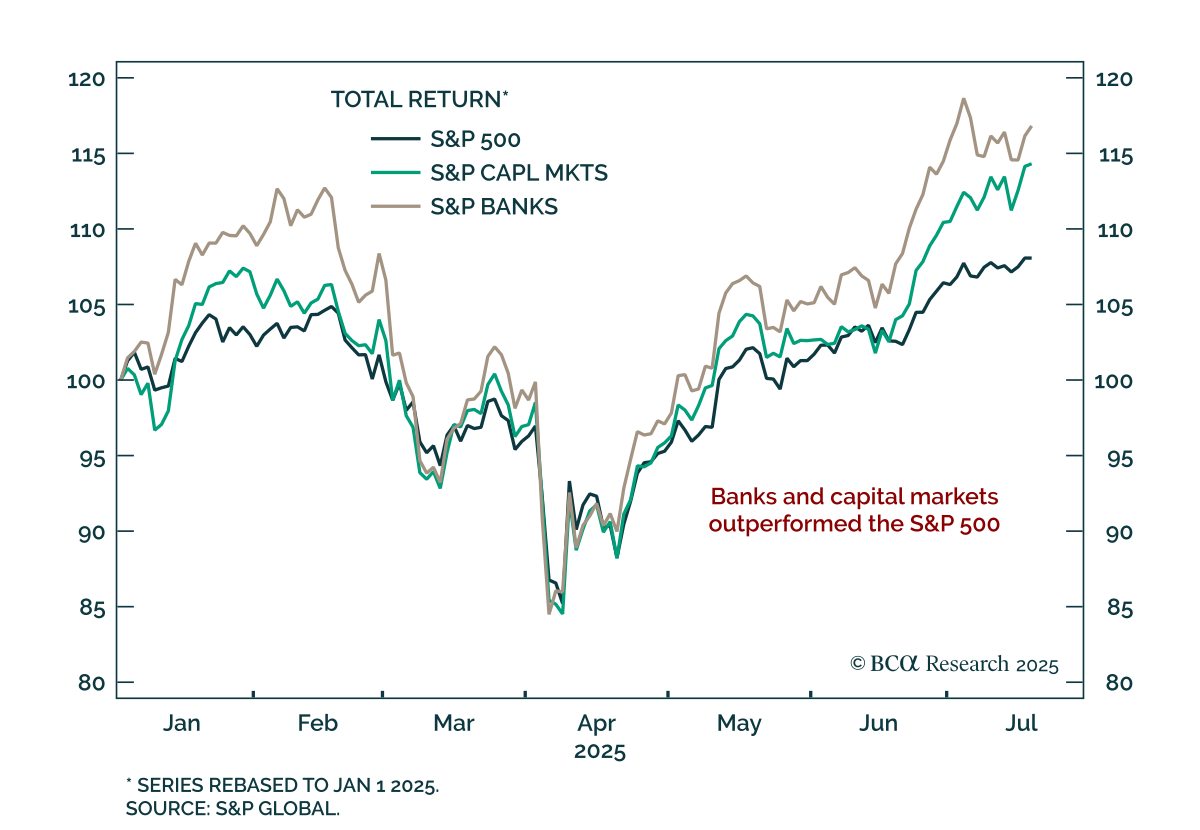

This week our three screeners identify: Equity plays on US banks, stocks that benefit from heightened US fiscal uncertainty, and a global Value and Technical basket of stocks.

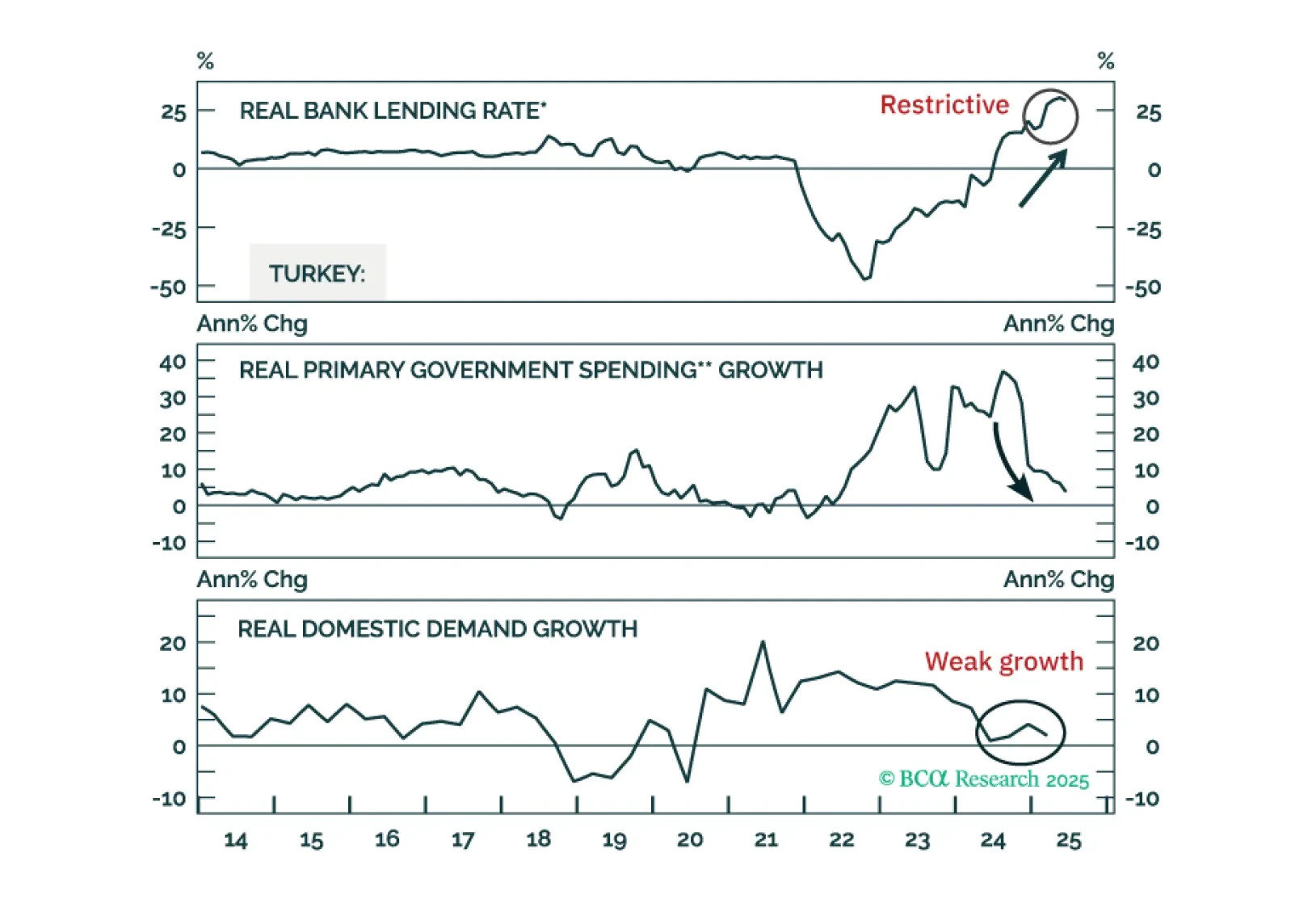

Thanks to the tight monetary and fiscal policies so far, inflation and growth are heading lower in Turkey. Buy 2-year local currency bonds, currency unhedged. Also, upgrade Turkey's domestic bonds from neutral to overweight and stocks from underweight to neutral within their respective EM portfolios.

This insight gives life to four high-conviction views on European small caps, aero¬space & defense, banks, and telecoms by harnessing the power of BCA’s Equity Analyzer (EA).