Equities

Macroeconomic and business conditions are gradually becoming more favorable for Tech as the bottoming of demand is in sight. Yet, we don’t believe that now is an attractive entry point - the good news is fully priced in, and technicals signal a pullback. However, the sector is worth monitoring as we are getting closer to a sustainable rebound. Our positioning remains unchanged.

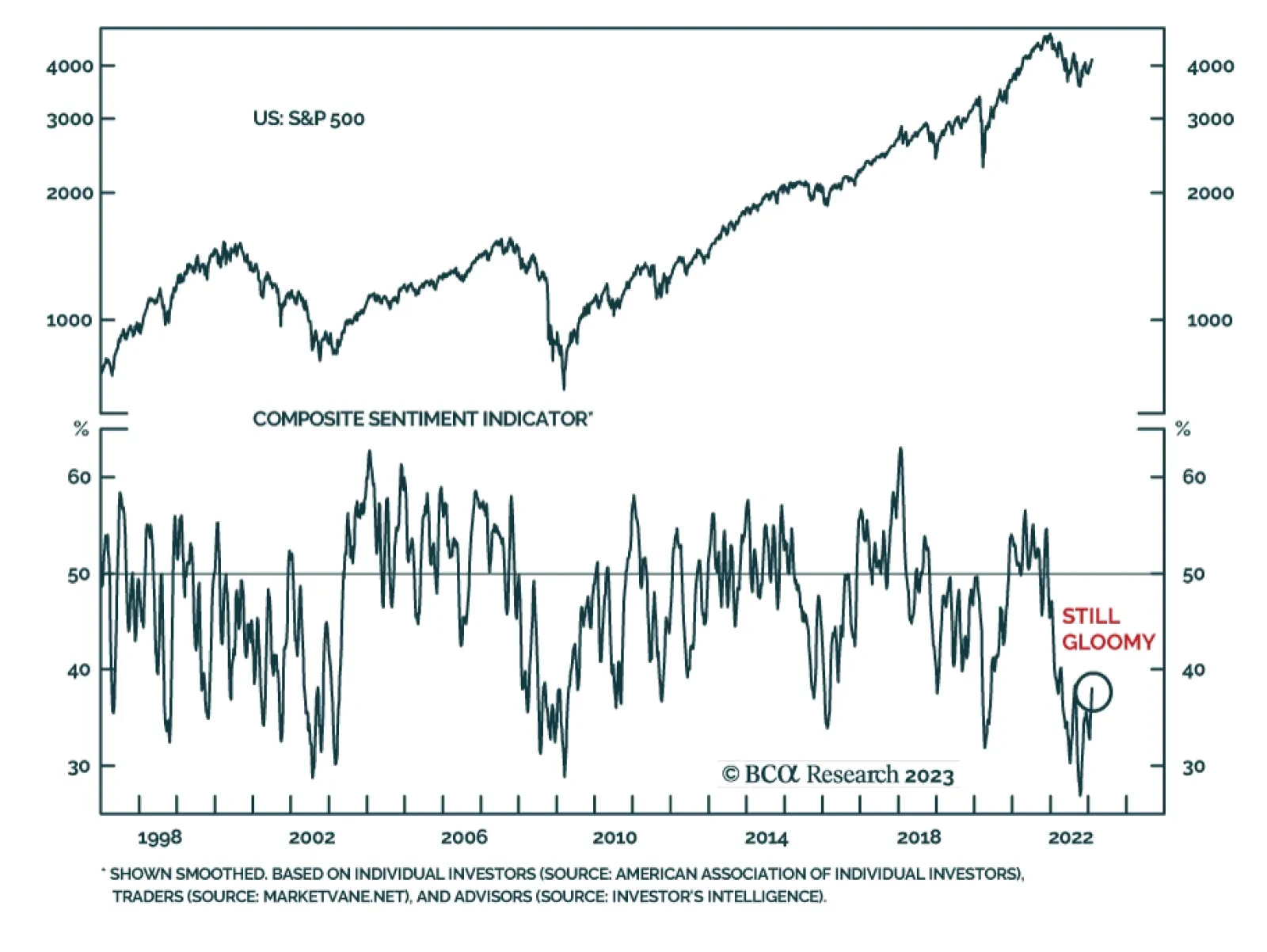

Ironically, increased confidence that the economy can withstand higher bond yields may be necessary to lift yields to a level that is actually detrimental to growth. Thus, until more investors are convinced that a recession will be averted, a recession will be averted. Remain tactically bullish on stocks for now. A more defensive posture will likely be necessary later this year.

The Fed is betting that the usual non-linearity of unemployment is different this time, but so far, there is nothing to suggest that it is different. We discuss the key signposts to watch out for, plus the implications for interest rates and asset allocation.

This is the first of two Special Reports aiming to answer client questions in response to the recent dramatic changes in stock-bond correlations. In this report we focus on what role US Treasurys have played since 1872, how the current regime shift in stock-bond correlation compares to 150-years of history, and how it will impact asset allocation going forward.

The Fed’s actions at its meeting last Wednesday were no surprise – downshifting to 25 basis points while guiding for more hikes was widely expected – but Chair Powell’s newly conciliatory tone at the press conference helped to spark a two-day equity rally. We remain overweight equities, expecting the S&P 500 to rally into the mid-4,000s at some point in the first half.

The risk-on rally is challenging our annual forecast so we are cutting some losses. But we still think central banks and geopolitics will combine to reverse the rally later this year.