Equities

The latest round of earnings calls from the systemically important banks was encouraging on balance. Households are still flush and still spending and consumer and business delinquencies remain remarkably low. Though a recession is surely coming, it doesn’t seem to be lurking just around the corner.

The dollar has entered a structural bear market. Although the greenback could get a temporary reprieve during the next recession, investors should position for a weaker dollar over the long haul.

China's recovery will be driven by consumer spending in general and on services in particular, while industrial sectors will disappoint.

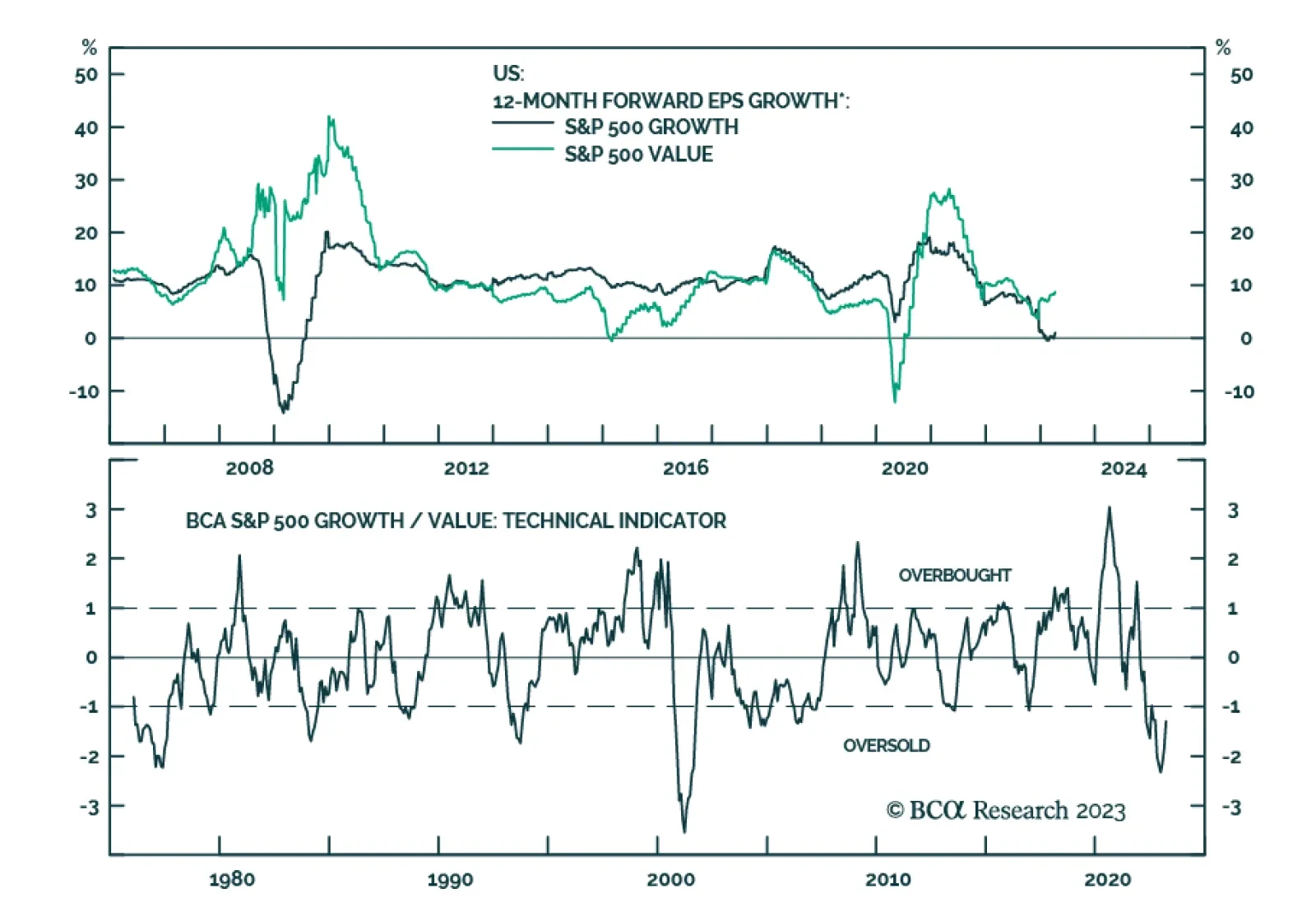

The YTD market rally was driven by outperformance of high-quality growth stocks which offer protection in uncertain times. As growth continues to slow, high-quality growth stocks should continue to do well. Hence, we are moving to overweight Growth vs. Value.

Investors and regulators would be foolishly complacent if they didn’t consider the possibility that the banking turmoil could reduce credit availability and slow economic activity, but the most recent data suggest that the aggregate banking system is bouncing back nicely.

We Introduce our new macro models for the Eurozone’s equity earnings, which include sectoral forecasts. Find out what they predict for the next six-to-nine months.