Equities

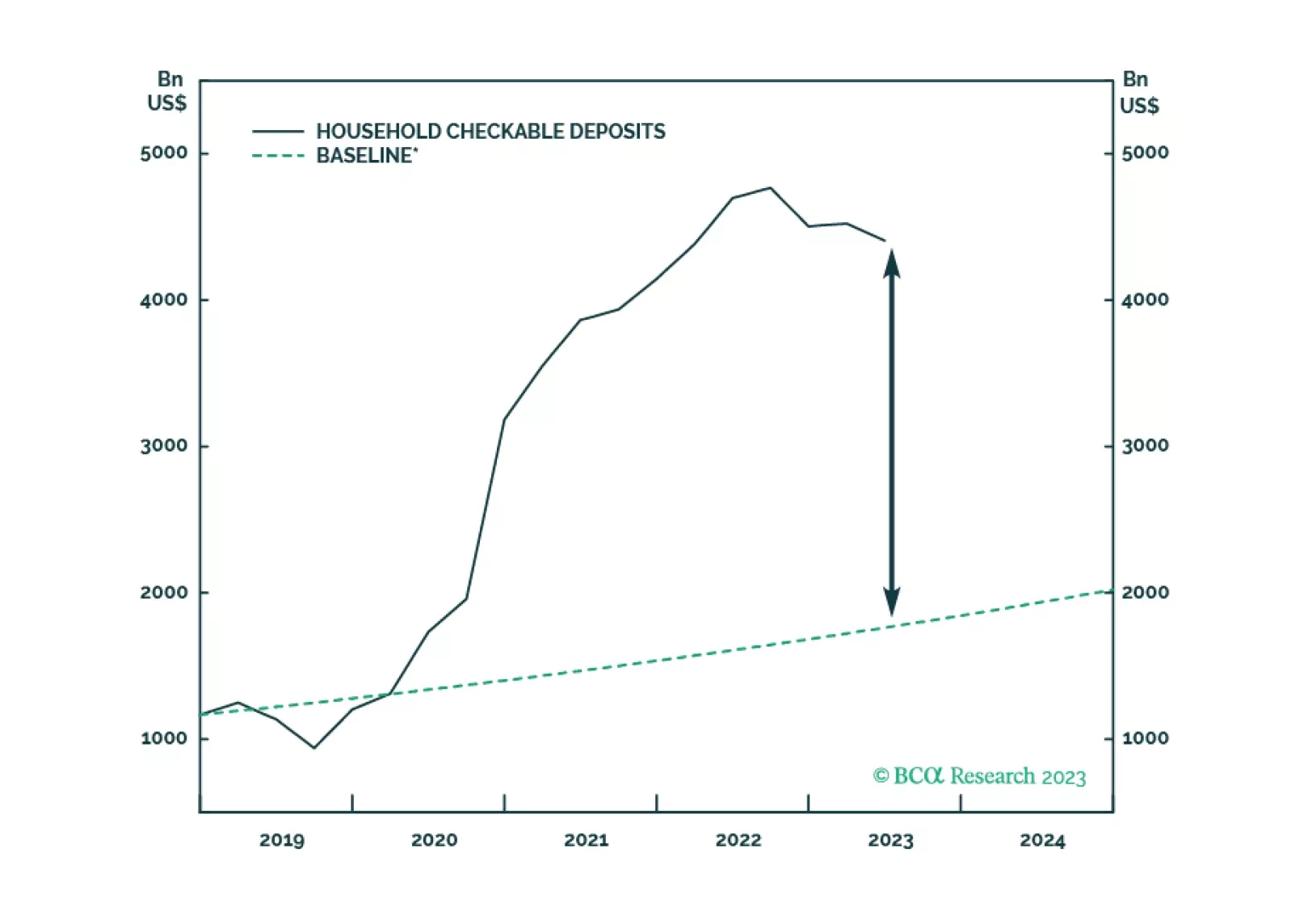

The biggest banks report that consumer credit card delinquencies still have yet to get back to pre-COVID levels and other credit performance indicators, leading and lagging, remain solid. There is still a great deal of cash sloshing around the banking system, though consumption has clearly slowed. We reiterate our view that a recession is coming, but not before the year is out.

The Hamas attack against Israel, timed almost 50 years to the day after a similar surprise attack on Yom Kippur of 1973, has evoked parallels with the 1970s. Parallels not only with Middle Eastern geopolitics then and now, but also with inflation, economics, and financial markets. In this report, we explain what went wrong in the 1970s and whether the mistakes will be repeated. Plus: the sharp sell-offs in some Latin American currencies are reaching a potential turning-point.

Q3-2023 is expected to mark the end of the earnings recession for the past three quarters, opening the door to positive earnings growth. Whether that would be sustainable or will sputter once the recession settles in as expected in 2024 remains to be seen. However, much of earnings growth is already priced in.

More equity volatility is coming in the short run. Trump’s nomination looks to be smooth, which marginally reduces the incumbent party advantage and increases policy uncertainty.