Equities

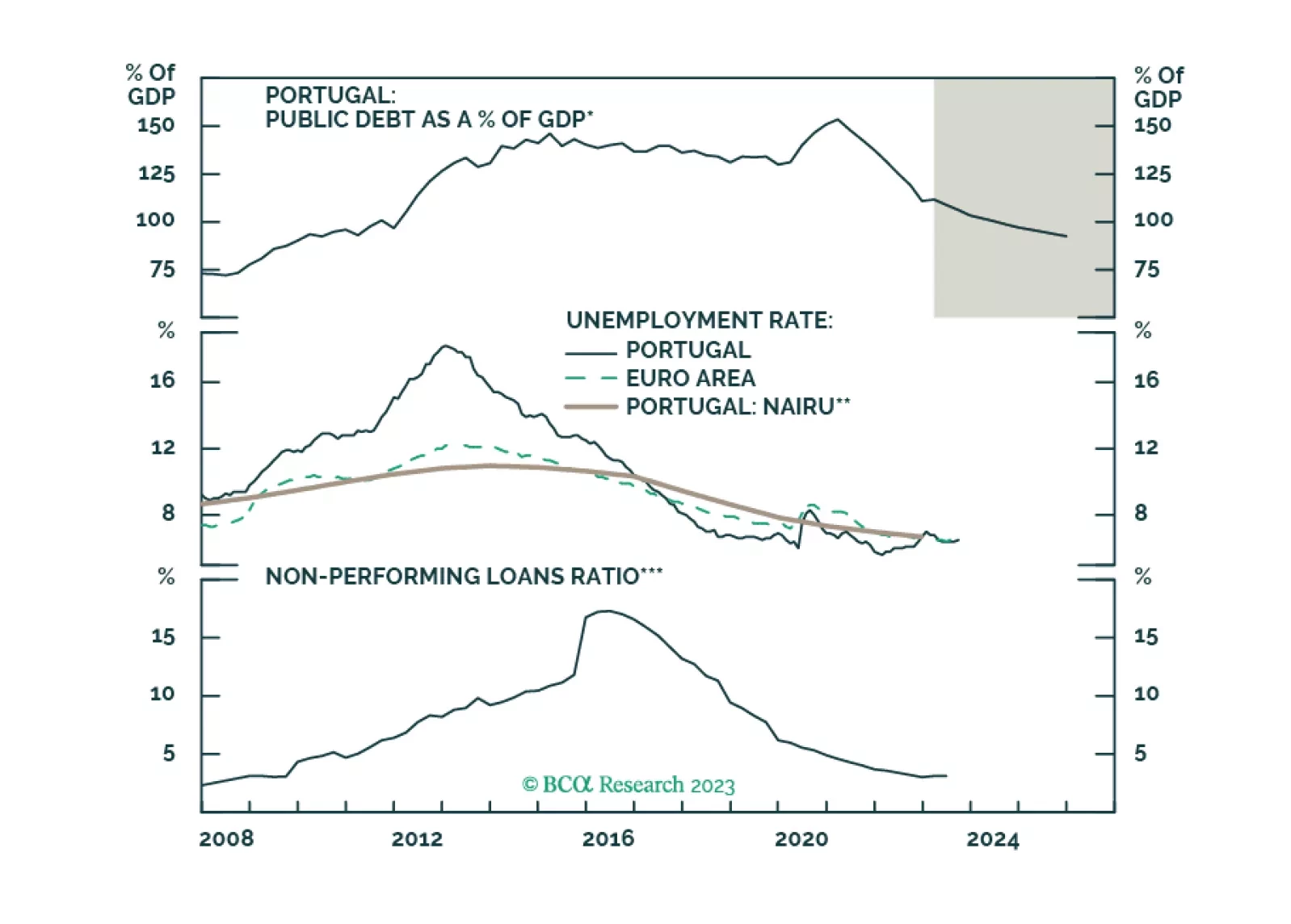

The first stop of the EIS Special Series: PIGS Have Wings takes us to Portugal.

The Q3 earnings season is coming to an end. By Friday, 481 companies in the S&P 500 index had reported earnings. In aggregate, the results are generally favorable. The share of companies whose earnings exceeded analyst expectations (81.9%) is above the…

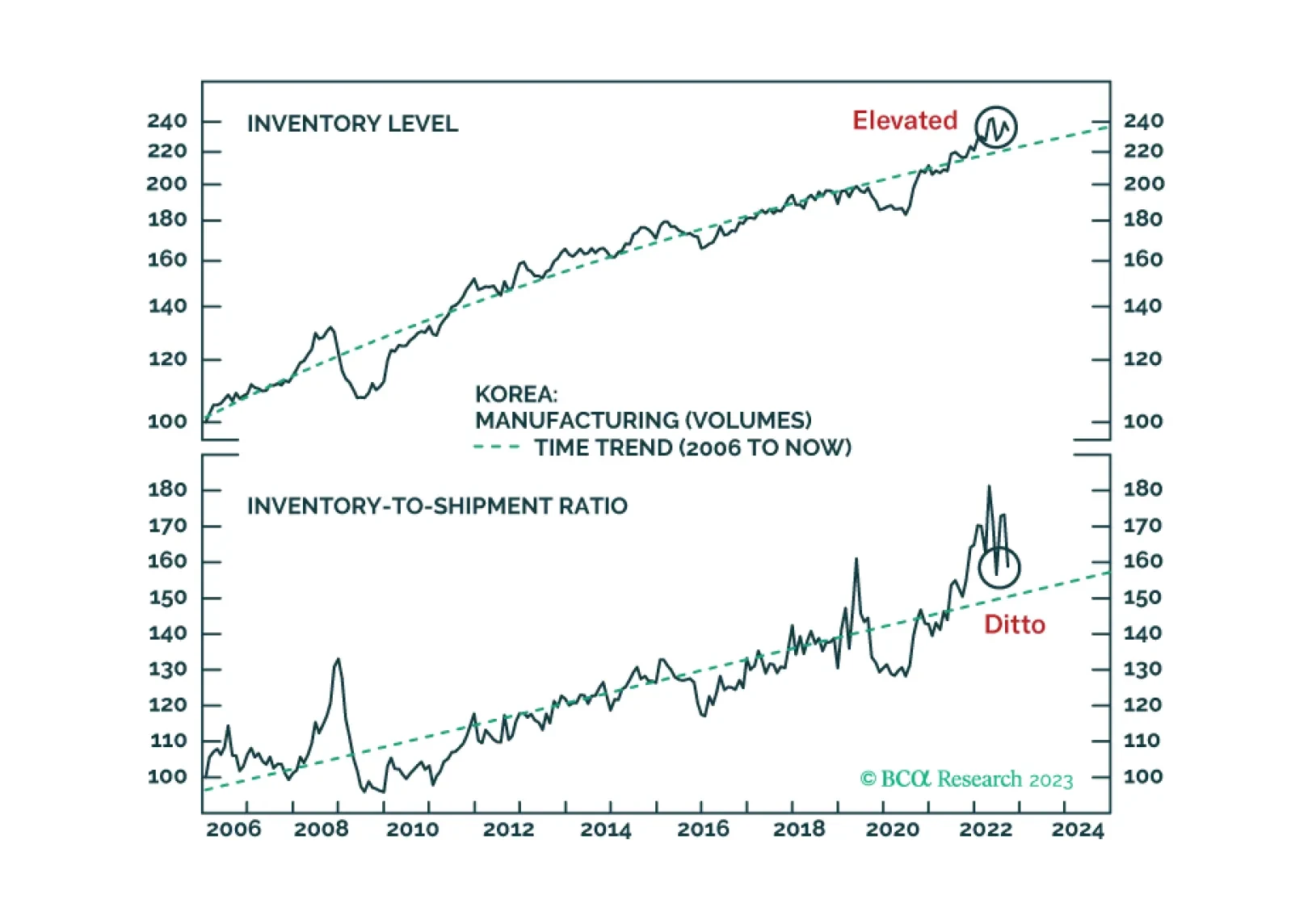

According to BCA Research's Emerging Markets Strategy service, investors should focus on fluctuations in final demand rather than inventories. A common narrative endorsed by many market participants is that inventory restocking worldwide will support the…

European flash PMI estimates for November sent a slightly less pessimistic signal on Thursday. The Eurozone composite PMI climbed by 0.6 points to 47.1, beating expectations of a more muted increase to 46.8. Notably, both the manufacturing and services…

Global cyclical sectors are outperforming defensive sectors on a year-to-date basis. The bulk of this outperformance occurred in the first seven months of the year. Relative valuations contributed to this dynamic as last year's selloff was more pronounced…

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.

In the recently held Polish general elections, the ruling Law & Justice Party (PiS) lost power. Chances are that a coalition led by the Civic Platform party will form a government next month. The new coalition ran on a pro-European Union (EU) platform…

Confidence is on the mend in the Euro Area. The rebounding ZEW growth expectations index reveals that investors are becoming more optimistic. The German IFO's business climate index inched higher in October for the first time since April, suggesting that…

Global equities have had a stellar 2023, rising by 16% year-to-date and outperforming global bonds by roughly the same amount. However, the large concentration of US stocks in the Magnificent Seven has called into question the legitimacy of this rally. There…

After dipping into negative territory between June and early August, the Global Economic Surprise Index has since rebounded, signalling an improvement in economic momentum. Initially, this rebound was isolated to the US. However, the trend has been broadening…