Emerging Markets

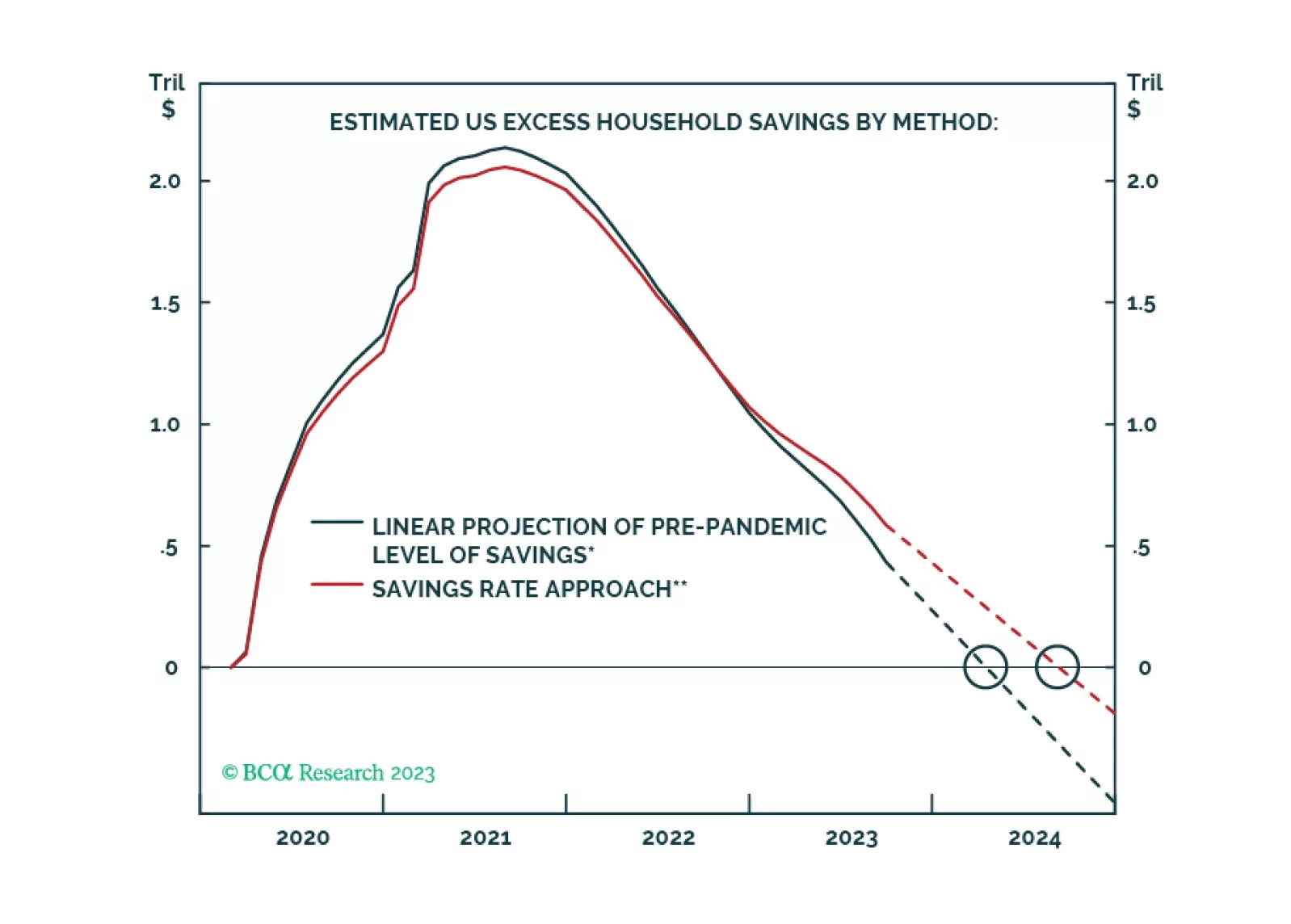

Inflation won’t fall fast enough for the Fed to cut rates preemptively before recession arrives. The risk/rewards balance is unfavorable for risk assets. Stay overweight bonds versus equities.

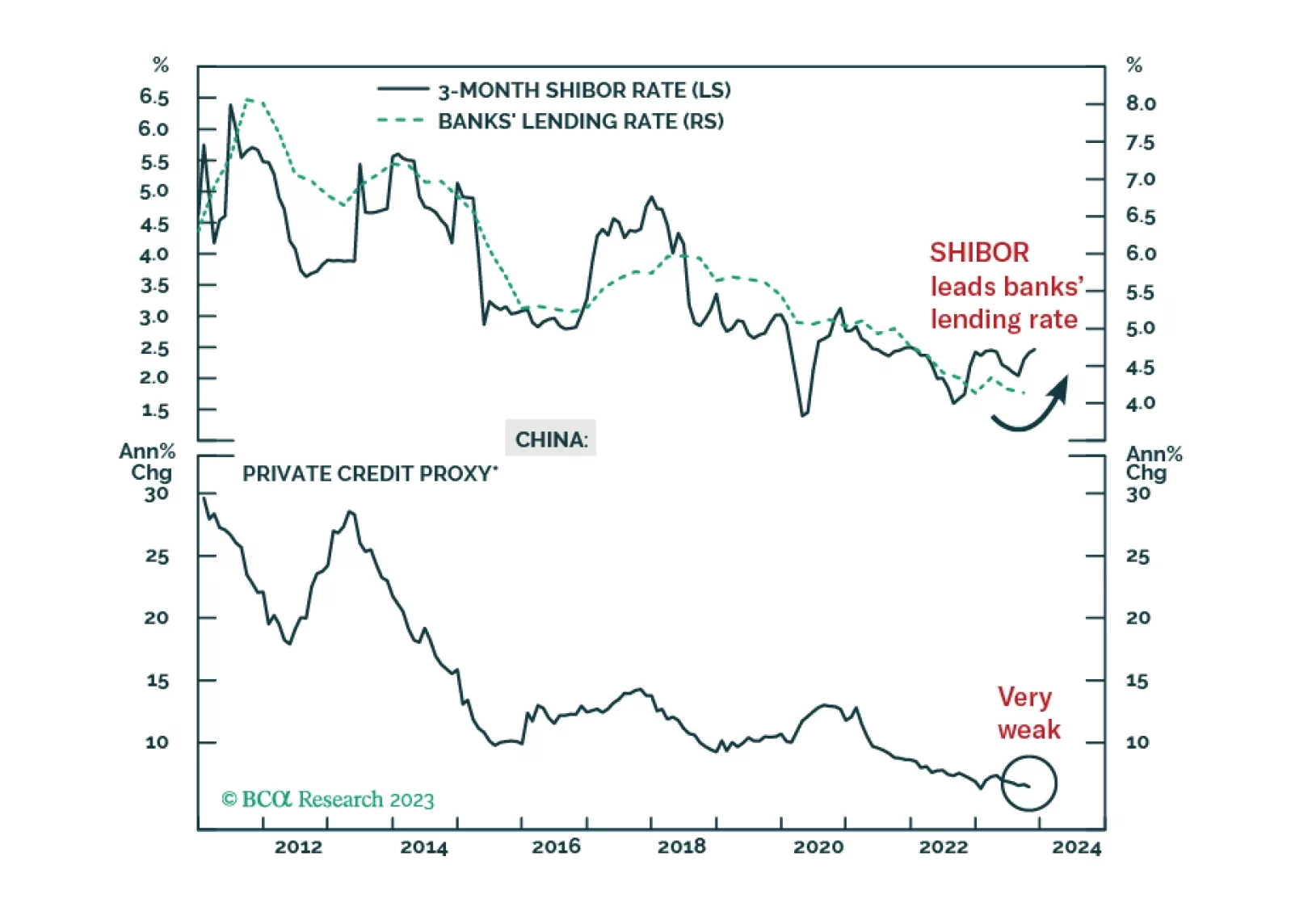

A cyclical recovery in China’s economy is still not imminent. The PBoC has tightened interbank liquidity to stabilize the exchange rate since late August. This does not bode well for the real economy. The uptick in onshore bond yields and the RMB’s appreciation will be transient. Equity investors should stay cautious.

Today, we are sending you the BCA annual outlook for 2024. The report is an edited transcript of our recent conversation with Mr. X and his daughter, Ms. X, who are long-time BCA clients with whom we discuss the economic and financial market outlook for the next twelve months toward the end of each year.

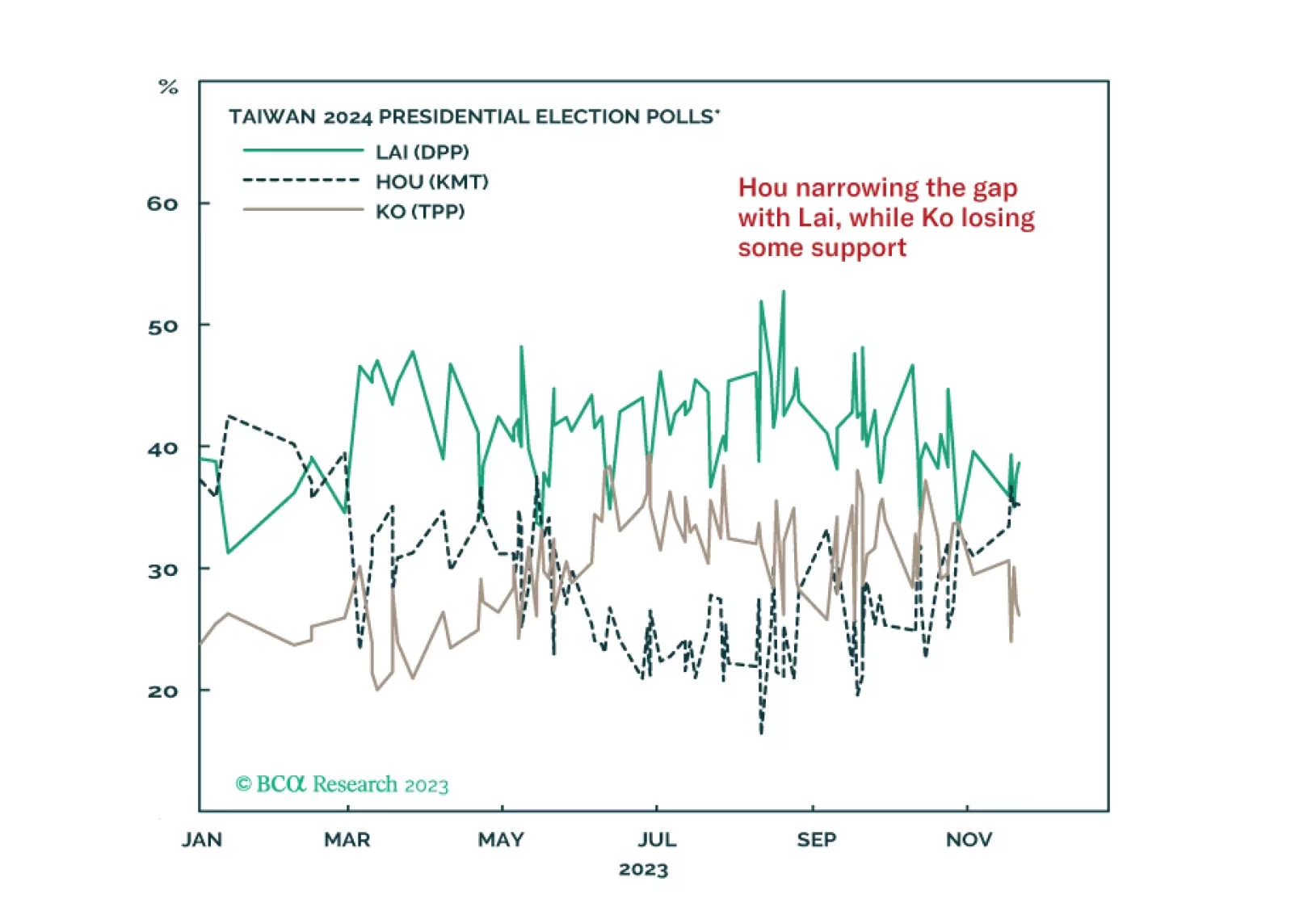

A series of notable events took place over the Thanksgiving holiday but none of them force us to change our fundamental assessments. The conflict in the Middle East is likely to escalate rather than de-escalate, while the Taiwan Strait has at least a 50/50 chance of seeing tensions escalate next year.

Global smartphone demand will likely find a bottom in 2024Q1 and rebound modestly between 2024Q2 and Q4. Competition in the global smartphone market will intensify. Chinese phone makers will gain market share from Apple and Samsung. Continue overweighting Taiwanese stocks, including tech, within the global equity benchmark.

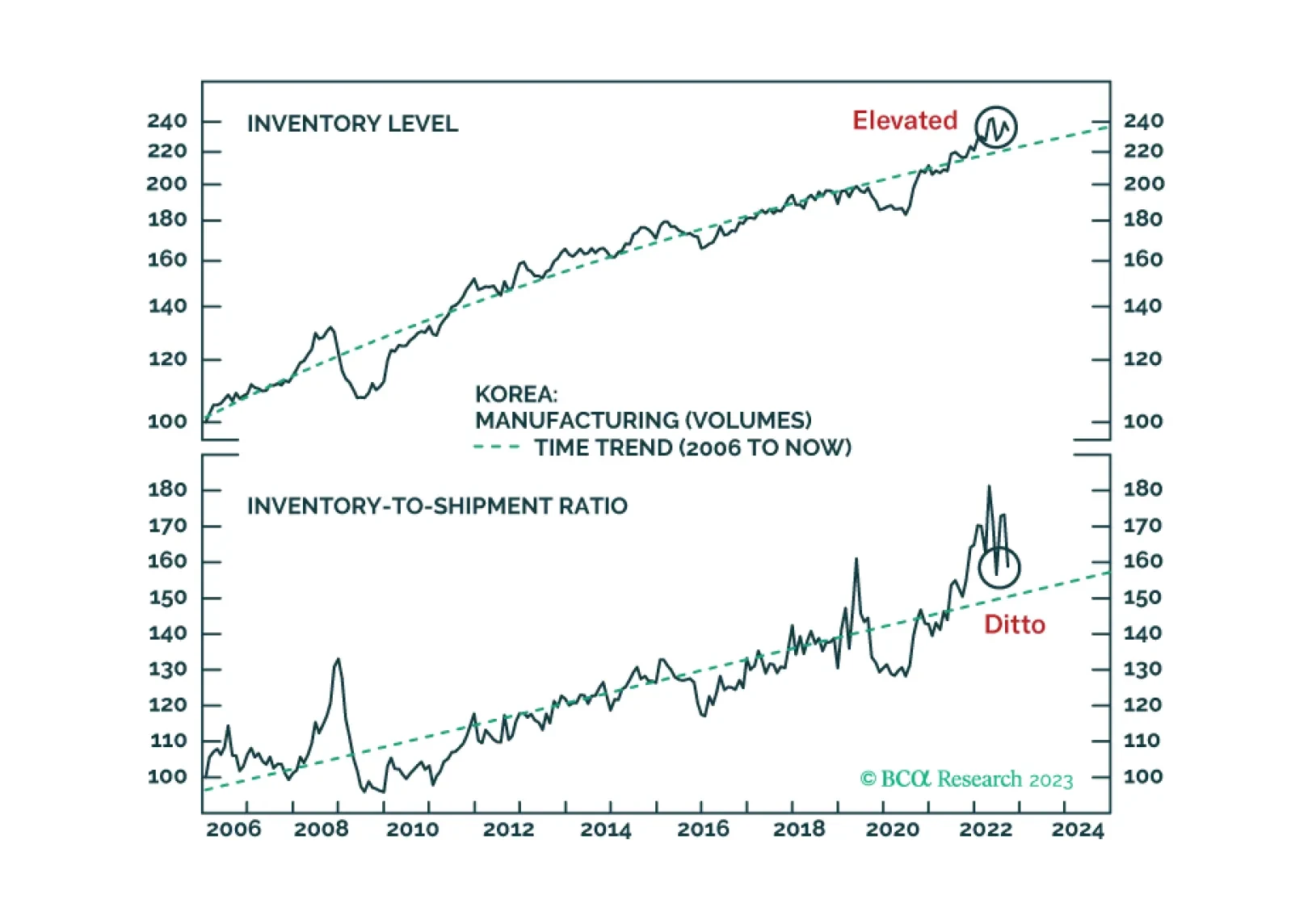

Contrary to the prevalent belief in the global investment community, goods/merchandise inventories in the US and East Asia are rather elevated. Financial markets respond to final demand fluctuations, not inventory restocking. Global manufacturing/trade will continue contracting, even though the pace of contraction might moderate in the near run. We recommend that investors fade the current rally.