Emerging Markets

China is trying to export its way out of its economic slowdown while the US has already formed a hawkish consensus on foreign policy and trade. Investors should take cover as global financial markets are underrating the new phase of the trade war, which will escalate from here.

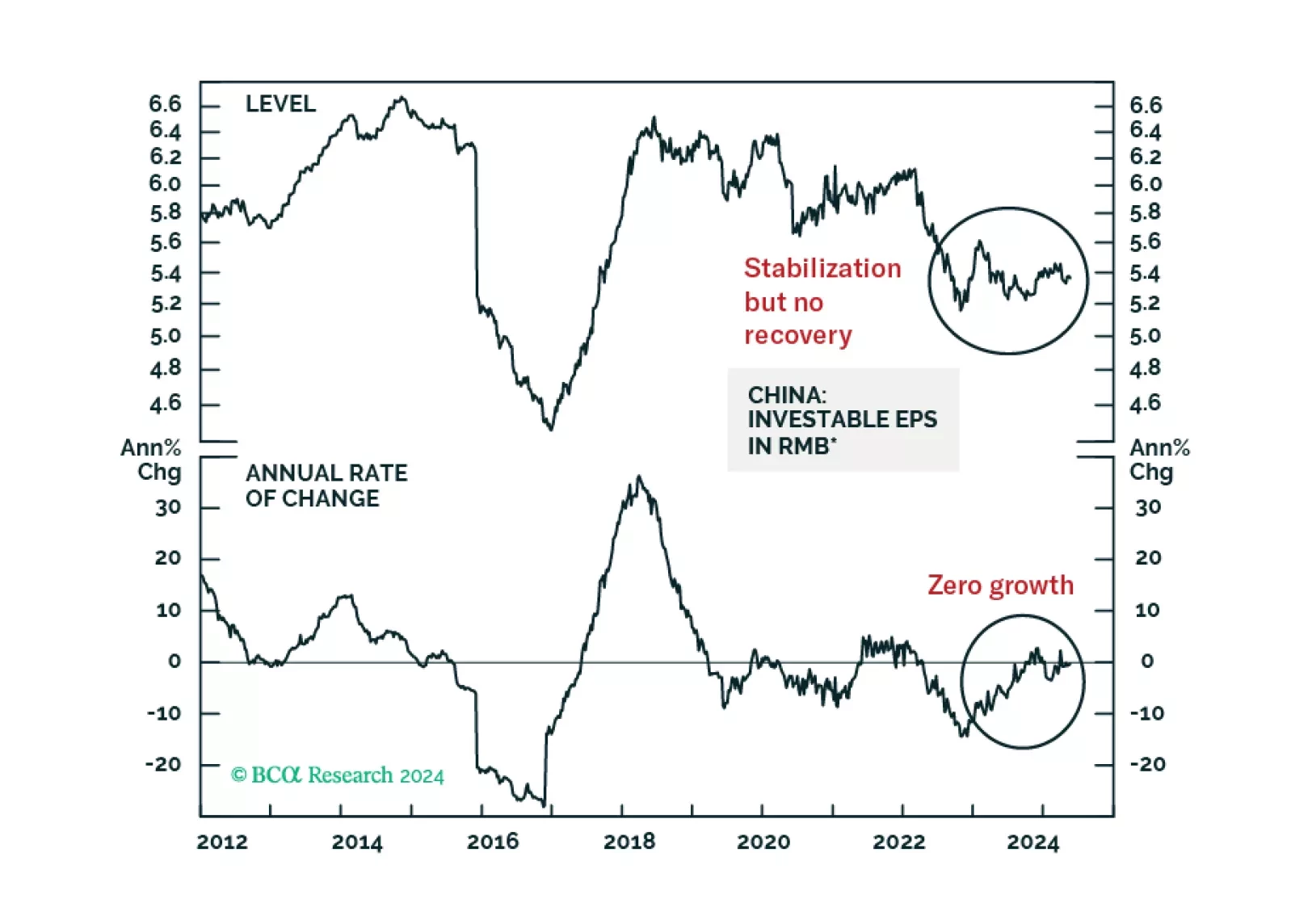

The RMB 500 billion program is small, as it is equivalent to only 4% of property developers' total funding from the past 12 months. This will preclude a recovery in property construction this year. Corporate profits will determine the path of China’s share prices on a cyclical time horizon. Deflation in China will persist for now, which will depress corporate profits even if volumes grow modestly.

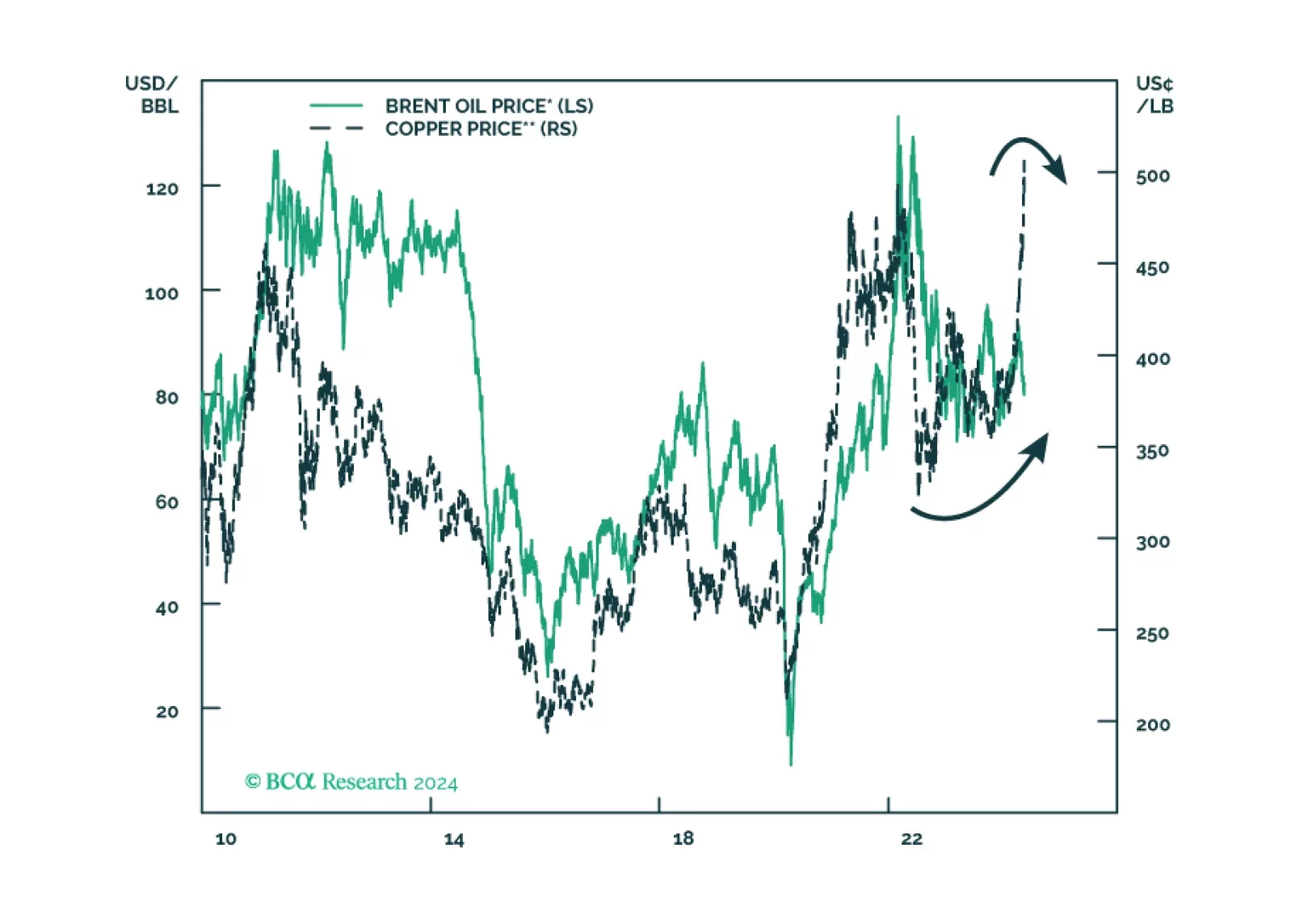

The death of the Iranian president reinforces our base case view of Middle Eastern instability and at least minor oil supply shocks. Rapid geopolitical developments in recent weeks are pointing to a new bout of global instability. The US is hobbled by its election. Conflicts with Russia, China, and Iran are all now escalating at the same time, at least marginally. Investors should reduce risk and shift to more defensive assets, markets, and sectors.

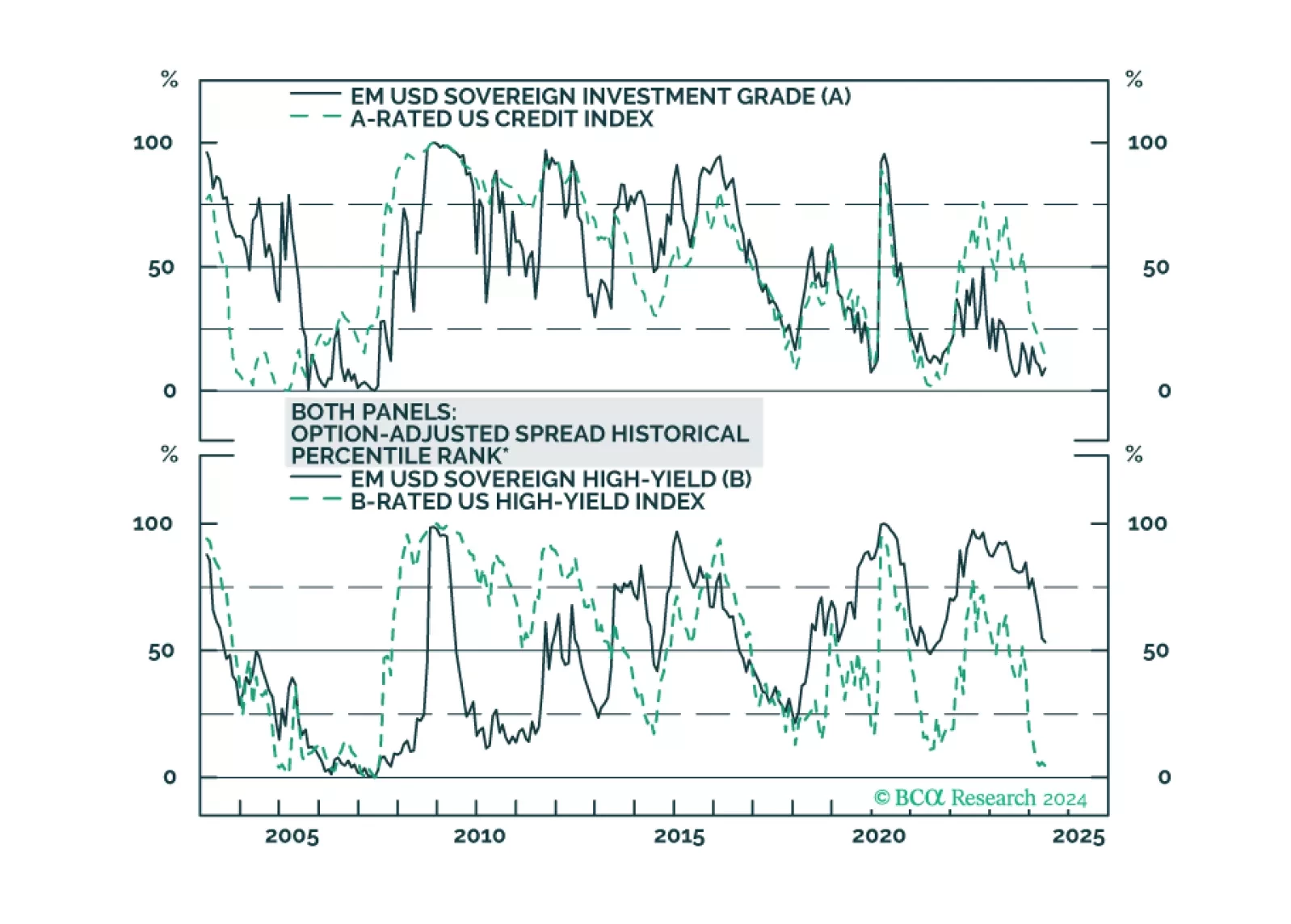

We dig into the USD-denominated Emerging Market Sovereign Index to see which credit tiers and countries offer value relative to US Credit.

The stock market will suffer a setback from the weakening labor market and a rebound in US and global policy uncertainty.