Electric Vehicles

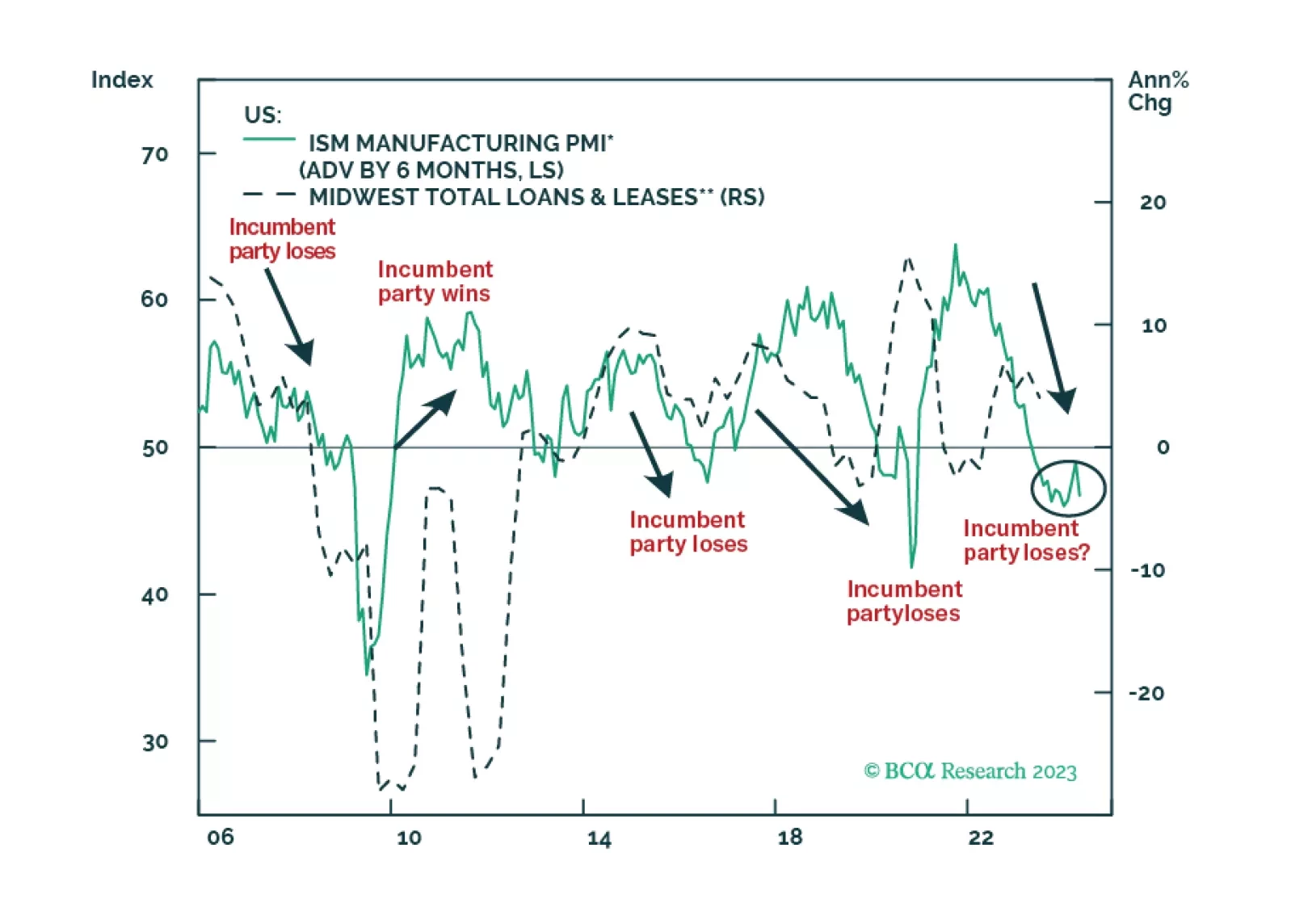

President Biden is facing foreign challenges on three fronts and these challenges are coalescing around the critical states of the Midwest. Take risks off the table and stay defensive in 2024.

The EU’s transition to a carbon tax launched this week via its Carbon Border Adjustment Mechanics (CBAM) will lead to higher inflation in the medium term (3 – 5 years out), and will stoke consumer (i.e., voter) antipathy if it becomes effective in 2026. As a result, the tax will be watered down. Food and energy prices are particularly at risk, as imported fertilizers, and electricity-generation and -transmission components made from steel and aluminum are affected by the CBAM. We remain long oil, gas and metals equity exposure via the XOP, XME and COMT ETFs. We also remain long gold to hedge inflation.

Investors remain cautious about the US economy and still have significant cash that needs to be put to work which could extend the rally further. Earnings rebound later in the year will be supported by rising sales growth and surging earnings of the Magnificent Seven. A restocking cycle, and a pickup in freight activity support transports. Upgrade Transports to an overweight.

Among the critical materials needed for the global energy transition, Li is expected to see the largest increase in demand from 2022 to 2050. Li supply is not constrained, but continued investment in mining and refining will be required to meet increasing demand. We expect strong Li-ion battery demand in the major economies of the world – the EU, US and China – will keep a bid under Li, and allow growing supply to find a home. At tonight’s close we are getting long the LIT ETF, consistent with our view.

Both EV and Green Energy themes still hold strategic promise for investors, posing large upside, despite prevailing macro headwinds. While both themes have yet to claw back their pandemic peaks, a broadening of the rally supports a run for both, even in the face of high valuations.

Oil and metals reacted positively to the PBOC's 10 bp cut in the seven-day reverse repo rate, which will be part of the larger monetary and fiscal support needed to revive the economy. While deposit rates at state-owned banks have been reduced, additional rate cuts are expected. On the fiscal side, tax breaks and credit support are planned for the domestic EV market, while authorities are reportedly mulling further assistance for the property market.

The CCP is poised to roll out a re-boot of China’s economy that will focus on its comparative advantage in the processing of base metals – particularly copper – and the export of metals-intensive products like EVs. The re-boot will emphasize deeper policy coordination to revive construction, manufacturing, exports and renewed efforts to attract and retain FDI. This will be bullish for commodities – particularly conventional energy and metals – as funding flows to SOEs.

Innovative Tech will face macroeconomic headwinds in a new “higher for longer” interest regime. Yet, the long-term opportunity of the cohort is tremendous. Investors need to be judicious with the timing of adding new capital to these themes to bolster long-term returns.

Global demand for new energy vehicles (NEVs) remains in a long-term uptrend, propelled by falling battery prices, improved driving range and an upgraded charging infrastructure. That said, diminishing policy support in China and Europe will spark a drop in the growth rate of global NEV sales to about 35% this year, down from about 60% last year. Global NEV-related stocks are likely to rise on a structural basis, but we recommend that investors wait for a better entry point given that valuations remain high.