Elections

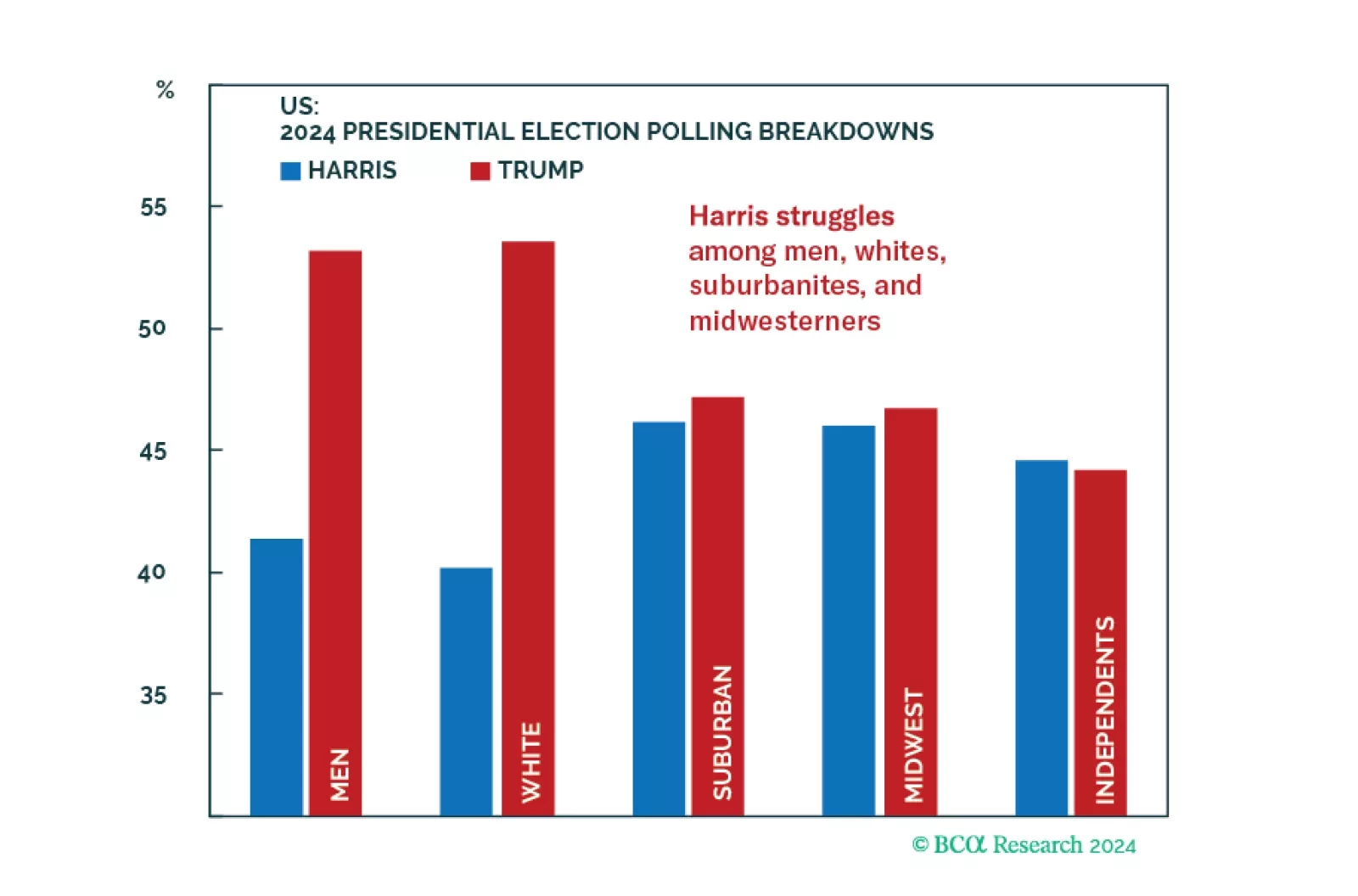

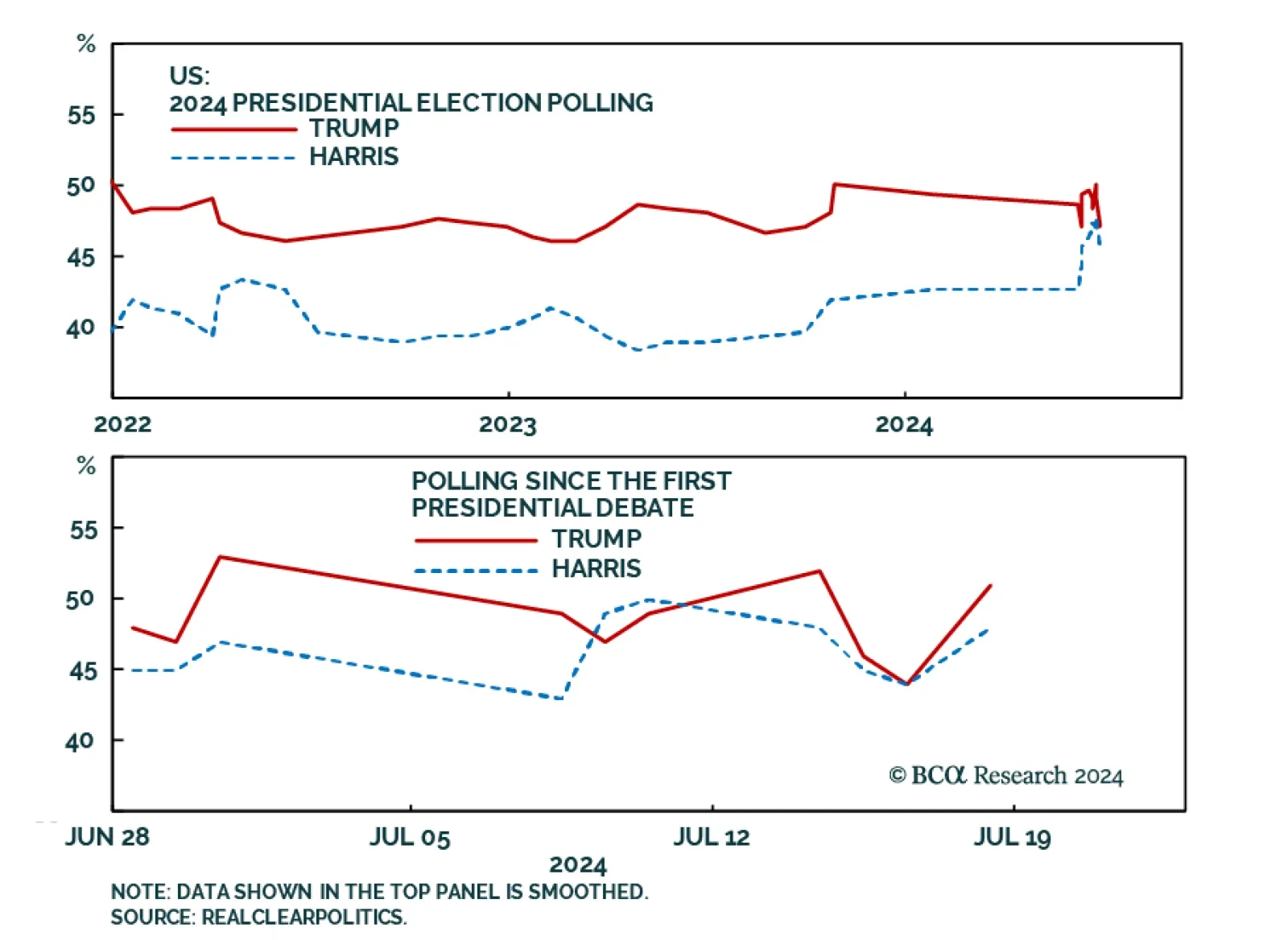

Harris picked Walz to patch up her weak side in the electorally vital Midwest. But the US election will continue to weigh on risk appetite, stocks, and high-beta assets because the odds of a single-party sweep are at least 50%, probably higher. Policy uncertainty and risk premiums will rise, not fall, in the coming months.

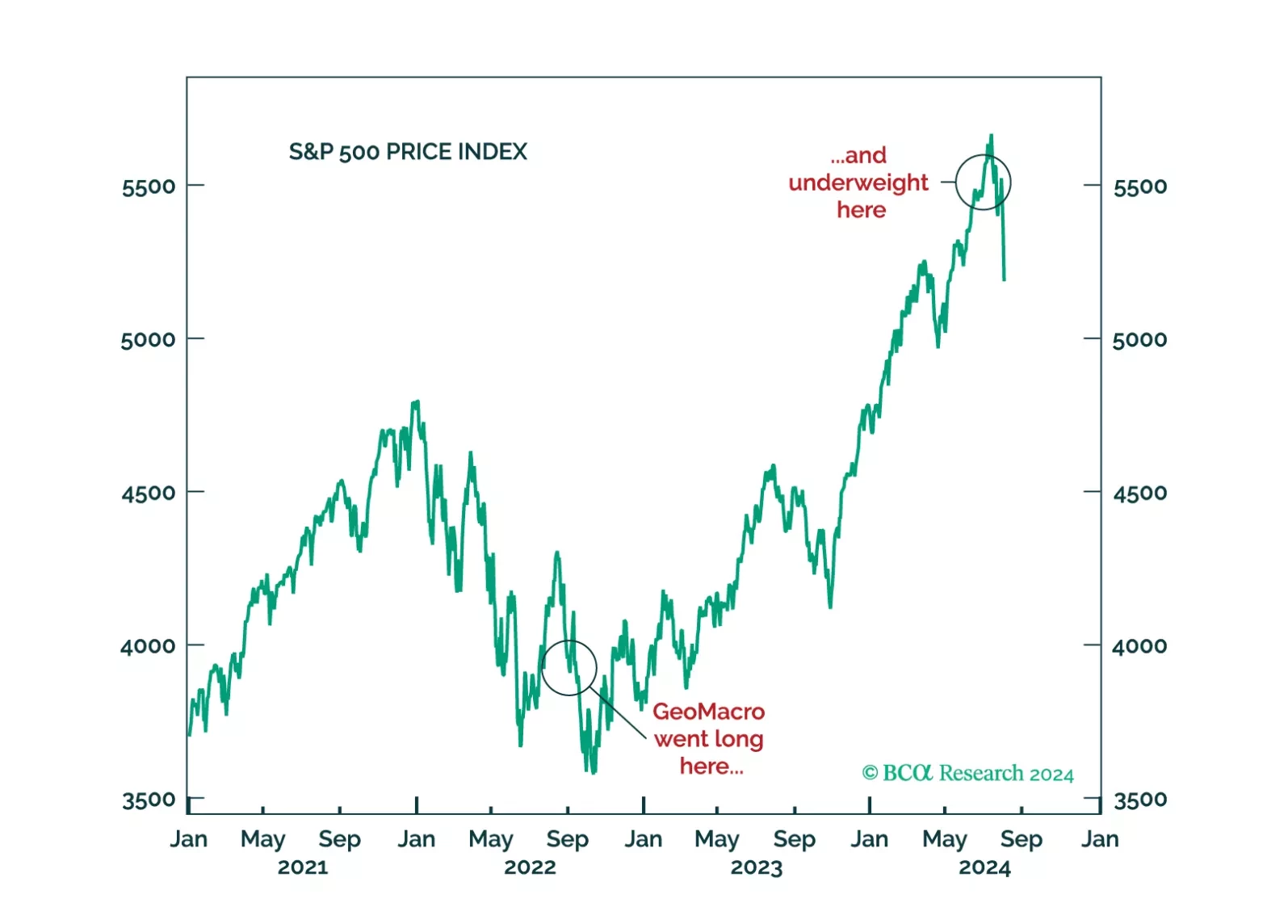

The decision by GeoMacro team on July 2 to short USDJPY and underweight equities has proven to be prescient. We still do not like the market setup from here on out. A recession would, obviously, be negative for risk assets. But even if investors avoid that scenario, the transition from cash- to leverage-driven growth is unlikely without a significant Fed rate-cutting cycle.

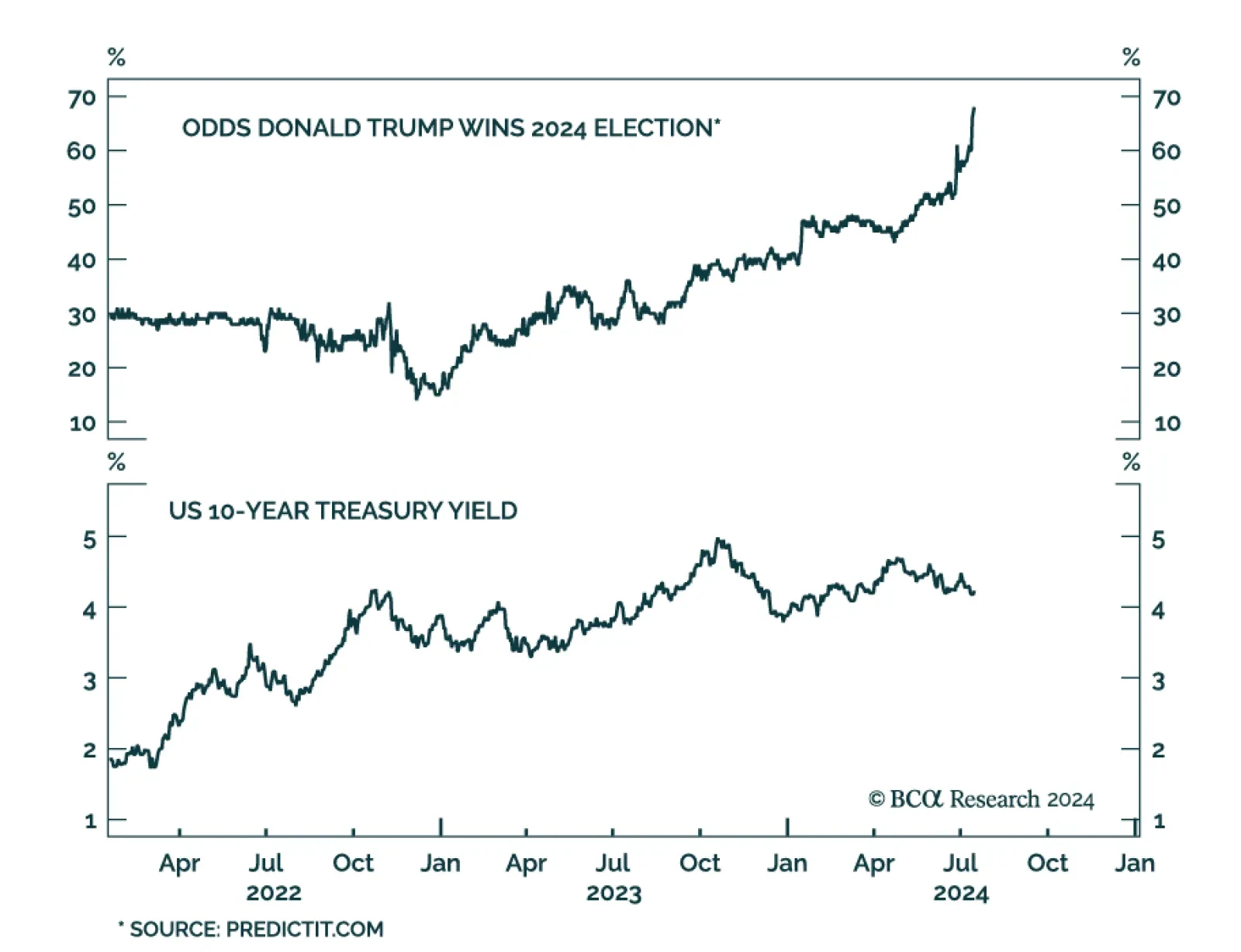

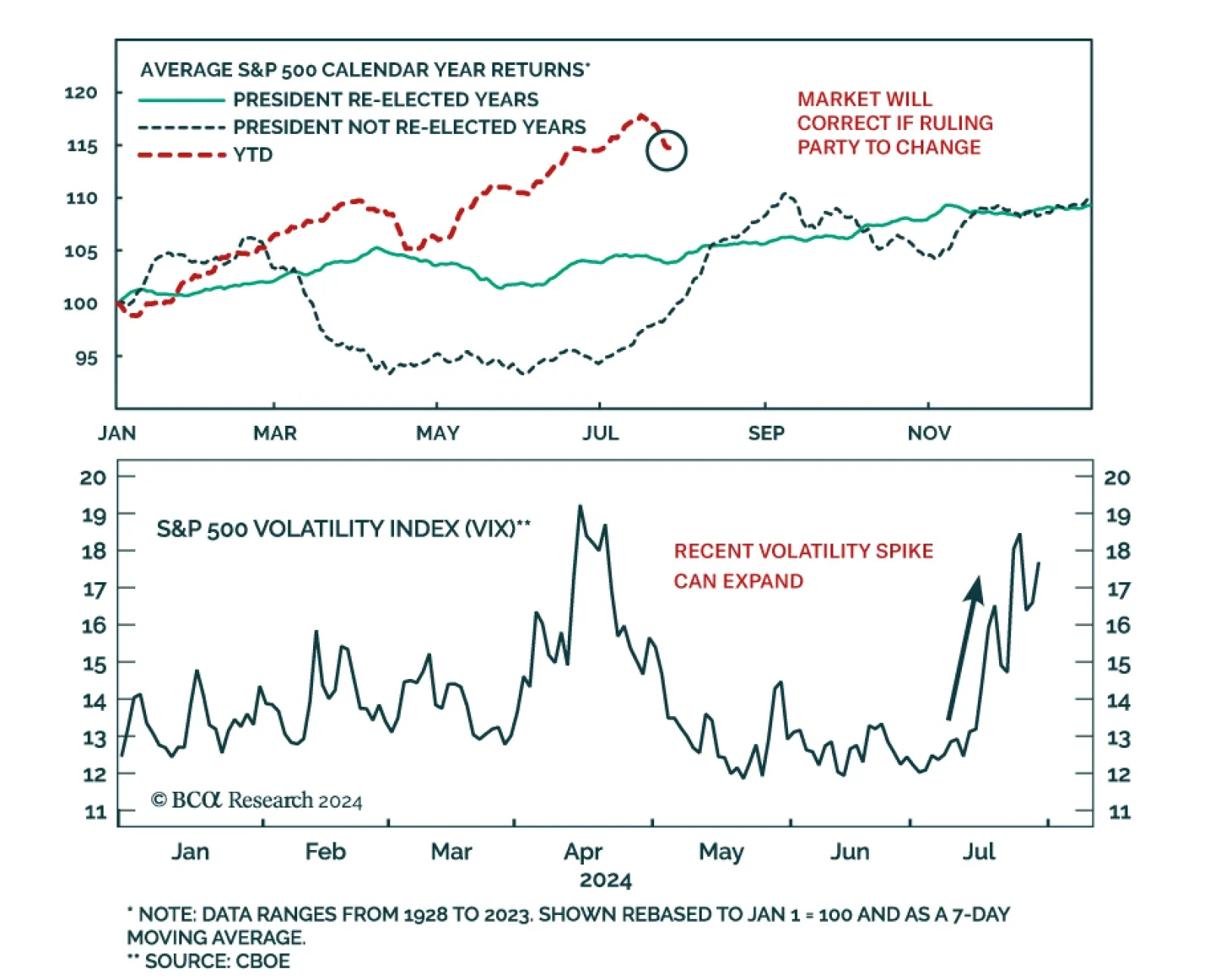

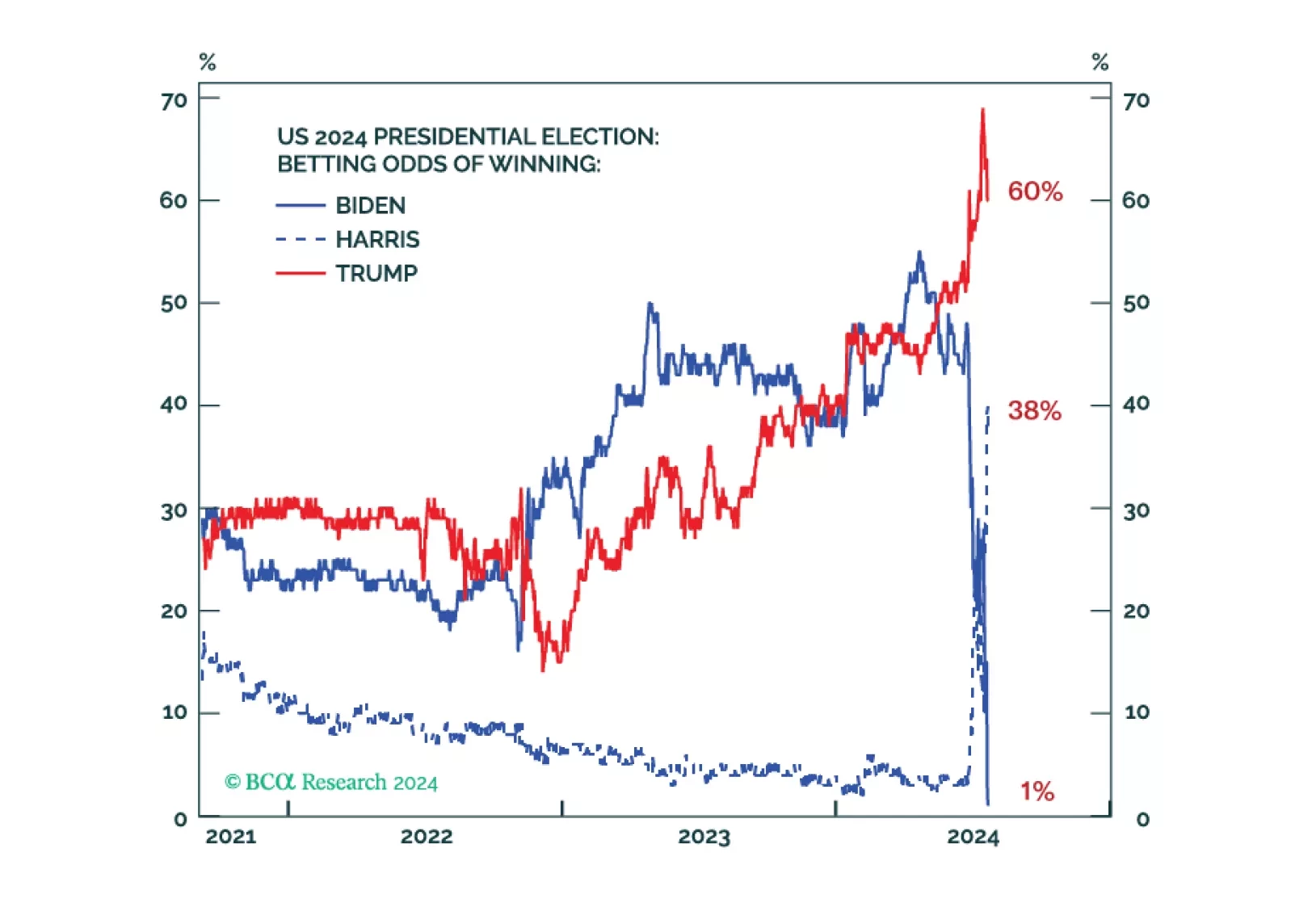

Republicans are favored but the election is still competitive. Equities, corporate credit, and cyclical sectors will fall until policy uncertainty is reduced.

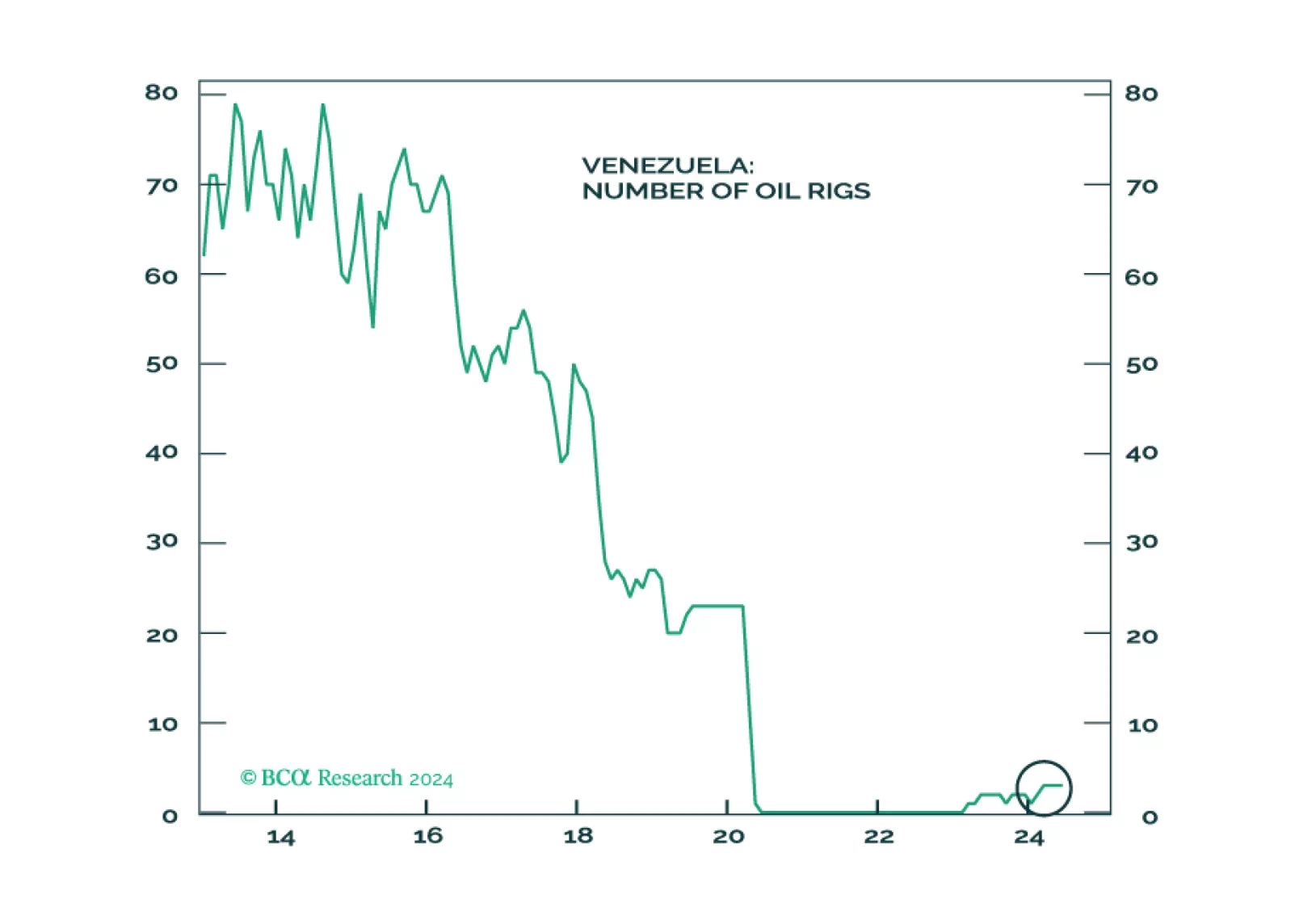

Oil markets will not be impacted by Venezuela in the near term, but by shocks from the Middle East. Maduro’s ability to stay in power in the short-term removes an avenue of oil supply relief. The same avenue is cut off if Trump is reelected. Geopolitical shocks in Venezuela could present tactical buying opportunities for Chile, Peru, and Colombia.

Investors should focus on growth concerns rather than the “Trump trade.” Bond yields will fall in the short run due to cyclically disinflationary economic slowdown, rather than rise in anticipation of a Republican full sweep and inflationary policies, which are likely but not yet a done deal.

As Trump’s victory odds rise, the underperformance of European equities deepens. How negative would a global trade war be for European assets?

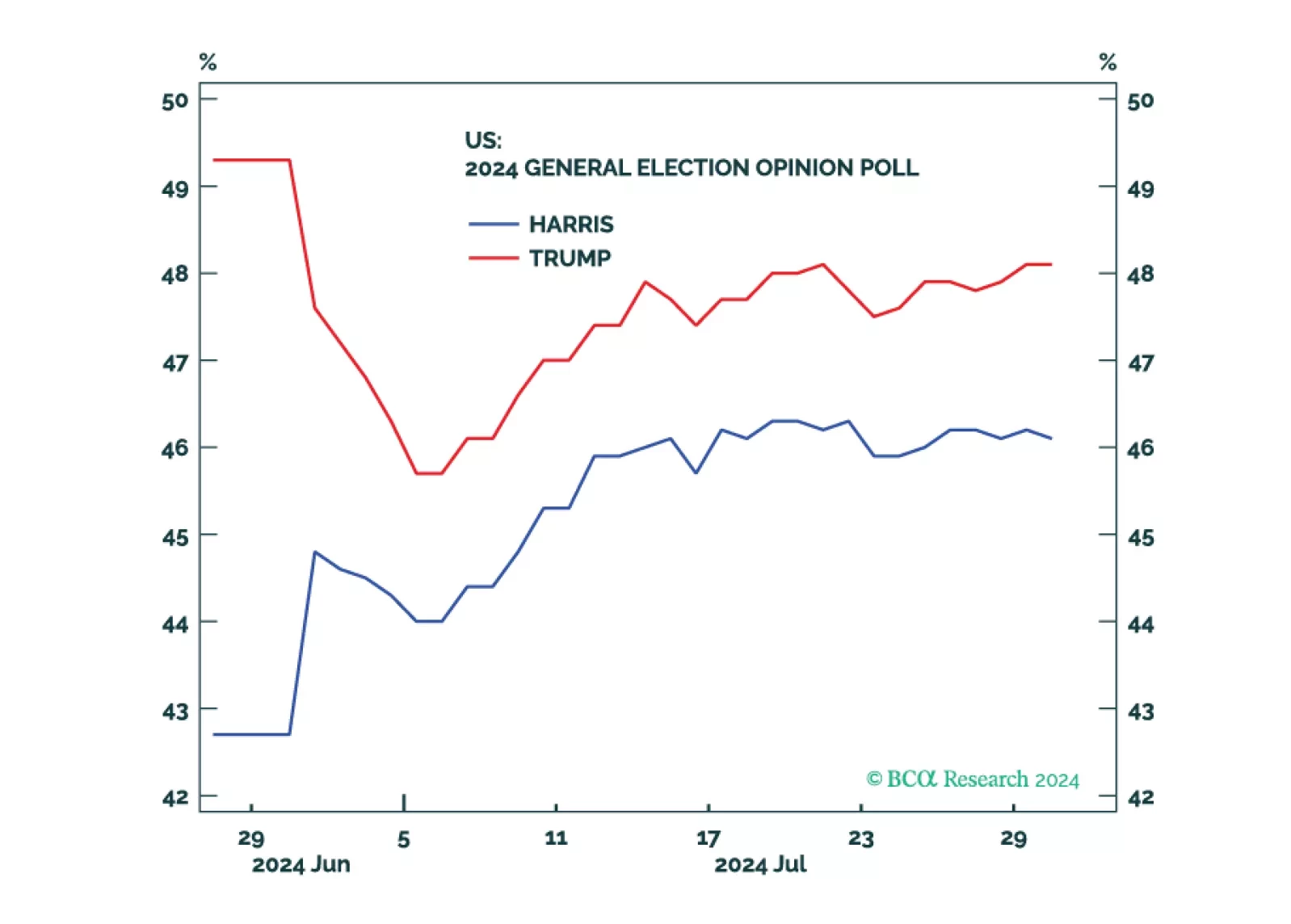

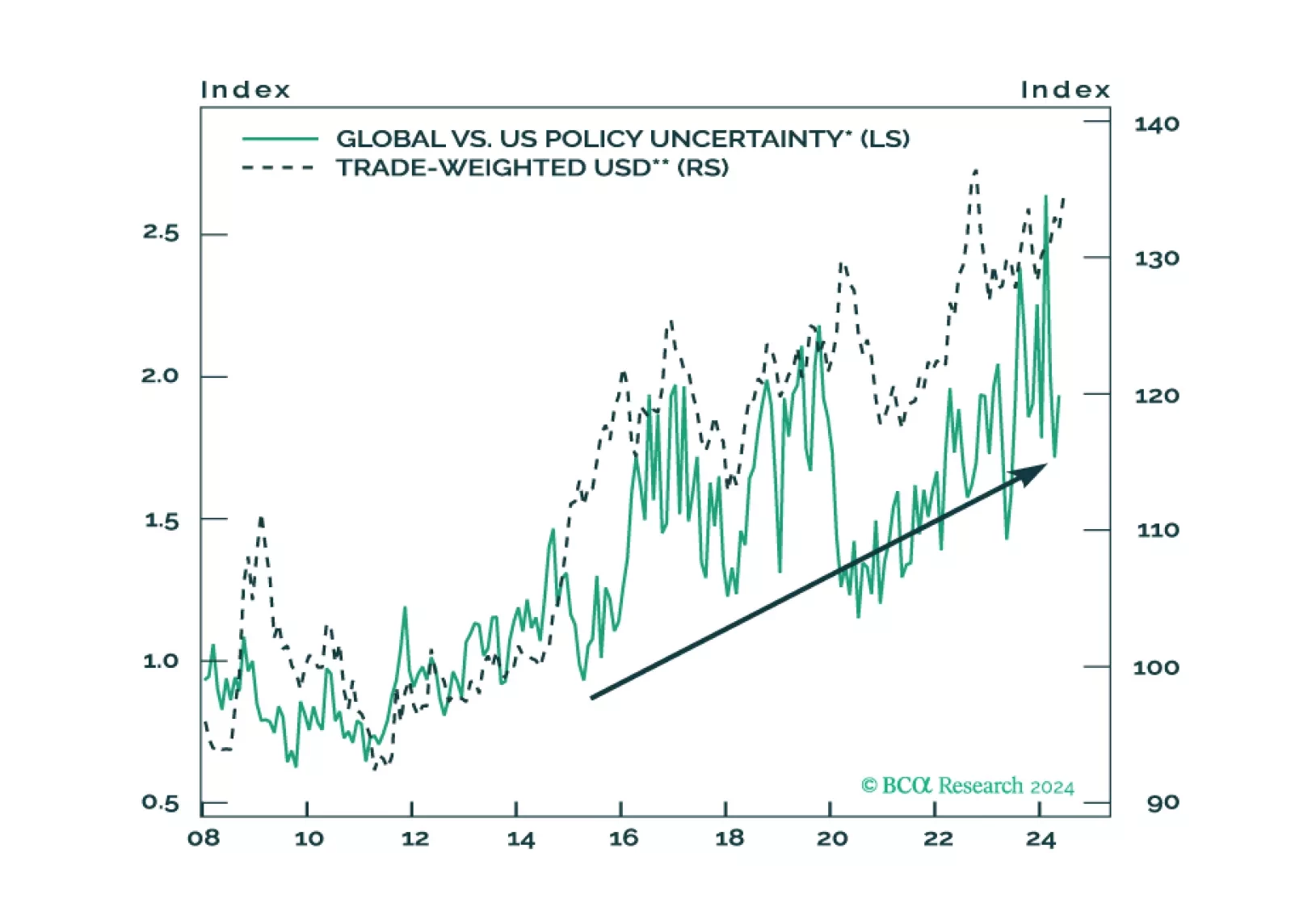

Investors should overweight US assets and de-risk their portfolios in anticipation of a major increase in policy uncertainty and geopolitical risk surrounding the US election and its global ramifications.