Elections

Highlights We remain bullish on global equities and spread product but acknowledge a variety of risks to our thesis. One such risk involves a scenario where a weaker U.S. economy hurts President Trump’s re-election prospects, causing investors to price in an Elizabeth Warren victory. According to the betting markets, she is the current front-runner for the Democratic nomination. A Warren presidency would likely be bad news for drug makers and health care insurers, defense contractors, banks, oil and gas companies (especially frackers), and tech stocks. Infrastructure and home builder stocks would probably benefit at the margin. Despite these risks, equity investors can take comfort in the following: 1) Global growth should strengthen, thanks in part to easier monetary policies; 2) China will be more keen to cut a trade deal with Trump if Warren looks like she will become the Democratic nominee; and 3) A Warren victory is less likely to translate into a Democratic takeover of the Senate than, say, a Biden victory. Feature The Warren Factor We remain bullish on global equities and other risk assets but continue to be on the lookout for evidence of any scenario that could undermine our thesis. One particular risk, which we explore in this week’s report, is the possibility that a weaker U.S. economy further undermines Donald Trump’s poll numbers, thus raising the odds that Democratic Senator Elizabeth Warren wins the White House next year. Presidential approval ratings tend to correlate well with the state of the economy (Chart 1). Since 1952, no sitting president has lost an election when unemployment has been falling except for Gerald Ford in the wake of Nixon’s scandal and unprecedented resignation. In contrast, two presidents (Jimmy Carter and George H.W. Bush) have lost against the backdrop of rising unemployment. Chart 1Incumbents Fare Better When The Economy Is Doing Well

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

President Trump’s approval ratings are quite poor given how low unemployment is these days. His perceived handling of the economy is the only area where he has continued to poll relatively well (Chart 2). If he were to lose his standing on this issue, his re-election prospects would deteriorate substantially. Chart 2Trump Gets Reasonably High Marks On His Handling Of The Economy, But Not Much Else

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

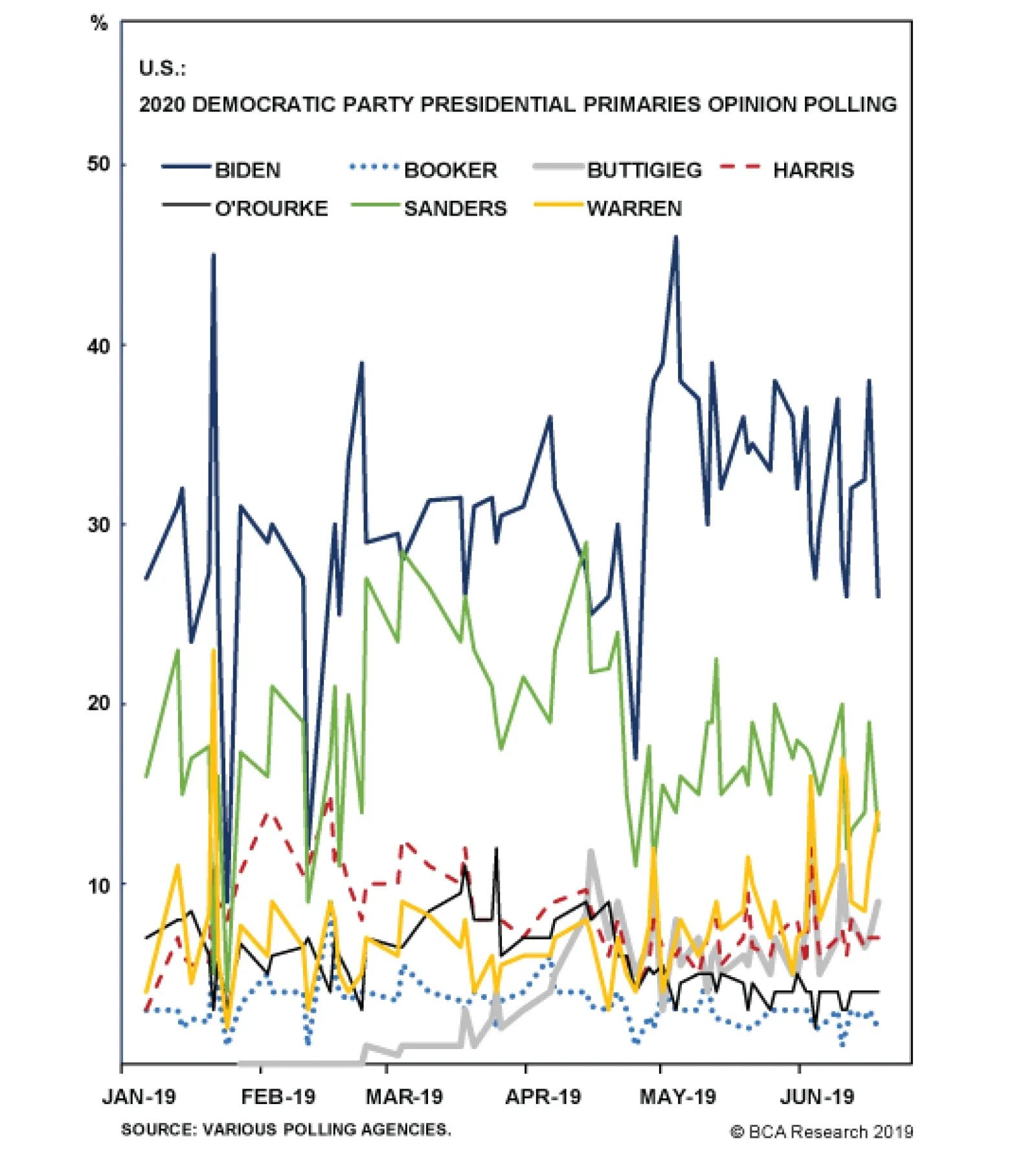

Among the Democratic contenders, Elizabeth Warren is currently running behind Joe Biden in the polls, but bests Biden in online betting markets such as PredictIt (Chart 3). It is not clear if Warren’s standing in the betting markets is a statistical anomaly or truly reflects the “wisdom of the crowds.” Warren tends to poll best among better-educated voters – the sort who are more likely to use betting markets. Like Andrew Yang, who PredictIt gives a rather dubious 12% chance of winning the Democratic nomination (above the 11% garnered by Kamala Harris), Warren’s prospects may be inflated by the composition of the betting pool. That said, Warren is benefiting from a deep-seated shift to the left in political preferences among Democratic primary voters, as BCA’s Geopolitical Strategy recently observed in a report entitled “American Politics Warrants Near-Term Caution.1” Chart 4 shows that the share of Democrats who identify as “liberal” has more than doubled since the mid-1990s at the expense of those who identify as “moderate” or “conservative.” The “Great Awokening” is transforming the Democratic Party into a much more radical force than it was under Bill Clinton or even, for that matter, under Barack Obama.2 Chart 3Who Will Win The 2020 Democratic Nomination?

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

Chart 4Democratic Party Shifting To The Left

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

Soak The Rich If Donald Trump was the right’s answer to populism, Warren, along with fellow traveler Bernie Sanders, is the left’s embodiment of the populist spirit. Not only has Warren pledged to raise the federal minimum wage to $15/hour, she has promised to roll back Trump’s corporate tax cuts. If that were not enough, she has also touted a 2% annual wealth tax on households with a net worth in excess of $50 million (rising to 3% for those with a net worth above $1 billon). Her team claims the wealth tax would bring in $2.75 trillion over a 10-year period (roughly 1% of GDP).3 It would help finance free universal health care coverage, fund a “Green New Deal,” and pay off most student loans. A Different Type Of Protectionist While Warren holds fairly protectionist views on international trade, they are qualitatively different from Trump's vision. Whereas Donald Trump has focused his efforts on reducing America’s bilateral trade deficits with other economies, Warren has concentrated on “social justice” issues. In the first few decades following World War II, trade agreements strove to cut tariffs and other overt trade barriers. Once this had been largely achieved, negotiations began to focus on fostering what trade economist Robert Lawrence has called “deep integration.” This involved harmonizing tax and regulatory policies across countries, strengthening intellectual property rules, and so on. Warren and other critics on the left have complained that this newfound emphasis of trade policy has helped multinational companies at the expense of ordinary workers. She has espoused creating prerequisites for all future trade agreements, including stronger protections for human rights, collective-bargaining, and environmental standards. Such preconditions would make it difficult for many countries, China included, to reach a deal with the U.S. on trade. What Warren Means For Investors Regardless of what one thinks about the overall merits of Elizabeth Warren’s political agenda, it is reasonable to conclude that equity investors would suffer if most of her preferred policies were implemented. In fact, as we were writing this report, Warren retweeted a CNBC story entitled “Wall Street executives are fearful of an Elizabeth Warren presidency” with a trollish comment saying “I’m Elizabeth Warren and I approve this message.”4 Box 1 reviews the impact of a Warren victory on various industries. Briefly stated, a Warren presidency would likely be bad news for drug makers and health care insurers, defense contractors, banks, oil and gas companies (especially frackers), and tech stocks. Infrastructure and home builder stocks would probably benefit at the margin. BOX 1 Elizabeth Warren’s Impact On U.S. Equity Sectors Negative Health care: Favors eliminating private health insurance; Backs price controls on pharmaceuticals; Advocates creating a government-owned pharmaceutical manufacturer to mass-produce generic drugs. Banks: Supports making it easier for individuals to file for bankruptcy; Would restore Glass-Steagall, effectively reversing some the mergers that took place during the financial crisis; Favors making private equity firms responsible for the debts of the companies they purchase as well as for some of their pension obligations. Defense: Has called for a smaller defense budget and promised to end “the stranglehold of … the so-called Big Five defense contractors.” Energy: Pledged to sign an executive order on her first day in office placing a complete moratorium on all new fossil fuel leases for offshore drilling and on public lands; Favors banning fracking everywhere and supports the introduction of a cross-border carbon tax. Tech: Anti-trust efforts are likely to be increased under a Warren administration. She has singled out Amazon, Facebook, and Google as companies she believes should be broken up. She recently added Apple to the list, citing her belief that the Apple app store unfairly gives an edge to Apple products. Marginally Positive Infrastructure: Infrastructure stocks (except for nuclear) would probably benefit from a Warren victory due to increased public-sector investment spending. Home builders: Home builders could gain from stepped-up efforts to expand home ownership. Warren is also in favor of decriminalizing illegal immigration which, despite her ostensible efforts to help blue collar workers, could dampen wage pressures in the construction sector. Despite these clear downside risks, we would dissuade investors from turning bearish on stocks right now. There are a few reasons for this. Global Growth Should Rebound Chart 5Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

Easier Financial Conditions Will Boost Global Growth

First and foremost, global growth is likely to stabilize over the coming months and rebound into yearend. Global financial conditions have loosened significantly, thanks in part to easier central bank policy (with the ECB’s rate cut and QE announcement this week being just the latest example). Looser financial conditions are positive for growth prospects (Chart 5). Manufacturing activity has been held back by weakness in the auto sector (Chart 6). Judging by the outperformance of auto stocks since mid-August (Chart 7), the auto recession may be coming to an end (we have been recommending global auto stocks since August 29). Chart 6Auto Sector: The Culprit Behind The Manufacturing Slowdown

Auto Sector: The Culprit Behind The Manufacturing Slowdown

Auto Sector: The Culprit Behind The Manufacturing Slowdown

Chart 7Global Auto Manufacturers: Better Times Ahead?

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

In the U.S., the economic surprise index has jumped firmly into positive territory (Chart 8). Real consumer spending is on track to rise by a sturdy 3.1% in Q3, according to the Atlanta Fed’s GDPNow model, following a blockbuster 4.7% reading in Q2. Given the decline in mortgage rates over the past few months, residential investment should also recover later this year (Chart 9). Chart 8U.S. Data Has Begun To Surprise On The Upside

U.S. Data Has Begun To Surprise On The Upside

U.S. Data Has Begun To Surprise On The Upside

Chart 9Lower Mortgage Rates Bode Well For Housing

Lower Mortgage Rates Bode Well For Housing

Lower Mortgage Rates Bode Well For Housing

Trump, Warren, And Trade The trade war represents the biggest risk to our sanguine outlook on global growth. Now that Trump has proven his credentials as “Tariff Man,” he has to prove that he is the “Master Negotiator” he claimed to be on the campaign trail. This means getting a deal done with China. As we saw with the revised NAFTA agreement, the new deal does not need to be radically different from the status quo for Trump to sell it as a game changer, and a 'win' for the American people. Trump’s decision to delay the October 1st tariff hikes by two weeks, following China’s announcement that it will waive tariffs on some U.S. imports, certainly moves things in the right direction. As we go to press, conflicting media reports are circulating that Trump is considering an interim trade deal that would delay and possibly roll back some U.S. tariffs in exchange for commitments from China to purchase more U.S. agricultural goods and better enforce intellectual property rights.5 If such an agreement materializes, it would be very much consistent with our expectation of a de-escalation in the trade war as the election approaches. How Warren’s ascent could alter the trade war calculus is unclear. On the one hand, given her own protectionist leanings, Trump may be reluctant to cede any ground to her by further softening his stance towards China. On the other hand, the Chinese are more likely to cut a deal with Trump if Biden’s star continues to fade, thus making it easier for Trump to secure an agreement. From China’s perspective, better the devil you know than the devil you don’t. On balance, we lean towards the latter theory, although much will depend on how the ongoing trade negotiations unfold. Trump Prefers Warren What does seem certain is that Trump’s re-election prospects are better if Warren gets the nomination than if Biden does. In head-to-head matchups against Trump, Biden outperforms Warren in the country as a whole, as well as in individual swing states (Chart 10). Chart 10Biden's Chances Of Beating Trump Are Better Than Warren’s

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

Even if Warren did become the nominee and went on to beat Trump, her margin of victory would be slimmer than Biden’s. This implies that she would have a smaller chance of bringing over the Senate to the Democratic side. Without Democratic control of the senate, the Republicans will thwart much of her agenda and many of the pro-business policies they have enacted will remain on the books. Investment Conclusions When it comes to investing, there is no shortage of risks to worry about. One way of benchmarking the degree to which stocks are discounting these risks is by estimating the equity risk premium. Today, equity risk premia remain fairly elevated, especially outside the United States (Chart 11). Chart 11AEquity Risk Premia Remain Quite High (I)

Equity Risk Premia Remain Quite High (I)

Equity Risk Premia Remain Quite High (I)

Chart 11BEquity Risk Premia Remain Quite High (II)

Equity Risk Premia Remain Quite High (II)

Equity Risk Premia Remain Quite High (II)

One can see this point by calculating how much various stock market indices would need to fall over, say, the next ten years for stocks to underperform bonds. Even if one were to assume that nominal dividend payments per share do not rise at all over the next decade, U.S. equities would still need to decline by more than 18% in real terms for stocks to underperform bonds. Japanese stocks would need to fall by 28%. Euro area stocks would need to drop by 41%. U.K. stocks would need to tumble by almost 60%! (Chart 12). Chart 12AStocks Need To Fall By A Considerable Amount For Bonds To Outperform Over A 10-Year Horizon (I)

Stocks Need To Fall By A Considerable Amount For Bonds To Outperform Over A 10-Year Horizon (I)

Stocks Need To Fall By A Considerable Amount For Bonds To Outperform Over A 10-Year Horizon (I)

Chart 12BStocks Need To Fall By A Considerable Amount For Bonds To Outperform Over A 10-Year Horizon (II)

Stocks Need To Fall By A Considerable Amount For Bonds To Outperform Over A 10-Year Horizon (II)

Stocks Need To Fall By A Considerable Amount For Bonds To Outperform Over A 10-Year Horizon (II)

To be sure, much of the relative attractiveness of stocks is a function of how low real yields are. In absolute terms, global equities are poised to deliver long-term real returns on par with their historic average. U.S. stocks should generate returns that are somewhat below their historic average given that they trade at premium to their global peers. Valuations are mainly useful for gauging the long-term outlook for assets. Over a horizon of around 12 months, cyclical factors are the dominant drivers of both stocks and bonds (Chart 13). The rebound in government bond yields since last Thursday has erased most of the extreme overbought conditions that prevailed in fixed-income markets. Nevertheless, as we highlighted in last week’s report entitled “Bond Yields Have Hit Bottom,” yields should move higher over the coming months as global growth picks up and inflation eventually rises.6 As a countercyclical currency, the dollar should also start to weaken later this year. The combination of stronger global growth and a weaker dollar will boost commodity prices, EM currencies and equities, and cyclical stocks. Industrials, materials, and energy stocks should all gain. Financials will also benefit from a modest resteepening of yield curves. Financials are overrepresented in value indices while tech is underrepresented. Indeed, a trade that is long the former while short the latter has tracked the value/growth split very closely (Chart 14). Value stocks are very cheap compared to growth stocks based on standard valuation measures such as price-to-earnings, price-to-book, and dividend yield. The outperformance of value stocks over the past few days versus both growth and momentum stocks is likely to continue. Chart 13Economic Growth Drives Stocks And Bonds Over 12-Month Horizons

Economic Growth Drives Stocks And Bonds Over 12-Month Horizons

Economic Growth Drives Stocks And Bonds Over 12-Month Horizons

Chart 14Is Value Turning The Corner?

Is Value Turning The Corner?

Is Value Turning The Corner?

Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Footnotes 1 Please see Geopolitical Strategy Weekly Report, “American Politics Warrants Near-Term Caution,” dated July 19, 2019. 2 Matthew Yglesias, “The Great Awokening,” Vox, April 1, 2019. 3 Please see Emmanuel Saez and Gabriel Zucman, January 18, 2019. 4 Elizabeth Warren, “I'm Elizabeth Warren and I approve this message,” Twitter, 10 September 2019, 2:39 pm. 5 Jenny Leonard and Shawn Donnan, “Trump Advisers Considering Interim China Deal to Delay Tariffs,” Bloomberg, September 12, 2019. 6 Please see Global Investment Strategy Weekly Report, “Bond Yields Have Hit Bottom,” September 6, 2019. Strategy & Market Trends MacroQuant Model And Current Subjective Scores

Elizabeth Warren And The Markets

Elizabeth Warren And The Markets

Strategic Recommendations Closed Trades

HighlightsEuropean fiscal stimulus will not drive European equity outperformance – Europe needs China to open the stimulus taps.Our mega-theme of European integration continues – the continent is politically stable.The U.S.-China trade war is an opportunity for Europe. Any Sino-American trade deal is unlikely to resolve tech disputes. Go long European tech stocks versus American.The euro has room to grow as a global reserve currency given the dollar’s mounting structural flaws. Look for an opportunity to go long EUR/USD on a strategic basis within the near future.FeatureTalk of European fiscal stimulus is accelerating as investors look for reasons to take advantage of depressed European valuations (Chart 1) and traditional late-cycle outperformance relative to the U.S. (Chart 2). We are skeptical of the thesis. Chart 1European 'Cheapness' An Obvious Inducement

European 'Cheapness' An Obvious Inducement

European 'Cheapness' An Obvious Inducement

Chart 2Euro Stocks Outperform Late In The Cycle

Euro Stocks Outperform Late In The Cycle

Euro Stocks Outperform Late In The Cycle

Europe is a price taker, not a price maker, when it comes to global growth. In order for investors to generate alpha from an overweight Europe position, the rest of the world needs to pick up the slack and reverse the current decline in economic fundamentals. That will require policy action on the behalf of the Fed, the Trump administration, and – most relevant to Europe – Chinese fiscal policy.That said, long-term investors should start thinking about increasing exposure to Europe. Not only is the continent well priced relative to the rest of the world, but it may have two more things going for it. First, political risks remain low. Second, Europe stands to gain in any prolonged China-U.S. confrontation. The flipside risk is that it stands to lose enormously in any temporary resolution as well.Europe Is A Derivative – Not A Source – Of Global Growth…Despite accounting for 16% of global GDP, the Euro Area generates an ever-shrinking proportion of the annual incremental change in global GDP (Chart 3). This is not surprising, given that the world has undergone significant transformation due to China’s industrialization and the growth of EM economies. Chart 3Europe’s Contribution To Global Growth Declining

Europe: Not A Price Maker

Europe: Not A Price Maker

China’s imports today drive Euro Area manufacturing PMI broadly and Chinese retail sales drive German manufacturing orders specifically (Chart 4). As such, it is critically important to watch Chinese total social financing (TSF) impulse, which closely leads Europe’s exports to China by six months (Chart 5). Chart 4Europe And Germany Rely On China

Europe And Germany Rely On China

Europe And Germany Rely On China

Chart 5China's Credit Cycle Drives EU Exports

China's Credit Cycle Drives EU Exports

China's Credit Cycle Drives EU Exports

The problem is that the Chinese credit impulse has only tepidly recovered and implies more downside to European exports ahead. In addition, hopes of a rebound in Chinese retail sales have been dashed (Chart 6). The jump in auto sales in June was the result of heavy discounts offered by manufacturers and dealers to clear inventory before new emission standards came into effect on July 1. Due to the frontloading, car sales are now declining in what is traditionally an off-season for car purchases in China. While the worst may be over, weakness could linger for months. Chart 6China's Retail Sales Flashing Red

China's Retail Sales Flashing Red

China's Retail Sales Flashing Red

The bottom line is that without an upturn in global growth, Europe will remain in the doldrums. The good news is that BCA’s Chief Strategist Peter Berezin expects precisely such a development in the second half of 2019.1 The bad news is that Chinese credit stimulus appears to be weighed down by a combination of impaired transmission mechanisms and policymaker unwillingness to launch an old-school credit orgy (Chart 7). This is creating a highly unusual – for this cycle – development where China is not playing its usual counter-cyclical role amidst the global manufacturing cycle (Chart 8). Chart 7China's Credit Stimulus Restrained Thus Far

China's Credit Stimulus Restrained Thus Far

China's Credit Stimulus Restrained Thus Far

Chart 8Beijing Goes On Strike As Global Spender

Beijing Goes On Strike As Global Spender

Beijing Goes On Strike As Global Spender

Without more Chinese stimulus, European fiscal spending won’t be that meaningful.As such, it is difficult to get excited about European growth. As we discussed in last week’s missive, Europe is moving gingerly towards more fiscal spending. However, it has already done so this year, with fiscal thrust at 0.46% of GDP, the highest figure since 2009 (Chart 9). Did anyone notice? Not really. Chart 9Headwinds Overpower EU's Strong Fiscal Thrust

Headwinds Overpower EU's Strong Fiscal Thrust

Headwinds Overpower EU's Strong Fiscal Thrust

Moreover Euro Area countries have to submit their 2020 budgets in early Q4 to the European Commission. It is unlikely that these proposals will be meaningful, given that there is not yet enough panic to spur massive stimulus.Bottom Line: Yes, Europe will provide more fiscal spending in 2020. But it will remain at the mercy of global growth given its high-beta nature.…But At Least It Is Not Falling Apart! That said, not all is disappointing on the Old Continent. For one, the aforementioned fiscal thrust at least prevented a deeper slowdown this year – and the drop-off in thrust next year will be less dramatic as budgets turn more accommodative.Meanwhile political risk is falling. Anti-establishment parties are either cleaning up their act, putting on a tie, and becoming part of the establishment, or they are losing power. Our long-held thesis that European integration would persist into the next decade remains well-supplied with empirical evidence.2On the Euroskepticism front, much of the hype today surrounds the collapse of the Five Star Movement (M5S) coalition with the League in Italy. The formerly Euroskeptic M5S has shed its critique of European integration and has decided to partner with the center-left and pro-establishment Democratic Party (PD).This is merely the tip of the iceberg. Several key developments throughout 2019 have signaled to investors that the Euroskeptic moment has passed. For a plethora of data and polling to support this view, please refer to our May report on the European Parliament (EP) election. Here we merely survey the latest developments:European Parliament Election: As expected in our EP election forecast, the May contest was a non-event. Support for the euro and the EU is trending higher (Chart 10 and 11), and 73% of Euroskeptic seats are held by Eastern European or U.K. MEPs (Chart 12), both irrelevant for EU policy.3 Chart 10Even Italy Swings In Favor Of Euro

Even Italy Swings In Favor Of Euro

Even Italy Swings In Favor Of Euro

Chart 11Public Opinion Supports The Union

Public Opinion Supports The Union

Public Opinion Supports The Union

Chart 12Euroskepticism Overstated

Europe: Not A Price Maker

Europe: Not A Price Maker

Random Elections: We rarely cover politics in Denmark or Finland, but the two Nordic countries have been at the forefront of the anti-establishment, right-wing, evolution in Europe. As such, the elections in Denmark (in June) and Finland (in April) were relevant. The Danish People’s Party (DPP) – one of the original “People’s Parties,” founded in 1995 – was massacred, losing 21 seats in the 179-seat legislature.In Finland, the moderately Euroskeptic Finns similarly saw a disappointing – if not as disastrous – performance.Finally, Austrian election on September 29 will likely see the other Europe’s prominent right-wing, Euroskeptic, party – the Freedom Party of Austria (FPO) – decline below 20% for the first time since 2008. Chart 13Macron Recovering In Polls

Macron Recovering In Polls

Macron Recovering In Polls

France: Our high conviction view in February that the Yellow Vest protest would ultimately dissipate proved correct. President Emmanuel Macron has also seen a recovery in polling. Although tepid, at least he appears to be diverging from the trajectory of his disastrously unpopular predecessor François Hollande (Chart 13).The good news for Macron is that he continues to lead Marine Le Pen by double digits in the theoretical 2022 second round. While this represents a considerable improvement for Le Pen from her 2017 performance, the fact is that she has had to adjust her policies and rebrand the National Front in order to close the gap with Macron. The party is now called the National Rally and has publicly revised its stance towards both the EU and the euro.4The events in France, Denmark, Finland, and Austria have largely gone unnoticed amidst the China-U.S. trade war, attacks against Federal Reserve independence, and general breakdown in global institutions and paradigms. But they reveal that Euroskepticism in Europe is evolving from a definitive one – in or out – to a much more nuanced position.For students of history, this is not a surprise. European integration has always been a push-pull process. Charles de Gaulle famously caused a total breakdown in integration during the 1965 “Empty Chair Crisis” when France recalled its representative in Brussels and refused to take its seat on the Council.De Gaulle was a Euroskeptic in so far as he believed that European integration was a national, not a supra-national process.5 It could proceed apace, but only if controlled by national capitals. As such, he warred with the Commission all the time. However, de Gaulle did not want to eliminate European integration as he understood its geopolitical and economic imperative. He simply wanted to shape the process to fit French interests.Absolutist Euroskepticism – the idea that all European institutions ought to be replaced by national ones – is an alien idea to the post-World War Two continent, one imported from the nineteenth century. The irony of Brexit, therefore, is that the most vociferous supporters of an absolute end to the EU integrationist project are now abandoning their fellow absolutists on the continent.Geopolitical and structural factors are also pushing European Euroskeptics to evolve from absolutists to modern-era Gaullists. We have identified most of these factors before, but they are worth repeating:Europe has a geopolitical imperative to integrate. In a multipolar world dominated by global powers like the U.S. and China – and with Russia, India, Japan, Iran, and Turkey playing an increasingly independent role – European states are not large enough on their own to defend their economic and geopolitical interests. Chart 14Geopolitical Forces Behind Integration

Geopolitical Forces Behind Integration

Geopolitical Forces Behind Integration

The purpose of integration is to aggregate the geopolitical power of Europe’s individual states amidst rising global multipolarity. Chart 14 is a stylized visualization of what European integration is attempting. It illustrates that the average BCA Geopolitical Power Index (GPI) score of an EMU-5 country is well below that of a BRIC state.6 By aggregating their geopolitical power, European states retain some semblance of relevance in the world.Obviously this is merely a thought experiment as European integration is not aggregation and never will be. Not only is aggregation politically unfeasible, but there is also a lot of double counting in simply adding GPI scores of European states. Nonetheless, the point is that European countries are asymptotically moving from the average to the aggregate score. Chart 15No Basis For Fascism In Great Recession

No Basis For Fascism In Great Recession

No Basis For Fascism In Great Recession

No, the Nazis are not coming. Europe has managed to recover from a generational financial crisis. Pessimists point to the depth of the crisis to explain why Europe is unsustainable, with angst matching the severity of the downturn. However, analogizing to the 1930s is folly. First, Europe’s shared memories of the ravages of populism act as antibodies preventing precisely the same infection from breaking out on the continent.7 Second, the European financial crisis was simply nowhere close to the depth of the Great Depression that rocked Germany as it descended into National Socialism (Chart 15). As for the argument that the European Central Bank fed populism through unorthodox policy easing, the tide of populism would have been much more formidable if Europe had been allowed to sink into deeper recession and deflation.Europeans are just not that desperate. Europe scores much better than the U.S. (or the U.K.) when it comes to the balance between the median income and middle-income share of total population. Chart 16 shows that most Euro Area economies have around 70% of their population in the middle-income bracket. Those that fall short nonetheless hug the line of best fit closely (Italy, Spain, Greece, and the Baltic States). The U.S., on the other hand, has one of the highest median income levels, but with barely 50% of the population considered in the middle-income. Meaning that a lot of the people below the median line are far below it. This is a recipe for actual populist political outcomes (President Trump), as opposed to artificial ones (Italy). Chart 16U.S. At Greater Risk Of Populism Than EU

Europe: Not A Price Maker

Europe: Not A Price Maker

European populism is artificial, U.S. populism is actual.What of the risks in Europe? For example, investors are concerned about mounting Target2 imbalances. Here we agree with our colleague Dhaval Joshi, who has pointed out that growing imbalances in Europe’s monetary system will only further constrain centrifugal forces among the nations.Target2 has seen a steady outflow of Italian cash to German banks as the ECB’s QE saw respective central banks purchase domestic bonds (Chart 17). This means that the Bank of Italy holds assets – BTPs – denominated in Italian euros, while the Bundesbank has a new liability to German banks denominated in German euros. EMU dissolution would be too painful due to this mismatch. Target2 is therefore not a threat to the EMU, but rather a Gordian Knot that can only be unraveled with immense pain and violence.That said, there may be an upcoming headline risk in Europe: the end of Chancellor Merkel’s reign. In our view, Merkel’s role in stabilizing Europe is greatly overstated. Her dithering and lack of conviction caused several crises to descend into chaos amidst the sovereign debt imbroglio. As such, an infusion of new blood will be positive for Europe. The populist threat is also overstated, with the Alternative for Germany (AfD) performing relatively tepidly in the polls. In fact, the liberal, Europhile, Greens are starting to gain votes (Chart 18). As such, an early election in Germany would create volatility and uncertainty but would not undermine our secular thesis on Europe. Chart 17Gordian Knot Supports Integration

Gordian Knot Supports Integration

Gordian Knot Supports Integration

Chart 18Germany Not Falling To Populism

Germany Not Falling To Populism

Germany Not Falling To Populism

Bottom Line: There is an ever-strengthening case for the sustainability of the Euro Area and European integration well into the next decade.From Geopolitical Gambit To A Geopolitical Safe-Haven?At this point, we have built a strong case for why Europe will remain a high-beta play on global growth that is unlikely to collapse. As such, investors should plow into Europe when the rest of the world is doing well with confidence that the continent will not descend into chaos.The U.S.- China trade war offers an intriguing opportunity for Europe.This is largely underwhelming as an investment thesis. Could there be something more exciting to the story given a slew of well-known headwinds to European growth from demographics, low productivity, and regulatory malaise?The trade war between the U.S. and China does offer an intriguing opportunity for Europe.There appears to be an interesting development where European equities outperform those of the U.S. during periods of trade war turbulence (Chart 19). The outperformance is not major, but it is highly counterintuitive. Chart 19Europe Outperforms Amid Trade War Shocks

Europe Outperforms Amid Trade War Shocks

Europe Outperforms Amid Trade War Shocks

As is understood, Europe is a high-beta play on global growth. Presumably, investors should abandon high-growth derivative plays when trade war accelerates. It is one of the reasons that EM equities and EM FX suffer whenever trade war accelerates.So why is Europe different? Because European exporters generally compete with their American counterparts (and Japanese and South Korean) for Chinese market share. And if China retaliates against U.S. companies, European companies stand to benefit, potentially massively.Take Boeing and Airbus. Boeing expects China to demand 7,700 new airplanes over the next two decades, an order valued at $1.2 trillion. It would be disastrous to the U.S. airline industry if the entirety of that order went to Airbus and its subsidiaries.8 According to the latest news reports, China has slowed down its airplane procurement to a crawl as it awaits the outcome of the dispute with the U.S.9 It is predictably using the procurement decision as leverage in the negotiations. Chart 20Europe To Lose If China Strikes U.S. Deal

Europe To Lose If China Strikes U.S. Deal

Europe To Lose If China Strikes U.S. Deal

Yet this “substitution effect” thesis is a double-edged sword for Europe. A resolution of the trade war between the U.S. and China would likely include a massive purchase of U.S. agricultural, commodity, and manufacturing goods: the so-called “Beef and Boeings” deal. China bears often point out that such a massive purchase will negatively impact China’s current account, which is barely in surplus thanks to China’s trade surplus with the U.S. (Chart 20). This is false. Chinese policymakers are not suicidal. The last thing China needs is a balance of payments crisis due to a trade deal with the U.S.China would simply rob Peter to pay Paul, pulling its orders of soy from Brazil and Airbus from Europe in order to make a deal with the U.S. As such, it is highly likely that European capital goods exporters would suffer in any trade war resolution between China and the U.S.That said, a substantive trade deal that resolves all U.S.-China tensions is extremely unlikely. The U.S. and China are not just commercial rivals, they are also geopolitical rivals. As such, the tech conflict between the U.S. and China will continue well beyond any resolution of the trade war. This could create an opportunity for Europe’s traditionally beleaguered tech stocks to finally outperform their American counterparts (Chart 21). Chart 21Go Long EU Tech Versus U.S. Tech

Go Long EU Tech Versus U.S. Tech

Go Long EU Tech Versus U.S. Tech

Bottom Line: A deterioration of the U.S.-China trade relationship would be a boon for European exporters. Short of a total breakdown of U.S.-China trade, however, European tech stocks may finally begin outperforming their U.S. counterparts thanks to the open distrust between U.S. and China.In addition, U.S. technology firms are likely going to face a slew of regulatory challenges over the next decade. While not necessarily negative, these challenges will nonetheless create new headwinds for the sector.10 We are therefore initiating a structural theme of being long European tech relative to U.S.Investment ImplicationsAre there any broader themes to be extracted from the combined geopolitical forecasts presented in this report? Europe will not collapse, and it may benefit from the souring of U.S.-China geopolitical and economic relations.Long euro is an obvious theme. As our colleague Dhaval Joshi has recently pointed out, the chasm between monetary policies of the Fed and the ECB has become a major geopolitical risk. This is because it has depressed the euro versus the dollar by at least 10 percent – based on the ECB’s own competitiveness indicators. The exchange rate distortion stemming from polarized monetary policies is the culprit for the euro area’s huge trade surplus with the United States (Chart 22).In the short term, EUR/USD may have reached its practical (and geopolitically acceptable) lows. Yes, the ECB is readying another round of monetary stimulus on September 12, but the fiscal policy counterpart is likely to be tepid and thus fail to (yet again) take advantage of historically depressed borrowing costs on the continent. The September 12 ECB meeting may therefore be a “sell the rumor, buy the news” event for EUR/USD. Chart 22Monetary Policy Accounts For Bilateral Surplus

Monetary Policy Accounts For Bilateral Surplus

Monetary Policy Accounts For Bilateral Surplus

Chart 23U.S. Rivals Buying Gold, Ditching Dollar

U.S. Rivals Buying Gold, Ditching Dollar

U.S. Rivals Buying Gold, Ditching Dollar

On the more cyclical and secular horizon, we see an opportunity for the euro to reestablish some of its lost reserve currency status due to the geopolitical conflict between China and the U.S. Washington’s willingness to use trade and financial sanctions for geopolitical benefit has given pause to central bank authorities around the world in using dollars as a reserve currency. Purchases of gold for FX reserve have surged, particularly among America’s geopolitical rivals (Chart 23), as our colleague Chester Ntonifor has recently pointed out.As we argued in a report entitled “Is King Dollar Facing Regicide?” the euro has some catch-up potential. In 1990, the combined currencies of the countries that today comprise the Euro Area accounted for 35% of total composition of global currency reserves. Today, the figure is merely 20% (Chart 24). Chart 24Euro Has Plenty Of Room To Grow As Reserve Currency

Europe: Not A Price Maker

Europe: Not A Price Maker

Could Europe supply the world with enough euros to replace USD as a reserve currency? This is highly unlikely. However, at the margin, an expansion of European liquidity is possible, particularly if Germany finally learns to love fiscal expansion and if European policymakers capitulate on the issuance of Eurobonds. However, such a lack of euro liquidity is not negative for the euro. The world could soon experience a situation where the demand for non-USD liquid assets dramatically increases due to the politicization of America’s reserve currency status while the supply of USD-alternatives remains relatively low. This should be positive for the only true alternative to the USD as a global reserve currency: the euro.As such, we will be looking to initiate a strategic long EUR/USD position, potentially sometime this fall as the ECB and FOMC meetings take place and the risk of a no-deal Brexit is averted. We do not expect the massive monetary policy divergence between Europe and the U.S. to continue, while the Euro Area’s political stability, and the broader geopolitical demand for a non-USD reserve currency, create more long-term tailwinds for the euro.Marko PapicConsulting Editor, BCA Research Chief Strategist, Clocktower GroupHousekeepingOur high-conviction view that no-deal Brexit odds were overrated has been confirmed by the recent events in the U.K. parliament. We are going long GBP-USD with a tight stop-loss of 3%. Since we expect further volatility – with an election likely and the Conservative Party performing well in the polls and monopolizing the Brexit vote in a first-past-the-post system – we will sell at the $1.30 mark.Footnotes1 Please see Global Investment Strategy, “Trade War: The Storm Before The Calm,” dated August 9, 2019, available at gis.bcaresearch.com.2 Please see Geopolitical Strategy, “Europe's Geopolitical Gambit: Relevance Through Integration,” dated November 3, 2011, available at gps.bcaresearch.com.3 The reason we extracted the U.K. Euroskeptics from the calculation is because with Brexit nigh, the U.K. members of European Parliament are no longer policy relevant. As for Central European Euroskeptics, we extracted them because they are irrelevant for EU policy as they hail from member states that – in truth – nobody seriously thinks would ever leave the EU.4 Ahead of the May EP election, National Rally electoral platform focused on “local, ecological, and socially responsible production." The party advocates combining environmentalism with protectionism, creating an ecological custom barrier at the EU’s doorstep which would defend the European market from products manufactured or produced with less environmentally friendly processes. On the matters of EU membership, the party now advocates a more traditionally Euroskeptic line, a purely Gaullist form of Euroskepticism that seeks to curb – or, at best, abolish – the EU Commission and replace its legislative prerogative by giving the Council of the EU all legislative powers. 5 Please see Julian Jackson, De Gaulle (Cambridge, MA: Harvard UP, 2018).6 We chose to use EMU-5 in the chart because it focuses on the top-five economies in the Euro Area: France, Germany, Italy, Spain, and the Netherlands. If we focused on the overall average EMU score, even one we weighed by population, the results would be even more stark in terms of loss of importance.7 And, worryingly, the U.S. lacks precisely the same shared memory of how wild pendulum swings of polarization can descend into extreme nationalism or left-wing extremism.8 Airbus would not have the capacity to fulfill that entire order today. However, demand creates its own supply, giving Airbus a reason to surge capex and reap the profits.9 Please see Reuters, “Exclusive: Boeing CEO eyes major aircraft order under any U.S.-China trade deal.”10 Please see Geopolitical Strategy, “Is The Stock Rally Long In The FAANG?,” dated August 1, 2018 and “Surviving A Breakup: The Investor’s Guide To Monopoly-Busting In America,” dated March 20, 2019, available at gps.bcaresearch.com.

Highlights An inevitable and imminent U.K. general election will be one of the most unpredictable and ‘non-linear’ elections ever. This non-linearity makes it difficult to take a high-conviction view on sterling’s direction because a tiny vote swing in one direction or another could be the difference between a no-deal Brexit – and the pound below parity against the euro – or a solid coalition for remain – and the pound at €1.30. Instead, a good strategy is to buy sterling volatility on the announcement of the election. The easiest way to implement this is simultaneously to buy at-the-money call and put options (versus either the euro or dollar). In a soft Brexit or remain, the U.K. equity sectors most likely to outperform the overall market are real estate and general retailers. In a hard Brexit, a U.K. sector likely to outperform the overall market is clothing and accessories. Feature Chart of the WeekSterling Volatility Could Go Up A Lot

Sterling Volatility Could Go Up A Lot

Sterling Volatility Could Go Up A Lot

Lyndon B Johnson famously said that that the first rule of politics is to learn to count. A government is a lame duck if it does not have a majority of legislators to drive and set its policy. Fifty years on, LBJ’s namesake is learning this first rule of politics. Boris Johnson is running a minority U.K. government. The irony is that this makes it impossible for a pro-Brexit Johnson to pass legislation for the Brexit process itself! Ending the free movement of EU citizens was supposedly one of the biggest ambitions of the Brexit vote. But astonishingly, even after a no-deal Brexit, free movement would not end – because EU law continues to apply until its legal foundation is repealed. The U.K. government wanted to end free movement through a new law, the immigration bill, but the proposed legislation, along with several other key new laws, cannot make it through parliament. The Most Non-Linear Election Looms The only way out of the impasse is to change the parliamentary arithmetic via a snap general election. The trouble is that the outcome of such an election is near impossible to predict. This is because the U.K.’s first past the post electoral system is designed for a head-to-head between two dominant parties. But right now, there are four parties in play – from left to right: Labour, Liberal Democrat, Conservative, and Brexit. While in Scotland, the SNP is resurgent. Making the next U.K. general election one of the most unpredictable and ‘non-linear’ elections ever. The outcome of a snap general election is near impossible to predict. For example, in the recent Brecon and Radnorshire by-election, the 10 percent of votes that went to the Brexit party syphoned just enough ‘leave’ votes from the Conservatives to hand the seat to the Lib Dems. Repeated nationwide, such a swing could inflict mortal damage to the Conservatives. On the other hand, the staunchly pro-remain Lib Dems could also syphon crucial votes from a Labour party that is prevaricating on its Brexit policy. Understanding this, Johnson isn’t using the next election to resolve Brexit; quite the opposite, he is using Brexit to resolve the next election – in his favour – with the ancient strategy of ‘divide and rule’. Unite ‘leave’ by tacking to the hard right, and divide ‘remain’ between Labour, Lib Dem, Green, SNP, and Plaid Cymru. However, it is a very risky strategy. A small but critical rump of Brexit party voters are diehard anti-establishment rather than pure leave votes; furthermore, remainers almost certainly will vote tactically as they did in 2017 when they obliterated the Conservatives’ overall majority. For U.K. investments, the inevitable imminent election dominates all other considerations, as its outcome will determine the U.K.’s ultimate trading relationship with the EU and rest of the world, as well as establish the U.K’s overarching economic policy and strategy. But to reiterate, the outcome is highly non-linear. A tiny vote swing in one direction or another could be the difference between a no-deal Brexit – and the pound below parity against the euro – or a solid coalition for remain – and the pound at €1.30, as sterling’s ‘Brexit discount’ is unwound (Chart I-2 and Chart I-3). Chart I-2Sterling's Brexit Discount Is 15 Percent, Based On Real Interest Rate Differentials...

Sterling's Brexit Discount Is 15 Percent, Based On Real Interest Rate Differentials...

Sterling's Brexit Discount Is 15 Percent, Based On Real Interest Rate Differentials...

Chart I-3...And Expected Interest Rate ##br##Differentials

...And Expected Interest Rate Differentials

...And Expected Interest Rate Differentials

The non-linearity makes it difficult to take a high-conviction view on sterling’s direction. Instead, as soon as an election is announced, a good strategy is to buy sterling volatility. Although it has risen recently, sterling volatility is only in the foothills relative to the heights of 2016, meaning plenty of upside (Chart I-1). The easiest way to implement this is simultaneously to buy at-the-money call and put options (versus either the euro or dollar). Brexit Investments A common question we get is what are the most Brexit-impacted investments, in both directions? As mentioned, the most obvious is sterling. Relative to the established relationship with interest rate differentials prior to the Brexit vote in 2016, the pound now carries a Brexit discount of around 15 percent. For U.K. investments, the inevitable imminent election dominates all other considerations. Related to this, the FTSE100 has outperformed the Eurostoxx600. This is exactly as theory would suggest. The FTSE100 and Eurostoxx600 are just a collection of global multi-currency earning companies quoted in pounds and euros respectively. So when sterling weakens, the multi-currency earnings increase more in FTSE100 index terms than in Eurostoxx600 index terms, resulting in FTSE100 outperformance (Chart I-4). Chart I-4The FTSE100 Outperforms When Sterling Weakens

The FTSE100 Outperforms When Sterling Weakens

The FTSE100 Outperforms When Sterling Weakens

Turning to U.K. equity sectors, those most likely to outperform the overall market in a soft Brexit are real estate and general retailers (Chart I-5 and Chart I-6). Chart I-5U.K. Real Estate Outperforms In A Soft Brexit

U.K. Real Estate Outperforms In A Soft Brexit

U.K. Real Estate Outperforms In A Soft Brexit

Chart I-6U.K. General Retailers Outperform In A Soft Brexit

U.K. General Retailers Outperform In A Soft Brexit

U.K. General Retailers Outperform In A Soft Brexit

While a sector likely to outperform the overall market in a hard Brexit is clothing and accessories (Chart I-7). Chart I-7U.K. Clothing And Accessories Could Outperform In A Hard Brexit

U.K. Clothing And Accessories Could Outperform In A Hard Brexit

U.K. Clothing And Accessories Could Outperform In A Hard Brexit

Four Disruptors Revisited The final section this week revisits the wider context for Brexit and other recent examples of populism. Specifically, they are backlashes to four structural disruptors to economies and financial markets. Disruptor 1: Protectionism. Since the Great Recession, an extremely polarised distribution of economic growth has left many people’s standard of living stagnant – despite seemingly decent headline economic growth and job creation (Chart I-8). Chart I-8Disruptor 1: Income Inequality Leads To Protectionism

Disruptor 1: Income Inequality Leads To Protectionism

Disruptor 1: Income Inequality Leads To Protectionism

Looking to find a scapegoat, economic nationalism and protectionism have resonated very strongly with voters in several major economies: the U.S., U.K., Italy, and Brazil. Other voters could follow in the same vein. But history teaches us that protectionism ends up hurting many more people than it helps. Disruptor 2: Technology. The bigger danger is that the malaise is being misdiagnosed. Many middle-income job losses are not due to globalization, but due to technology. A polarised distribution of economic growth has left many people’s standard of living stagnant. Specifically, Artificial Intelligence (AI) is replacing secure middle-income jobs and displacing workers into insecure low-income manual jobs – like bartending and waitressing – which AI cannot (yet) replace (Table I-1). And AI’s impact on middle-income jobs is only in its infancy.1 The worry is that by misdiagnosing the illness as globalization and wrongly responding with protectionism, the illness will get worse, rather than improve. Table I-1Disruptor 2: Technology

Brexit: Rock Meets Hard Place

Brexit: Rock Meets Hard Place

Disruptor 3: Debt super-cycles have reached exhaustion. Protectionism carries a further danger. Just like developed economies did a decade ago, major emerging market economies are now coming to the end of structural credit booms and need to wean themselves off their credit addictions (Chart I-9). At this point of vulnerability, aggressive protectionism risks tipping these emerging economies into a sharp slowdown. Chart I-9Disruptor 3: Debt Super-Cycles Have Reached Exhaustion

Disruptor 3: Debt Super-Cycles Have Reached Exhaustion

Disruptor 3: Debt Super-Cycles Have Reached Exhaustion

Disruptor 4: Financial markets are richly valued. Disruptors one, two and three come at a time when equities are valued to generate feeble total nominal returns over the next decade (Chart I-10). Extremely compressed risk premiums are justified so long as bond yields remain ultra-low. Otherwise, the rich valuations will come under pressure. Chart I-10Disruptor 4: Financial Markets Are Richly Valued

Disruptor 4: Financial Markets Are Richly Valued

Disruptor 4: Financial Markets Are Richly Valued

The long-term investment message is crystal clear. With the four disruptors in play, we strongly advise long-term investors not to follow passive (equity) index-tracking strategies. Instead, we advise long-term investors to follow bespoke structural investment themes as shown in our structural recommendations section. Please note that owing to my travelling there is no fractal trading system this week. Normal service will resume next week. Dhaval Joshi, Chief European Investment Strategist dhaval@bcaresearch.com Footnotes 1 Please see the European Investment Strategy Special Report ‘The Superstar Economy: Part 2’ January 19, 2017 available at eis.bcaresearch.com Cyclical Recommendations Structural Recommendations Closed Fractal Trades Trades Closed Trades Asset Performance Currency & Bond Equity Sector Country Equity Indicators Bond Yields Chart II-1Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-2Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-3Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Chart II-4Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Indicators To Watch - Bond Yields

Interest Rate Chart II-5Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-6Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-7Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Chart II-8Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Indicators To Watch - Interest Rate Expectations

Highlights While a self-fulfilling crisis of confidence that plunges the global economy into recession cannot be excluded, it is far from our base case. Provided the trade war does not spiral out of control, it is highly likely that global equities will outperform bonds over the next 12 months. The auto sector has been the main driver of the global manufacturing slowdown. As automobile output begins to recover later this year, so too will global manufacturing. Go long auto stocks. As a countercyclical currency, the U.S. dollar will weaken once global growth picks up. We expect to upgrade EM and European equities later this year along with cyclical equity sectors such as industrials, energy, and materials. Financials should also benefit from steeper yield curves. We still like gold as a long-term investment. However, the combination of higher bond yields and diminished trade tensions could cause bullion to sell off in the near term. As such, we are closing our tactical long gold trade for a gain of 20.5%. Feature “The Democrats are trying to 'will' the Economy to be bad for purposes of the 2020 Election. Very Selfish!” – @realDonaldTrump, 19 August 2019 8:26 am “The Fake News Media is doing everything they can to crash the economy because they think that will be bad for me and my re-election” – @realDonaldTrump, 15 August 2019 9:52 am Bad Juju Chart 1Spike In Google Searches For The Word Recession

A Psychological Recession?

A Psychological Recession?

President Trump’s remarks, made just a few days after the U.S. yield curve inverted, were no doubt meant to deflect attention away from the trade war, while providing cover for any economic weakness that might occur on his watch. But does the larger point still stand? Google searches for the word “recession” have spiked recently, even though underlying U.S. growth has remained robust (Chart 1). Could rising angst induce an actual recession? Theoretically, the answer is yes. A sudden drop in confidence can generate a self-fulfilling cycle where rising pessimism leads to less private-sector spending, higher unemployment, lower corporate profits, weaker stock prices, and ultimately, even deeper pessimism. Two things make such a vicious cycle more probable in the current environment. First, the value of risk assets is quite high in relation to GDP in many economies (Chart 2). This means that any pullback in equity prices or jump in credit spreads will have an outsized impact on financial conditions. Chart 2The Total Market Value Of Risk Assets Is Elevated

The Total Market Value Of Risk Assets Is Elevated

The Total Market Value Of Risk Assets Is Elevated

Chart 3Not Much Scope To Cut Rates

Not Much Scope To Cut Rates

Not Much Scope To Cut Rates

Second, policymakers are currently more constrained in their ability to react to adverse shocks, such as an intensification of the trade war, than in the past. Interest rates in Europe and Japan are already at zero or in negative territory (Chart 3). Even in the U.S., the zero-lower bound constraint – though squishier than once believed – remains a formidable obstacle. Chart 4 shows that the Federal Reserve has cut rates by over five percentage points, on average, during past recessions. It would be impossible to cut rates by that much this time around if the U.S. economy were to experience a major downturn. Chart 4The Fed Is Worried About The Zero Bound

The Fed Is Worried About The Zero Bound

The Fed Is Worried About The Zero Bound

Fiscal stimulus could help buttress growth. However, both political and economic considerations are likely to limit the policy response. While China is stimulating its economy, concerns about excessively high debt levels have caused the authorities to adopt a reactive, tentative approach. Japan is set to raise the consumption tax on October 1st. Although a variety of offsetting measures will mitigate the impact on the Japanese economy, the net effect will still be a tightening of fiscal policy. Germany has mused over launching its own Green New Deal, but so far there has been a lot more talk than action. President Trump floated the idea of cutting payroll taxes, only to abandon it once it became clear that the Democrats were unwilling to go along. On The Positive Side Despite these clear risks, we are inclined to maintain our fairly sanguine 12-to-18 month global macro view. There are a number of reasons for this: First, the weakness in global manufacturing over the past 18 months has not infected the much larger service sector (Chart 5). Even in Germany, with its large manufacturing base, the service sector PMI remains above 50, and is actually higher than it was late last year. This suggests that the latest global slowdown is more akin to the 2015-16 episode than the 2007-08 or 2000-01 downturns. Chart 5AThe Service Sector Has Softened Much Less Than Manufacturing (I)

The Service Sector Has Softened Much Less Than Manufacturing (I)

The Service Sector Has Softened Much Less Than Manufacturing (I)

Chart 5BThe Service Sector Has Softened Much Less Than Manufacturing (II)

The Service Sector Has Softened Much Less Than Manufacturing (II)

The Service Sector Has Softened Much Less Than Manufacturing (II)

Second, manufacturing activity should benefit from a turn in the inventory cycle over the remainder of the year. A slower pace of inventory accumulation shaved 90 basis points off of U.S. growth in the second quarter and is set to knock another 40 basis points from growth in the third quarter, according to the Atlanta Fed GDPNow model. Excluding inventories, U.S. GDP growth would have been 3% in Q2 and is tracking at 2.7% in Q3 – a fairly healthy pace given the weak global backdrop (Chart 6). Chart 6The U.S. Economy Is Still Holding Up Well

A Psychological Recession?

A Psychological Recession?

Outside the U.S., inventories are making a negative contribution to growth (Chart 7). In addition to the official data, this can be seen in the commentary accompanying the Markit manufacturing surveys, which suggest that many firms are liquidating inventories (Box 1). Falling inventory levels imply that sales are outstripping production, a state of affairs that cannot persist indefinitely. Third, and related to the point above, the automobile sector has been the key driver of the global manufacturing slowdown. This is in contrast to 2015-16, when the main culprit was declining energy capex. According to Wards, global vehicle production is down about 10% from year-ago levels, by far the biggest drop since the Great Recession (Chart 8). The drop in automobile production helps explain why the German economy has taken it on the chin recently. Chart 7Inventories Are Making A Negative Contribution To Growth

Inventories Are Making A Negative Contribution To Growth

Inventories Are Making A Negative Contribution To Growth

Chart 8Auto Sector: The Culprit Behind The Manufacturing Slowdown

Auto Sector: The Culprit Behind The Manufacturing Slowdown

Auto Sector: The Culprit Behind The Manufacturing Slowdown

Importantly, motor vehicle production growth has fallen more than sales growth, implying that inventory levels are coming down. Despite secular shifts in automobile ownership preferences, there is still plenty of upside to automobile usage. Per capita automobile ownership in China is only one-fifth of what it is in the United States, and one-fourth of what it is in Japan (Chart 9). This suggests that the recent drop in Chinese auto sales will be reversed. As automobile output begins to recover later this year, so too will global manufacturing. Investors should consider going long automobile makers. Chart 10 shows that the All-Country World MSCI automobiles index is trading near its lows on both a forward P/E and price-to-book basis, and sports a juicy dividend yield of nearly 4%.1 Chart 9The Automobile Ownership Rate Is Still Quite Low In China

The Automobile Ownership Rate Is Still Quite Low In China

The Automobile Ownership Rate Is Still Quite Low In China

Chart 10Auto Stocks Are A Compelling Buy

A Psychological Recession?

A Psychological Recession?

Fourth, our research has shown that globally, the neutral rate of interest is generally higher than widely believed. This means that monetary policy is currently stimulative, and will become even more accommodative as the Fed and a number of other central banks continue to cut rates. Remember that unemployment rates have been trending lower since the Great Recession and have continued falling even during the latest slowdown, implying that GDP growth has remained above trend (Chart 11). As diminished labor market slack causes inflation to rebound from today’s depressed levels, real policy rates will decline, leading to more spending through the economy. Chart 11Unemployment Rates Keep Trending Lower

Unemployment Rates Keep Trending Lower

Unemployment Rates Keep Trending Lower

The Trade War Remains The Biggest Risk The points discussed above will not matter much if the trade war spirals out of control. It is impossible to know what will happen for sure, but we can deduce the likely course of action based on the incentives that both sides face. President Trump has shown a clear tendency in recent weeks to try to de-escalate trade tensions whenever the stock market drops. This is not surprising: Despite his efforts to deflect blame for any selloff on others, he knows full well that many voters will blame him for losses in their 401(k) accounts and for slower domestic growth and rising unemployment. What about the Chinese? An increasing number of pundits have warmed up to the idea that China is more than willing to let the global economy crash if this means that Trump won’t be re-elected. If this is China’s true intention, the Chinese will resist making any deal, and could even try to escalate tensions as the U.S. election approaches. It is an intriguing thesis. However, it is not particularly plausible. U.S. goods exports to China account for 0.5% of U.S. GDP, while Chinese exports to the U.S. account for 3.4% of Chinese GDP. Total manufacturing value-added represents 29% of Chinese GDP, compared to 11% for the United States. There is no way that China could torpedo the U.S. economy without greatly hurting itself first. Any effort by China to undermine Trump’s re-election prospects would invite extreme retaliatory actions, including the invocation of the War Powers Act, which would make it onerous for U.S. companies to continue operating in China. Even if Trump loses the election, he could still wreak a lot of havoc on China during the time he has left in office. Moreover, as Matt Gertken, BCA’s Chief Geopolitical Strategist, has stressed, if Trump were to feel that he could not run for re-election on a strong economy, he would try to position himself as a “War President,” hoping that Americans rally around the flag. That would be a dangerous outcome for China. Chart 12Would China Really Be Better Off Negotiating With A Democrat As President?

Would China Really Be Better Off Negotiating With A Democrat As President?

Would China Really Be Better Off Negotiating With A Democrat As President?

In any case, it is not clear whether China would be better off with a Democrat as president. The popular betting site PredictIt currently gives Elizabeth Warren a 34% chance of winning, followed by Joe Biden with 26%, and Bernie Sanders with 15% (Chart 12). This means that two far-left candidates with protectionist leanings, who would stress environmental protection and human rights in their negotiations with China, have nearly twice as much support as the former Vice President. All this suggests that China has an incentive to de-escalate the trade war. Given that Trump also has an incentive to put the trade war on hiatus, some sort of détente between the U.S. and China, as well as between the U.S. and other players such as the EU, is more likely than not. Investment Conclusions Provided the trade war does not spiral out of control, it is very likely that global equities will outperform bonds over the next 12 months. Since it might take a few more months for the data on global growth to improve, equities will remain in a choppy range in the near term, before moving higher later this year. As we discussed last week, the equity risk premium is quite high in the U.S., and even higher abroad, where valuations are generally cheaper and interest rates are lower (Chart 13).2 Chart 13AEquity Risk Premia Remain Quite High (I)

Equity Risk Premia Remain Quite High (I)

Equity Risk Premia Remain Quite High (I)

Chart 13BEquity Risk Premia Remain Quite High (II)

Equity Risk Premia Remain Quite High (II)

Equity Risk Premia Remain Quite High (II)

The U.S. dollar is a countercyclical currency (Chart 14). If global growth picks up later this year, the greenback should begin to weaken. European and emerging market stocks have typically outperformed the global benchmark in an environment of rising global growth and a weakening dollar (Chart 15). We expect to upgrade EM and European equities – along with more cyclical sectors of the stock market such as industrials, materials, and energy – later this year. Chart 14The U.S. Dollar Is A Countercyclical Currency

The U.S. Dollar Is A Countercyclical Currency

The U.S. Dollar Is A Countercyclical Currency

Chart 15EM And Euro Area Equities Usually Outperform When Global Growth Improves

EM And Euro Area Equities Usually Outperform When Global Growth Improves

EM And Euro Area Equities Usually Outperform When Global Growth Improves

Thanks to the dovish shift by central banks around the world, government bond yields are unlikely to return to their 2018 highs anytime soon. Nevertheless, stronger economic growth should lift long-term yields at the margin, causing yield curves to steepen (Chart 16). Steeper yield curves will benefit beleaguered bank stocks. Chart 16Stronger Economic Growth Should Lift Long-Term Bond Yields, Causing Yield Curves To Steepen

Stronger Economic Growth Should Lift Long-Term Bond Yields, Causing Yield Curves To Steepen

Stronger Economic Growth Should Lift Long-Term Bond Yields, Causing Yield Curves To Steepen

Finally, a word on gold: We still like gold as a long-term investment. However, the combination of higher bond yields and diminished trade tensions could cause bullion to sell off in the near term. As such, we are closing our tactical long gold trade for a gain of 20.5%. Peter Berezin, Chief Global Strategist Global Investment Strategy peterb@bcaresearch.com Box 1 Evidence of Inventory Liquidation In The Manufacturing Sector

A Psychological Recession?

A Psychological Recession?

Footnotes 1 The top ten constituents of the MSCI ACWI Automobiles Index are Toyota (22.6%), General Motors (7.8%), Daimler (7.3%), Honda Motor (6.2%), Ford Motor (5.7%), Tesla (4.8%), Volkswagen (4.8%), BMW (3.8%), Ferrari (3.0%), Hyundai Motor (2.4%). 2 Please see Global Investment Strategy Special Report, “TINA To The Rescue?” dated August 23, 2019. Strategy & Market Trends MacroQuant Model And Current Subjective Scores

A Psychological Recession?

A Psychological Recession?

Tactical Trades Strategic Recommendations Closed Trades

Highlights So What? Prime Minister Boris Johnson’s threat to take the U.K. out of the EU without a withdrawal deal in place is a substantial 21% risk. Why? The odds of a no-deal exit could range from today’s 21% to around 30%, depending on whether Johnson manages to obtain some concessions from the EU in forthcoming negotiations. It is far too early to go bottom-feeding for the pound sterling, as Brexit risks are asymmetrical. We maintain our tactically cautious positioning, despite some cyclical improvements, due to elevated geopolitical risks in the United States, East Asia, and the Middle East. Feature Thank you Mr. Speaker, and of course I should welcome the prime minister to his place … the last prime minister of the United Kingdom. – Ian Blackford, head of the Scottish National Party in Westminster, July 25, 2019 Chart 1No-Deal Brexit Would Come At A Very Bad Time

No-Deal Brexit Would Come At A Very Bad Time

No-Deal Brexit Would Come At A Very Bad Time

The Federal Reserve cut interest rates for the first time since the global financial crisis in 2008 on July 31. The Fed suggested that the door is open for future cuts, though Chairman Jerome Powell signaled that the cut should not be seen as the launch of a “lengthy rate cutting cycle” but rather as a “mid-cycle adjustment” comparable to cuts in 1995 and 1998. President Donald Trump responded by declaring a new 10% tariff on $300 billion worth of imports from China! He resumed criticizing Powell for insufficient dovishness – and Trump could in fact fire Powell, though the decision would be contested at the Supreme Court. The Fed’s move shows that Trump’s direct handle on interest rates comes from his ability to control trade policy and hence affect the “the external sector.” The trade war with China has exacerbated a global manufacturing slowdown that is keeping global growth and U.S. inflation weak enough to justify additional rate cuts with each future deterioration (Chart 1). Improvements in global monetary and fiscal policy suggest that the U.S. and global economic expansion will be extended to 2021 or beyond, which is positive for equities relative to government bonds or cash, but we remain defensively positioned in the near-term due to a range of geopolitical risks, highlighted by the new tariffs. The unconvincing U.S.-China tariff ceasefire agreed at the Osaka G20 has fallen apart as we expected; the period of “fire and fury” between the U.S. and Iran continues; and the U.S. is entering what we expect to be a period of socio-political instability in the lead up to the momentous 2020 presidential election. Moreover the risk of a “no deal” Brexit, in which the U.K. exits the European Union and reverts to basic World Trade Organization tariff levels, is rising and will create acute uncertainty over the next three months despite the world’s easy monetary policy settings (Charts 2A & 2B). In June we upgraded our odds of a no-deal Brexit to 21%, up from 7% this spring. While not our base case, the probability is too high for comfort and the critical timing for the rest of Europe warns against taking on additional risk. The risk of a “no deal” Brexit ... is rising and will create acute uncertainty. Chart 2AUncertainty And Sentiment Getting Worse ...

Uncertainty And Sentiment Getting Worse ...

Uncertainty And Sentiment Getting Worse ...

Chart 2B... Despite Easy Monetary Policy

... Despite Easy Monetary Policy

... Despite Easy Monetary Policy

BoJo’s Gambit Boris Johnson – aka “BoJo” – former mayor of London and foreign secretary, cemented his position as the U.K.’s 77th prime minister on July 24. He immediately launched a gambit to renegotiate the U.K.’s withdrawal. He is threatening not to pay the “divorce bill” (the U.K.’s outstanding budget contributions for the 2014-20 budget period and other liabilities in subsequent decades) of 39 billion pounds. He insists that the Irish backstop (which would keep Northern Ireland or the U.K. in the EU customs union to prevent a hard border between the two Irelands) must be abandoned. He has stacked his cabinet with pro-Brexit hardliners who share his “do or die” stance that Brexit must occur on October 31 regardless of whether an agreement for an orderly exit is in place. These developments were anticipated – hence the decline in our GeoRisk indicator – but the pound sterling is falling now that the confrontation is truly getting under way (Chart 3). Parliament is adjourned in August, so Johnson’s hardline negotiating tactics will get full play in the media cycle until early September, when the real showdown begins. Crunch time will likely run up to the eleventh hour, with Halloween marking an ominous deadline. There is plenty of room for the pound to fall further throughout this period, according to our European Investment Strategy’s handy measure (Chart 4), because the success of Boris’s gambit depends entirely upon creating a credible threat of crashing out of the EU in order to wring concessions that could conceivably pass through the British parliament. Chart 3Our Market-Based Indicator Suggests Still Some Complacency On Brexit Risks

Our Market-Based Indicator Suggests Still Some Complacency On Brexit Risks

Our Market-Based Indicator Suggests Still Some Complacency On Brexit Risks

Chart 4GBP-EUR Still Has Room To Fall Under BoJo's Gambit

GBP-EUR Still Has Room To Fall Under BoJo's Gambit

GBP-EUR Still Has Room To Fall Under BoJo's Gambit

Geopolitically, the United Kingdom is not prohibited from exiting the EU without a deal. Though the empire is a thing of the past, the U.K. remains a major world power. It has Europe’s second-largest economy, nuclear weapons, a blue-water navy, a leading voice in global political institutions, and is a close ally of the United States. It mints its own coin. It is a sovereign entity that can survive on its own just as Japan can survive on its own. This geopolitical foundation always supported our view that there was a 50% chance of the referendum passing in 2016, and today it supports the view that fears over a no-deal Brexit are not misplaced. Investors should therefore not confuse Johnson’s bluster with that of Alexis Tsipras in 2015. A British government dead-set on delivering this outcome – given the popular mandate from the 2016 referendum and the government’s constitutional handling of foreign affairs as opposed to parliament – can probably achieve it. However, the probability of a no-deal Brexit may become overstated in the next two-to-three months. Economically and politically, a no-deal exit is extremely difficult to follow through on – hence our 21% probability. Estimates of the negative economic impact range from a 2% reduction in GDP growth to an 11% reduction (Table 1). The 8% drop cited by Scottish National Party leader Ian Blackford in his denunciation of Prime Minister Johnson’s strategy is probably exaggerated. The U.K.’s recorded twentieth-century recessions range from 2%-7% (Chart 5). These offer as good of a benchmark as any. While a no-deal exit is probably not going to create a shock the same size as the Great Depression or the Great Recession, the recessions of 1979 and 1990 would be bad enough for any prime minister or ruling party. Table 1Wide Range Of Estimates For Impact Of No-Deal Brexit

Tariffs ... And The Last Prime Minister Of The United Kingdom?

Tariffs ... And The Last Prime Minister Of The United Kingdom?

Chart 5