Elections

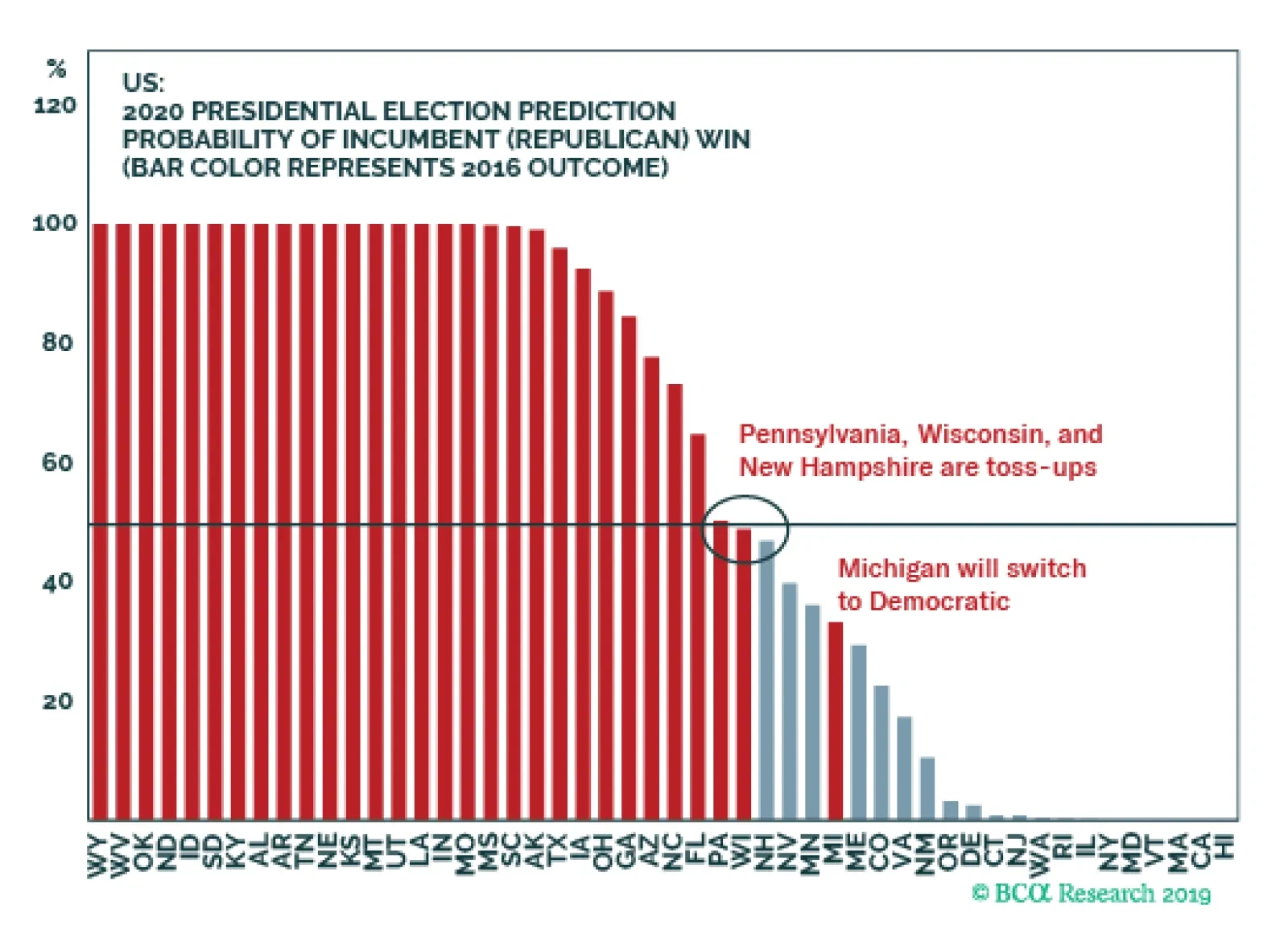

Our sister BCA Geopolitical Strategy Service has introduced a Presidential Election Model that uses political and economic variables to predict the Electoral College vote on the state-by-state level. The model would have predicted the past five elections correctly on an out-of-sample basis, and even the controversial win of George W. Bush over Al Gore in 2000. As of the latest available data, the model predicts that the Republicans will lose Michigan and Wisconsin (critical victories in 2016). Wisconsin, Pennsylvania, and New Hampshire become borderline or “toss-up” states: the probability of a Republican win in these states is 48.77%, 50.17%, and 46.90%, respectively. Even the smallest change in our model inputs can shift these states to either party. According to the model, President Trump is also at the lowest level of approval and weakest state-by-state economy that he can afford. If one of these factors stabilizes below today’s level, Trump will lose his reelection bid. Bottom Line: Quantitative modeling, entirely independent of our qualitative assessment, suggests that Trump is favored to win the 2020 election. However, he is skating on very thin ice with regard to key cyclical variables such as state-level economic performance and popular approval rating.

BCA’s Geopolitical Strategy's 2020 US Presidential Election Model

BCA’s Geopolitical Strategy's 2020 US Presidential Election Model

It is too soon to declare that Trump’s presidency is finished. On the contrary he is slightly favored to win reelection. President Trump’s low approval rating does not prohibit him from reelection. While historically low, it is also historically stable. If…

Highlights US politics are the chief source of global geopolitical risk over the coming year – and likely beyond. President Trump’s reelection remains our base case – the sitting president rarely loses if the economy is expanding. Yet the risk of a Democratic victory is high – Trump’s low approval rating, impending impeachment trial, and various policy troubles threaten his reelection bid. Trump’s tactics and the Democrats’ turn to the progressive left pose threats to BCA Research’s cyclically bullish house equity view. Feature If a time-traveler had accosted you in the fall of 2014 and told you that Donald Trump, the host of the reality TV show The Apprentice, would be the next American president, would you have believed him? What if the time-traveler had gone on to say that President Trump’s unconventional behavior would get him into hot water and that in 2020 he would become the first president in US history to be impeached and removed from office? Granting the premise, the second proposition is easier to imagine. And yet Trump is highly unlikely to be removed from office. He is in fact favored to be reelected. Just as his victory in 2016 proved more likely than the consensus held at the time, so his reelection in 2020 is more likely than the consensus holds today. The reason comes down to political constraints. First, the bar for removal in the Senate is very high. Second, it is easier for a sitting president to get reelected than it is for the opposition to convince voters to start over with something entirely different. Especially if the economy is in decent shape. In what follows we present our quantitative 2020 election model and our qualitative, constraints-based analysis of the election and likely market responses. Trump's fate is only one factor. But US politics is the chief source of market-relevant global political risk over the next 12-24 months. Not A Lame Duck (Yet) After a harrowing year in which global manufacturing slumped due to China’s tight credit policy and Trump’s trade war, the probability of a US recession is now – tentatively – subsiding (Chart 1). This is good news for Trump, whose presidency is hanging by a thread. Chart 1Recession Averted? Or Trump's Death Knell?

Recession Averted? Or Trump's Death Knell?

Recession Averted? Or Trump's Death Knell?

Chart 2Bookies Expect A Democrat Victory

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Betting markets like PredictIt.org suggest that Democrats are slightly more likely than Republicans to win the White House next November (Chart 2). The narrow spread is appropriate given that the balance of evidence is fairly even. However, if there is to be a tilt, it should go the opposite way, i.e. toward Republicans as the incumbent party. The history of US elections since 1860 shows a strong tendency for the incumbent party to hold the White House when the sitting president is running at the head of the ticket. This is especially true when there has not been a recession during the president’s four-year term. It is even true when the ruling party has lost seats in preceding congressional elections, as occurred in 2018 and as is often the case (Chart 3). Other than recession, the biggest exception to the sitting president’s victory – especially in modern times – is when a major scandal has occurred, as with Gerald Ford in 1976. This is clearly relevant to today. In these rare cases the incumbent president’s and incumbent party’s historic reelection rates are both 50/50. The implication of Chart 3 is that Trump’s odds, from a historical point of view, are slightly above 50%. Of course, history does not afford an example of a first-term president being impeached, acquitted, and running for election again.1 Yet this is the most likely outcome today, as there is not an overwhelming popular demand to remove Trump from office. Despite the revelations and public hearings in the impeachment inquiry so far, support for removal stands at 47%, while opposition to removal stands at 45% (Chart 4). In other words, there is no majority in favor of removal, but only a narrow plurality. Removal – nullifying an election result – requires more. Chart 3History Says Trump More Likely To Win Than Not

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 4No Consensus On Removal From Office

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

The spread is conspicuously close to the 46%-to-48% popular vote spread for Trump and Hillary Clinton, respectively, in 2016. The impeachment is not a tsunami of public opposition to the administration. It is a bare-knuckle power struggle: Trump tried to have his top rival investigated and tarred with corruption allegations, the Democrats are retaliating by trying to remove Trump prior to the election. Support for removal will fluctuate, but it will take more than 47% of the population to generate a 67-vote supermajority against Trump in a Republican-held Senate. Republican senators would be taking a grave risk in voting against their base when they have the option of deferring to voters in just 11 months’ time. Both Richard Nixon and Bill Clinton were in their second terms when Congress began moving articles of impeachment: the public had no other recourse in the event that they committed “high crimes and misdemeanors.” Trump is in his first term and is due for the public’s verdict shortly. Nixon resigned when it became clear that grassroots Republicans had lost faith in him and the Senate would not acquit. Trump’s political base has not yet lost faith – his approval among Republicans is still 90%, higher than the average of Republican presidents and at the high end of his term in office (Chart 5). When it comes to the final vote, some Republican senators may defect, but it would take 20 to remove Trump from office. This will require a Nixon-like hemorrhage of support. Remarkably Trump’s general approval rating has not been affected by the impeachment inquiry (Chart 6). His approval rating is still comparable to President Barack Obama’s rating at this stage in his first term (as well as Ronald Reagan’s). While Trump is highly unlikely to break above 50%, he is emphatically not a lame duck … at least not yet. Presidential approval tends to rise as the opposition nomination is settled and the election approaches. If Trump’s approval revives to the 46% of the popular vote he won in 2016, then he remains competitive in the swing states where the election will be fought and won. Chart 5Trump’s Political Base Geared Up For Battle

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 6A Precarious Approval Rating

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

What about the Republicans’ heavy losses in the midterm elections and special elections since 2016? Haven’t national voting trends already condemned Trump and the Republicans to a loss in 2020? Not necessarily. Democrats lost elections more dramatically in 2009-11 than Republicans lost in 2017-19 – both in voter support and turnout (Table 1) – and yet President Obama secured the victory in 2012. Presidential elections are a different beast. Table 1Democrats Suffered More Post-2008 Than Republicans Post-2016 … Yet Obama Won Reelection

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 7GOP Governorships At Low End Of Rising Trend

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

The same goes for Republican losses in recent gubernatorial races. In Kentucky the incumbent governor was a Republican and lost; in Louisiana the incumbent governor was a Democrat and won. The catch is that the number of Republican governors was extremely elevated prior to 2018. Recent losses have merely brought the Republicans back to the bottom of their upward channel as a share of the nation’s 50 governors (Chart 7). Thus while the interim elections are a warning sign to Trump and the GOP, they are not a death knell – as long as the economy rebounds and President Trump’s approval rises as the election approaches. Bottom Line: Trump is not a lame duck yet. His administration is embattled and the impeachment process could permanently damage his standing. But so far his general approval rating and the specific impeachment polling suggest that he will stay in office and remain competitive in the 2020 race. If the election were today he would almost surely lose, but a lot can change in 12 months. If the economy avoids recession, then investors should take reelection as their base case. Cyclical Constraints Will Prevail A recession is the surest way to render a president a lame duck. It does not have to be a technical recession. The contraction in the manufacturing sector – and corresponding cutbacks in lending in the manufacturing-heavy and electorally vital Midwest – are extremely threatening to a president who promised to revive manufacturing and trade (Chart 8). Incumbency, economic growth, failed impeachment, and partial policy victory are enough to win the key swing states. Having declared that “trade wars are good and easy to win,” President Trump will not be able to hide from a deeper slowdown in the industrial heartland. State-level wage growth is positive, but swing states, particularly Trump swing states, are seeing a sharp drop-off from the highs prior to the trade war (Chart 9). The solution is the trade ceasefire being pursued with China. Trump is now in the position of the Federal Reserve Chairman: he can no longer afford to hike (tariff) rates, and the equity market may force him to cut, as long as he can reasonably hope to improve the economy. If the economy is lost, the trade war is back on. Chart 8An Urgent Need For A Trade Ceasefire

An Urgent Need For A Trade Ceasefire

An Urgent Need For A Trade Ceasefire

Chart 9Trump Swing States Took A Hit From The Trade War

Trump Swing States Took A Hit From The Trade War

Trump Swing States Took A Hit From The Trade War

Chart 10Buttigieg And Warren More Favorable Than Others

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Are incumbency, economic growth, failed impeachment, and partial policy victories enough to get Trump over the line in the key swing states?2 Subjectively, we think so. The Democrats have to win all of the states they won in 2016 plus Michigan and Florida (or two other states in place of Florida, such as Wisconsin and Pennsylvania). President Trump can afford to lose Michigan and one other state (but not Florida). This assessment has little to do with the Democratic presidential nominee – as yet unknown – and everything to do with whether the incumbent president or party has been fundamentally discredited. Democratic candidates like Senator Elizabeth Warren and Mayor Pete Buttigieg are generally more competitive than consensus holds. Warren, for instance, is one of the few candidates in recent elections who has a net positive favorability rating (Chart 10). But her favorability is not enough to overturn a sitting president – that will most likely require a shock that renders the status quo intolerable. The cyclical constraints on Trump and his opponents are thus clear. What of the structural constraints? Trump’s 2016 victory is often attributed to long-running structural trends in the US such as deindustrialization, immigration, and racial attitudes. The Democrats’ “blue wall” in the Rust Belt crumbled because Trump courted the working-class voter there and/or stoked racial anxieties. The implication, however, is that Trump still has an advantage in these swing states. Older voters and especially white voters have drifted toward Republicans for several years – the trend was interrupted only by the Great Recession, which saw a surge in Democratic support that has now subsided (Chart 11). Chart 11Old And White People Drifting To GOP Over Time ... Excepting The Great Recession

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

While the white share of the swing states is falling over time, that trend is not sufficient to prevent Trump from winning the Electoral College in the year 2020. Instead the rapidly changing racial and ethnic composition of society should be seen as motivating the attitudes that Trump exploits. Trump’s electoral strategy of maximizing white turnout and support for the Republican Party, which we dubbed “White Hype” in 2016, is still the only way for him to achieve a popular vote victory in 2020, and hence the clearest pathway for him to achieve an Electoral College victory (Chart 12). Needless to say, tensions and controversies over race and immigration will swell in the coming year. Chart 12Electoral College Scenarios Show Trump Win Still Possible

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 13Swing State Turnout Follows Unemployment

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

By the same token, demographic change means that the Democrats can theoretically win by performing no better than they did in 2016 in terms of voter turnout and support rates (see the “Status Quo” scenario in Chart 12). This is a low hurdle for Democrats – suggesting once again that the election will be extremely close, that Trump can win only through the Electoral College (not the popular vote), and that the election outcome will ultimately swing on the cyclical factors outlined above, particularly the state of the economy. A final word about voter turnout. The greatest electoral risk to President Trump is an increase in voter turnout among traditionally low turnout groups that heavily favor the Democratic Party, such as young people and minorities. Given the surge in turnout for the 2018 midterm elections, and the extremely controversial and heated environment surrounding Trump’s presidency, there is considerable reason to suspect that 2020 will be a high-turnout election. Other things being equal, this would likely penalize Trump’s reelection prospects. However, it is important to recognize that voter turnout in swing states is fairly well correlated with the unemployment rate (Chart 13). Depending on the state, surges in turnout occurred in 1992, in the wake of recession; 2004, in the wake of recession, terrorism and war; and 2008, in the wake of the great financial crisis. The exception is Pennsylvania, where a surge in white voter turnout helped Trump pull off a surprise win in the state. Turnout is the hardest political variable to predict, so it is not clear whether Trump’s scandals and impeachment will do the trick. But an increase in the unemployment rate would virtually destroy Trump’s bid, being negatively correlated with presidential approval and positively correlated with voter turnout. Bottom Line: Trump’s executive powers give him the potential to achieve some additional policy victories that could boost his approval rating – namely a trade ceasefire with China that simultaneously improves the economic outlook. Meanwhile structural factors such as demographics do not forbid Trump from winning the Electoral College – on the contrary, aging and the decline in the white share of the population mean that Trump’s electoral strategy could succeed again in 2020, but will be much harder to pull off after 2020. Introducing … BCA’s Geopolitical Strategy 2020 US Presidential Election Model The BCA Geopolitical Strategy Presidential Election Model is a state-by-state model that uses political and economic variables to predict the Electoral College vote. What differentiates our model from that of others is that it attempts to predict the probability of the incumbent party winning the Electoral College votes in each of the 50 states. The model would have predicted the past five elections correctly on an out-of-sample basis, even the controversial win of George W. Bush over Al Gore in 2000. Why do we predict the electoral vote rather than the popular vote? First, the winner of the presidential election is determined by the Electoral College, not the popular vote. Second, in recent history, two candidates who lost the popular vote (George W. Bush in 2000 and Donald Trump in 2016) won the election. It is possible that we will see a similar result in 2020, given President Trump’s low national popularity yet distinctive policy pitch for the Midwestern states (e.g. economic patriotism, hardline on immigration). With only minor exceptions, electoral votes are allocated based on a winner-take-all process, as opposed to proportionately to the popular vote. Hence the best way to forecast the presidential election winner is to predict the probability of winning each state, i.e. receiving all the electoral votes assigned to each state.3 Due to the data availability of our input variables, our sample size includes nine elections (1984 to 2016) across 50 states, making for a total of 450 observations. We designed the model to be as succinct as possible. It includes four explanatory variables: A weighted average of the Federal Reserve Bank of Philadelphia State Leading Index, from the beginning of the previous presidential term until September of the election year. The state leading indexes predict the 6-month growth rate of the state coincident indexes, which include nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average).4 Chart 14Voters Make Up Their Minds Ahead Of Time

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

We use a weighted average of all the monthly forecasts in the presidential term preceding an election, where later months are weighted more heavily than earlier months. Our sample includes 6-month growth rates up to and including September of the election year, which means it includes a rough forecast of the direction of the state’s economy in Q1 of the new president’s term. Since we weigh recent months more heavily, our model assigns more importance to forward-looking factors. It is sufficient to end our calculations of the average state leading indexes in September of the election year. First, the October data comes out in early November, just days before the election, which would be an insufficient lead-time for our final forecast. Second, most voters make their decision at least one month in advance of the election and last-minute changes in economic forecasts will likely not influence their decision (Chart 14). The incumbent party’s margin of victory in the previous presidential election in each state. This is measured as the incumbent party vote share minus the non-incumbent party vote share. Simply put, if the incumbent party failed to secure a solid win in a given state in the previous election, the probability of securing a solid win in the current election is much smaller. Average national approval level of the incumbent president in July of the election year. We tested the correlation between presidential approval in every month leading up to the election versus the election outcome and found that July approval levels have the second-highest correlation with the popular vote and Electoral College vote (Chart 15). Average October approval levels have slightly higher correlation with election outcomes, but not sufficiently so to sacrifice three months of lead-time. A “time for change” variable. This is a categorical variable indicating whether the incumbent party has been in the White House for one or more terms. Academic literature shows that a party that has occupied the White House for two terms or more is much less likely to win an election than a party that is running for a second term.5 Chart 15Voters Mostly Decided By July

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

The output of our model is the probability of an incumbent win in each state. There are two ways of aggregating these probabilities to produce a national-level outcome: Allocate the number of Electoral College votes won by the incumbent proportionally to their probability of victory in each state, and then sum them up across all states. This method would smooth out potential errors in our forecast. The Republican Party is expected to win with 279 Electoral College votes in 2020. Assume a probability threshold of 50%: any state with an incumbent win that is at least 50% likely is fully assigned to the incumbent. While this method could significantly sway our forecast towards one of the parties because of small changes in probability, it is closer to the political reality. Even the smallest majority in a given state will (usually) result in the winning candidate getting all of the state’s Electoral College votes. We therefore adopt this method in our aggregation.6 Our model performs well in back tests: it correctly predicted every election in in-sample tests and every election from 2000 to 2016 in out-of-sample tests (Chart 16). Chart 16BCA Research Geopolitical Strategy Election Model: Back Tests Accurate

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 17 shows our initial 2020 prediction. Overall, the Republican Party is expected to win 279 Electoral College votes, a 25-vote decrease from its 2016 result. Chart 17Trump Narrowly Slated To Win 2020 With 279 Electoral College Votes

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

As of the latest available data, our model predicts that the Republicans will lose Michigan and Wisconsin (critical victories in 2016). Wisconsin, Pennsylvania, and New Hampshire become borderline or “toss-up” states: the probability of a Republican win in these states is 48.77%, 50.17%, and 46.90%, respectively. Even the smallest change in our inputs can shift these states to either party. The two inputs that can affect our forecast are the state leading index and President Trump’s approval level, since the other two inputs – the time for change variable and last election’s margin of victory – are fixed. Table 2 shows the predicted Electoral College votes for the Republican Party for various scenarios of these two variables. According to the model, President Trump is currently at the lowest level of approval and weakest state-by-state economy that he can afford. If one of these factors stabilizes below today’s level, Trump will lose his reelection bid. Table 2Small Decline In State Economies Could Ruin Trump’s 2020 Bid

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

In the worst-case scenario for Trump – if his approval and the state leading indexes drop to the lowest levels they have touched in Trump’s presidency – the Republican Party will only manage to secure 230 Electoral College votes. The opposite, optimistic scenario would see them winning with 329 votes. An interesting takeaway from our model is that it captures the increase in American political polarization that has been widely observed by scholars. The 2020 forecast shows that many states will be won or lost by the incumbent party with extreme certainty (0% or 100%). Results of in-sample predictions show that this trend has been increasing since 1992 (Chart 18, top panel), which is also in line with our own measure of polarization (Chart 18, bottom panel). Since the results are based on in-sample estimations, the coefficients remain constant, so the differences in the results can be attributed to the underlying data. The impression of ever-intensifying polarization in the US is correct. What does this mean for Trump? He cannot be written off simply because he has a relatively low approval rating. Structural political factors that propelled him to the White House are still in place. His approval and the economy must deteriorate to change this base case. The chief risk to our model is the accuracy and interpretation of presidential approval polling. While polling data always has a margin of error, it is possible that approval polling is underestimating Trump’s support, particularly on the state level, as was witnessed in 2016 (Chart 19). Chart 18Rising Polarization – It’s Empirical

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 19State-Level Polling Still A Risk

State-Level Polling Still A Risk

State-Level Polling Still A Risk

We have a high degree of confidence in professional pollsters, who have also made improvements since 2016. But asking Americans whether they “approve” of the unorthodox Trump may be a different proposition than in the past, disguising voting intentions to some degree. By choosing the level of Trump’s approval in our model (see Appendix), we are guarding against overstating his support and not allowing much room for any dampening effects or self-censorship, which is thus a risk to our model. Bottom Line: Quantitative modeling, entirely independent of our qualitative assessment, suggests that Trump is favored to win the 2020 election. However, he is skating on very thin ice with regard to key cyclical variables such as state-level economic performance and popular approval rating. If his approval level suffers from a slowing economy, or scandal and impeachment, then he will lose the critical toss-up states and the White House. Investment Conclusions In this report we have outlined a case where President Trump, despite his extreme unorthodoxy in general, and acute vulnerability at this moment in time, is still the most likely winner of the 2020 election. Elections are a Bayesian process in which investors should establish a clear prior, or starting place, and update their probabilities according to reliable data streams. This report establishes our prior and our key data streams. So what? Does it matter if Trump is reelected? Is it relevant to investors? From a bird’s eye view, Trump has made a few decisions that clearly distinguish his term in office from that of previous presidents. First, Trump replaced Janet Yellen with Jerome Powell at the Federal Reserve. It is debatable whether or how this affected the normalization of monetary policy. What is clear is that Trump made a change at the helm while pushing through highly stimulative fiscal policy. Fed hikes contributed to a rise in bond yields and an increase in market volatility, and the Fed was ultimately forced to adjust. Trump has vociferously criticized the Fed and demanded ever-lower rates. Second, by embracing sweeping Republican tax reform, Trump initiated pro-cyclical fiscal stimulus that widened the US’s monetary and economic divergence from the rest of the world, while exacerbating the US’s long-term fiscal woes. Third, by adopting protectionist trade policy to confront China’s mercantilism, Trump rattled global sentiment and contributed to a manufacturing recession. As long as our view remains correct, investors will have a base case that is cyclically bullish. Of these three macro developments, the only one that the election could substantially change is trade policy – and yet the Democrats are also taking a more hawkish approach to China. On the fiscal front, the Democrats will raise taxes, but they will not impose austerity – instead they propose large expansions of entitlements that the populace increasingly demands. Populist social spending combined with geopolitical struggle with China ensures that the deficit/GDP ratio will go up regardless of the party in power. From a market point of view, the historical record suggests that presidential elections – specifically elections that lead to gridlock between the White House and Congress, since we do not expect the Democrats to lose the House of Representatives – usually see a rising US stock market beforehand and a higher degree of volatility afterwards (Chart 20). Relative to developed market equities, US stocks typically underperform, and only resume their rise in the second half of the following year (i.e. 2021). Comparing Trump to other first-term presidents, it is clear that his “pluto-populism” (populism plus tax cuts for the rich) has exerted a reflationary effect on the equity market (Chart 21). As long as the data show that he has a fair chance of reelection, investors will have a base case that is cyclically bullish, despite the volatility to come from the Democrats’ taxation and regulation proposals. Chart 20Equity Outcomes Surrounding US Presidential Votes

Equity Outcomes Surrounding US Presidential Votes

Equity Outcomes Surrounding US Presidential Votes

Chart 21Trump A Reason To Be Bullish

Trump A Reason To Be Bullish

Trump A Reason To Be Bullish

What is most striking about Trump’s presidency is the low real total return on US Treasuries. This is despite his aggressive foreign and trade policy, which has motivated safe-haven flows into Treasuries this year (Chart 22). The bottom line is that the output gap is closed, the labor market is tight, and fiscal policy is expansive, putting upward pressure on yields. Given that Trump needs to cultivate a China ceasefire and economic improvement for reelection, this trend should continue until the next recession looms. Chart 22Trump Marks End Of Bull Market In Bonds

Trump Marks End Of Bull Market In Bonds

Trump Marks End Of Bull Market In Bonds

The risk, however, is that Trump’s precarious China negotiations fall through, or that his scandals cause a permanent downshift in his approval rating, rendering him a lame duck. Not only would this free him of the election constraint that currently forces him to pursue pro-market policies, but it would also make a Democratic victory more likely. The Democratic nomination, meanwhile, could easily produce a progressive populist in the figure of Elizabeth Warren, who is still a frontrunner in the Democratic nomination. A bear market could develop quite easily if a normal equity market correction, which improves the odds of a Democratic victory becomes entangled in expectations that Warren is set to win the nomination. If the opposition can summon enough votes to unseat an incumbent president, chances are that the circumstances will include a “blue wave” that also sees the Democrats take the Senate. This would institute another sweeping change to American policy, this time in a direction that is unfriendly to corporate profits. As the probability of such a scenario rises, the equity market will have to discount it. Expectations of a Trump victory will spur the market upward – but investors should be wary. If this very long bull market has continued all the way to November 3, 2020, and President Trump is confirmed in office, the positive stock market reaction will likely provide an excellent time for booking profits and reducing risk. In a second term, Trump will be unshackled from his electoral constraints – very much unlike a first-term Democrat. This would free him to pursue his trade wars with fewer inhibitions – against China but also likely against Europe. A continuation of the trade war has important impacts across the full slate of global assets, as outlined in Chart 23, which depicts the movement of assets on days in which US equities reacted negatively to trade war developments. Chart 23A Trump Second Term Means Trade War With Fewer Constraints

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

With 11 months to go, we are a world away from the election. The party nomination process, or third-party candidates, could overturn all expectations. But if there is one certainty, it is that polarization and political risk will rise in the coming 12-24 months. The losing side of the population will have deep heartburn. A crisis of legitimacy could easily haunt the next administration. There could be hanging chads, vote recounts, faithless electors, or contested results. The outcome of the election could turn upon unprecedented developments in the Electoral College, Supreme Court, or even in cyberspace. If the Democrats win, redistribution will amplify partisanship. If Trump wins, inequality will rise. There is no easy way forward for the United States. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Ekaterina Shtrevensky Research Analyst ekaterinas@bcaresearch.com Appendix 1: The Approval Question: Level Or Change? Chart 24Trump’s Historically Low Approval Rating

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

The chief risk to our model is the interpretation of the presidential approval rating and its impact on the election. President Trump’s approval rating is notoriously low compared to the average president (Chart 24). While many authors use approval rating (or popularity) in their models, some argue that it is not the approval level, but the change in approval leading up to the election that matters.7 Consider the following: if President Trump’s approval increases from today’s level of 43% by 5%, he would be at the same level of approval as the average president if their approval were to drop by 5%. A model based on approval level would place these two presidents equally, while a model based on the change in approval would favor Trump. So which one is correct? We compare the incumbent’s popular vote in post-WWII elections with four different “variations” of incumbent president approval: the average level in July of the election year (as in our model); the deviation of the average October level from the election-year average, the change during the last two years of the term; and the range throughout the entire term. Directionally, the results are as expected. Level and change in approval are positively correlated with the popular vote, while a less stable approval (higher range) is negatively correlated (Chart 25A). We also find that approval level has the best fit with the election outcome, followed by the change in approval in the two years leading up to the election. However, if we restrict the sample size to the range of elections used in our model, 1984 to 2016, we find that the change in approval has a much better fit than the level (Chart 25B). In other words, in modern elections the presidential candidate’s momentum matters more in the final outcome. Chart 25AHigh, Rising, And Stable Approval Ratings …

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Chart 25B… Help Presidents Win Elections

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

We tested each variation of approval as an input in our model instead of the July approval level. Table 3 summarizes the results. Trump wins in all four versions. Table 3All Measures Of Approval Favor Trump In 2020

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

Our current model penalizes Trump the most, while the model based on approval range favors him. This makes sense, given that President Trump’s approval is relatively low but very stable (Chart 26). Chart 26Trump Approval Very Low … And Very Stable

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

We will continue to use approval level in our model to generate updated predictions, given that this measure has the best long-term historical fit with the election outcome. However, given that President Trump is performing relatively well on these other measures of approval, there is upside risk to his 2020 performance. Appendix 2: A Word About The Probit Model Table 4 presents the regression coefficients of our model. Since this is a probit model, the coefficients cannot be directly interpreted as they would in an ordinary regression. The coefficients in a probit regression model measure the change in the Z-score associated to each independent variable for a one-unit change in that variable. Table 4BCA 2020 US Presidential Election Model Statistics

US Election 2020: Civil War Lite

US Election 2020: Civil War Lite

The sign of the coefficient corresponds to the direction of change in probability. So increases in the state leading index, presidential approval, or the incumbent’s margin of victory in the last election increase the probability of the incumbent winning a state. Of course, the latter variable is fixed and will not change until the election. At the same time, having occupied the White House for two terms or more decreases the probability of an incumbent win. But this is not the case in the current election. Footnotes 1 Andrew Johnson, the first to be impeached, did not run in 1868; Ulysses Grant bowed out after two terms in 1876, amid the “Great Barbecue” scandal; Warren Harding died before the election of 1924, amid the infamous “Teapot Dome” scandal; Harry Truman stepped down amid scandal after two terms in 1952; Richard Nixon resigned before the election of 1976; Bill Clinton was impeached and hit the two-term limit before the election of 2000. For these examples, and the electoral impact of great scandals in general, please see Allan J. Lichtman, Predicting The Next Presidency: The Keys To The White House 2016 (Rowman and Littlefield, 2016). 2 Trump’s policy record contains one major legislative victory, the Tax Cut and Jobs Act of 2017, along with a number of works in progress. The Republicans’ failed attempt to repeal and replace the Affordable Care Act (Obamacare) exacted an opportunity cost: it deprived Trump and the GOP Congress of time needed to legislate a southern border wall, while mobilizing the opposition for all subsequent elections. As for other policies, the renegotiation of NAFTA is only a partial success as the USMCA has not been ratified. The promised infrastructure package will become a campaign pledge for the second term. We expect some kind of North Korea deal. 3 To this end, we use a probit model, where the dependent variable is stated as 1 = incumbent party won all Electoral College votes in this state, or 0 = incumbent party did not win any Electoral College votes in this state. This model allows us to measure the probability that a state with certain characteristics will fall into one of these two categories. 4 “The leading index for each state predicts the six-month growth rate of the state’s coincident index. In addition to the coincident index, the models include other variables that lead the economy: state-level housing permits (1 to 4 units), state initial unemployment insurance claims, delivery times from the Institute for Supply Management (ISM) manufacturing survey, and the interest rate spread between the 10-year Treasury bond and the 3-month Treasury bill.” See the Federal Reserve Bank of Philadelphia, www.philadelphiafed.org. 5 Alan I. Abramowitz, “Forecasting the 2008 Presidential Election with the Time-for-Change Model,” Political Science and Politics, Vol. 41, No. 4 (Oct., 2008), pp. 691-695. 6 We also assume that the Democrats always win the District of Columbia. 7 Please see Michael S. Lewis-Beck, Charles Tien, “Forecasting presidential elections: When to change the model,” International Journal of Forecasting, Volume 24, Issue 2, April–June 2008, Pages 227-236, and Mark Zandi, Dan White, Bernard Yaros, “2020 Presidential Election Model,” Moody’s Analytics, September 2019.

Highlights The Fed is the usual culprit for killing business cycles — but the Fed is on hold. This makes geopolitics the likeliest candidate to kill the cycle. The key geopolitical risks are US political turmoil, China’s economic policy, and the US-Iran confrontation. Nevertheless, policymakers are adjusting to the threat of recession, which points to a continuation of this long-in-the-tooth expansion. The US-China talks will be driven by Trump’s need for an economic boost ahead of the US election. If the economy or Trump’s approval rating fails anyway, then all bets are off. Go long gold as a strategic hedge. Feature Great power struggle, or “multipolarity,” continues to be our mega-theme in 2020. The world does not operate like a normal society, with a single government that possesses a monopoly on the use of force and ensures stability. Nations are individualistic, armed, and dangerous, creating what scholar Hedley Bull once called “The Anarchical Society.” This is not pure chaos, but rather a community of nations that lacks a clear and undisputed leader. Hence, quarrels break out often. Updating our geopolitical power index shows that the rise of China remains the most disruptive trend in global politics (Chart 1). The gap between the US and China has closed until recently, with China’s downshift in growth rates, but American fear is just being awakened (Chart 2). Given that Beijing threatens the US’s military and technological dominance over the long run, Washington will continue to develop a containment policy. Chart 1China's Geopolitical Rise Is Disruptive

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 2China-US Power Gap Is Narrowing

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

China is too big to quarantine, especially for a relatively unpopular first-term American president who eschews international coalition-building. The European Union’s decline in relative power is more marked than that of the United States, but China does not pose as much of a security threat to Europe. This trend exacerbates the already serious divergence in the trans-Atlantic alliance – which will worsen if Trump wins on November 3, 2020. Hence, globalization faces persistent challenges, as indicated by the falling import share of global output (Chart 3). This multi-decade process has peaked, creating a headwind for trade-exposed firms over the long run. What about the next 12 months? Will geopolitics kill the bull market? Not necessarily. Just as central bankers have cut interest rates to guard against deflationary risks (Chart 4), so the key governments are adjusting policies to avoid recessionary risks, especially with the memory of 2008 still fresh. Simply put: The Fed is on pause, Trump wants to be reelected, and China cannot afford a hard landing. Chart 3Globalization Faces Challenges

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 4Policymakers Are Reacting To Deflationary Risks

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Clearly the risks to this view are elevated. The chief ones: (1) President Trump becomes a lame duck, cannot run on an economic platform, and thus makes a desperate attempt to win as a “war president” (2) Xi Jinping overestimates his advantage, in domestic or foreign policy, and makes a policy mistake (3) the US-Iran conflict spirals out of control due to Iran’s economic vulnerability. Other risks, such as Brexit, pale by comparison. Fear And Loathing On The Campaign Trail It is too soon to declare that Trump’s presidency is finished. On the contrary he is slightly favored to win reelection: • The Senate is unlikely to remove him from office. Republican support for the president is well above average despite evidence that Trump tried to get Ukrainian officials to investigate his political rival (Chart 5). The implication is that a year from now Democrats will have suffered a policy failure while Trump will have been cleared of charges. Chart 5Trump Still Popular Among Republicans

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

• The odds of recession in the coming year are low. The US voter is buffered by rising real incomes and wages and high net wealth (Chart 6). To unseat a sitting president requires a recessionary backdrop that fundamentally discredits him and his party – not just slowing growth. Chart 6Pocketbook Voter Theory To The Test

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

• Trump’s low approval rating does not prohibit him from reelection. While historically low, it is also historically stable. Our quantitative election model – which predicts Trump will win the Electoral College with 279 votes by clinging onto Pennsylvania – shows that Trump’s victory margin would increase if we looked not at the average level of his approval but at its change, momentum, or low range (i.e. stability). Table 1 shows the results of all four variations of his approval rating, with ascending chances of winning key swing states. Table 1All Measures Of Trump’s Approval Rating Get Him 270 Electoral College Votes

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Trump’s odds of winning will affect the US equity market throughout the year. As long as he remains competitive, i.e. neither scandal nor the economy cause his approval rating to break down, he will have reason to temper his policies to cater to US financial markets. Foreign and trade policies are Trump’s only ways to improve the economy and voter support. Trump’s only remaining way to boost the economy and improve voter support lies in foreign policy and trade policy. Specifically, he will stop increasing tariffs on China – and maybe even roll back tariffs to August 2019 or even April 2019 levels (Chart 7) – at least as long as the manufacturing recession persists. Chart 7Some Tariff Rollback Is Possible

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

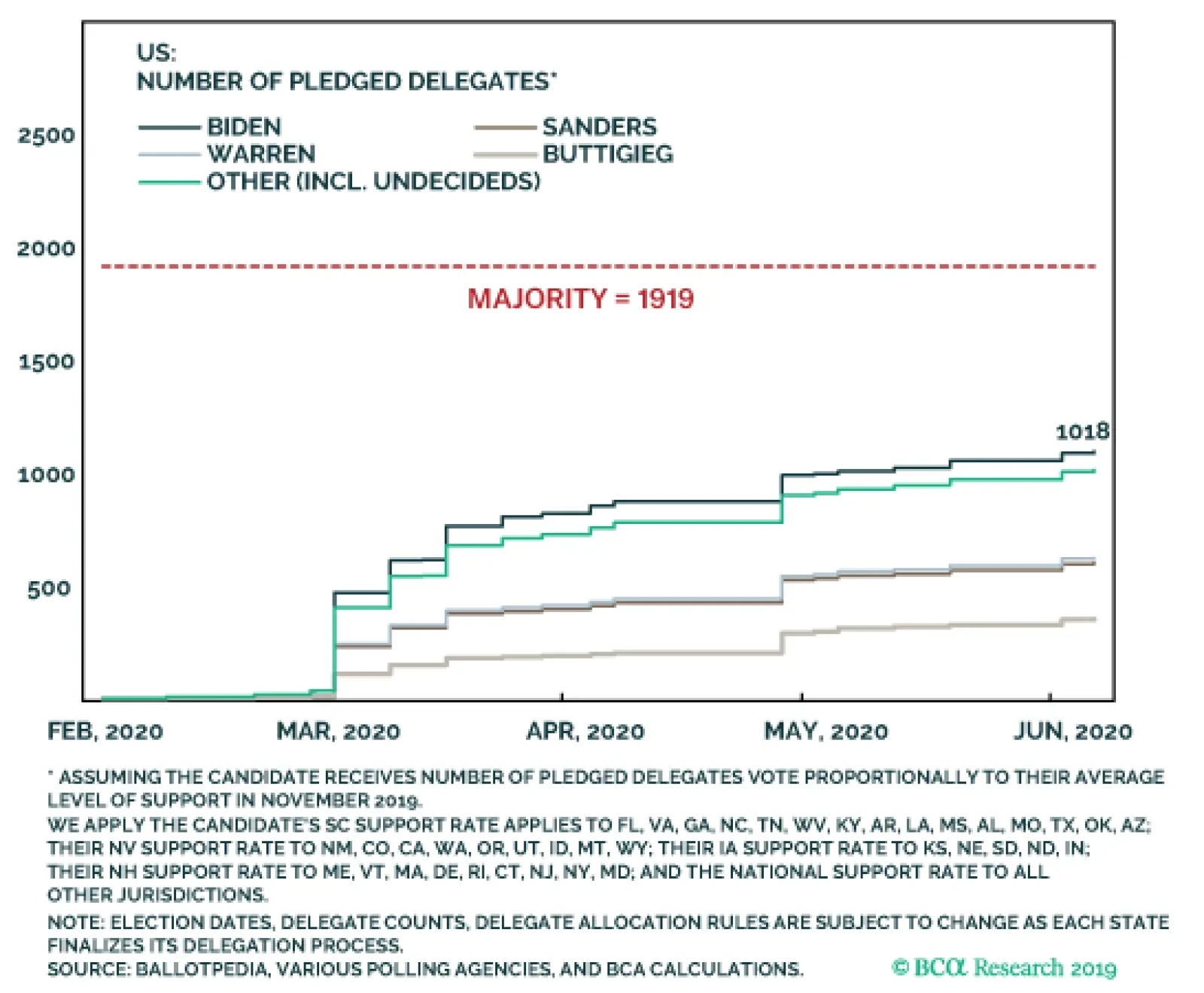

China is unlikely to implement painful structural changes when Trump could be gone in 12 months’ time. Strategic tensions outside of trade will undermine any ceasefire. Hence economic policy uncertainty will remain elevated even though it will drop off from recent peaks. Assuming the electoral constraint prevents Trump from levying sweeping tariffs on China or Europe, he will be limited to other foreign and trade policies to try to boost his approval rating or fire up his base: • We expect a third summit with Kim Jong Un of North Korea. Trump is rumored to be considering some troop reduction in exchange for progress on denuclearization (neither of which would be irreversible). • Otherwise Trump could turn to saber-rattling, since Pyongyang is threatening to resume long-range tests and the economic consequences of another round of “fire and fury” would be limited. • Trump could also rattle the saber against Iran, Venezuela, or other rogue states. If Trump becomes uncompetitive in the election, then the market will sell off. The market will have to price not only policy discontinuity (e.g. higher taxes), but also the chance of a progressive-populist taking the White House. Moreover, if a Democrat is able to unseat an incumbent president, the Democrats will take the Senate as well. Trump is a known unknown; this scenario would be an unknown unknown. The Democratic Party’s primary election will consume the first half of the year. It culminates in the Democratic National Convention, strategically chosen to take place in Milwaukee, Wisconsin on July 13-16. Wisconsin is one of three critical swing states. Will former Vice President Joe Biden win the nomination? A high conviction is not warranted. Biden is clearly the frontrunner, but we think a progressive can pull it off. A simulation of the Democratic Convention “pledged delegates,” based on November polling in the first four primary elections, shows Biden far short of a majority (Chart 8). He needs to outperform his polls, but this will be difficult given that he is well-known, has not performed well in debates, and will have Mayors Pete Buttigieg and Michael Bloomberg nipping at his heels in the Midwest and Northeast, respectively. Chart 8Do Not Discount A Progressive Win

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Over time, candidates will drop out, so it is more informative to look at the “centrist” candidates as a whole compared to the “progressives.” Here the early primary polling suggests that the progressives will come closest to victory (Chart 9). Chart 9Progressives Come Closest To Victory

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

The trend within the party is to move to the left. Senators Elizabeth Warren and Bernie Sanders are tied as voters’ second choice – even Buttigieg supporters are split between Biden and Warren (Chart 10). What is unknown is whether Warren (or Sanders) can consolidate the progressive vote faster than Biden (or Buttigieg) consolidates the centrist vote. Chart 10If Biden Falters, Progressives Are Next In Line

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 11Structural Imbalances Give Rise To Populism

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Trends pointing toward a progressive victory may not at first trouble the market, but any signs that a progressive is pulling ahead decisively will force investors to sharply upgrade the probability that he or she will win the White House. This will cause equity volatility, which could become self-reinforcing. A progressive nominee would force investors to recognize that populism and political risk are here to stay – which is our expectation given that they are motivated by polarization, inequality, and other structural imbalances in the United States (Chart 11). Left-wing or progressive populism is far more negative for corporate earnings than Trump’s right-wing or “pluto-populism.” Sanders or Warren present the worst case for investors because they favor trade protectionism in addition to higher taxes and minimum wages. Most presidents achieve their chief legislative priority in their first term and there is no reason to assume a progressive presidency would be any different. The implication is higher corporate taxes as well as individual taxes to pay for a sweeping expansion of the social safety net – positive for the economy perhaps but negative for corporate earnings. Chart 12A Progressive Win Threatens Key Sectors

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

An extensive re-regulation of the US economy would occur regardless, since it falls under executive authority. It would affect the key equity sectors in the US bourse, technology and health (Chart 12), as well as energy and financials. The choice of a centrist Democrat like Biden (or Buttigieg) would be the least negative outcome for US equities of all the Democrats. The market would probably cheer a Trump versus Biden matchup for this reason. Biden favors higher taxes and regulation but is an establishment politician and known quantity. However, even Biden will be pulled to the left by the current within his party once in office; and Buttigieg will govern to the left of Biden. Trump’s reelection would spur a relief rally in US equities, but it would be short-lived. He would solidify low taxes and deregulation and would have a real chance of passing an infrastructure package. But he would also curtail labor force growth with his border wall and double down on trade protectionism – likely against Europe as well as China this time. His unpredictable and aggressive tendencies would be turbo-charged by a new popular mandate. We expect to cut back on risk exposure upon Trump’s reelection, assuming the bull market has survived to return him to office. A Democratic victory would mark another reversal in US policy orientation. Given our view that the White House call is also the Senate call, this would be the third time since 2008 that the country has witnessed a total reversal. Domestic American political risk will not end with the election: a legitimacy crisis could follow a narrow election, and institutional erosion continues regardless. It is too soon to call peak polarization, as the election will result in either a left-wing government bent on redistributing wealth or a right-wing Trump administration that exacerbates inequality. A centrist "return to normalcy" is possible with a Biden or Buttigieg victory. This reinforces our constructive cyclical view. Bottom Line: The chief risk from US politics in 2020 is Trump becoming a lame duck and resorting to belligerent foreign policy to try to win back voters through a rally around the flag. The chief risk of the Democratic nomination, and the general election, is a left-wing populist winning the White House. Any Democratic victory would likely bring the Senate, removing a key constraint. Over time the median voter is moving to the left. The Man Who Changed China Chart 13Xi Is Purging Misallocated Capital

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Xi Jinping undoubtedly represents a “new era” in China – a reassertion of Communist Party rule. The party faced a crisis of legitimacy amid the Great Recession and Arab Spring and was determined to regain political, economic, and social control. Xi had previously been anointed but was all too happy to take on the role of neo-Maoist strongman. Yet Xi’s playbook is close to that of President Jiang Zemin’s: centralize the party, repress dissent, modernize the military, restructure banks and the economy, upgrade the country’s science and technology, and expand China’s global influence. The difference is that while Jiang rode the high tide of globalization, Xi is riding the receding tide. Jiang culled two-thirds of the country’s state-owned enterprises, laying off over 40 million people, confident that a surge of new growth would ensue. Xi is also cracking down – allowing bankruptcies to purge misallocated capital (Chart 13) – but with a large debt load and shrinking labor force, he needs the state sector to put a floor under growth rates. The takeaway is that Xi will act pragmatically to boost growth when China’s stability is threatened, as he did in 2015-16. The trade war has already forced him to backtrack on the 2017-18 deleveraging campaign and stimulate the economy. The combined fiscal and credit impulse amounts to 6.6% of GDP from trough to now, and it hasn’t peaked. The implication is that Chinese growth – and global growth – will pick up from here (Chart 14). Chinese authorities are still trying to contain the growth in leverage, which has kept this year’s stimulus in check. But the chief banking regulator has also stated that as long as the macro-leverage ratio is not growing faster than 10%, this goal is met (Chart 15). Chart 14Chinese Growth Will Pick Up

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 15China Says Leverage Already Contained

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

The economy has not yet durably bottomed, so the state will continue adding support. The coming year is the third and final year of the “Three Battles” – against poverty, pollution, and systemic risk – as well as the final year of the thirteenth five-year plan. Beijing is falling short on its targets for real urban per capita income (Chart 16) and poverty elimination (Chart 17). A last-minute rush to meet these targets is likely and will require more fiscal stimulus. Chart 16Beijing Falls Short Of Urban Income Target...

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 17...And Poverty Target

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

This is not an argument for a blowout credit splurge. China is saving dry powder for a further escalation in the US containment strategy and a worse economic downturn. Do not expect a blowout Chinese credit splurge. The core constraint on policy is unemployment. Stimulus efforts have created a bottom in the employment component of the manufacturing PMI as well as a notable uptick in the demand for urban labor (Chart 18). To withdraw stimulus now – or tighten policy – would be to trigger a relapse in an economy that is ultimately at risk of a debt-deflation trap. Chart 18Chinese Stimulus Shows Up In Employment

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 19A Banking Crisis Is A Risk To The Chinese Economy

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Tougher controls on credit and shadow banking have seen an uptick in corporate defaults and bank failures. With the government deliberately imposing pain on bloated sectors of the economy, financial turmoil could spread. Newspaper mentions of defaults, layoffs, and bankruptcies have only slightly subsided since stimulus efforts began (Chart 19). If bank failures spiral out of control, the economy will tank. The state will have to fight fires. Tariffs have accelerated the trend of firms relocating out of China, which began because of rising wages and a darkening business environment (Chart 20). A questionable trade ceasefire will not reverse the process as American and Asian companies are seeking a lasting solution, which requires them to set up shop elsewhere. China will want to mitigate the process, first by stabilizing domestic growth, and second by accepting Trump’s tactical trade retreat. Xi is also trying to avoid diplomatic isolation by courting trade partners other than the US, since the ceasefire is unreliable and the US containment strategy is presumed to continue. This involves outreach to the rest of Asia, Russia, and Europe, and even to distrustful neighbors like Japan and India. Europe is the swing player. China’s Asian neighbors, and Australia and New Zealand, have reason to fear Beijing’s growing clout and seek the US’s security umbrella. Russia and China are informal allies. But the European public is not interested in the new cold war – China does not threaten Europe from next door, like Russia does, and the Trump administration is threatening Europe with both trade war and Middle Eastern instability. European leaders are happy to take the market share that the US is leaving, as is clear from direct investment (Chart 21). Only a concentrated US diplomatic effort can address this divergence, which is not forthcoming in 2020. Chart 20Firms Are Relocating Out Of China

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 21Europe Exploits US-China Rift

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

A new Democratic administration, or a change in Trump strategy in the second term, could eventually produce a multilateral western coalition demanding that China open up and liberalize parts of its economy. But Europe will need to be convinced of the underlying reality that China is doubling down on the state-led industrial policies that provoked the Americans to begin with. Beijing is after economic self-sufficiency, indigenous innovation, and leadership in high-tech production and new frontiers. Its official research and development budget is not its only means for achieving this end (Chart 22) – it also has state-backed acquisitions and cyber campaigns. Germany and Europe have begun scrutinizing Chinese investment, separately from the United States. Chart 22Beijing Is After Economic Self-Sufficiency

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

The danger to China – and the world – is that Xi Jinping might overplay his hand. He could overtighten money, credit, or property regulations and spoil the economy when global growth is vulnerable. His anti-corruption campaign is a telling reminder of his heavy hand in domestic affairs (Chart 23). Chart 23Xi Jinping Risks Overplaying His Hand

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Chart 24China Needs To Calm Things Down

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

He could also suppress protesters in Hong Kong and rattle sabers over Taiwan or the South China Sea in a way that undermines the trade ceasefire. Or he could fail to bring the North Koreans to heel. These strategic tensions are significant only insofar as they undermine the trade ceasefire or provoke US-China saber-rattling. Failing to act as an honest broker in the Iran crisis would also irk Europeans and give them an excuse to side with the US. Bottom Line: China will continue modestly stimulating the economy next year to achieve a durable stabilization in growth. The risk of debt-deflation and rising unemployment ultimately necessitates this policy. Beijing can accept Trump’s tariff rollback for the sake of stability – China’s policy uncertainty relative to the rest of the world is off the charts and Beijing has an interest in calming things down (Chart 24). Yet Beijing will double down on indigenous innovation, while courting the rest of the world so as to preempt criticism and isolate the Americans. The risk is that Xi proves too heavy-handed when it comes to domestic leverage, the tech grab, strategic disputes, or trade talks with Washington. The Strait Of Hormuz Risk Chart 25US-Iran Conflict Still Unresolved

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

In a special report earlier this year entitled “The Polybius Solution” we argued that while the US-China conflict is the major long-term geopolitical conflict, the US-Iran showdown could supersede it in the short term. This remains a risk for 2020, as the Trump administration’s confrontation with Iran is fundamentally unresolved (Chart 25). The Trump administration is still enforcing “maximum pressure” sanctions, which have reduced Iranian oil exports from 1.8 million barrels per day at their recent peak to 100,000 barrels per day in November (Chart 26). These are crippling sanctions that have sent Iran’s economy reeling. Chart 26Iran Remains Under

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Iran’s Supreme Leader Ayatollah Ali Khamenei has ruled out negotiations with Trump. They would be unpopular at home without a major reversal on sanctions from Trump (Chart 27). Chart 27Major US Reversal Prerequisite For Iran Talks

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Trump presumably aims to avoid an oil shock ahead of the election. The US and its allies have visibly shied away from conflict in the wake of Iran’s provocations, including the spectacular attack on eastern Saudi Arabia that knocked 5.7 million barrels of oil per day offline in September. However, this does not mean the odds of war are zero. The Americans or the Iranians could miscalculate. Both sides might think they can improve their standing at home by flexing their muscles abroad. Iran is a rational actor and would not normally court American airstrikes or antagonize a potentially lame duck president. Yet it is under extreme pressure due to the sanctions. It faces significant unrest both at home and in its sphere of influence (Iraq and Lebanon). Opinion polls show that the public primarily blames the government for the collapsing economy, and yet that American sanctions are siphoning off some of this anger (Chart 28). This could tempt the leaders to continue staging provocations in the Strait of Hormuz or elsewhere in the region. Chart 28Iranians Blame Tehran, Tehran Blames America

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Hardline military leaders and politicians currently receive the most favor in polling, while the reformist President Rouhani – undercut by the American withdrawal from the 2015 deal – is among the least popular (Chart 29). The Majlis (parliament) elections in February will likely reverse the reformist turn in Iranian politics that began in 2012. The regime stalwarts are gearing up for the supreme leader’s succession in the coming years. While a Democratic White House could restore the 2015 deal, that ship may have sailed. Chart 29Rouhani And Reformists In Trouble

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

A historic oil supply disruption is a fatter tail risk than investors realize. Chart 30The Iranians May Take Excessive Risk

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Trump, under impeachment, could seek to distract the public. This was Bill Clinton’s tactic with Operations Infinite Reach, Desert Fox, and Allied Force in 1998-99. These operations were minor and not comparable to a conflict with Iran. However, Trump may be emboldened. On paper the US strategic petroleum reserve (along with OPEC and other petroleum reserves) could cover most major oil shock scenarios. According to Hugo Bélanger, Senior Analyst at BCA Research Commodity & Energy Strategy, a supply outage the size of the Abqaiq attack in September would have to persist for four months to cause enough price pressure to harm the US economy and decrease Trump’s chances of winning reelection. The simulations in Chart 30 overstate the gasoline price impact by assuming that global oil reserves remain untapped. Thus while the Iranians may take excessive risks, the Trump administration may not refrain this time from airstrikes. Bottom Line: While the Middle East is always full of risks to oil supply, Iran’s vulnerability and Trump’s status at home make the situation unusually precarious. A historic oil supply disruption is a fatter tail risk than investors realize. Europe Is A Price Taker, Not A Price Maker Just as the US and China have a shared incentive to avoid tariff-induced recession, so the UK and EU have a shared incentive to prevent a shock reversion to basic WTO tariffs. The December 31, 2020 deadline for the UK-EU trade deal, like the various deadlines for Brexit itself, can be delayed. Even Prime Minister Boris Johnson has proved unwilling to exit without a deal and even a hung parliament has proved capable of preventing him from doing so. The negotiation of a trade deal – which is never easy and always drags on – will be a lower-order risk in the wake of the past two years’ Brexit-induced volatility. Johnson will not be held hostage by hardline Brexiters given that Brexit itself will be complete. If our view on Chinese growth is correct, then Europe’s economy can recover and European political risk will be a “red herring” in 2020, as it was in 2019. Instead the EU presents an opportunity. Chart 31Euro Area Breakup Risk Has Subsided

2020 Key Views: The Anarchic Society

2020 Key Views: The Anarchic Society

Euro Area break-up risk has subsided after a series of challenges in the wake of the sovereign debt crisis (Chart 31). There is not a basis for a reversal of this trend, at least not until a full-blown recession afflicts the continent. The rise in anti-establishment parties coincided with a one-off surge in migration that is finished – and successful populists from Greece to Italy have moderated on euro membership once in power. Germany is entering a profound transition driven by de-globalization and tensions with the United States. It is more likely to have an early election than the consensus holds. But it is fundamentally stable and supportive of European integration. In fact the great debate about fiscal policy poses an upside risk over the long run both for European equities and the European project. We remain optimistic on French structural reforms even though President Emmanuel Macron must overcome significant public opposition. An eerie quiet hangs over Russia, making it one of our “Black Swan” risks for 2020. Oil prices are not very high, which discourages foreign adventures, and President Vladimir Putin has spent his fourth term trying to consolidate international gains and improve domestic stability. But approval of the government is weak, the job market is deteriorating, and social unrest is cropping up. There is plenty of room to ease monetary and fiscal policy, but a sharp downturn could provide the basis for an aggressive foreign policy action to shore up regime support. The US election also presents the risk of renewed US-Russian tensions, whether over election interference or a Democratic victory. Investment Conclusions Geopolitics is the likeliest candidate to derail the global bull market in 2020. Nevertheless, policymakers are adjusting to their constraints. Trump and Xi are negotiating a ceasefire and a disorderly Brexit is off the table. Even Trump’s impeachment shows that the US system of checks and balances remains intact. After all, there is nothing to prevent removal from office if Trump further antagonizes public opinion and the Republican Senate. This means that policy uncertainty will decline on the margin in 2020, even as it remains elevated due to the danger of the underlying events. The nature of US economic imbalances suggests that the policy discontinuity of a Democratic victory on November 3, 2020 would be better for the economy (via household consumption) than it would be for corporate earnings. Policy continuity with the Trump administration suggests the opposite. On a sectoral basis we recommend going long US energy large cap stocks and short info-tech and communications. Energy has limited downside even if a progressive wins whereas tech has limited upside even if Trump wins. The BCA Research House View expects the US dollar to weaken as global growth rebounds, stocks to outperform bonds and cash, and developed market equities to outperform those of the United States. But a Republican victory in November would push against these trends as it is more bullish for the greenback and for US equities relative to global. As a play on the global growth rebound we expect, we recommend going long industrial metals. Like our colleagues at BCA Research Commodity & Energy Strategy, we are initiating this as a tactical trade but it may become strategic. We are reinitiating a tactical long Korea / short Taiwan equity trade. Taiwanese political risk is understated ahead of January’s election and the island is the epicenter of the US-China cold war. We are restoring our long gold trade as a strategic hedge. Populism and de-globalization are potentially inflationary, but they are also linked with great power competition which will increase the frequency of geopolitical crises. In either case, gold is the right safe haven to own. Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com

Germany is wading deeper into a period of political risk surrounding Chancellor Angela Merkel’s “lame duck” phase. The federal election of 2021 already looms large. Our indicator is only beginning to price this trend which can last for the next two years. …

Highlights The US-China trade talks will continue despite Hong Kong. The UK election will not reintroduce no-deal Brexit risk – either in the short run or the long run. European political risk is set to rise from low levels, but Euro Area break-up risk will not. There is no single thread uniting emerging market social unrest. We remain constructive on Brazil. Feature Chart 1Taiwan Indicator To Rise Despite Ceasefire

Taiwan Indicator To Rise Despite Ceasefire

Taiwan Indicator To Rise Despite Ceasefire

President Trump signed the Hong Kong Human Rights and Democracy Act into law on November 27. The signing was by now expected – Trump was not going to veto the bill and invite the Senate to override him with a 67-vote at a time when he is being impeached. He does not want to familiarize the Senate with voting against him in supermajorities. The Hong Kong bill will not wreck the US-China trade talks, but it is a clear example of our argument that strategic tensions will persist and cast doubt on the durability of the “phase one trade deal” being negotiated. It is better to think of it as a ceasefire, as Trump’s electoral constraint is the clear motivation. Trump is embattled at home and will contend an election in 11 months. He will not impose the tariff rate hike scheduled for December 15. A relapse into trade war would kill the green shoots in US and global growth, which partly stem from the perception of easing trade risk. Only if Trump’s approval rating collapses, or China stops cooperating, will he become insensitive to his electoral constraint. Will China abandon the talks and leave Trump in the lurch? This is not our base case but it is a major global risk. So far China is reciprocating. Xi Jinping’s political and financial crackdown at home, combined with the trade war abroad, has led to an economic slowdown and an explosion in China’s policy uncertainty relative to America’s. A trade ceasefire – on top of fiscal easing – is a way to improve the economy without engaging in another credit splurge. The US and China will continue moving toward a trade ceasefire, despite the Hong Kong bill. The move toward a trade ceasefire will probably keep our China GeoRisk Indicator from rising sharply over the next few months. However, our Taiwan indicator, which we have used as a trade war proxy at times, may diverge as it starts pricing in the heightened political risk surrounding Taiwan’s presidential election on January 11, 2020 (Chart 1). Sanctions, tech controls, Hong Kong, Taiwan, North Korea, Iran, the South China Sea, and Xinjiang are all strategic tensions that can flare up. Yes, uncertainty will fall and sentiment will improve on a ceasefire, but only up to a point. China’s domestic policy decisions are ultimately more important than its handling of the trade war. At the upcoming Central Economic Work Conference authorities are expected to stay focused on “deepening supply-side structural reform” and avoiding the use of “irrigation-style” stimulus (blowout credit growth). But this does not mean they will not add more stimulus. Since the third quarter, a more broad-based easing of financial controls and industry regulations is apparent, leading our China Investment Strategy to expect a turning point in the Chinese economy in early 2020. This “China view” – on stimulus and trade – is critical to the outlook for the two regions on which we focus for the rest of this report: Europe and emerging markets. Assuming that China stabilizes, these are the regions where risk assets stand to benefit the most. Europe is a political opportunity; the picture in emerging markets is, as always, mixed. United Kingdom: Will Santa Bring A Lump Of Coal? The Brits will hold their first winter election since 1974 on December 12. Prime Minister Boris Johnson’s Conservative Party has seen a tremendous rally in opinion polls, although it has stalled at a level comparable to its peak ahead of the last election in June 2017 (Chart 2). Another hung parliament or weak Tory coalition is possible. Yet the Tories are better positioned this time given that the opposition Labour Party is less popular than two years ago, while the Liberal Democrats are more capable of stealing Labour votes. The Tories stand to lose in Scotland, but the Brexit Party of Nigel Farage is not contesting seats with them and is thus undercutting Labour in certain Brexit-leaning constituencies. Markets would enjoy a brief relief rally on a single-party Tory majority. This would enable Johnson to get his withdrawal deal over the line and take the UK out of the EU in an orderly manner by January 31. The question would then shift to whether Johnson feels overconfident in negotiating the post-Brexit trade agreement with the EU, which is supposed to be done by December 31, 2020. This date will become the new deadline for tariff increases, but it can be extended. Johnson is as unlikely to fly off the cliff edge next year as he was this year, and this year he demurred. Negotiating a trade agreement is easier when the two economies are already integrated, have a clear (yet flexible) deadline, and face exogenous economic risks. Our political risk indicator will rise but it will not revisit the highs of 2018-19 (Chart 3). The pound’s floor is higher than it was prior to September 2019. Chart 2Tories Look To Be Better Positioned For A Single Party Majority

Tories Look To Be Better Positioned For A Single Party Majority

Tories Look To Be Better Positioned For A Single Party Majority

Chart 3UK Risk Will Rise, But Not To Previous Highs

UK Risk Will Rise, But Not To Previous Highs

UK Risk Will Rise, But Not To Previous Highs

Bottom Line: A hung parliament is the only situation where a no-deal Brexit risk reemerges in advance of the new Brexit day of January 31. The market is underestimating this outcome based on our risk indicator. But Johnson himself prefers the deal he negotiated and wishes to avoid the recession that would likely ensue from crashing out of the EU. And a headless parliament can prevent Johnson from forcing a no-deal exit, as investors witnessed this fall. We remain long GBP-JPY. Germany: The Risk Of An Early Election Germany is wading deeper into a period of political risk surrounding Chancellor Angela Merkel’s “lame duck” phase, doubts over her chosen successor, and uncertainty about Germany’s future in the world. The federal election of 2021 already looms large. Our indicator is only beginning to price this trend which can last for the next two years (Chart 4). On October 27 Germany’s main centrist parties suffered a crushing defeat in the state election of Thuringia. For the first time, the Christian Democratic Union (CDU) not only lost its leadership position, but also secured less vote share than both the Left Party and the right-wing Alternative für Deutschland (AfD) (Chart 5, top panel). Chart 4Germany Is Heading Toward A Period Of Greater Political Risk

Germany Is Heading Toward A Period Of Greater Political Risk

Germany Is Heading Toward A Period Of Greater Political Risk