Elections

Highlights Our top five geopolitical “Black Swans” are risks that the market is seriously underpricing. With the “phase one” trade deal signed, Chinese policy could become less accommodative, resulting in a negative economic surprise. The trade deal may fall victim to domestic politics, raising the risk of a US-China military skirmish. A Biden victory at the Democratic National Convention or a Democratic takeover of the White House could trigger social unrest and violence in the US. A pickup in the flow of migrants to Europe would fundamentally undermine political stability there. Russia’s weak economy will add fuel to domestic unrest, risking an escalation beyond the point of containment. Feature Over the past four years, we have started off the year with our top five geopolitical “Black Swans.” These are low-probability events whose market impact would be significant enough to matter for global investors. Unlike the great Byron Wien’s perennial list of market surprises, we do not assign these events a “better than 50% likelihood of happening.” We offer risks that the market is seriously underpricing by assigning them only single-digit probabilities when we think the reality is closer to 10%-15%, a level at which a risk premium ought to be assigned. Some of our risks below are so obscure that it is not clear how exactly to price them. We exclude issues that are fairly probable, such as flare-ups in Indo-Pakistani conflict. The two major risks of the year – discussed in our annual outlook – are that either US President Donald Trump or Chinese President Xi Jinping overreaches in a major way. But what would truly surprise the market would be a policy-induced relapse in Chinese growth or a direct military clash between the two great powers. That is how we begin. Other risks stem from domestic affairs in the US, Europe, and Russia. Black Swan 1: China’s Financial Crisis Begins The risk of Xi Jinping’s concentration of power in his own person is that individuals can easily make mistakes, especially if unchecked by advisors or institutions. Lower officials will fear correcting or admonishing an all-powerful leader. Inconvenient information may not be relayed up the hierarchy. Such behavior was rampant in Chairman Mao Zedong’s time, leading to famine among other ills. Insofar as President Xi’s cult of personality successfully imitates Mao’s, it will be subject to similar errors. If President Xi overreaches and makes a policy mistake this year, it could occur in economic policy or other policies. We begin with economic policy, as we have charted the risks of Xi’s crackdown on the financial system since early 2017 (Chart 1). Chart 1A Crackdown On Financial Risk Could Cause China's Economy To Derail

A Crackdown On Financial Risk Could Cause China's Economy To Derail

A Crackdown On Financial Risk Could Cause China's Economy To Derail

Chart 2Easing Of Trade Tensions May Re-Incentivize Tighter Policy

Easing Of Trade Tensions May Re-Incentivize Tighter Policy

Easing Of Trade Tensions May Re-Incentivize Tighter Policy

This year is supposed to be the third and final year of Xi Jinping’s “three battles” against systemic risk, pollution, and poverty. The first battle actually focuses on financial risk, i.e. China’s money and credit bubble. The regime has compromised on this goal since mid-2018, allowing monetary easing to stabilize the economy amid the trade war. But with a “phase one” trade deal having been signed, there is an underrated risk that economic policy will return to its prior setting, i.e. become less accommodative (Chart 2). When Xi launched the “deleveraging campaign” in 2017, we posited that the authorities would be willing to tolerate an annual GDP growth rate below 6%. This would not only cull excesses in the economy but also demonstrate that the administration means business when it says that China must prioritize quality rather than quantity of growth. While Chinese authorities are most likely targeting “around 6%” in 2020, it is entirely possible that the authorities will allow an undershoot in the 5.5%-5.9% range. They will argue that the GDP target for 2020 has already been met on a compound growth rate basis (Chart 3), as astute clients have pointed out. They may see less need for stimulus than the market expects. Chart 3Chinese Authorities Might Tolerate A Growth Undershoot In 2020

Chinese Authorities Might Tolerate A Growth Undershoot In 2020

Chinese Authorities Might Tolerate A Growth Undershoot In 2020

Similarly, while urban disposable income is ostensibly lagging its target of doubling 2010 levels by 2020, China’s 13th Five Year Plan, which concludes in 2020, conspicuously avoided treating urban and rural income targets separately. Chart 4Lower Impetus For Economic Support Due To Improvements In National Income?

Lower Impetus For Economic Support Due To Improvements In National Income?

Lower Impetus For Economic Support Due To Improvements In National Income?

Chart 5Has China's Stimulus Peaked?

Has China's Stimulus Peaked?

Has China's Stimulus Peaked?

If the authorities focus only on general disposable income, then they are on track to meet their target (Chart 4). This would reduce the impetus for greater economic support. There are already tentative signs that Chinese authorities are “satisfied” with the amount of stimulus they have injected: some indicators of money and credit have already peaked (Chart 5). The crackdown on shadow banking has eased, but informal lending is still contracting. The regime is still pushing reforms that shake up state-owned enterprises. The Xi administration may aim only for stability, not acceleration, in the economy. An added headwind for the Chinese economy stems from the currency. The currency should track interest rate differentials. Beijing’s incremental monetary stimulus, in the form of cuts to bank reserve requirement ratios (RRRs), should also push the renminbi down over time (Chart 6). However, an essential aspect of any trade deal with the Trump administration is the need to demonstrate that China is not competitively devaluing. Hence the CNY-USD could overshoot in the first half of the year. This is positive for global exports to China, but it tightens Chinese financial conditions at home. A stronger than otherwise justified renminbi would add to any negative economic surprises from less accommodative monetary and fiscal policy. Conventional wisdom says China will stimulate the economy ahead of two major political events: the centenary of the Communist Party in 2021 and the twentieth National Party Congress in 2022. The former is a highly symbolic anniversary, as Xi has reasserted the supremacy of the party in all things, while the latter is more significant for policy, as it is a leadership reshuffle that will usher in the sixth generation of China’s political elite. But conventional wisdom may be wrong – the Xi administration may aim only for stability, not acceleration, in the economy. It would make sense to save dry powder for the next US or global recession. The obvious implication is that China’s economic rebound may lose steam as early as H2 – but the black swan risk is that negative surprises could cause a vicious spiral inside of China. This is a country with massive financial and economic imbalances, a declining potential growth profile, and persistent political obstacles to growth both at home and abroad. Corporate defaults have spiked sharply. While the default rate is lower than elsewhere, the market may be sniffing out a bigger problem as it charges a much higher premium for onshore Chinese bonds (Chart 7). Chart 6CNY-USD Overshoot Would Tighten Chinese Financial Conditions

CNY-USD Overshoot Would Tighten Chinese Financial Conditions

CNY-USD Overshoot Would Tighten Chinese Financial Conditions

Chart 7Is China's Bond Market Sniffing Out A Problem?

Is China's Bond Market Sniffing Out A Problem?

Is China's Bond Market Sniffing Out A Problem?

Bottom Line: Our view is that China’s authorities will remain accommodative in 2020 in order to ensure that growth bottoms and the labor market continues to improve. But Beijing has compromised its domestic economic discipline since 2018 in order to fight trade war. The risk now, with a “phase one” deal in hand, is that Xi Jinping returns to his three-year battle plan and underestimates the downward pressures on the economy. The result would be a huge negative surprise for the Chinese and global economy in 2020. Black Swan 2: The US And China Go To War In 2013, we predicted that US-China conflict was “more likely than you think.” This was not just an argument for trade conflict or general enmity that raises the temperature in the Asia-Pacific region – we included military conflict. Chart 8Americans' Attitudes Toward China Plunged …

Five Black Swans In 2020

Five Black Swans In 2020

At the time, the notion that a Sino-American armed conflict was the world’s greatest geopolitical threat seemed ludicrous to many of our clients. We published this analysis in October of that year, months after the Islamic State “Soldier’s Harvest” offensive into Iraq. Trying to direct investors to the budding rivalry between American and Chinese naval forces in the South China Sea amidst the Islamic State hysteria was challenging, to say the least. The suggestion that an accidental skirmish between the US and China could descend into a full-blown conflict involved a stretch of the imagination because China was not yet perceived by the American public as a major threat. In 2014, only 19%of the US public saw China as the “greatest threat to the US in the future.” This came between Russia, at 23%, and Iran, at 16%. Today, China and Russia share the top spot with 24%. Furthermore, the share of Americans with an unfavorable view of China has increased from 52% to 60% in the six intervening years (Chart 8). The level of enmity expressed by the US public toward China is still lower than that toward the Soviet Union at the onset of the Cold War in the 1950s (Chart 9). However, the trajectory of distrust is clearly mounting. We expect this trend to continue: anti-China sentiment is one of the few sources of bipartisan agreement remaining in Washington, DC (Chart 10). Chinese sentiment toward the United States has also darkened dramatically. The geopolitical rivalry is deepening for structural reasons: as China advances in size and sophistication, it seeks to alter the regional status quo in its favor, while the US grows fearful and seeks to contain China. Chart 9… But Not Yet To War-Inducing Levels

Five Black Swans In 2020

Five Black Swans In 2020

Chart 10Distrust Of China Is Bipartisan

Five Black Swans In 2020

Five Black Swans In 2020

Chart 11Newfound American Concern For China’s Repression

Five Black Swans In 2020

Five Black Swans In 2020

One example of rising enmity is the US public’s newfound concern for China’s domestic policies and human rights, specifically Beijing’s treatment of its Uyghur minority in Xinjiang. A Google Trends analysis of the term “Uyghur” or “Uyghur camps” shows a dramatic rise in mentions since Q2 of 2018, around the same time the trade war ramped up in a major way (Chart 11). While startling revelations of re-education camps in Xinjiang emerged in recent years, the reality is that Beijing has used heavy-handed tactics against both militant groups and the wider Uyghur minority since at least 2008 – and much earlier than that. As such, the surge of interest by the general American public and legislators – culminating in the Uyghur Human Rights Policy Act of 2019 – is a product of the renewed strategic tension between the two countries. The “phase one” trade deal risks falling victim to domestic politics due to greater public engagement in foreign policy. The same can be said for Hong Kong: the US did not pass a Hong Kong Human Rights and Democracy Act in 2014, during the first round of mass protests, which prompted Beijing to take heavy-handed legal, legislative, and censorship actions. It passed the bill in 2019, after the climate in Washington had changed. Why does this matter for investors? There are two general risks that come with a greater public engagement in foreign policy. First, the “phase one” trade deal between China and the US could fall victim to domestic politics. This deal envisions a large step up in Sino-American economic cooperation. But if China is to import around $200 billion of additional US goods and services over the next two years – an almost inconceivable figure – the US and China will have to tamp down on public vitriol. This is notably the case if the Democratic Party takes over the White House, given its likely greater focus on liberal concerns such as human rights. And yet the latest bills became law under President Trump and a Republican Senate, and we fully expect a second Trump term to involve a re-escalation of trade tensions to ensure compliance with phase one and to try to gain greater structural concessions in phase two. Second, mounting nationalist sentiment will make it more difficult for US and Chinese policymakers to reduce tensions following a potential future military skirmish, accidental or otherwise. While our scenario of a military conflict in 2013 was cogent, the public backlash in the United States was probably manageable.1 Today we can no longer guarantee that this is the case. China has greater control over the domestic narrative and public discourse, but the rise of the middle class and the government’s efforts to rebuild support for the single-party regime have combined to create an increase in nationalism. Thus it is also more difficult for Chinese policymakers to contain the popular backlash if conflict erupts. In short, the probability of a quick tamping down of public enmity is actively being reduced as American public vilification of China is closing the gap with China’s burgeoning nationalism at an alarming pace. Chart 12Tsai Ing-Wen Enjoys A Greater Mandate On Higher Turnout …

Five Black Swans In 2020

Five Black Swans In 2020

Another of our black swan risks – Taiwan island – is inextricably bound up in this dangerous US-China dynamic. To be clear, Washington will tread carefully, as a conflict over Taiwan could become a major war. Nevertheless Taiwan’s election, as we expected, has injected new vitality into this already underrated geopolitical risk. It is not only that a high-turnout election (Chart 12) gave President Tsai Ing-wen a greater mandate (Chart 13), or that her Democratic Progressive Party retained its legislative majority (Chart 14). It is not only that the trigger for this resounding victory was the revolt in Hong Kong and the Taiwanese people’s rejection of the “one country, two systems” formula for Taiwan. It is also that Tsai followed up with a repudiation of the mainland by declaring, “We don’t have a need to declare ourselves an independent state. We are an independent country already and we call ourselves the Republic of China, Taiwan.” Chart 13… Popular Support …

Five Black Swans In 2020

Five Black Swans In 2020

Chart 14… And A Legislative Majority

Five Black Swans In 2020

Five Black Swans In 2020

This statement is not a minor rhetorical flourish but will be received as a major provocation in Beijing: the crystallization of a long-brewing clash between Beijing and Taipei. Additional punitive economic measures against Taiwan are now guaranteed. Saber-rattling could easily ignite in the coming year and beyond. Taiwan is the epicenter of the US-China strategic conflict. First, Beijing cannot compromise on its security or its political legitimacy and considers the “one China principle” to be inviolable. Second, the US maintains defense relations with Taiwan (and is in the process of delivering on a relatively large new package of arms). Third, the US’s true willingness to fight a war on Taiwan’s behalf is in doubt, which means that deterrence has eroded and there is greater room for miscalculation. Bottom Line: A US-China military skirmish has been our biggest black swan risk since we began writing the BCA Geopolitical Strategy. The difference between then and now, however, is that the American public is actually paying attention. Political ideology – the question of democracy and human rights – is clearly merging with trade, security, and other differences to provoke Americans of all stripes. This makes any skirmish more than just a temporary risk-off event, as it could lead to a string of incidents or even protracted military conflict. Black Swan 3: Social Unrest Erupts In America There are numerous lessons that one can learn from the ongoing unrest in Hong Kong, but perhaps the most cogent one is that Millennials and Generation Z are not as docile and feckless as their elders think. Images of university students and even teenagers throwing flying kicks and Molotov cocktails while clad in black body armor have shocked the world. Perhaps all those violent video games did have a lasting impact on the youth! What is surprising is that so few commentators have made the cognitive leap from the ultra-first world streets of Hong Kong to other developed economies. Perhaps what is clouding analysts’ minds is the idiosyncratic nature of the dispute in Hong Kong, the “one China” angle. However, Hong Kong youth are confronted with similar socio-economic challenges that their peers in other advanced economies face: overpriced real estate and a bifurcated service-sector labor market with few mid-tier jobs that pay a decent wage. In the US, Millennials and Gen Z are also facing challenges unique to the US. First, their debt burden is much more toxic than that of the older cohorts, given that it is made up of student loans and credit card debt (Chart 15). Second, they find themselves at odds – demographically and ideologically – with the older cohorts (Chart 16). Chart 15Younger American Cohorts Plagued By Toxic Debt

Five Black Swans In 2020

Five Black Swans In 2020

Chart 16Younger And Older Cohorts At Odds Demographically

Five Black Swans In 2020

Five Black Swans In 2020

The adage that the youth are apolitical and do not turn out to vote may have ended thanks to President Trump. The 2018 midterm election, which the Democratic Party successfully turned into a referendum on the president, saw the youth (18-29) turnout nearly double from 20% to 36% (the 30-44 year-old cohort also saw a jump in turnout from 35.6% to 48.8%). The election saw one of the highest turnouts in recent memory, with a 53.4% figure, just two points off the 2016 general election figure (Chart 17). Chart 17Massive Turnout To The 2016 Referendum On Trump

Five Black Swans In 2020

Five Black Swans In 2020

Despite the high turnout in 2018, the-most-definitely-not-Millennial Vice President Joe Biden continues to lead the Democratic Party in the polls. Chart 18Biden Unpopular Among Young American Voters

Five Black Swans In 2020

Five Black Swans In 2020

Chart 19Bookies Pulled Down "Uncle Joe's" Odds, Capturing Democratic Party Zeitgeist

Five Black Swans In 2020

Five Black Swans In 2020

His probability of winning the nomination is not overwhelming, but it is the highest of any contender. In recent polls, Biden comes third place in Millennial/Gen-Z vote preferences (Chart 18). Yet he is hardly out of contention, especially for the 30-44 year-old cohort. The view that “Uncle Joe” does not fit the Democratic Party zeitgeist has become so entrenched in the Democratic Party narrative that it became conventional wisdom last year, pulling oddsmakers and betting markets away from the clear frontrunner (Chart 19). As such, a Biden victory at the Democratic National Convention in Milwaukee, Wisconsin on July 13-16 may come as an affront to the left-wing activists who will surely descend on the convention. This will particularly be the case if Biden wins despite the progressive candidates amassing a majority of overall delegates, which is possible judging by the combined progressive vote share in current polling (Chart 20). He would arrive in Milwaukee without clearing the 1990 delegate count required to win on the first ballot. On the second ballot, his presidency would then receive a boost from “superdelegates” and those progressives who are unwilling to “rock the boat,” i.e. unify against an establishment candidate with the largest share of votes. This is also how Mayor Michael Bloomberg could pull off a surprise win. Chart 20Progressives Come Closest To Victory

Five Black Swans In 2020

Five Black Swans In 2020

Such a “brokered” – or contested – convention has not occurred since 1952. However, several Democratic Party conventions came close, including 1968, 1972, and 1984. The 1968 one in Chicago was notable for considerable violence and unrest. Even if the Milwaukee Democratic Party convention does not produce unrest, it could sow the seeds for unrest later in the year. First, a breakout Biden performance in the primaries is unlikely. As such, he will likely need to pledge a shift to the left at the convention, including by accepting a progressive vice-presidential candidate. Second, an actual progressive may win the primary. Chart 21Zealots In Both Parties Perceive Each Other As A National Threat

Five Black Swans In 2020

Five Black Swans In 2020

It is likely that either of the two options would be seen as an existential threat to many of Trump’s loyal supporters across the United States. President Trump’s rhetoric often paints the scenario of a Democratic takeover of the White House in apocalyptic terms. And data suggests that the zealots in both parties perceive each other as a “threat to the nation’s wellbeing” (Chart 21). The American Civil War in the nineteenth century began with the election of a president. This is not just because Abraham Lincoln was a particularly reviled figure in the South, but because the states that ultimately formed the Confederacy saw in his election the demographic writing-on-the-wall. The election was an expression of a general will that, from that point onwards, was irreversible. Given demographic trends in the US today, it is possible that many would see in Trump’s loss a similar fait accompli. If one perceives progressive Democrats as an existential threat to the US constitution, rebellion is the obvious and rational response. There is a risk of rebellion from Trump’s most ardent supporters if he loses the White House. Bottom Line: Year 2020 may be a particularly violent one for the US. First, left wing activists may be shocked and angered to learn that Joe Biden (or Bloomberg) is the nominee of the Democratic Party come July. With so much hype behind the progressive candidates throughout the campaign, Biden’s nomination could be seen as an affront to what was supposed to be “the big year” for left-wing candidates. Second, investors have to start thinking about what happens if Biden – or a progressive candidate – goes on to defeat President Trump in the general election. While liberal America took Trump’s election badly, it has demographics – and thus time – on its side. Trump’s most ardent supporters may conclude that his defeat means the end of America as they know it. Black Swan 4: Europe’s Migration Crisis Restarts Chart 22Decline In Illegal Immigration Dampened European Populism

Five Black Swans In 2020

Five Black Swans In 2020

It is a testament to Europe’s resilience that we do not have a Black Swan scenario based on an election or a political crisis set on the continent in 2020. Support for the common currency and the EU as a whole has rebounded to its highest since 2013. Even early elections in Germany and Italy are unlikely to produce geopolitical risk. The populists in the former are in no danger of outperforming whereas the populists in the latter barely deserve the designation. But what if one of the reasons for the surge in populism – unchecked illegal immigration – were to return in 2020? The data suggests that the risk of migrant flows has massively subsided. From its peak of over a million arrivals in 2015, the data shows that only 125,472 migrants crossed into Europe via land and sea routes in the Mediterranean last year (Chart 22). Why? There are five reasons that we believe have checked the flow of migrants: Supply: The civil wars in Syria, Iraq, and Libya have largely subsided. Heterogenous regions, cities, and neighborhoods have been ethnically cleansed and internal boundaries have largely ossified. It is unlikely that any future conflict will produce massive outflows of refugees as the displacement has already taken place. These countries are now largely divided into armed, ethnically homogenous, camps. Enforcement: The EU has stepped up border enforcement since 2015, pouring resources into the land border with Turkey and naval patrols across the Mediterranean. Individual member states – particularly Italy and Hungary – have also stepped up border enforcement policy. While most EU member states have publicly chided both for “draconian” policies, there is no impetus to force Rome and Budapest to change policy. Libyan Imbroglio: Conflict in Libya has flared up in 2019 with military warlord Khalifa Haftar looking to wrest control from the UN-backed Government of National Accord led by Fayez al-Serraj. The Islamic State has regrouped in the country as well. Ironically, the conflict is helping stem the flow of migrants as African migrants from sub-Saharan countries dare not cross into Libya as they did in 2015 when there was a brief lull in fighting. Turkish benevolence: Ankara is quick to point out that it is the only thing standing between Europe and a massive deluge of migrants. Turkey is said to host somewhere between two and four million refugees from various conflicts in the Middle East. Fear of the crossing: If crossing the Mediterranean was easy, Europe would have experienced a massive influx of migrants throughout the twentieth century. Not only is it not easy, it is costly and quite deadly, with thousands lost each year. Furthermore, most migrants are not welcomed when they arrive to Europe, many are held in terrible conditions in holding camps in Italy and Greece. Over time, migrants who made it into Europe have reported these dangers and conditions, reducing the overall demand for illegal migration. We do not foresee these five factors changing, at least not all at once. However, there are several reasons to worry about the flow of migrants in 2020. US-Iran tensions have sparked outright military action, while unrest is flaring up across Iran’s sphere of influence. Going forward, Iran could destabilize Iraq or fuel Shia unrest against US-backed regimes. Second, Afghanistan has been the source of most migrants to Europe via sea and land Mediterranean routes – 19.2%. The conflict in the country continues and may flare up with President Trump’s decision to formally withdraw most US troops from the country in 2020. Third, a break in fighting in Libya may encourage sub-Saharan migrants to revisit routes to Europe. Migrants from Guinea, Cote d’Ivoire, and the Democratic Republic of Congo make up over 10% of migrants to Europe. Finally, Turkish relationship with the West could break up further in 2020, causing Ankara to ship migrants northward. We highly doubt that President Erdogan will risk such a break, given that 50% of Turkish exports go to Europe. A European embargo on Turkish exports – which would be a highly likely response to such an act – would crush the already decimated Turkish economy. Bottom Line: While we do not see a return to the 2015 level of migration in 2020, we flag this risk because it would fundamentally undermine political stability in Europe. Black Swan 5: Russia Faces A “Peasant Revolt” Our fifth and final black swan risk for the year stems from Russia. This risk may seem obvious, since the US election creates a dynamic that revives the inherent conflict in US-Russian relations. Russia could seek to accomplish foreign policy objectives – interfering in US elections, punishing regional adversaries. The Trump administration may be friendly toward Russia but Trump is unlikely to veto any sanctions passed by the House and Senate in an election year, should an occasion for new sanctions arise. Conversely Russia could anticipate greater US pressure if the Democrats win in November. Yet it is Russia’s domestic affairs that represent the real underrated risk. Putin’s fourth term as president has been characterized by increased focus on domestic political control and stability as opposed to foreign adventurism. The creation of a special National Guard in 2016, reporting directly to Putin and responsible for quelling domestic unrest, symbolizes the shift in focus. So too does Russia’s adherence to the OPEC 2.0 regime of production control to keep oil prices above their budget breakeven level. Meanwhile Putin’s courting of Europe for the Nordstream II pipeline, and his slight peacemaking efforts with Ukraine, has suggested a slightly more restrained international posture. Chart 23Sluggish Wage Growth Threatens Russian Stability

Sluggish Wage Growth Threatens Russian Stability

Sluggish Wage Growth Threatens Russian Stability

Strategically it makes little sense for Russia to court negative attention at a time when the US and Europe are at odds over trade and the Middle East, the US is preoccupied with China and Iran, and Russia itself faces mounting domestic problems. The domestic problems are long in coming. The central bank has maintained a stringent monetary policy for the better part of the decade. Despite cutting interest rates recently, monetary and credit conditions are still tight, hurting domestic demand. Moscow has also imposed fiscal austerity, namely by cutting back on state pensions and hiking the value added tax. Real wage growth is weak (Chart 23), retail sales are falling, and domestic demand looks to weaken further, as Andrija Vesic of BCA Emerging Markets Strategy observes in a recent Special Report. The effect of Russia’s policy austerity has been a drop in public approval of the administration (Chart 24). Protests erupted in 2019 but were largely drowned out by the larger and more globally significant protests in Hong Kong. These were met by police suppression that has not removed their underlying cause. Putin’s first major decision of the new year was to reshuffle the government, entailing Prime Minister Dmitri Medvedev’s transfer to a new post and the appointment of a new cabinet. This move reveals the need to show some accountability to reduce popular pressure. While Moscow now has room to cut interest rates and ease fiscal policy, it is behind the curve and the weak economy will add fuel to domestic unrest. Meanwhile Putin’s efforts to alter the Russian constitution so he can stay in power beyond current term limits, effectively becoming emperor for life, like Xi Jinping, should not be dismissed merely because they are expected. They reflect a need to take advantage of Putin’s popular standing to consolidate domestic political power at a time when the ruling United Russia party and the federal government face discontent. They also ensure that strategic conflict with the United States will take on an ideological dimension. Chart 24Austerity Weighed On The Administration's Popularity In Russia

Austerity Weighed On The Administration's Popularity In Russia

Austerity Weighed On The Administration's Popularity In Russia

Chart 25Russian Political Risk Is Unsustainably Low

Russian Political Risk Is Unsustainably Low

Russian Political Risk Is Unsustainably Low

Russia's recent cabinet shakeup is positive from the point of view of economic reform. And the country's monetary and fiscal room provide a basis for remaining overweight equities within EM, as our Emerging Markets Strategy recommends. However, Russian equities have rallied hard and the political risk is understated. Bottom Line: It is never easy predicting Putin’s next international move. Our market-based indicators of Russian political risk have hit multi-year lows, but both the domestic and international context suggest that these lows will not be sustained (Chart 25). A new bout of risk can emanate from Putin, or from changes in Washington, or from the Russian people themselves. What would take the world by surprise would be domestic unrest on a larger scale than Russia can easily suppress through the police force. Housekeeping We are closing our long European Union / short Chinese equities strategic trade with a 1.61% loss since inception on May 10, 2019. Dhaval Joshi of BCA’s European Investment Strategy downgraded the Eurostoxx 50 to underweight versus the S&P 500 and the Nikkei 225 this week. He makes the point that the Euro Area bond yield 6-month impulse hit 100 bps – a critical technical level – and will be a strong headwind to growth. We will look to reopen this trade at a later date when the euphoria over the “phase one” trade deal subsides, as we still favor European equities and DM bourses over EM. We will reinstitute our long Brent crude H2 2020 versus H2 2021 tactical position, which was stopped out on January 9, 2020. We remain bullish on oil fundamentals and expect Middle East instability to add a political risk premium. China's stimulus and the oil view also give reason for us to reinitiate our long Malaysian equities relative to EM as a tactical position. The Malaysian ringgit will benefit as oil prices move higher, helping Malaysian companies make payments on their large pile of dollar-denominated debt and improving household purchasing power. Higher oil prices also correlate with higher equity prices, while China's stimulus and the US trade ceasefire will push the US dollar lower and help trade revive in the region. Marko Papic Consulting Editor marko@bcaresearch.com Matt Gertken Vice President Geopolitical Strategist mattg@bcaresearch.com Footnotes 1 Observe how little attention the public paid to US-China saber-rattling around China’s announcement of an Air Defense Identification Zone in the East China Sea that year.

Highlights Duration: Despite recent setbacks, global growth looks set to improve and policy uncertainty set to ease during the next couple of months. Both will conspire to push bond yields higher. Investors should maintain below-benchmark portfolio duration. US political risks could flare again around mid-year, sending yields lower. TIPS: We recommend that investors enter TIPS breakeven curve flatteners, both because short-term inflation expectations will respond more quickly than long-term expectations to stronger realized inflation data and to hedge against the risk of an oil supply shock. High-Yield: Investors should add (or increase) exposure to the high-yield energy sector, within an overweight allocation to junk bonds. Junk energy spreads are attractive, and exposure to the sector will mitigate the impact of a potential oil supply shock. Feature Only a month ago, investors were becoming more optimistic about a global growth rebound and the US/China phase 1 trade deal was pushing political risk into the background. Both of those factors caused the 10-year Treasury yield to rise throughout December, hitting an intra-day Christmas Eve peak of 1.95% (Chart 1). But since then, softer global PMI data and the US/Iranian military conflict brought global growth concerns and political risk back to the fore, breaking the uptrend in yields. Chart 1Bond Bear On Pause

Bond Bear On Pause

Bond Bear On Pause

Global growth and political uncertainty are two of the five macro factors that we identify as important for US bond yields.1 And despite the recent setback, we think both factors will push yields higher in the coming months. Global Growth We have found that the Global Manufacturing PMI, the US ISM Manufacturing PMI and the CRB Raw Industrials index are the three global growth indicators that correlate most strongly with US bond yields. One reason for the recent pullback in yields is the disappointing December data from the Global and US Manufacturing PMIs. The ISM Manufacturing PMI moved deeper into recessionary territory. The Global Manufacturing PMI had been in a clear uptrend since mid-2019, but fell back to 50.1 in December, from 50.3 the month before (Chart 2). The US and Chinese PMIs also declined in December, though they remain well above the 50 boom/bust line (Chart 2, panels 3 & 4). The Eurozone and Japanese PMIs, meanwhile, are still in the doldrums (Chart 2, panels 2 & 5). More worrying than the small tick down in Global PMI is the US ISM Manufacturing PMI moving deeper into recessionary territory, from 48.1 to 47.2. However, we have good reason to think that stronger data are just around the corner (Chart 3). Chart 2Global PMI Ticks Down

Global PMI Ticks Down

Global PMI Ticks Down

Chart 3ISM Manufacturing Index Will Rebound

ISM Manufacturing Index Will Rebound

ISM Manufacturing Index Will Rebound

First, the difference between the new orders and inventories components of the ISM index often leads the overall index at turning points, 2016 being a prime example (Chart 3, top panel). Much like in 2016, a gap is opening up between new orders-less-inventories and the overall ISM. Second, the non-manufacturing ISM index remains strong despite the weakness in manufacturing (Chart 3, panel 2). With no contagion to the service sector of the economy, we’d expect manufacturing to pick back up. Third, the ISM Manufacturing index has diverged sharply from the Markit Manufacturing PMI, with the Markit index printing well above the ISM (Chart 3, panel 3).2 The ISM index has been more volatile than the Markit index in recent years, and should trend toward the Markit index over time. Fourth, regional Fed manufacturing surveys have generally been stronger than the ISM during the past few months. A simple regression model of the ISM index based on data from regional Fed surveys suggests that the ISM index should be at 49.7 today, instead of 47.2 (Chart 3, bottom panel). Finally, unlike the PMI surveys, the CRB Raw Industrials index has increased quite sharply in recent weeks (Chart 4). We should note that it is not the CRB index itself but rather the ratio between the CRB index and gold that tracks bond yields most closely, and this ratio has actually declined lately due to the strength in gold. Nonetheless, a sustained turnaround in the CRB index would mark a big change from 2019 and would send a strong bond-bearish signal. Chart 4CRB Sends A Bond-Bearish Signal

CRB Sends A Bond-Bearish Signal

CRB Sends A Bond-Bearish Signal

Political Uncertainty The second factor that sent bond yields lower during the past few weeks was the military conflict between the US and Iran. Tensions appear to have de-escalated for now, and we would expect any flight-to-quality flows to unwind during the next few weeks.3 But while we see policy uncertainty easing in the near-term, sending bond yields higher, we reiterate our view that US political uncertainty is the number one risk factor that could derail the 2020 bear market in bonds.4 Specifically, we see two looming US political risks. The first relates to President Trump’s re-election odds. For now, Trump’s approval rating is in line with past incumbent presidents that have won re-election (Chart 5). But if his approval doesn’t keep pace in the coming months, he will try to do something to change his fortunes. That could mean re-igniting the trade war with China, or once again ramping up tensions with Iran. A Bernie Sanders or Elizabeth Warren victory would send a flight-to-quality into bonds. The second risk is that one of the progressive candidates – Bernie Sanders or Elizabeth Warren – secures the Democratic nomination for president. Right now, both trail Joe Biden in the polls and betting markets (Chart 6), but things could change rapidly as the primary results come in during the next few months. The stock market would certainly sell off if an Elizabeth Warren or Bernie Sanders presidency seems likely, sending a flight to quality into bonds.5 Chart 5Trump’s Approval Rating Must Rise

Bond Market Implications Of An Oil Supply Shock

Bond Market Implications Of An Oil Supply Shock

Chart 6Democratic Nomination Betting Odds

Democratic Nomination Betting Odds

Democratic Nomination Betting Odds

Bottom Line: Despite recent setbacks, global growth looks set to improve and policy uncertainty set to ease during the next couple of months. Both will conspire to push bond yields higher. Investors should maintain below-benchmark portfolio duration. US political risks could flare again around mid-year, sending yields lower. Playing An Oil Supply Shock In US Bond Markets US/Iranian military tensions are easing for now, but could flare again in the future. For that reason, it’s worth considering how US bond markets would respond in the event of a conflict between the US and Iran that removed a significant amount of the world’s oil supply from the market, causing the oil price to spike. The first implication is that US bond yields would fall. Even though it’s tempting to say that the inflationary impact of higher oil prices would push yields up, this effect would not dominate the flight-to-quality into US bonds that would result from the increase in political uncertainty. Case in point, Chart 1 shows that, while the inflation component of yields was stable as tensions flared during the past few weeks, it didn’t come close to offsetting the drop in the 10-year real yield. Beyond the impact on Treasury yields, there are two other segments of the US bond market that would be materially impacted by an oil supply shock: the TIPS breakeven inflation curve and corporate bond spreads. Buy TIPS Breakeven Curve Flatteners Table 1CPI Swap Curve Sensitivity To Oil

Bond Market Implications Of An Oil Supply Shock

Bond Market Implications Of An Oil Supply Shock

When considering the impact of an oil supply shock on TIPS breakeven inflation rates, we first look at how the cost of inflation protection is influenced by changes in the oil price. Table 1 shows the sensitivity of weekly changes in different CPI swap rates to a $1 increase in the price of Brent crude oil. We use CPI swap rates instead of TIPS breakeven inflation rates because data are available for a wider maturity spectrum. Our analysis applies equally to the TIPS breakeven inflation curve. Two conclusions are apparent from Table 1. First, the entire CPI swap curve is positively correlated with the oil price, a higher oil price moves CPI swap rates higher and vice-versa. Second, the sensitivity of CPI swap rates to the oil price is greater at the short-end of the curve than at the long-end. This is fairly intuitive given that higher oil prices are inflationary in the short-term but could be deflationary in the long-run if they hamper economic growth. Chart 7Coefficients Stable Over Time

Coefficients Stable Over Time

Coefficients Stable Over Time

Chart 7 shows that our two main conclusions are not dependent on the chosen time horizon. The 2-year CPI swap rate is positively correlated with the oil price for our entire sample period, as is the 10-year rate except for a brief window in 2014. The 2-year rate’s sensitivity is also consistently higher than the 10-year’s. Based on this analysis, we can suggest two good ways to hedge against the risk of an oil supply shock that sends prices higher: Buy inflation protection, either in the CPI swaps market or by going long TIPS versus duration-equivalent nominal Treasuries. Buy CPI swap curve (or TIPS breakeven inflation curve) flatteners.6 But we can introduce one more wrinkle to our analysis. Oil prices can rise because of stronger demand or because a shock suddenly removes supply from the market. It’s possible that the cost of inflation protection behaves differently in each case. Fortunately, the New York Fed has made an attempt to distinguish between those two scenarios. In its weekly Oil Price Dynamics Report, the Fed decomposes Brent oil price changes into demand-driven changes and supply-driven changes.7 It does this by looking at how other financial assets respond to oil price changes each week. Chart 8 shows the cumulative change in the Brent oil price since 2010, along with the New York Fed’s supply and demand factors. According to the Fed, demand has pressured the oil price higher since 2010, but this has been more than offset by greater supply. Chart 8Supply & Demand Oil Price Decomposition

Supply & Demand Oil Price Decomposition

Supply & Demand Oil Price Decomposition

Using the New York Fed’s supply and demand series, we look at how CPI swap rates respond to higher oil prices in three different scenarios. First, we identify 252 weeks when demand and supply both contributed to higher oil prices. Second, we identify 95 weeks when higher oil prices were driven solely by demand. Finally, and most pertinently, we identify 92 weeks when higher oil prices were driven only by supply (Table 2). Table 2Weekly Change In CPI Swap Rate When Brent Oil Price Increases

Bond Market Implications Of An Oil Supply Shock

Bond Market Implications Of An Oil Supply Shock

Results for the ‘Demand & Supply Driven’ and ‘Demand Driven’ scenarios are consistent with our results from Table 1. CPI swap rates across the entire curve move higher more than half the time, with greater increases at the short-end of the curve. However, the scenario we are most interested in is the ‘Supply Driven’ scenario. Presumably, a military conflict with Iran that took oil supply off the market would lead to less supply and also a decrease in global demand. Results for this scenario are more mixed. The 1-year CPI swap rate still rises 60% of the time, but rates further out the curve are somewhat more likely to fall. With this in mind, CPI swap curve or TIPS breakeven curve flatteners look like the best way to hedge against an oil supply shock, better than an outright long position in inflation protection. This is good news, since we have previously argued that owning TIPS breakeven curve flatteners is a good idea even without an oil supply shock.8 Corporate bond excess returns respond positively to changes in the oil price. We recommend that investors enter TIPS breakeven curve flatteners, both because short-term inflation expectations will respond more quickly than long-term expectations to stronger realized inflation data and to hedge against the risk of an oil supply shock. Buy Energy Junk Bonds Table 3Corporate Bond Sensitivity To Oil

Bond Market Implications Of An Oil Supply Shock

Bond Market Implications Of An Oil Supply Shock

Corporate bonds are the second segment of the US fixed income market that could be materially impacted by an oil supply shock, particularly bonds in the energy sector. To assess the potential value of corporate bonds as a hedge, we repeat the above analysis but use weekly corporate bond excess returns versus duration-matched Treasuries instead of CPI swap rates. Table 3 shows that investment grade and high-yield corporate bond returns both respond positively to changes in the oil price. Further, we see that energy bonds are more sensitive to the oil price, outperforming the overall index when the oil price rises, and vice-versa. Chart 9 shows that, while oil price sensitivities vary considerably over time, they are almost always positive. Also, energy sector sensitivity has been consistently above that of the benchmark index since 2014. Chart 9Betas Mostly Positive

Betas Mostly Positive

Betas Mostly Positive

Going one step further, we once again use the New York Fed’s supply and demand decomposition to identify weeks when supply and/or demand was responsible for higher oil prices. Because we have more historical data for corporate bonds than for CPI swaps, this time we identify 340 weeks when both supply and demand drove the oil price higher, 123 weeks when only demand drove it higher and 142 weeks when only supply was responsible for the higher oil price (Table 4). Table 4Weekly Corporate Bond Excess Returns (BPs) When Brent Oil Price Increases

Bond Market Implications Of An Oil Supply Shock

Bond Market Implications Of An Oil Supply Shock

Results for the ‘Demand & Supply Driven’ and ‘Demand Driven’ scenarios show that higher oil prices boost excess returns to both investment grade and high-yield corporate bonds more than half the time. Energy bonds also tend to outperform their respective benchmark indexes in the ‘Demand & Supply Driven’ scenario, but perform roughly in-line with the benchmark in the ‘Demand Driven’ scenario. But once again, it is the ‘Supply Driven’ scenario that we are most interested in. Here, we see that an oil supply disruption that leads to higher oil prices also leads to lower corporate bond excess returns. This is true for both the investment grade and high-yield indexes and for energy bonds in both rating categories. However, we also note that high-yield energy debt significantly outperforms the overall junk index during these “risk off” periods. In contrast, investment grade energy debt is not a clear outperformer. Chart 10HY Energy Spreads Are Very Attractive

HY Energy Spreads Are Very Attractive

HY Energy Spreads Are Very Attractive

These results line up with our intuition. When oil prices are driven higher by demand it could simply be a sign of strong economic growth and not any specific trend related to the energy sector. As such, we’d expect all corporate bonds to perform well in those scenarios, but wouldn’t necessarily expect energy debt to outperform. However, supply disruptions in the Middle East directly benefit US shale oil players, whose debt is principally found in the high-yield energy sector. The investment grade energy sector is less exposed to the US shale space, and its documented outperformance in the ‘Supply Driven’ scenario is weaker as a result. We already recommend an overweight allocation to high-yield bonds and a neutral allocation to investment grade corporates. Within that overweight allocation to high-yield bonds, we recommend shifting some exposure toward the energy sector for two reasons. First, high-yield energy was severely beaten-down last year and is ripe for a rebound if global economic growth recovers, as we expect (Chart 10). Second, our analysis suggests that an allocation to energy will help mitigate losses in the event of a renewed flaring of US/Iranian tensions that removes oil supply from the market. Bottom Line: We recommend that investors initiate TIPS breakeven curve flatteners (or CPI swap curve flatteners) and add exposure to the high-yield energy sector. Both positions look attractive on their own terms, but will also help hedge the risk of an oil supply disruption if US/Iranian tensions flare back up in the months ahead. Ryan Swift US Bond Strategist rswift@bcaresearch.com Footnotes 1 The others are: the output gap, the US dollar and sentiment. For more details please see US Bond Strategy Weekly Report, “Bond Kitchen”, dated April 9, 2019, available at usbs.bcaresearch.com 2 The Markit index is used in the construction of the Global PMI shown in Chart 2, 3 For more details on the politics behind the US/Iran conflict please see Geopolitical Strategy Special Alert, “A Reprieve Amid The Bull Market In Iran Tensions”, dated January 8, 2020, available at gps.bcaresearch.com 4 Please see US Bond Strategy Special Report, “2020 Key Views: US Fixed Income”, dated December 10, 2019, available at usbs.bcaresearch.com 5 Please see Global Investment Strategy Weekly Report, “Elizabeth Warren And The Markets”, dated September 13, 2019, available at gis.bcaresearch.com 6 In the TIPS market, an example of a breakeven curve flattener would be to buy 2-year TIPS and short the 2-year nominal Treasury note, while also buying the 10-year nominal Treasury note and shorting the 10-year TIPS. 7 https://www.newyorkfed.org/research/policy/oil_price_dynamics_report 8 Please see US Bond Strategy Weekly Report, “Position For Modest Curve Steepening”, dated October 29, 2019, available at usbs.bcaresearch.com Fixed Income Sector Performance Recommended Portfolio Specification

Highlights Global Investment Strategy View Matrix

Time For A Breather

Time For A Breather

Receding trade tensions; diminished risks of a hard Brexit; reduced odds of a victory for Elizabeth Warren in the US presidential elections; liquidity injections by most major central banks; and improved sentiment about the state of the global economy all helped push stocks higher late last year. Some clouds have formed over the outlook since the start of the year, however. The December US ISM manufacturing index fell to the lowest level since 2009, while the PMIs in the euro area, UK, and Japan gave up some of their November gains. The conflict between the US and Iran also flared up. Although tensions have abated in recent days, BCA’s geopolitical strategists worry that the détente may not last. The US is seeking to shift its military focus towards East Asia in order to counter China’s ascendency. They argue that this could create a dangerous power vacuum in the Middle East. Stock market sentiment is quite bullish at the moment, which makes equities more vulnerable to any disappointing news. While we are maintaining our positive 12-month view on global equities and high-yield credit in anticipation that global growth will rebound convincingly later this year, we are downgrading our tactical 3-month view to neutral. Ho Ho Ho After handing investors a sack of coal last Christmas, Santa was back to his true self this past holiday season. Global equities rose 3.4% in December, finishing the year off with a stellar fourth quarter which saw the MSCI All-Country World index surge by 8.6%. Five forces helped push stocks higher: 1) Receding trade tensions; 2) Diminished risks of a hard Brexit; 3) Reduced odds of a victory for Elizabeth Warren in the US presidential elections; 4) Liquidity injections by the Fed, ECB, and the People’s Bank of China; and arguably most importantly 5) Improved sentiment about the state of the global economy. Tarrified No More Trade tensions subsided sharply after China and the US reached a “Phase One” agreement. The deal prevented tariffs from rising on December 15th on $160 billion of Chinese imports. It also rolls back the tariff rate from 15% to 7.5% on about $120 billion in imports that have been subject to levies since September (Chart 1). Chart 1The Evolution Of The US-China Trade War

The Evolution Of The US-China Trade War

The Evolution Of The US-China Trade War

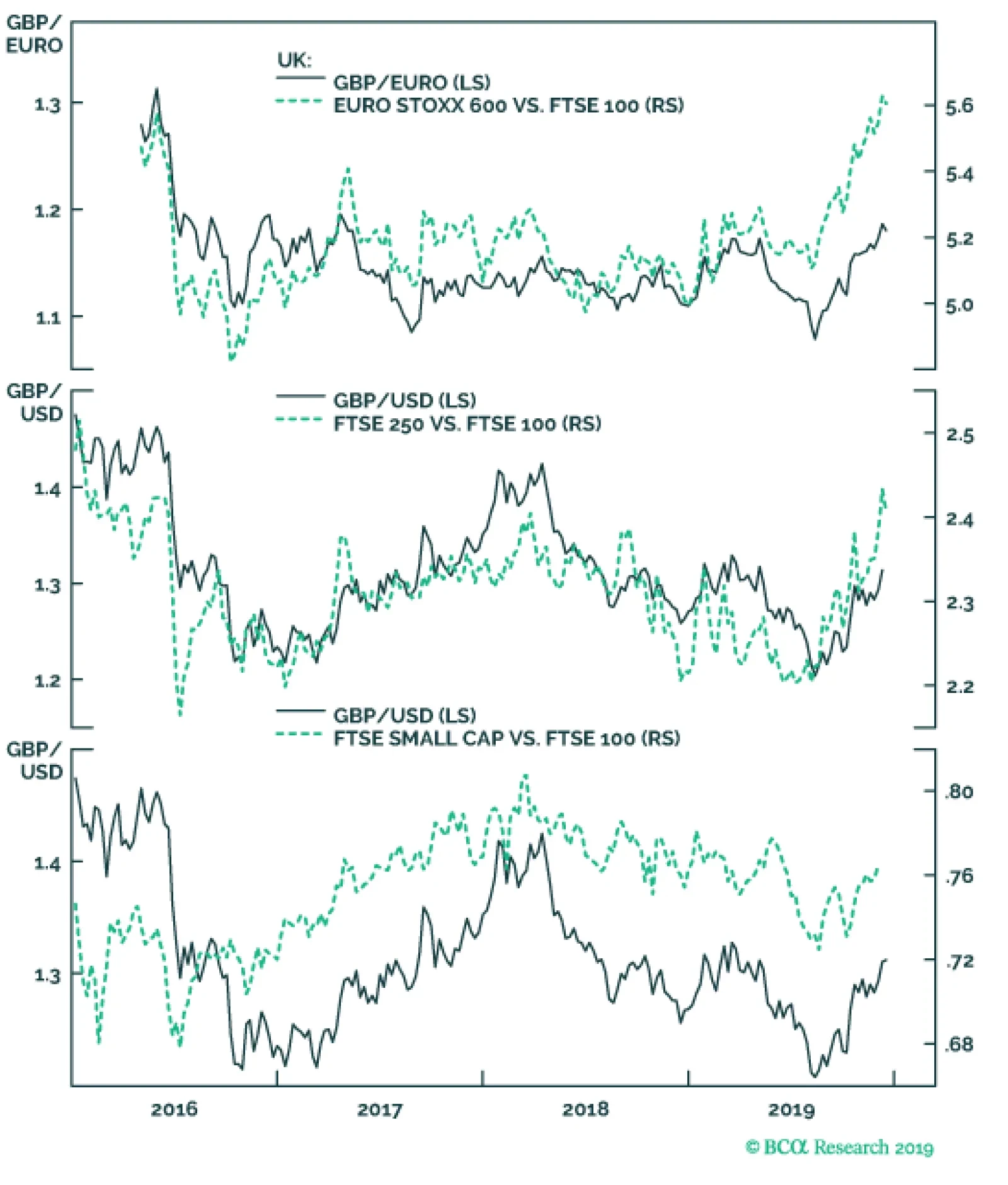

In addition, the Trump Administration allowed the November 13th deadline on European auto tariffs to lapse. This suggests that the US is unlikely to impose tariffs under the Section 232 investigation of auto imports. The auto sector has been at the forefront of the global manufacturing slowdown, so any good news for that industry is welcome. To top it all off, the US House of Representatives ratified the USMCA, the successor to NAFTA, on December 19th. We expect it to be signed into law in the first quarter of this year. Brexit Risks Fading... Chart 2The Majority Of British Voters Aren't Keen On Brexit

The Majority Of British Voters Aren't Keen On Brexit

The Majority Of British Voters Aren't Keen On Brexit

Boris Johnson’s commanding victory in the UK elections has given him the votes necessary to push a withdrawal bill through parliament by the end of the month. The British government will then seek to negotiate a free trade agreement by the end of the year. A “no-deal” Brexit is unacceptable to the majority of British voters (Chart 2). As such, the Johnson government will have no choice but to strike a deal with the EU. ... While Trump Gains On the other side of the Atlantic, President Trump’s re-election prospects improved late last year despite (and perhaps because of) the ongoing impeachment process. There is an uncanny correlation between the probability that betting markets assign to a Trump victory and the value of the S&P 500 (Chart 3). Chart 3An Uncanny Correlation

An Uncanny Correlation

An Uncanny Correlation

Chart 4Who Will Win The 2020 Democratic Nomination?

Time For A Breather

Time For A Breather

It certainly has not hurt market sentiment that Elizabeth Warren’s poll numbers have been dropping recently (Chart 4). Warren’s best hope was to squeeze out Bernie Sanders as soon as possible, thereby leaving the far-left populist lane all to herself. That dream appears to have been dashed, which suggests that even if Trump loses, a centrist like Joe Biden could emerge as president. An Uneasy Truce It remains to be seen how President Trump’s decision to assassinate General Qassem Soleimani, a top Iranian commander, will affect the election outcome. A YouGov/HuffPost poll taken over the weekend revealed that 43% of Americans approved of the airstrike against Soleimani compared to 38% that disapproved.1 History suggests that the public’s patience for war will quickly wear thin if it results in American casualties or significantly higher gasoline prices. Neither side has an incentive to allow the conflict to spiral out of control. Foreign minister Mohammad Javad Zarif tweeted on Tuesday shortly after Iran lobbed missiles at two US military bases that Iran had “concluded” its retaliatory strike, adding that “We do not seek escalation or war.” Despite claims on Iranian public television that 80 “American terrorists” were killed in the attacks, no US troops were harmed. This suggests that the Iranians may be putting on a show for domestic consumption. The US economy is less vulnerable to spikes in oil prices than in the past. Nevertheless, plenty of things could still go wrong. BCA’s geopolitical team, led by Matt Gertken, has argued that the US is seeking to shift its military focus towards East Asia in order to counter China’s ascendency. This could create a dangerous power vacuum in the Middle East. There is also a risk that President Trump overplays his hand. Contrary to the President’s claims, Soleimani was quite popular in Iran (Chart 5). If Trump begins to mock the Iranian leadership’s feeble response, Iran will have no choice but to take more aggressive action. Chart 5Soleimani Was More Popular In Iran Than Trump Claims

Time For A Breather

Time For A Breather

Chart 6US Economy Is Less Vulnerable To Spikes In Oil Prices Than In The Past

US Economy Is Less Vulnerable To Spikes In Oil Prices Than In The Past

US Economy Is Less Vulnerable To Spikes In Oil Prices Than In The Past

One thing that could embolden Trump is that the US economy is less vulnerable to spikes in oil prices than in the past. US oil output reached as high as 12.9 mm b/d in 2019, allowing the country to become a net exporter of oil for the first time in history (Chart 6). Any increase in oil prices would incentivize further domestic production, which would help bring prices back down. The US economy has also become less energy intensive – it takes less than half as much oil to produce a unit of GDP today than it did in the early 1980s. Finally, unlike in the past, the Fed will not need to raise rates in response to higher oil prices due to the fact that inflation expectations are currently well anchored. In fact, as we discuss below, we expect the Fed and other central banks to continue to provide a tailwind for growth over the course of 2020. The Fed’s “It’s Not QE” QE Program The jump in overnight lending rates in mid-September torpedoed the Federal Reserve’s efforts to shrink its balance sheet. Thanks to a steady stream of Treasury bill purchases since then, the Fed’s asset holdings have swelled by over $400 billion, reversing more than half of the decline observed since early 2018 (Chart 7). Chart 7Fed's Asset Holdings Are Growing Anew

Fed's Asset Holdings Are Growing Anew

Fed's Asset Holdings Are Growing Anew

Chart 8The Fed's Balance-Sheet Expansion Helped Fuel The Dot-Com Bubble

The Fed's Balance-Sheet Expansion Helped Fuel The Dot-Com Bubble

The Fed's Balance-Sheet Expansion Helped Fuel The Dot-Com Bubble

The Fed has insisted that its latest intervention does not amount to a new QE program, stressing that it is buying short-term securities rather than long-dated bonds. In so doing, it is simply creating bank reserves, rather than seeking to suppress the term premium by altering the maturity structure of the private sector’s holdings of government debt. Nevertheless, even such straightforward interventions have proven to be powerful signaling tools. By growing its balance sheet, a central bank is implicitly promising to keep monetary policy very accommodative. It is worth remembering that the run-up in the NASDAQ in 1999 coincided with a significant balance-sheet expansion by the Fed in response to Y2K fears, which came on the heels of three “insurance cuts” in 1998 (Chart 8). Gentle Jay Paves The Way Chart 9Inflation Expectations Remain Muted

Inflation Expectations Remain Muted

Inflation Expectations Remain Muted

In 2000, the Fed moved quickly to reverse the liquidity injection it had orchestrated the prior year. We do not expect such a reversal anytime soon. Moreover, unlike in 2000, when the Federal Reserve kept raising rates – ultimately bringing the Fed funds rate up to 6.5% in May 2000 – the Fed is likely to stay on hold this year. The Fed’s ongoing strategic policy review is poised to move the central bank even closer towards explicitly adopting an average inflation target of 2% over the course of a business cycle. Since inflation tends to fall during recessions, this implies that the Fed will seek to target an inflation rate somewhat higher than 2% during expansions. Realized core PCE inflation has averaged only 1.6% since the recession ended. Both market-based and survey-based measures of long-term inflation expectations remain downbeat (Chart 9). This suggests that the bar for raising rates this year is quite high. More Monetary Easing In The Euro Area And China Chart 10Chinese Monetary Easing Should Help Global Growth Bottom Out

Chinese Monetary Easing Should Help Global Growth Bottom Out

Chinese Monetary Easing Should Help Global Growth Bottom Out

The ECB resumed its QE program in November after a 10-month hiatus. While the current pace of €20 billion in monthly asset purchases is well below the prior pace of €80 billion, the central bank did say it would continue buying assets for “as long as necessary” to bring inflation up to its target. The language harkens back to Mario Draghi’s 2012 “whatever it takes” pledge, this time applied to the ECB’s inflation mandate. Not to be outdone, the People’s Bank of China cut the reserve requirement ratio by 50 basis points last week, a move that will release RMB 800 billion ($US 115 billion) of fresh liquidity into the banking system. Historically, cuts in reserve requirements have led to faster credit growth and ultimately, to stronger economic growth both in China and abroad (Chart 10). The PBOC has also instructed lenders to adopt the Loan Prime Rate (LPR) as the new benchmark lending rate. The LPR currently sits 20bps below the old benchmark rate (Chart 11). Hence, the PBOC’s order amounts to a stealth rate cut. Our China strategists expect further reductions in the LPR over the next six months. In addition, the crackdown on shadow bank lending seems to be subsiding, which bodes well for overall credit growth later this year (Chart 12). Chart 11China: Stealth Monetary Easing

China: Stealth Monetary Easing

China: Stealth Monetary Easing

Chart 12Crackdown On Shadow Banking In China Is Easing

Crackdown On Shadow Banking In China Is Easing

Crackdown On Shadow Banking In China Is Easing

Rising Economic Confidence Chart 13Recession Fears Amongst Economists Began To Gather Steam At The Start Of Last Year

Recession Fears Amongst Economists Began To Gather Steam At The Start Of Last Year

Recession Fears Amongst Economists Began To Gather Steam At The Start Of Last Year

Chart 14The Wider Public Was Also Worried About A Downturn

The Wider Public Was Also Worried About A Downturn

The Wider Public Was Also Worried About A Downturn

At the start of 2019, nearly half of US CFOs thought the economy would be in a recession by the end of the year. Similarly, two-thirds of European CFOs and four-fifths of Canadian CFOs expected their respective economies to succumb to recession. Professional economists were equally dire (Chart 13). Households also became increasingly worried about a downturn. Google searches for “recession” spiked to near 2009-highs last summer (Chart 14). The mood has certainly improved since then. According to the latest Duke CFO survey, optimism about the economic outlook has increased. More importantly, CFO optimism about the prospects for their own firms has risen to the highest level in the 18-year history of the survey (Chart 15). Chart 15CFOs Have Become More Optimistic Of Late

CFOs Have Become More Optimistic Of Late

CFOs Have Become More Optimistic Of Late

Show Me The Money Going forward, global growth needs to accelerate in order to validate the improved confidence of CFOs and investors alike. We think that it will, thanks to the lagged effects from the easing in financial conditions in 2019, a turn in the global inventory cycle, a de-escalation in the trade war, easier fiscal policy in the UK and euro area, and re-upped fiscal/credit stimulus in China. For now, however, the economic data remains mixed. On the positive side, household spending is still robust across most of the world, a fact that has been reflected in the resilience of service-sector PMIs (Chart 16). Chart 16AThe Service Sector Has Remained Resilient (I)

The Service Sector Has Remained Resilient (I)

The Service Sector Has Remained Resilient (I)

Chart 16BThe Service Sector Has Remained Resilient (II)

The Service Sector Has Remained Resilient (II)

The Service Sector Has Remained Resilient (II)

Chart 17US Wage Growth Has Picked Up, Especially At The Bottom Of The Income Distribution

Time For A Breather

Time For A Breather

Chart 18US Housing Backdrop Is Solid

US Housing Backdrop Is Solid

US Housing Backdrop Is Solid

The US consumer, in particular, is showing little signs of fatigue. The Atlanta Fed GDPNow estimates that real personal consumption grew by 2.4% in the fourth quarter, having increased at an average annualized pace of 3% in the first three quarters of 2019. Both a strong labor market and housing market have buoyed US consumption. Payrolls have risen by an average of 200K per month for the past six months, double what is necessary to keep up with labor force growth. This week’s strong ADP release – which featured a 29K jump in jobs in goods-producing industries in December, the best since April – suggests that today’s jobs report will remain healthy. In addition, wage growth has picked up, particularly at the bottom of the income distribution (Chart 17). Residential construction has also been strong. Homebuilder sentiment reached the best level since June 1999 (Chart 18). Global Manufacturing: Too Early To Call The All-Clear The outlook for manufacturing remains the biggest question mark in the global economy. The US ISM manufacturing index dropped to 47.2 in December, its lowest level since June 2009. The composition of the report was poor, with the new orders-to-inventory ratio dropping close to recent lows. Chart 19Other US Manufacturing Gauges Are Not As Weak As The ISM

Other US Manufacturing Gauges Are Not As Weak As The ISM

Other US Manufacturing Gauges Are Not As Weak As The ISM

We would discount the ISM report to some extent. The regional Fed manufacturing indices have not been nearly as disappointing as the ISM (Chart 19). The Markit PMI, which tracks US manufacturing activity better than the ISM, clocked in at a respectable 52.4 in December, down only slightly from November’s reading of 52.6. Nevertheless, it is hard to be excited about the near-term outlook for US manufacturing, especially in light of Boeing’s decision to suspend production of the 737 Max temporarily. Most estimates suggest that the production halt will reduce real US GDP growth by 0.3%-to-0.5% in the first quarter. The euro area manufacturing PMI gave up some of its November gains, falling to 46.3 in December. While the index is still above its September low of 45.7, it has been under 50 for 11 straight months now. The UK and Japanese PMI also retreated. Chinese manufacturing has shown clearer signs of bottoming out. Despite dipping in December, the private sector Caixin manufacturing PMI remains near its 2017 highs. The official PMI published by the National Bureau of Statistics is less upbeat, but still managed to come in slightly above 50 in December. The production subcomponent reached the highest level since August 2018. Reflecting the positive trend in the Chinese economy, Korean exports to China rose by 3.3% in December, the first positive growth rate in 14 months (Chart 20). Taiwan’s exports have also rebounded. The manufacturing PMI rose above 50 in both economies in December. In Taiwan’s case, this was the first time the PMI moved into expansionary territory since September 2018. On balance, we continue to expect global manufacturing to recover in 2020. This is in line with our observation that global manufacturing cycles typically last three years, with 18 months of weaker growth followed by 18 months of stronger growth (Chart 21). That said, the weakness in European and US manufacturing (at least judged by the ISM) is likely to give investors pause. Chart 20Some Positive Signs Emerging From Korea And Taiwan

Time For A Breather

Time For A Breather

Chart 21A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

A Fairly Regular Three-Year Manufacturing Cycle

Investment Conclusions We turned bullish on stocks in late 2018, having temporarily moved to the sidelines during the summer of that year. Global equities have gained 25% since our upgrade. We see another 10% of upside for 2020, led by European and EM bourses. Despite its recent gains, the real value of the MSCI All-Country World Index is only 3% above its prior peak in January 2018. The 12-month forward PE ratio of 16.3 is still somewhat lower than it was back then. The valuation picture is even more enticing if we compare equity earnings yields with bond yields, which is tantamount to computing a rough equity risk premium (ERP). The global ERP remains quite high by historic standards, especially outside the US where earnings yields are higher and bond yields are generally lower (Chart 22). Chart 22The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

The Equity Risk Premium Is Fairly High, Especially Outside The US

Chart 23Stock Market Sentiment Is Quite Bullish

Stock Market Sentiment Is Quite Bullish

Stock Market Sentiment Is Quite Bullish

Nevertheless, sentiment is quite positive towards stocks at the moment (Chart 23). Elevated bullish sentiment, against the backdrop of ongoing uncertainty about the outlook for global manufacturing and an uneasy truce between the US and Iran, poses a near-term headwind to risk assets. As such, while we are maintaining our positive 12-month view on global equities and high-yield credit, we are downgrading our tactical 3-month view to neutral for the time being. We do not regard this as a major realignment of our views; we will turn tactically bullish again if stocks dip about 5% from current levels. Peter Berezin Chief Global Strategist peterb@bcaresearch.com Footnotes 1 Ariel Edwards-Levy, “Here's What Americans Think About Trump's Iran Policy,” TheHuffingtonPost.com (January 6, 2020). MacroQuant Model And Current Subjective Scores

Time For A Breather

Time For A Breather

Strategic Recommendations Closed Trades

Highlights The US and Iran are not rushing into a full-scale war for the moment – and yet the bull market in US-Iran tensions will continue for at least the next 2-3 years (Chart 1). This means that while global risk assets can take a breather from Iran geopolitical risk – if not other risks to the heady rally – the breather is not a fundamental resolution and Iran will remain market-relevant in 2020. A Reprieve … Chart 1Bull Market In US-Iran Tensions

Bull Market In US-Iran Tensions

Bull Market In US-Iran Tensions

On January 8 President Donald Trump spoke at the White House in response to a barrage of missiles fired by the Iranian Revolutionary Guards Corps (IRGC) at bases with US troops in al-Asad and Erbil, Iraq. Trump remarked that Iran “appears to be standing down,” judging by the fact that the missile strikes did not kill American citizens – Trump’s explicit red line – or cause any significant casualties or damage. Iran’s Foreign Minister Javad Zarif claimed that Iran’s strikes “concluded proportionate measures” in response to the US killing of Quds Force chief Qassem Soleimani in Baghdad on January 3, which itself followed unrest at the US embassy in Baghdad and American strikes on Iran-backed Iraqi militias (Map 1). Supreme Leader Ayatollah Ali Khamenei gave ambivalent comments, saying military operations were not in themselves sufficient but that Iran must focus on removing the US presence from the region. Map 1US And Iran Sparring Across The Region

A Reprieve Amid The Bull Market In Iran Tensions

A Reprieve Amid The Bull Market In Iran Tensions

President Trump’s speech was transparently a campaign speech, not a war speech. He did not imply in any way that the US military would retaliate to the missile strikes, but said Americans should be “grateful and happy” that Iran did a “good thing” for the world by refraining from drawing American blood. Instead Trump focused on Iran’s nuclear program, denouncing the 2015 nuclear deal with Iran (the Joint Comprehensive Plan of Action or JCPA). He implored the parties of that agreement – the UK, Germany, France, Russia, and China – to join him in negotiating a new deal to replace it. The goal of the new negotiations would be to prevent Iran from ever obtaining a nuclear weapon and to halt its sponsorship of regional militants in exchange for economic development and opening up to the outside world. He called for NATO to take a more active role in the Middle East and he highlighted the US’s shared interest with Iran in combating the Islamic State in Iraq and Syria. The takeaway is that the Trump administration is not pursuing regime change but rather nuclear non-proliferation and a change in Iran’s regional behavior. The administration has often said as much, but the assassination of Soleimani escalated tensions and called into question Trump’s intentions. Financial markets will cheer the successful reestablishment of US deterrence vis-à-vis Iran, as it makes Iran less likely to retaliate to US pressure in ways that lead to a major military confrontation. The near-term risk of a massive oil supply shock will decline. Oil prices have already fallen back to where they stood before Soleimani’s death. … Amid A Bull Market In US-Iran Tensions Yet the saga does not end here. Iran’s ineffectual military strike could have been a feint, or Iran could follow up with more consequential retaliation later. Chart 2US Strategic Deleveraging From The Middle East

US Strategic Deleveraging From The Middle East

US Strategic Deleveraging From The Middle East

Iran has the ability to dial up its nuclear program step by step, sponsor regional attacks with plausible deniability, and foment regional unrest in important oil-producing countries. It can do these things in ways that do not clearly cross America’s red lines but still cause market-relevant tensions or disrupt oil supply. After all, Iran is still under punitive sanctions and desirous of demoralizing the US to hasten its departure from the region. So far Iran has not irreversibly abandoned its nuclear commitments or crossed any red lines regarding levels of uranium enrichment, but we fully expect it to threaten to do so and use its nuclear program to build up negotiating leverage. We doubt any serious US-Iran negotiations will take shape until 2021 at the earliest – and any negotiations could fail and lead to another, more serious round of military exchanges. This means that today’s reprieve may be tomorrow’s negative surprise for the markets. The fundamental basis for this bull market in US-Iran tensions is that the US is seeking to withdraw its strategic commitment to the region to counter China (Chart 2), yet Iran is filling the power vacuum and could conceivably create a regional empire (Map 2). President Trump will not want to appear to have been chased out of Iraq in an election year, even if he is in favor of strategic deleveraging, but Iran may try to do exactly that. Iran will also try to solidify its influence among those left exposed by the US’s deleveraging, namely in Iraq. Map 2Iran's Strategic 'Land Bridge' To The Mediterranean

A Reprieve Amid The Bull Market In Iran Tensions

A Reprieve Amid The Bull Market In Iran Tensions

Chart 3A Succession Crisis Looms

A Succession Crisis Looms

A Succession Crisis Looms