Economy

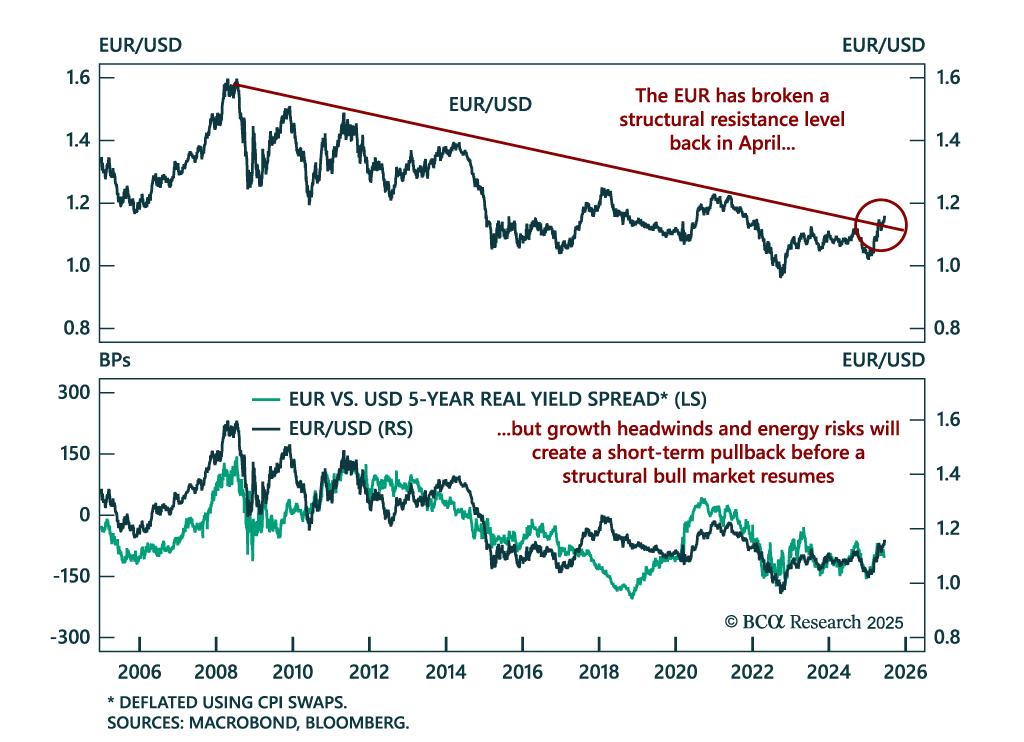

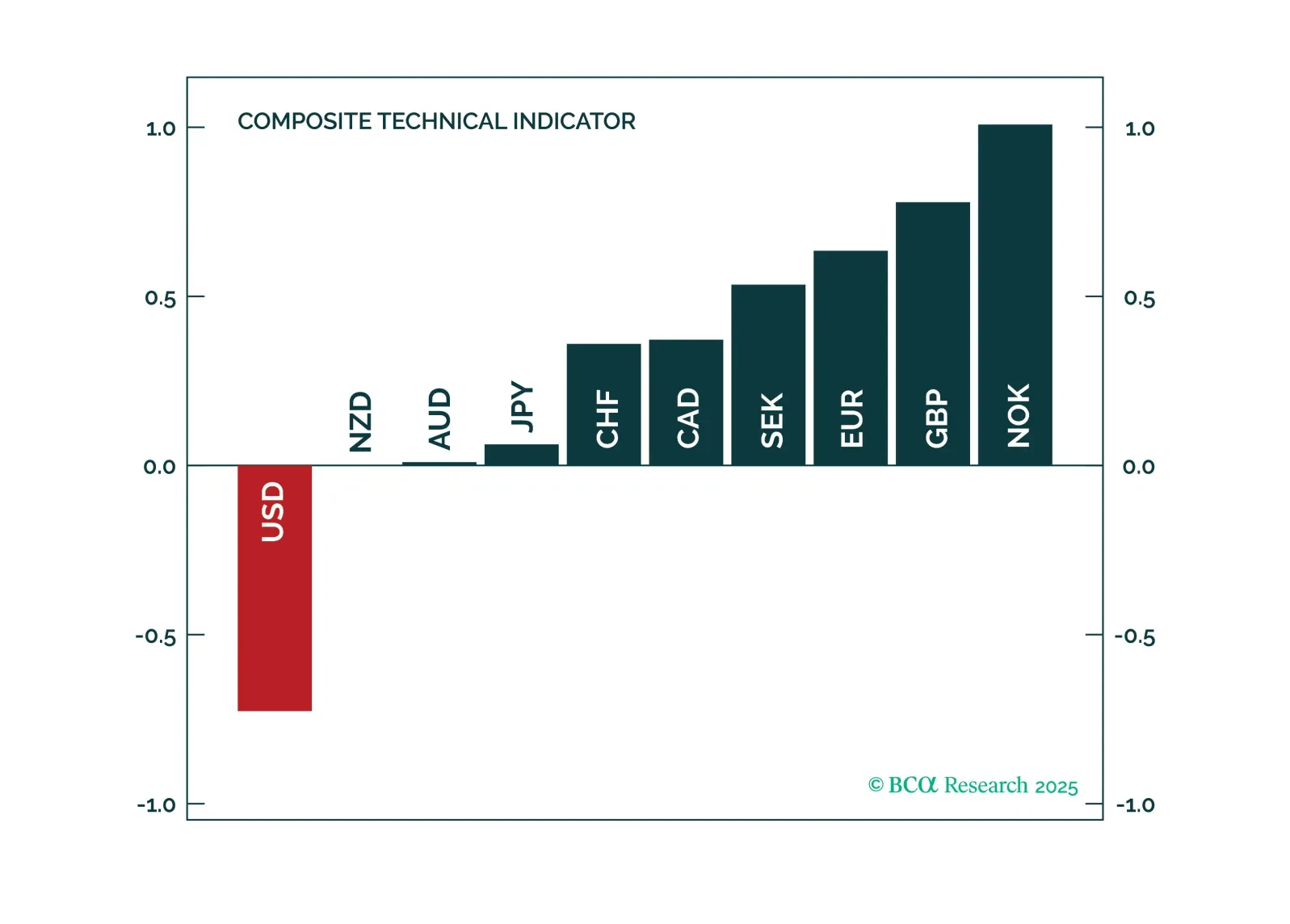

In this FX note, we provide a rationale for why it is important to pay attention to technical indicators, while still keeping your eyeball on the structural factors that drive currencies. This report answers the following questions: 1. Should you buy or sell the USD over a three-to-six month period from the pure lens of our proven technical indicators and 2. What are the best tactical cross trades among currencies.

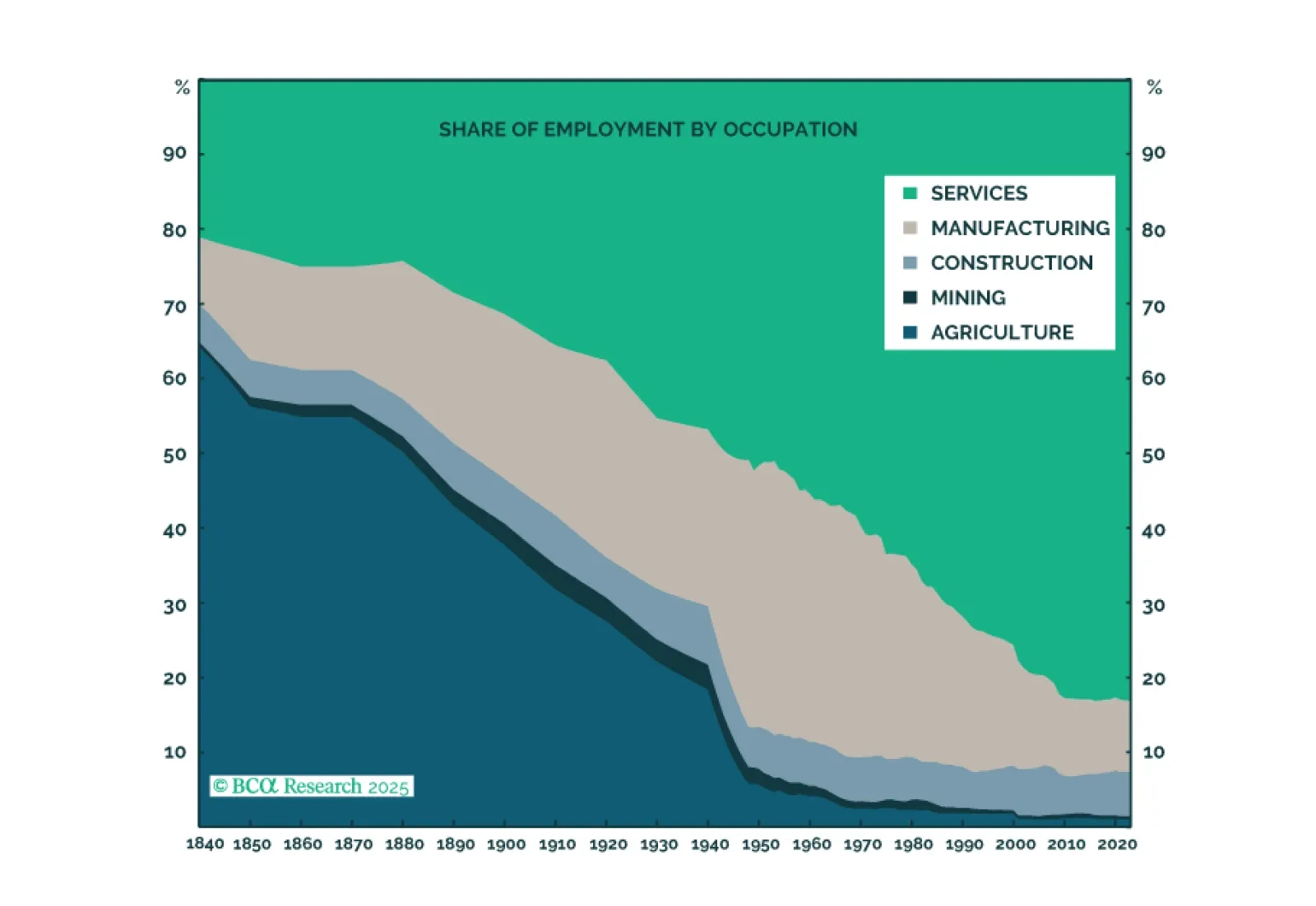

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

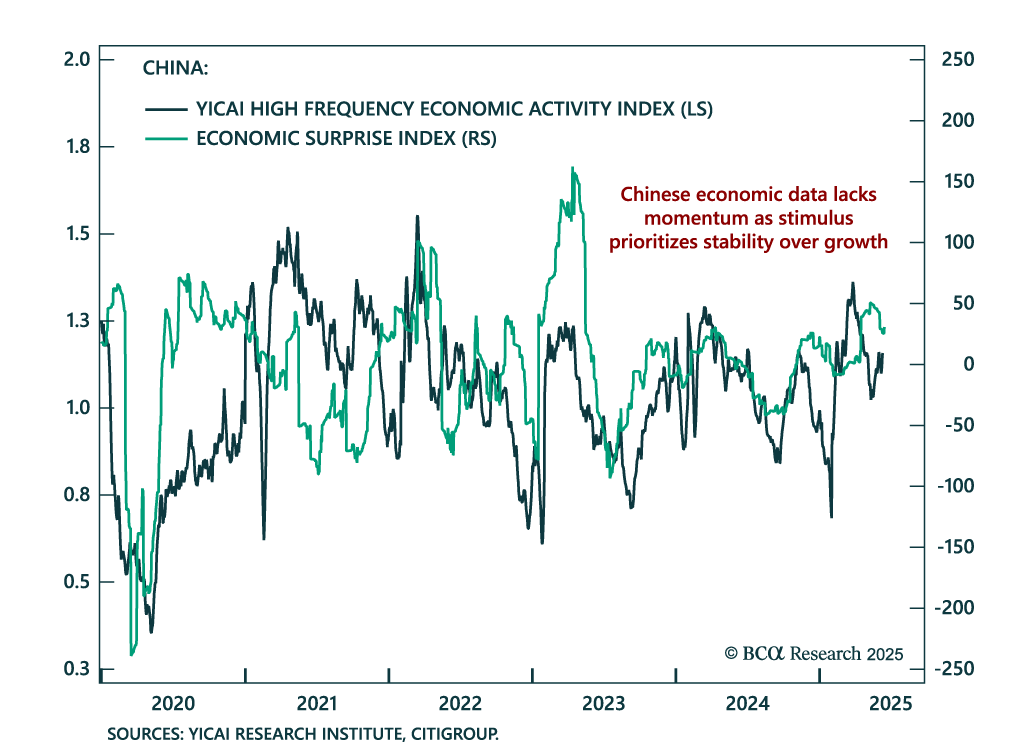

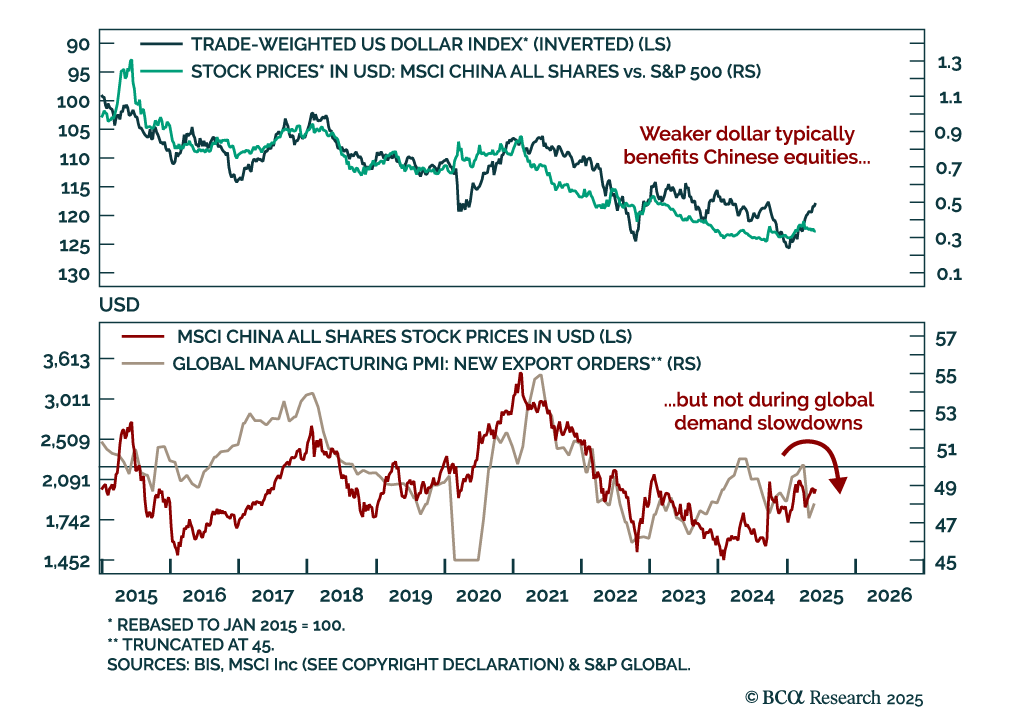

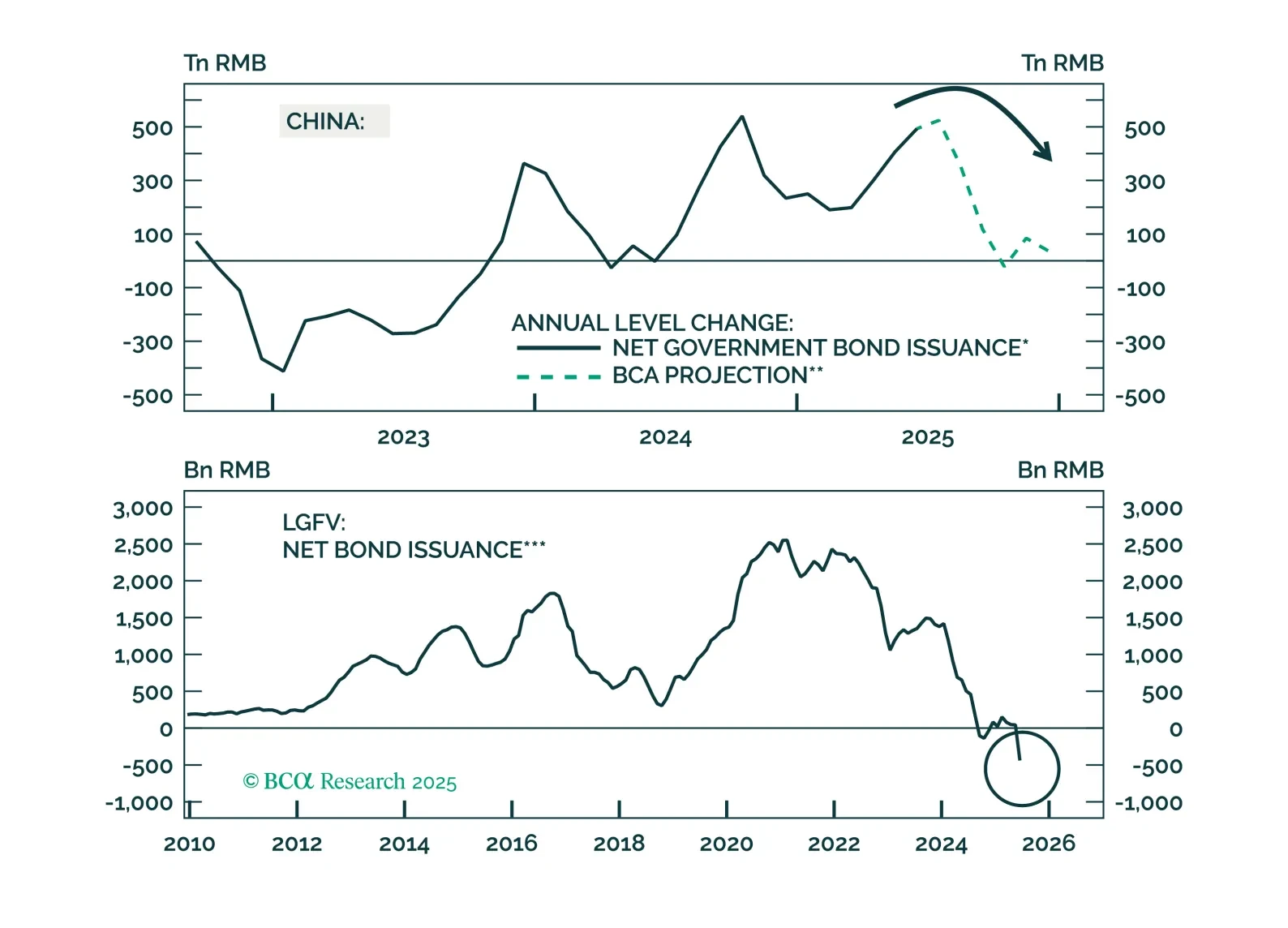

The London Sino-US trade talks offered hope of de-escalation, but Chinese equities remain under pressure from deflationary headwinds and lack a clear macro catalyst to trend higher.