Economy

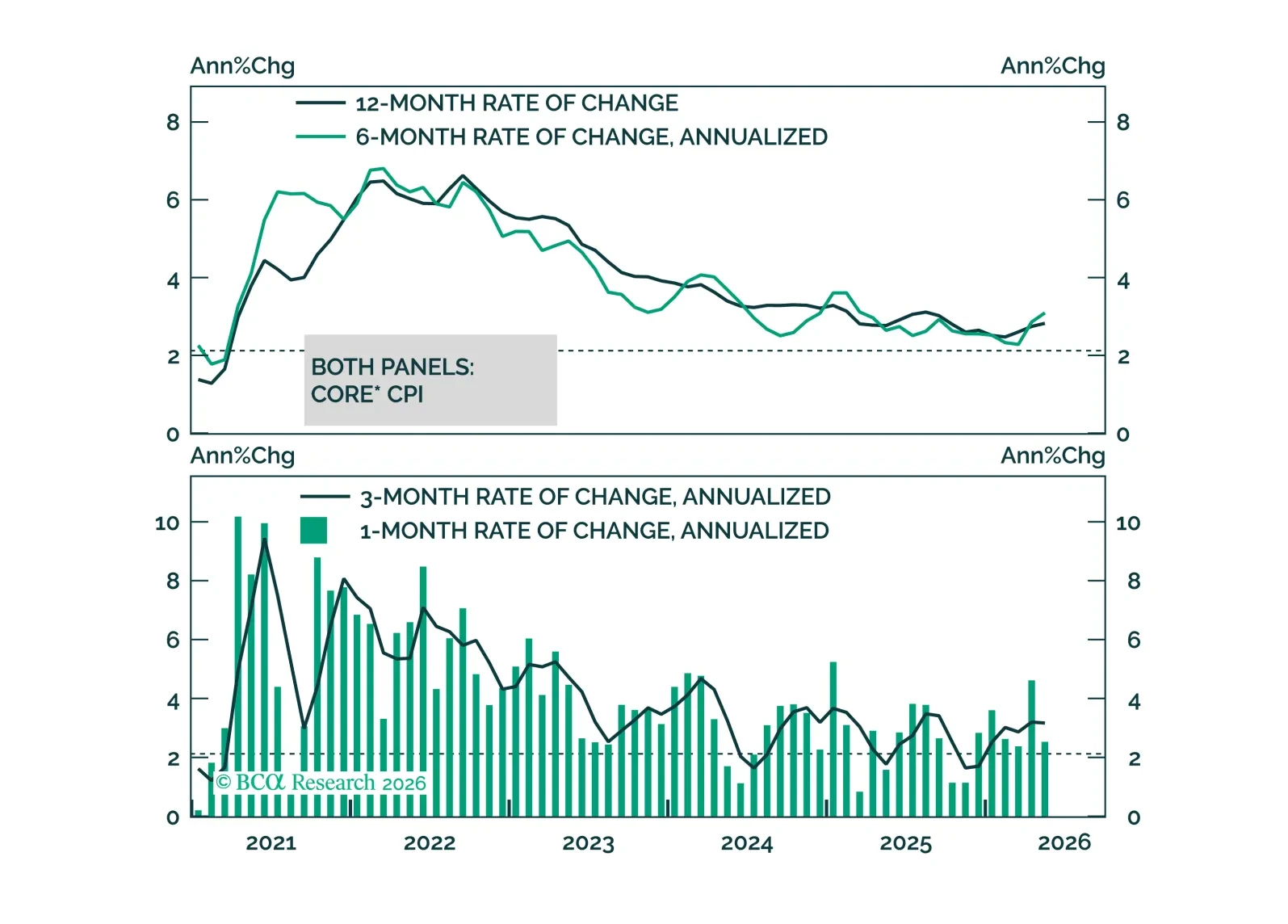

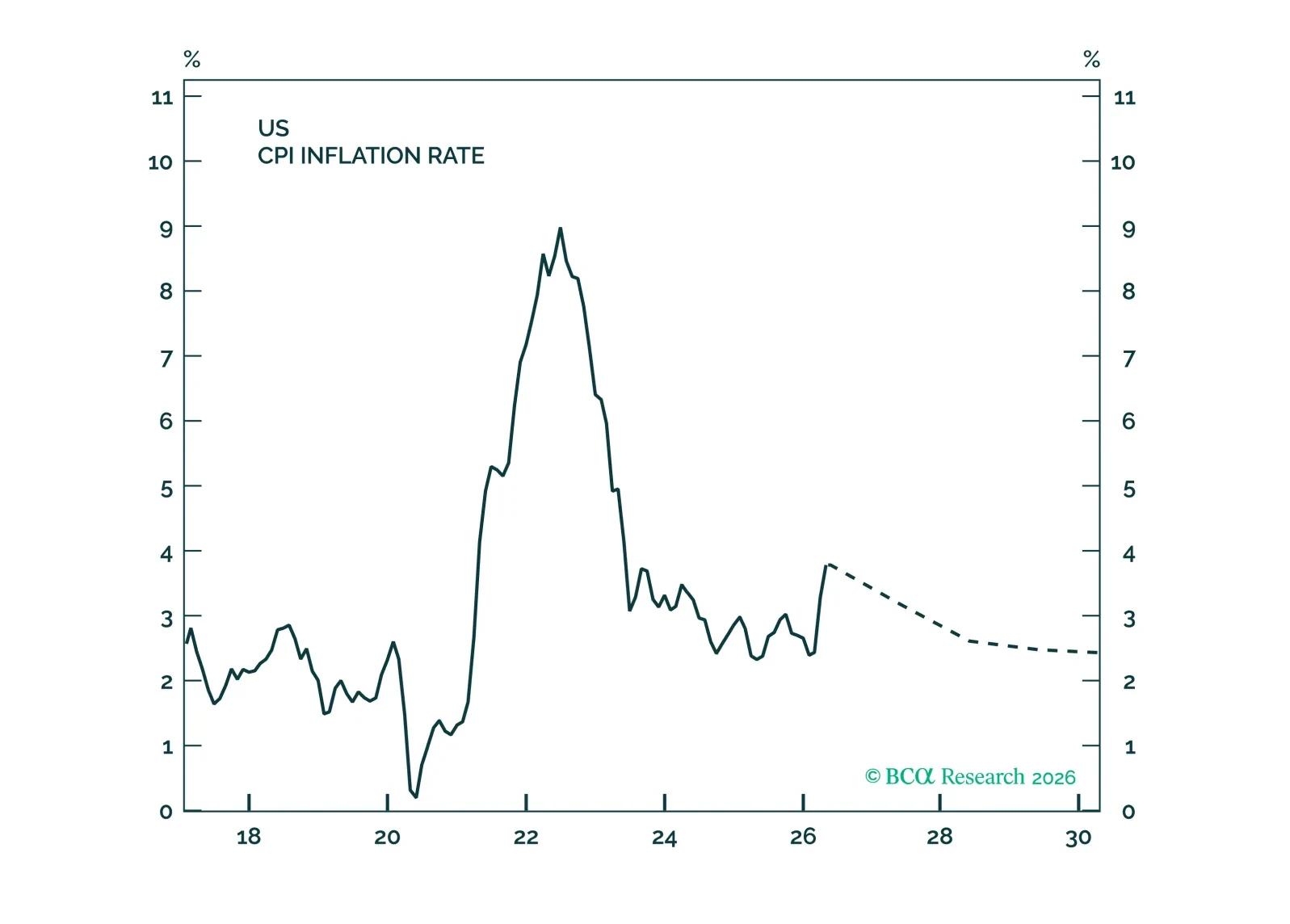

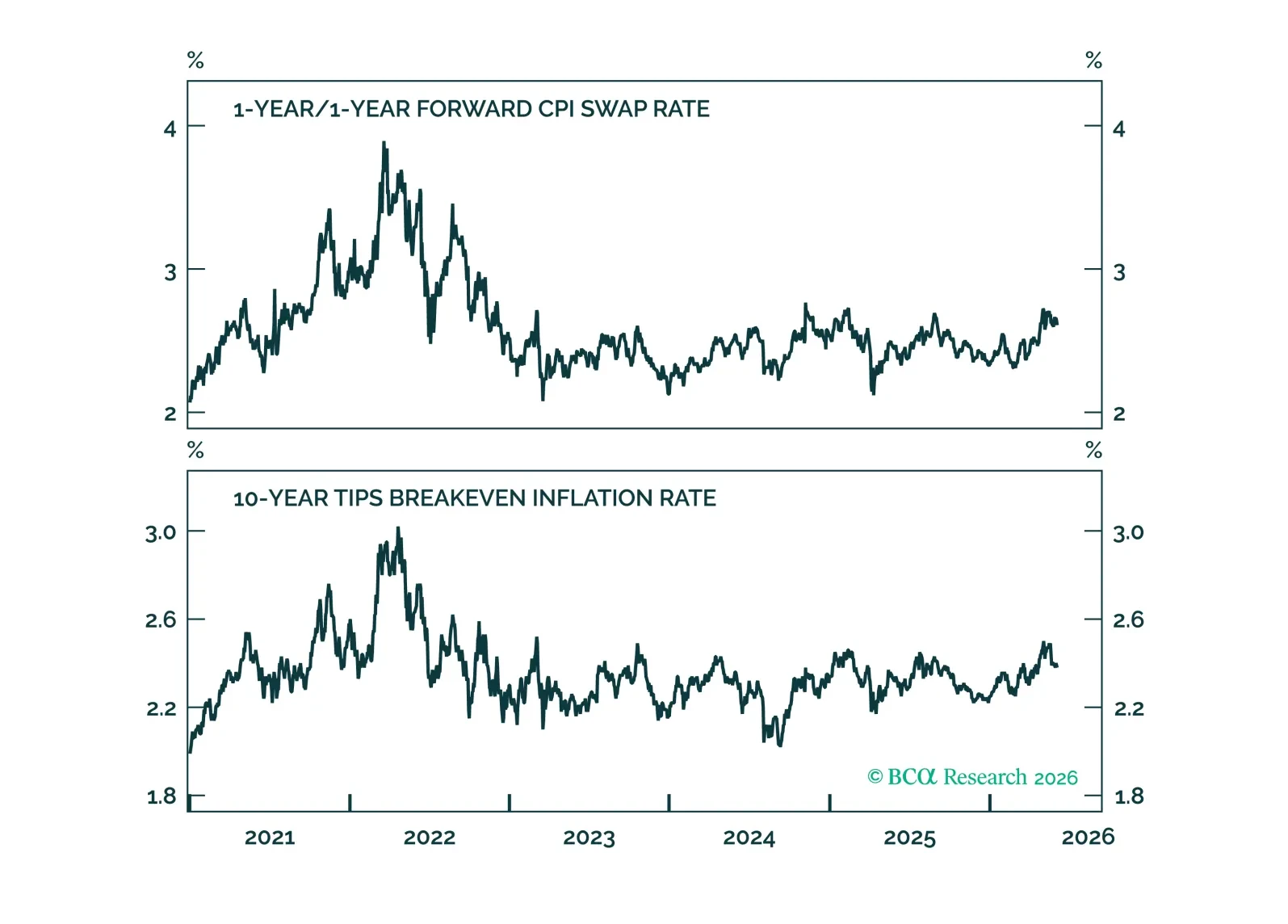

May CPI data show no evidence of passthrough from energy prices to core inflation. This will keep the Fed on hold for the time being.

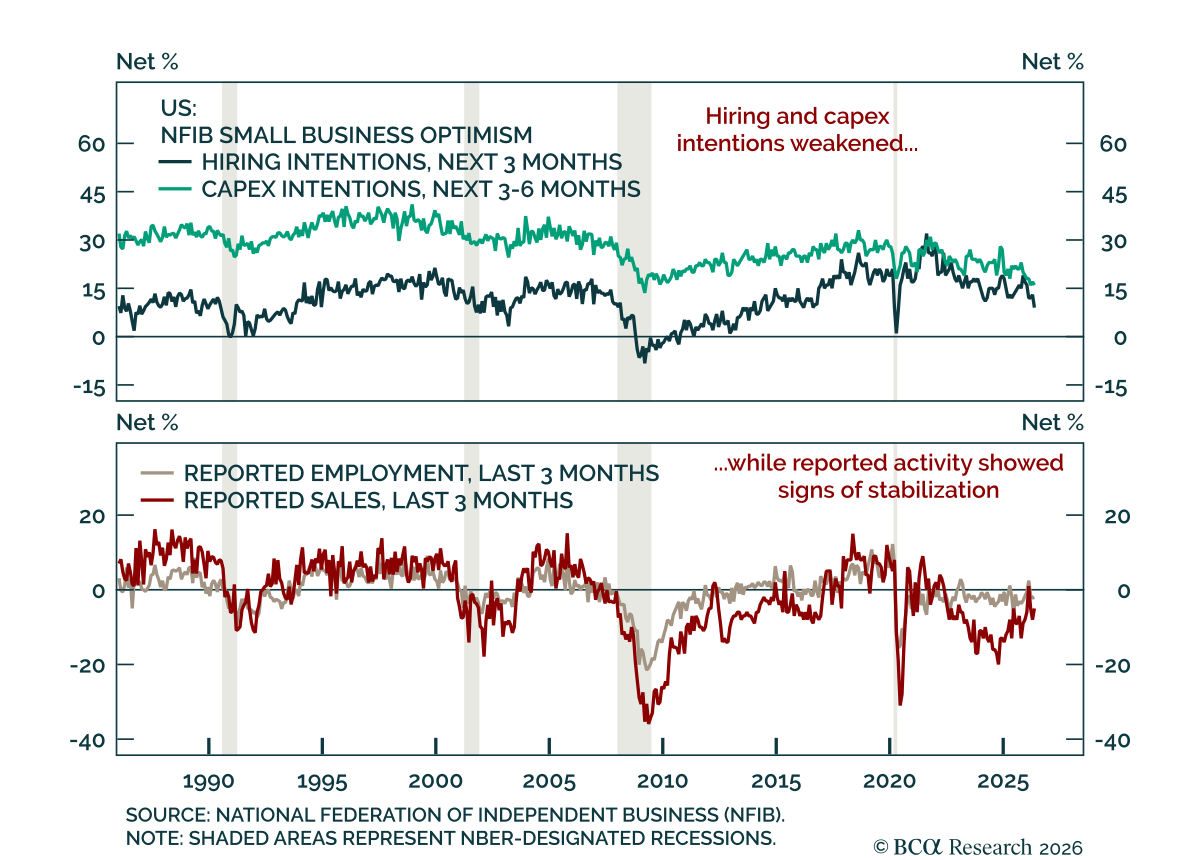

The May NFIB survey missed estimates and pointed to softer small-business conditions, though the signal on the broader labor market remains mixed. The headline index fell to 95.3 from 95.9. The overall picture was soft, with both capex and hiring intentions…

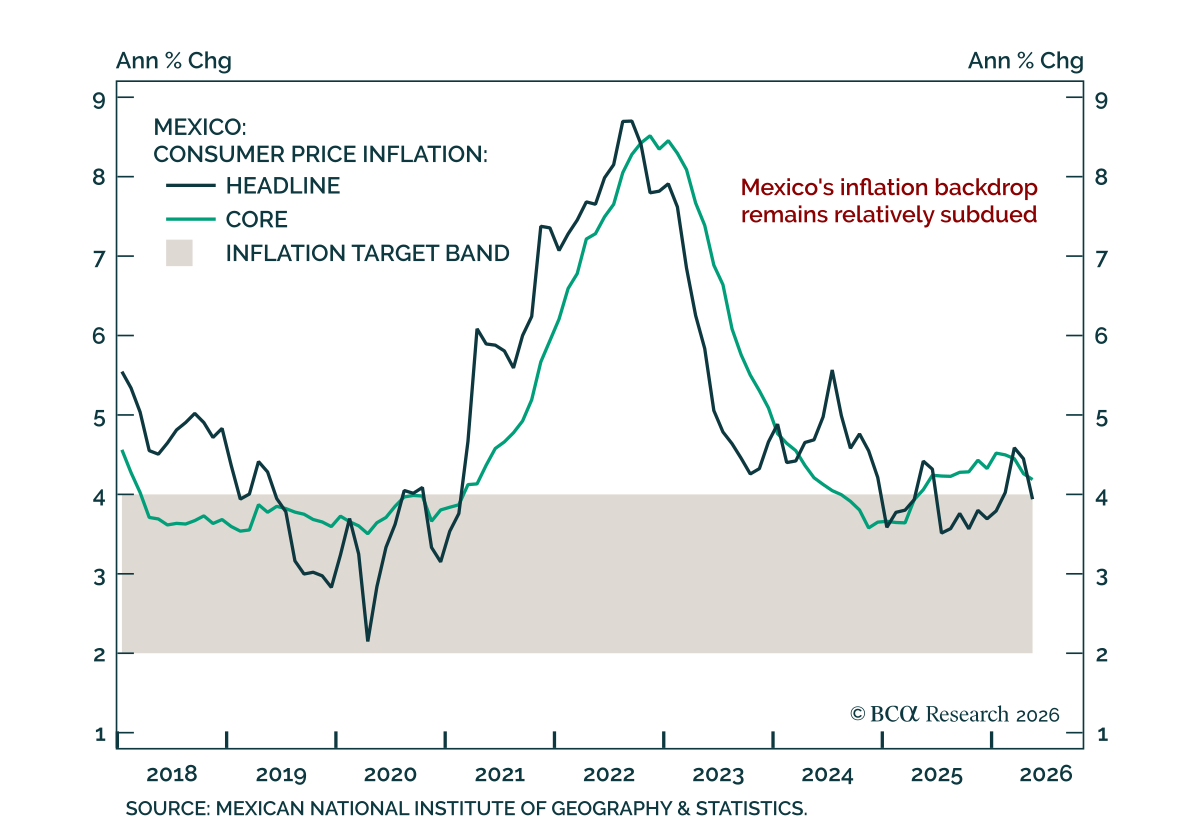

Mexican inflation has eased back to the high end of the target range, but Banxico likely still has room to cut over a cyclical horizon. Some concern around core price pressures remains, and Banxico ended its two-year easing cycle last month. Our Emerging…

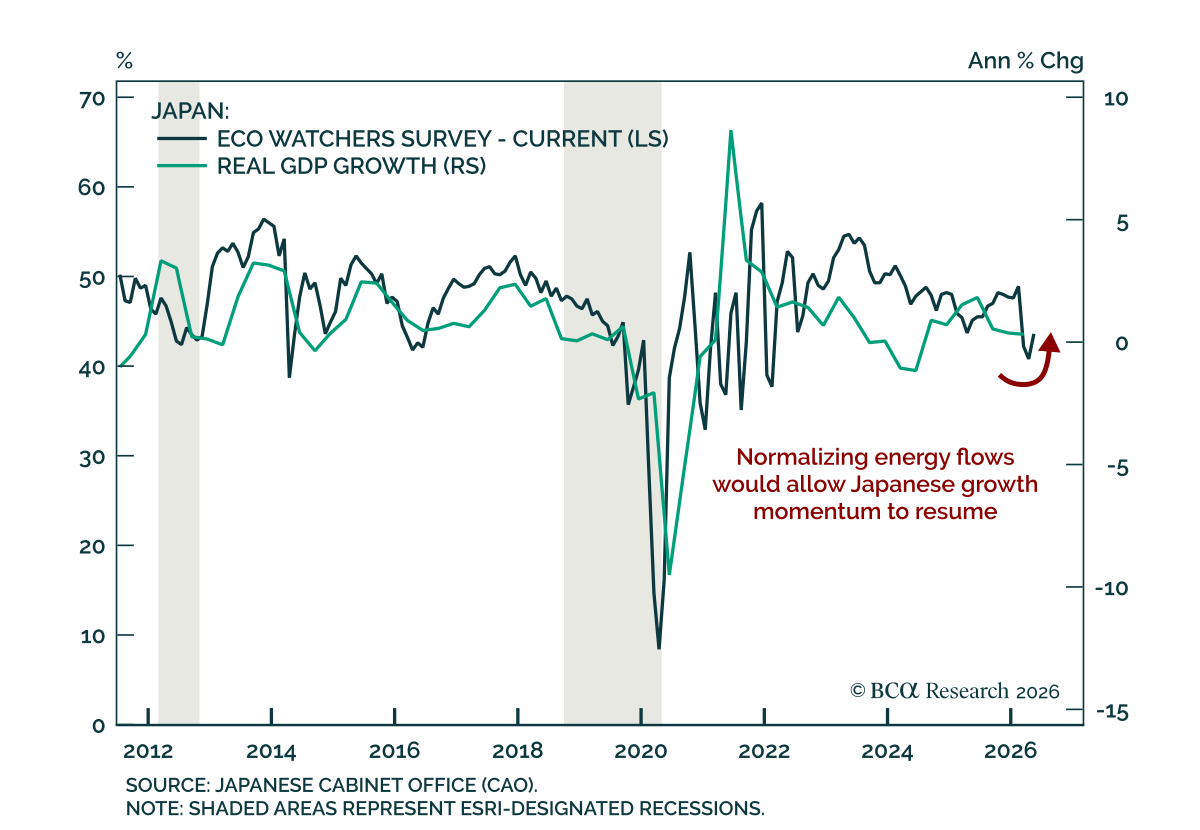

Japan’s May Eco Watchers Survey beat estimates, pointing to resilient growth despite the Middle East conflict. Both the current conditions and outlook indexes rose more than expected, to 43.6 from 40.8 and to 40.7 from 39.4, respectively. Both had plunged in…

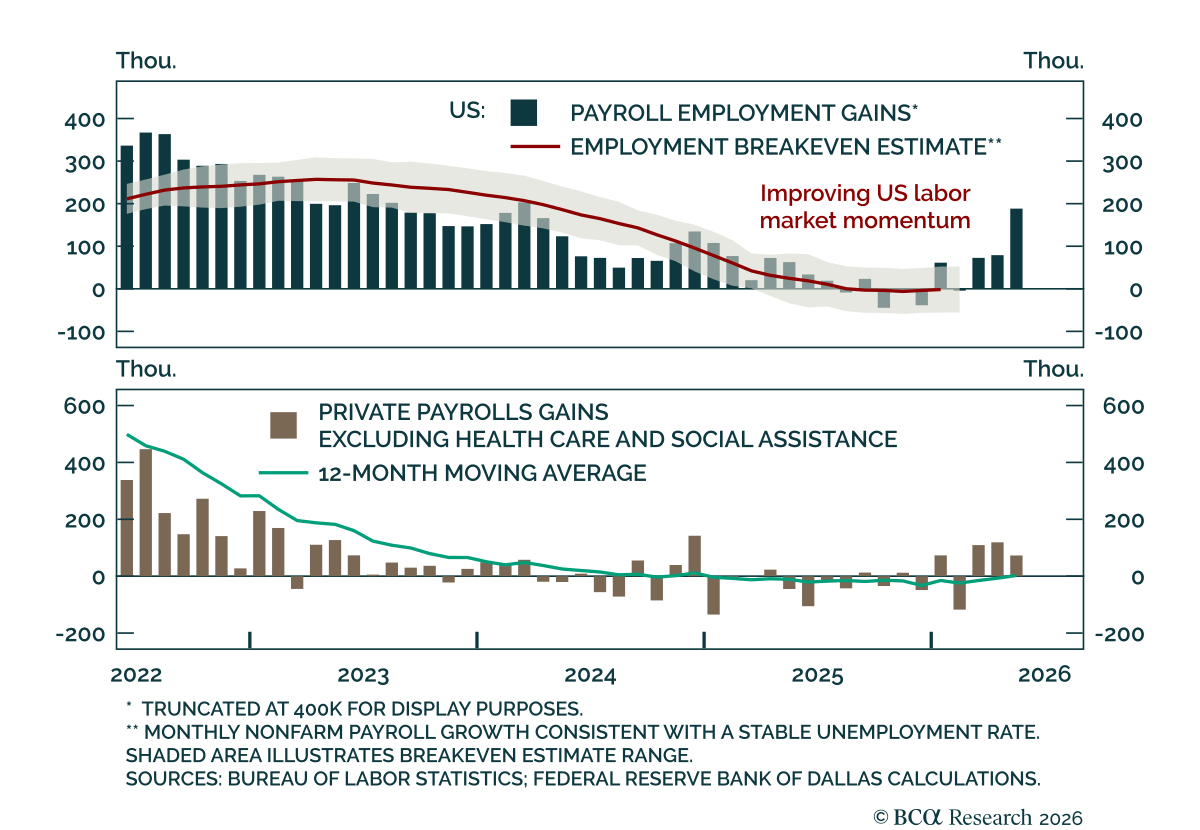

The blowout US payrolls report reinforces improving labor market momentum and upside risks to Fed policy, arguing for continued caution on duration. Non-farm payrolls rose 172k, well-above expectations of 88k, while the prior two months were revised sharply…

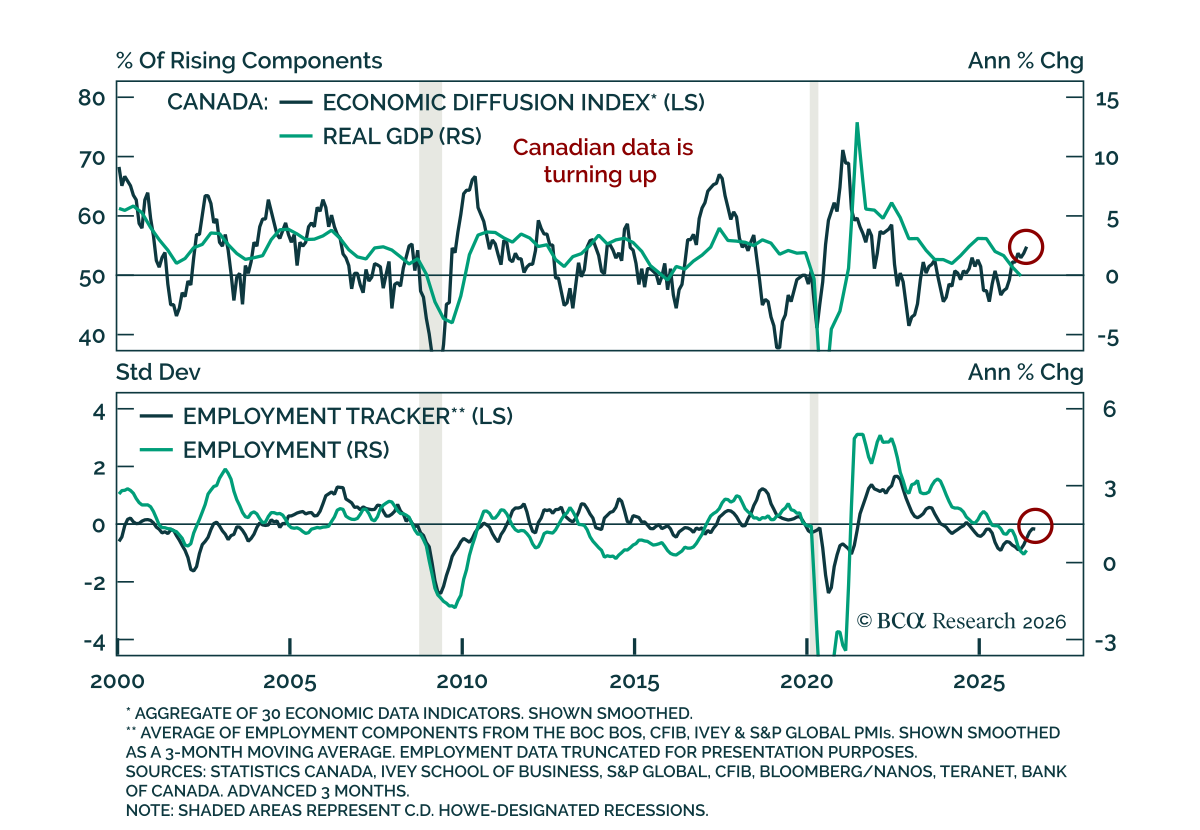

Canada’s labor market is showing early signs of stabilization, but not sufficient for the Bank of Canada to begin raising rates. Employment increased by 88k in May, well above expectations of 10k, led by a jump in full-time employment, while the unemployment…

The AI boom will increase inflation in the near term and could also raise it over the long term. The Fed’s reluctance to hike rates is understandable, but it risks amplifying what may already be a brewing stock market bubble.

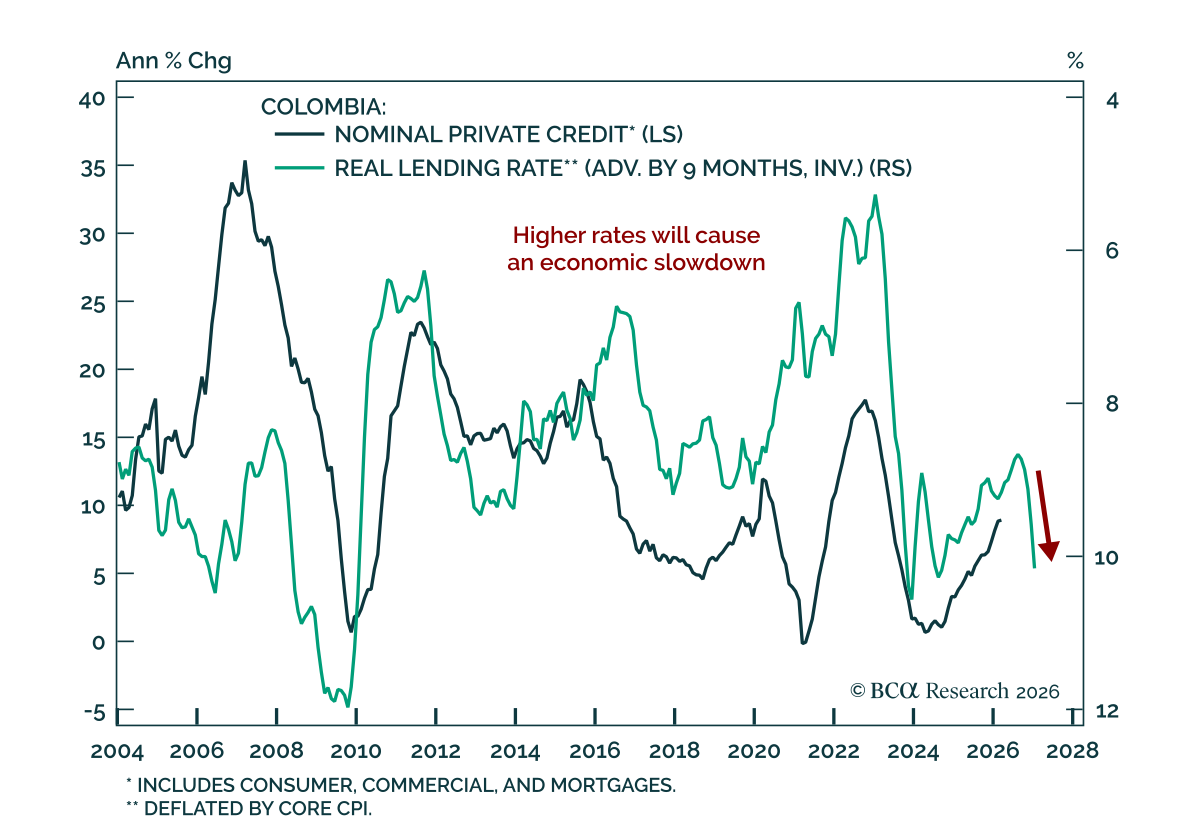

Our EM strategists view the rally in Colombian assets as being on borrowed time and recommend using near-term strength to reduce exposure. Colombia displays the markings of an attractive comeback story, with high interest rates, elevated oil prices, and a…

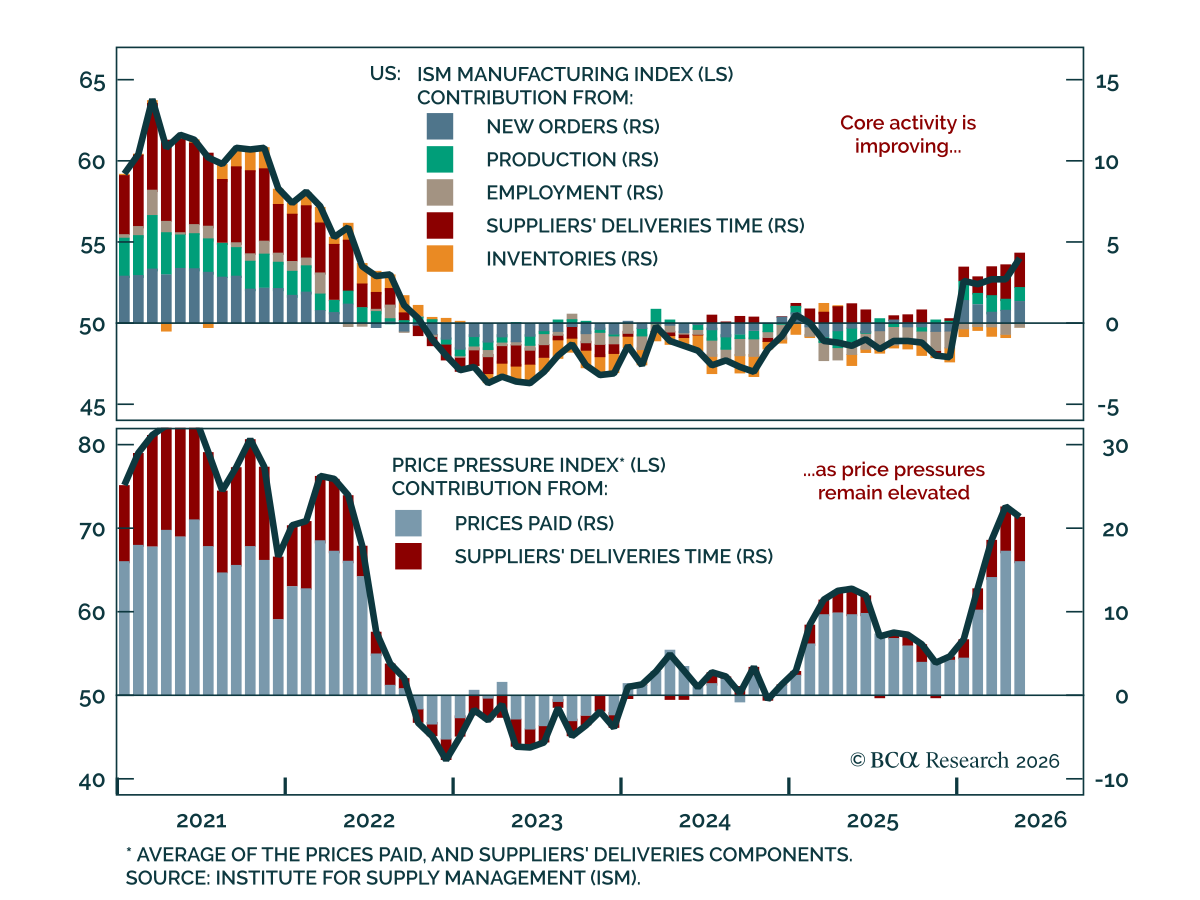

May’s US ISM Manufacturing report reinforces improving activity alongside persistent price pressure, highlighting continued inflationary impulse and hawkish risks to US monetary policy. The headline index came in at 54, above the market expectation of 53,…