Economy

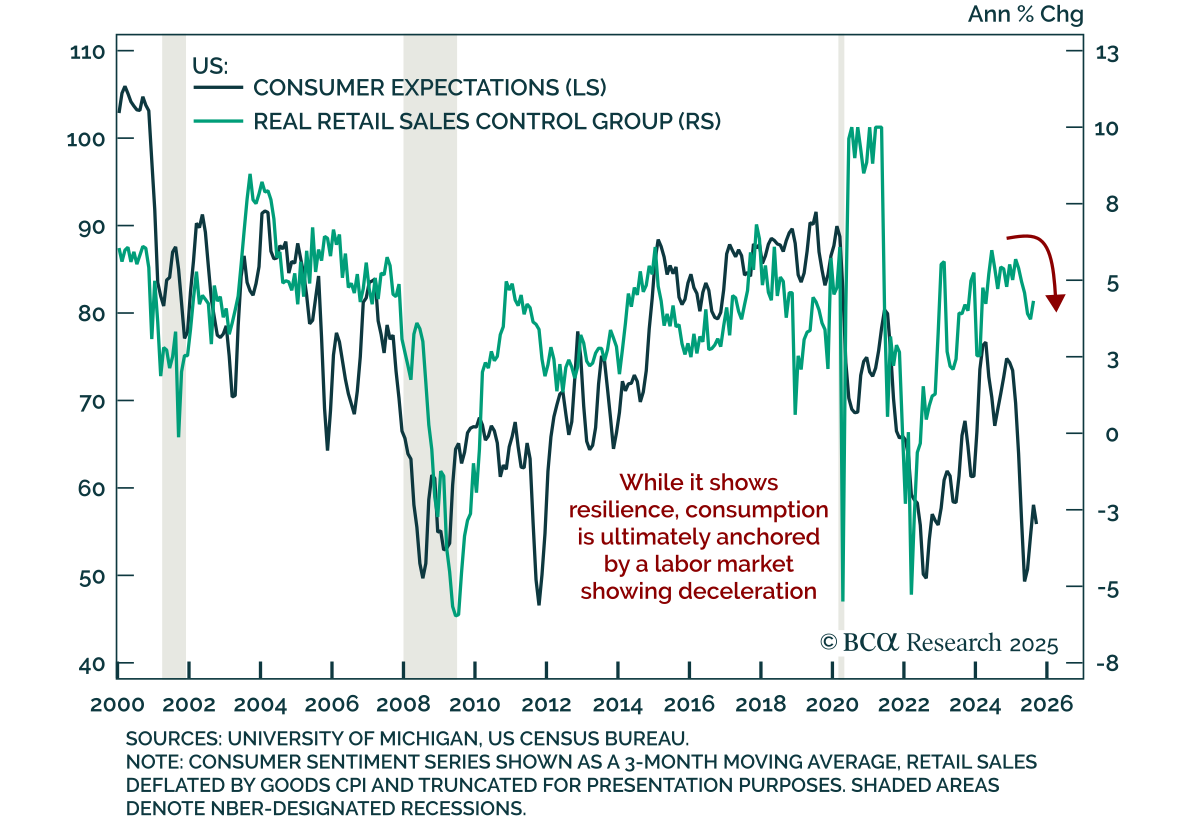

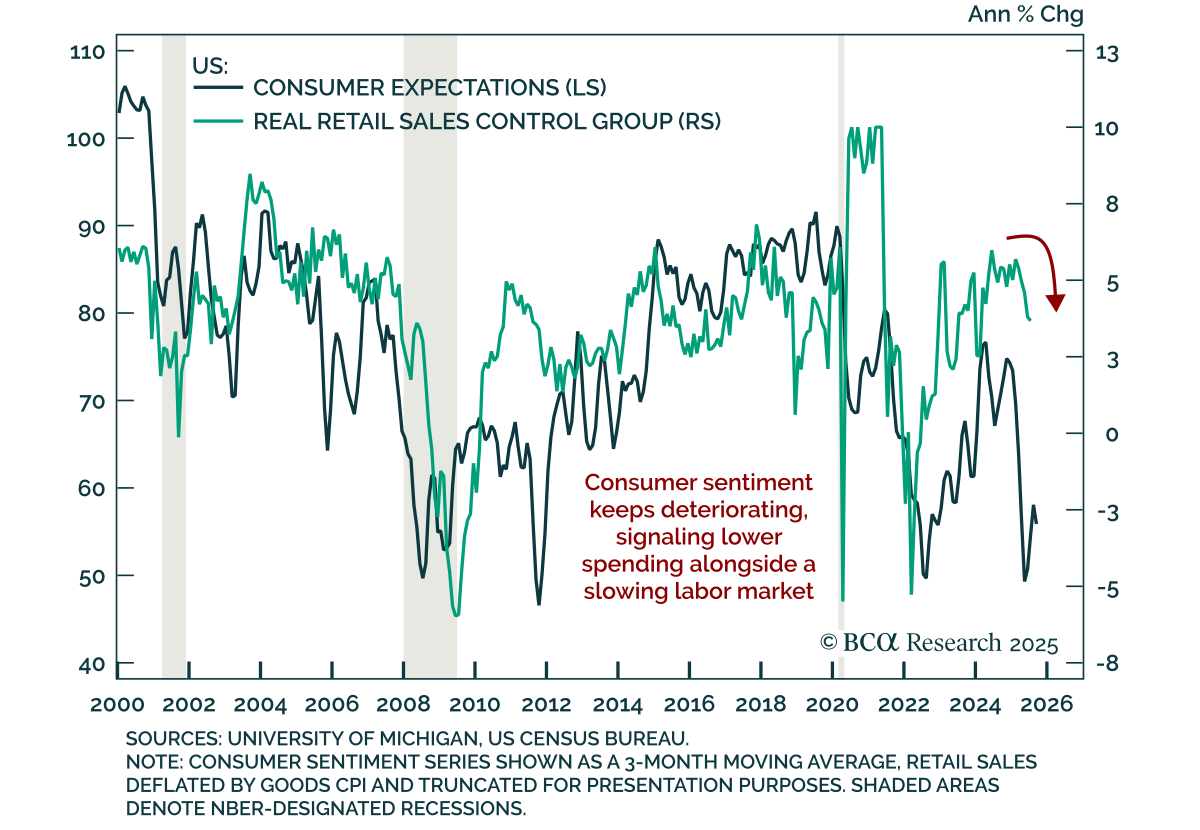

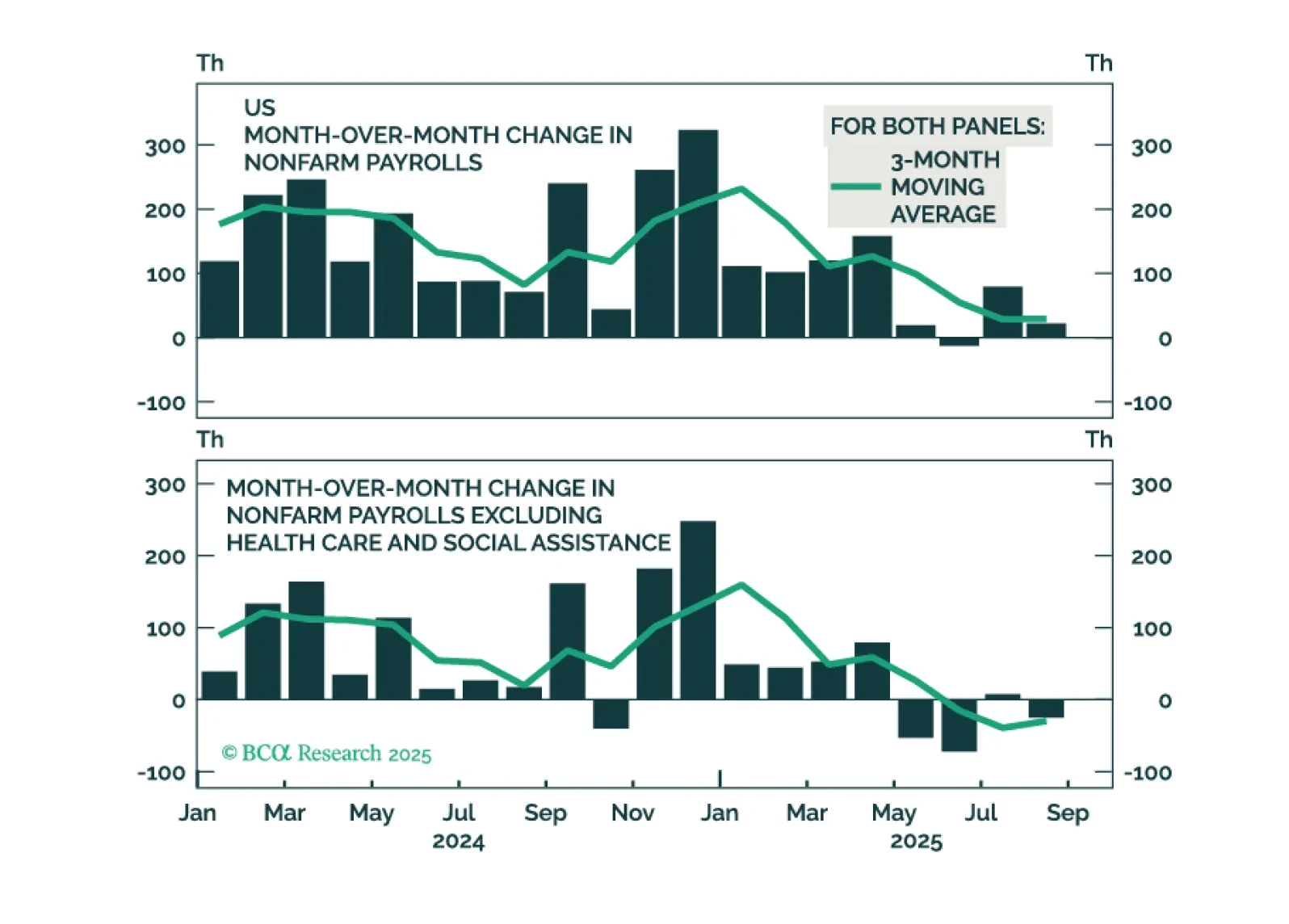

August retail sales beat expectations, but resilience in consumption does not alter a defensive stance as labor momentum weakens. Headline sales rose 0.6% m/m, unchanged from July, while core ex-autos and gas accelerated to 0.7% from 0.3%. The control group…

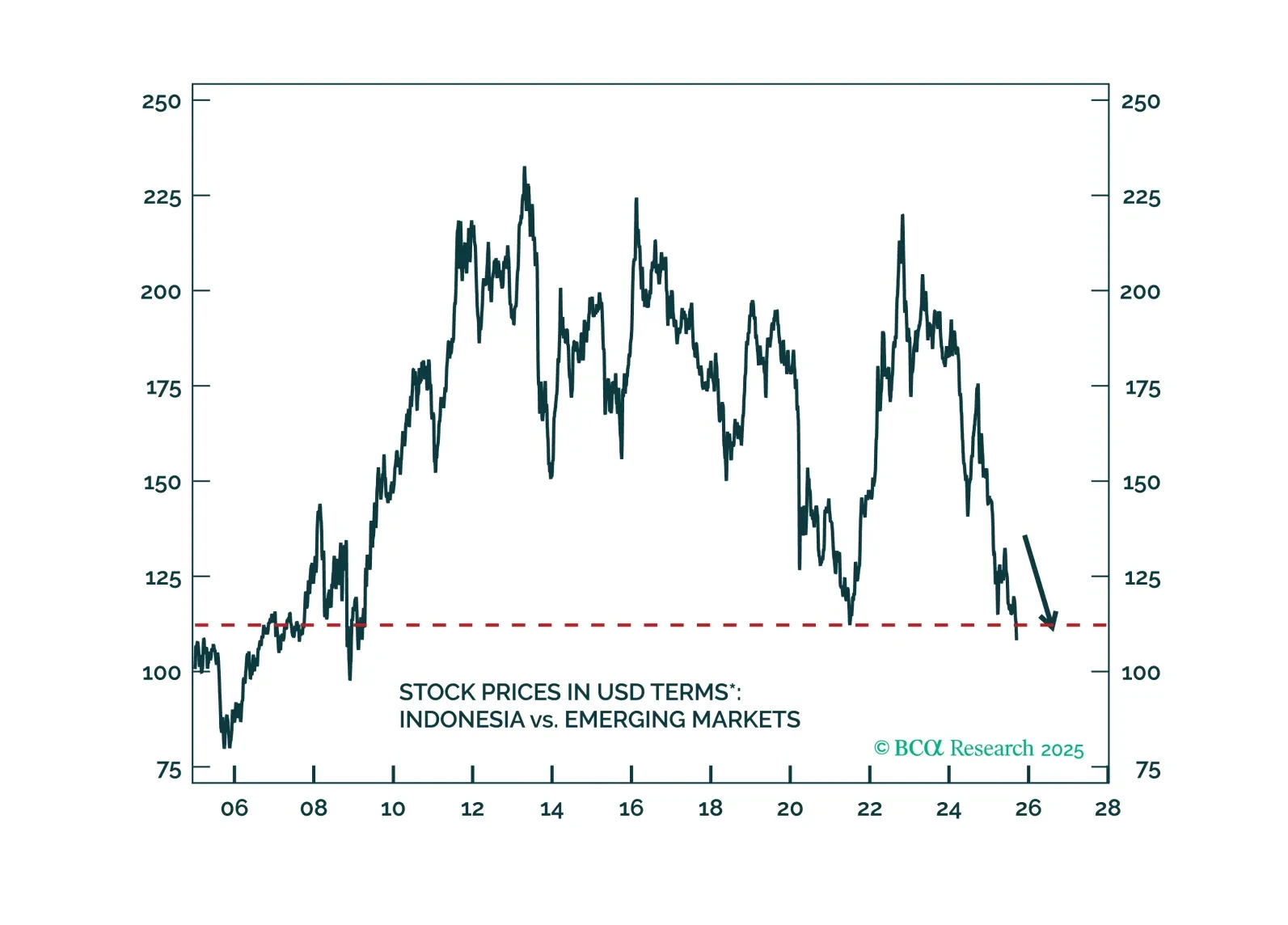

Indonesia’s policy easing will boost domestic demand, but fuel inflation. Current account deficit will widen, and the rupiah will weaken. Stay short the rupiah and go underweight Indonesian stocks, domestic bonds, and sovereign credit in their respective EM portfolios.

US consumer sentiment deteriorated in September, reinforcing signs of slowing consumption and supporting a defensive stance. The preliminary University of Michigan Consumer Sentiment Index dropped more than expected to 55.4 from 58.2, with declines in both…

While it is impossible to know exactly when global equities will peak, there are now enough vulnerabilities to justify keeping one’s finger near the eject button.

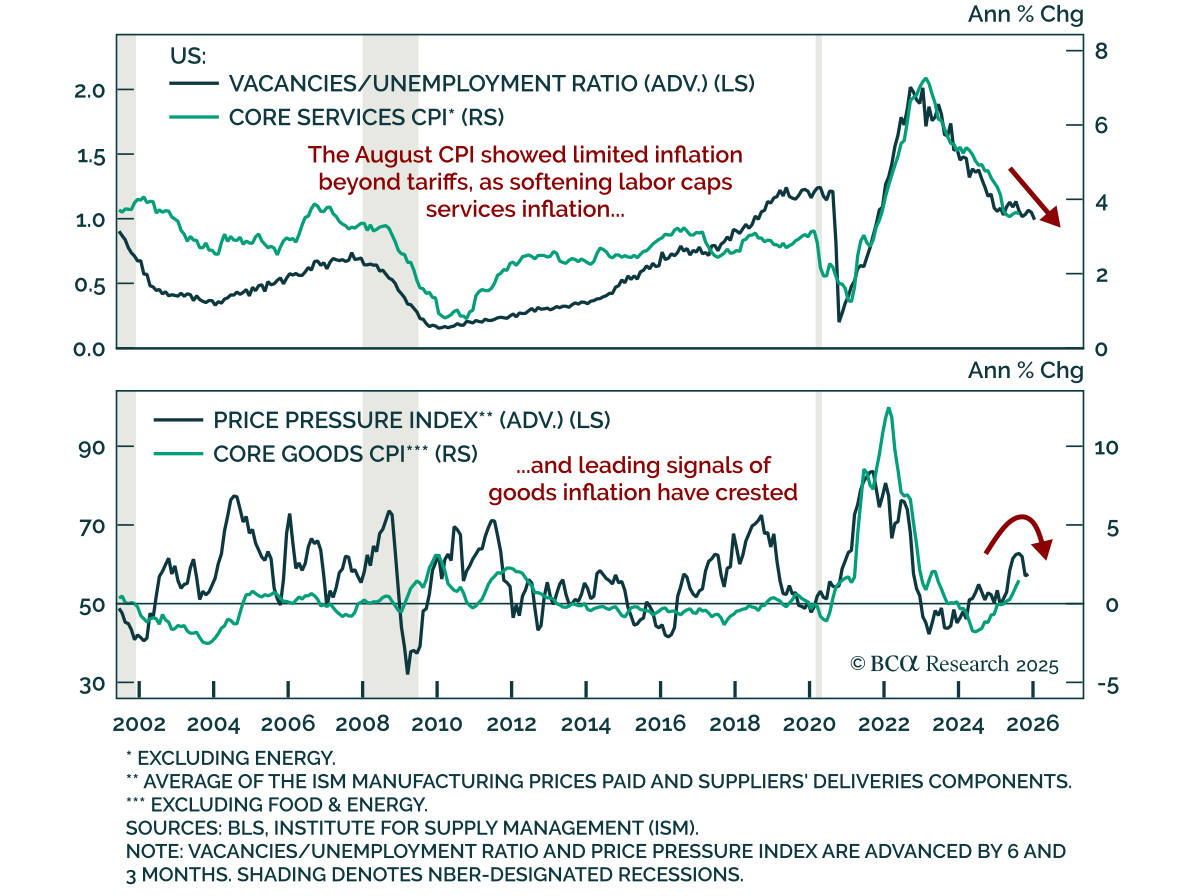

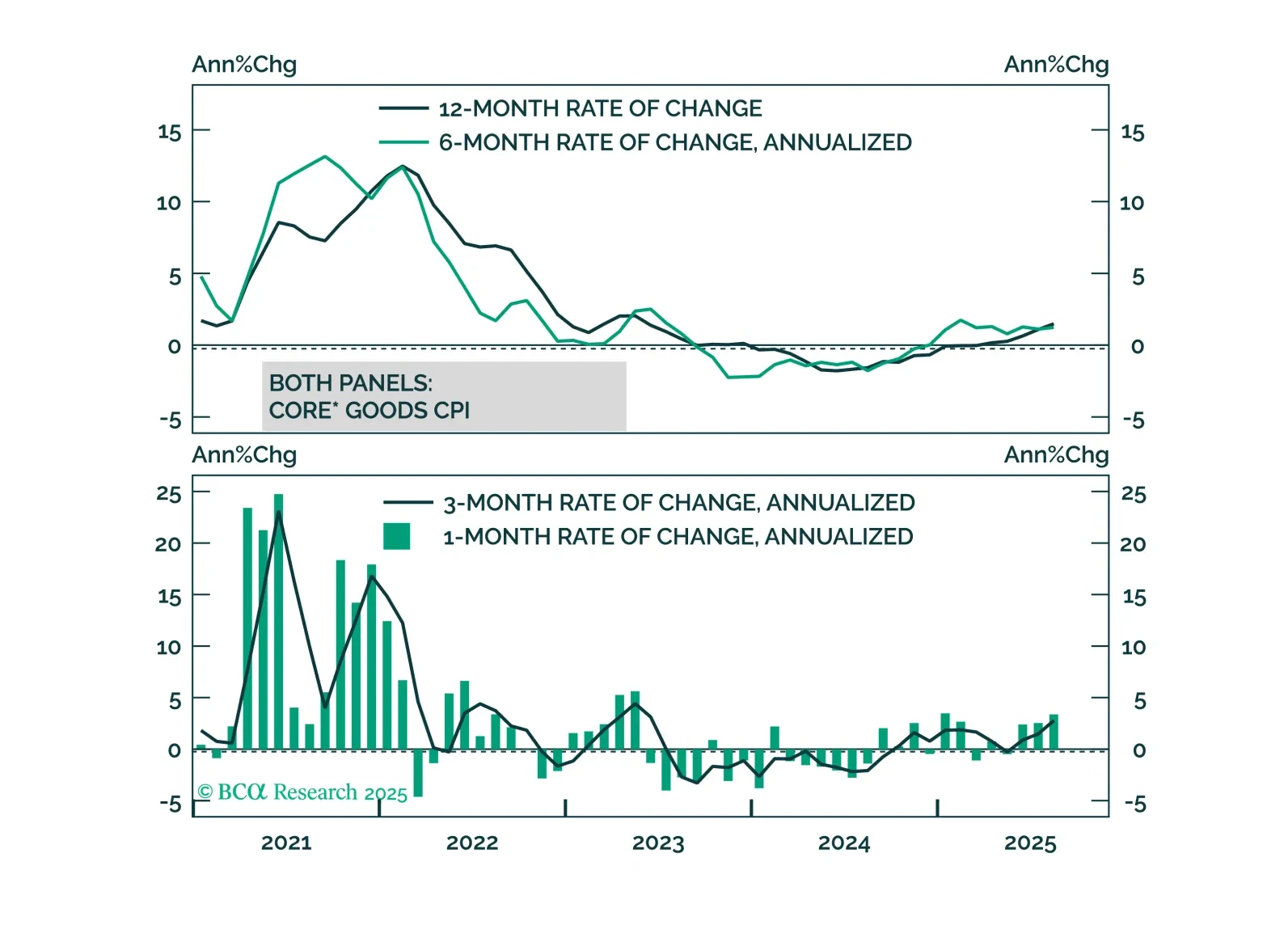

August US CPI was in line with expectations, reinforcing the case for Fed easing and a long-duration stance. Headline CPI rose 0.4% m/m (2.9% y/y), while core held at 0.3% m/m (3.1% y/y). Core goods inflation ticked up to 1.5% y/y from 1.1%, while services…

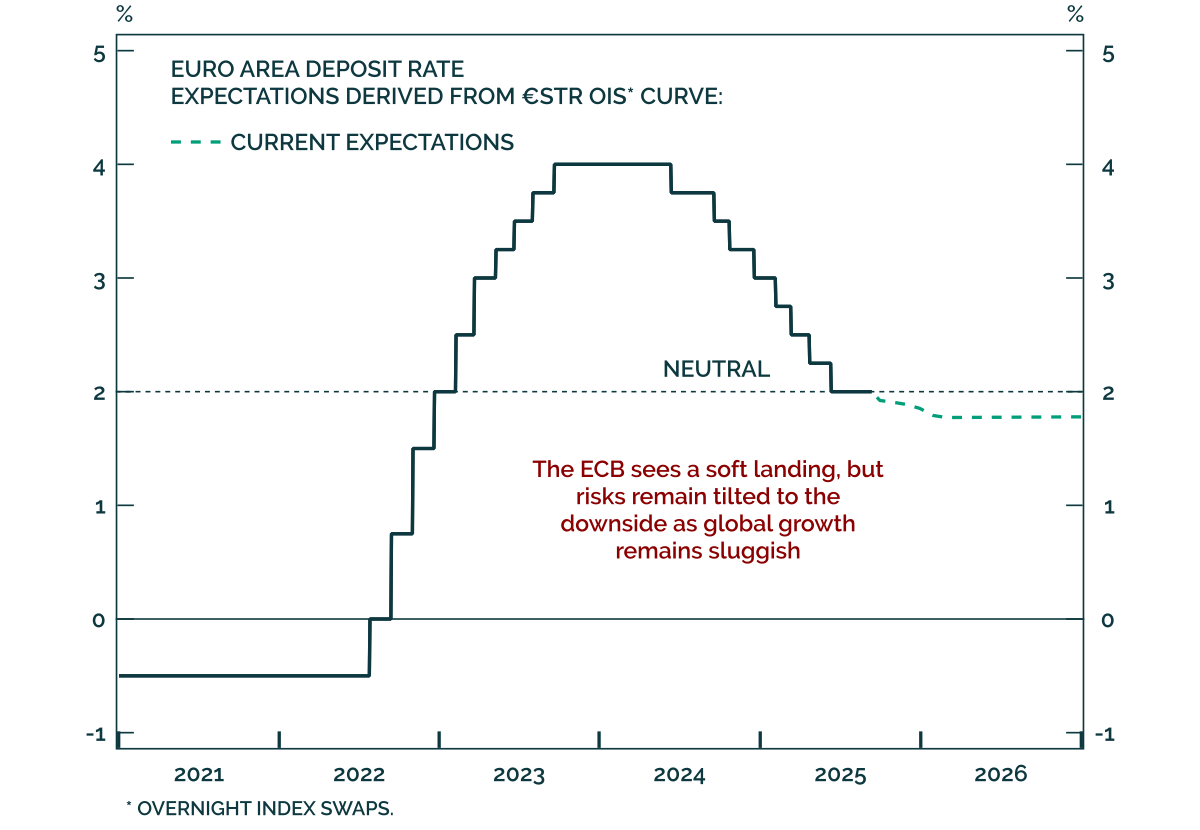

The ECB left policy unchanged in September, reiterating a data-dependent stance and signaling no urgency to ease. Markets barely reacted, consistent with a fully discounted decision. The Governing Council appears confident in a soft landing, making a December…

High US inflation is being driven by tariffs, not domestic inflationary pressure. This argues for Fed easing and a bull-steepening of the Treasury curve.

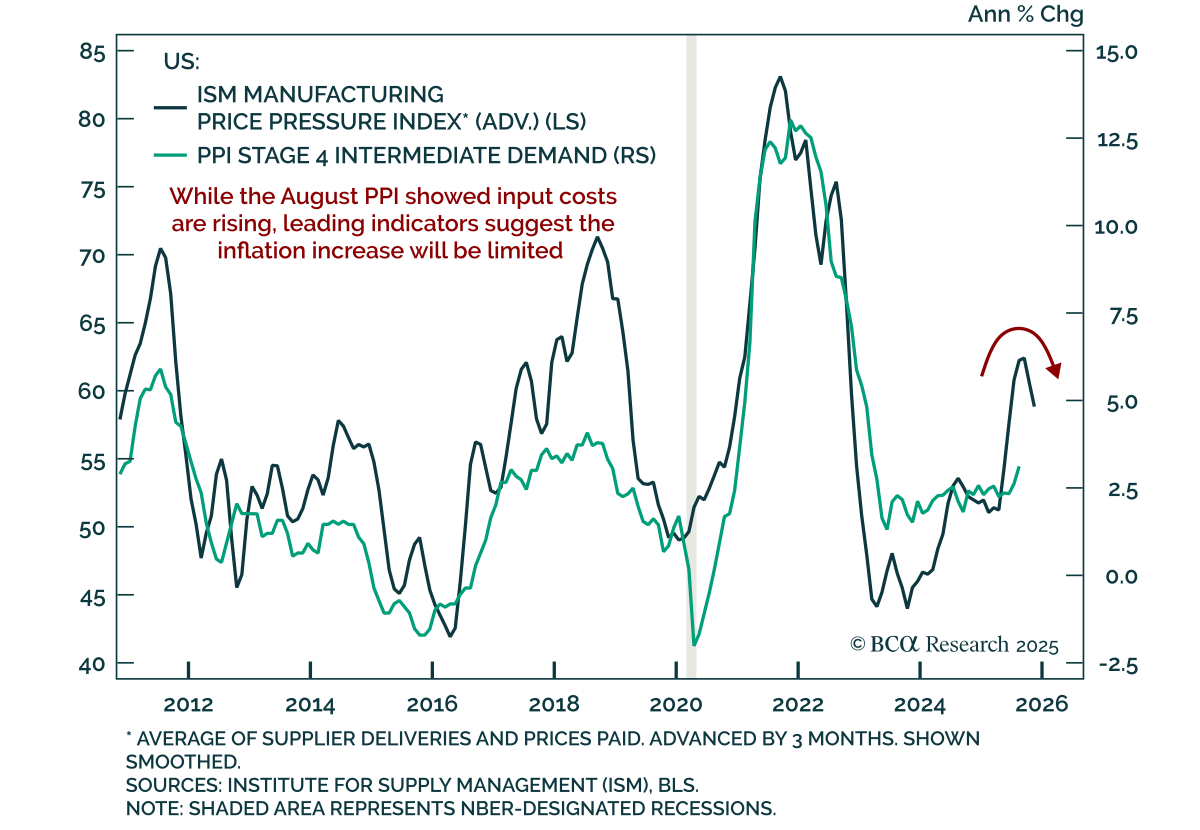

August PPI inflation cooled, reinforcing the case for Fed easing and long duration with steepeners. Headline PPI fell 0.1% m/m, bringing the annual rate down to 2.6% after July’s 0.7% gain. Core PPI (ex-food, energy, and trade) rose 0.3% m/m (2.8% y/y).…

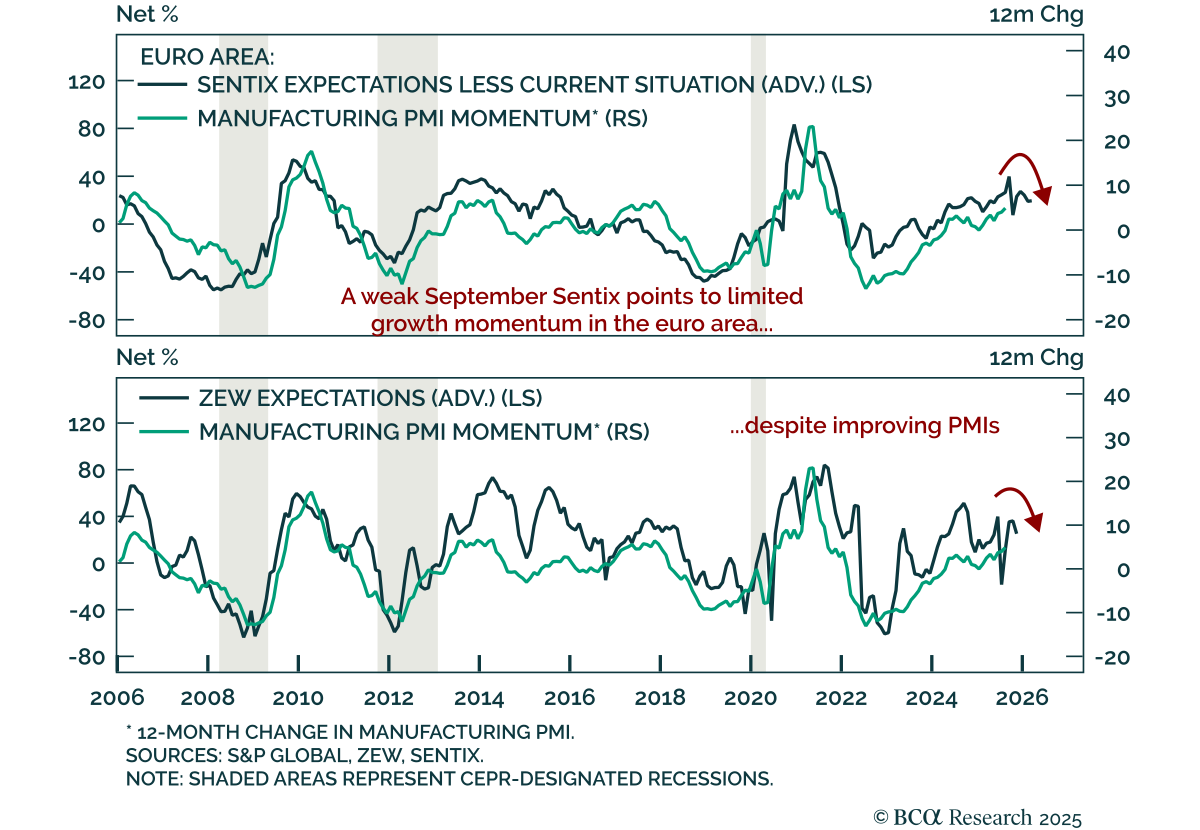

European sentiment continues to weaken, reinforcing the tactical case for US outperformance over Europe. The September Sentix Investor Confidence index fell to -9.2 from -3.7, defying expectations for an increase and signaling that August’s deterioration is…

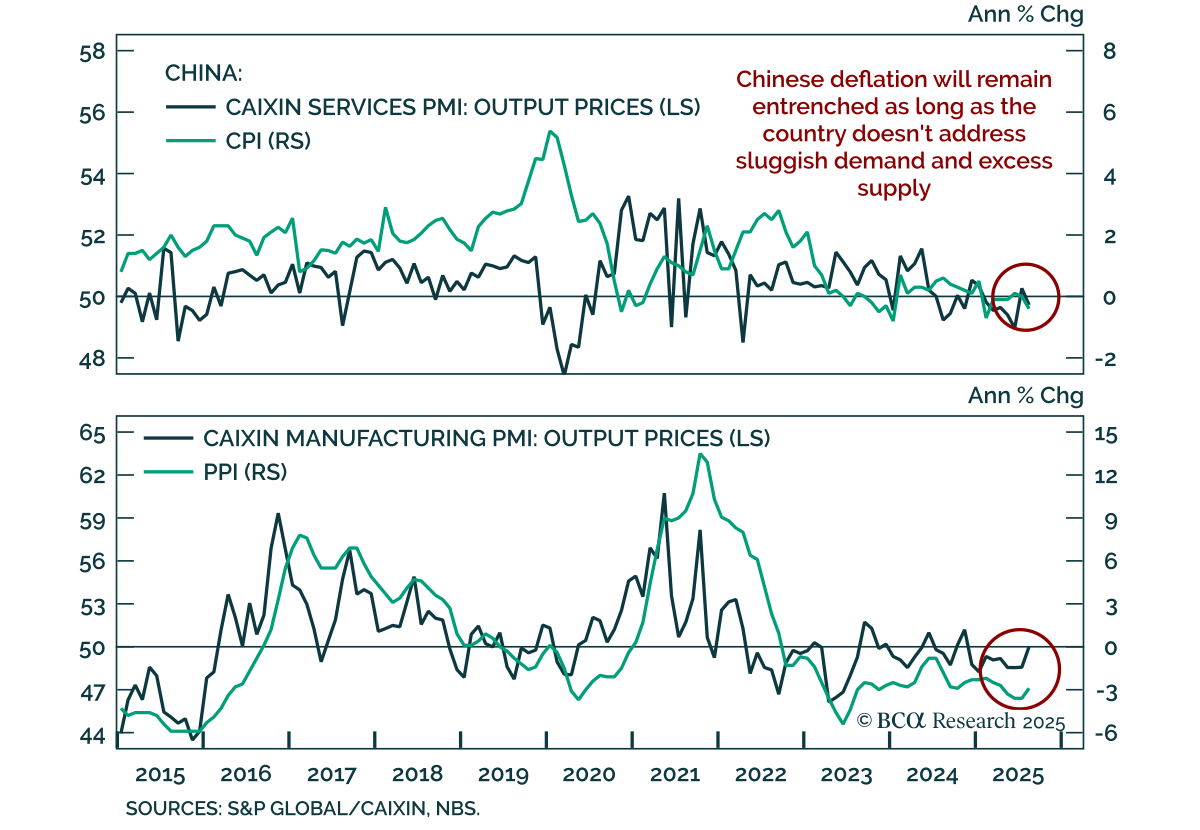

China’s August inflation data confirm entrenched deflation, reinforcing our overweight in onshore bonds and a tactical long in onshore small- and mid-caps versus large caps ahead of potential stimulus. Producer prices declined 2.9% y/y, easing from…