Economy

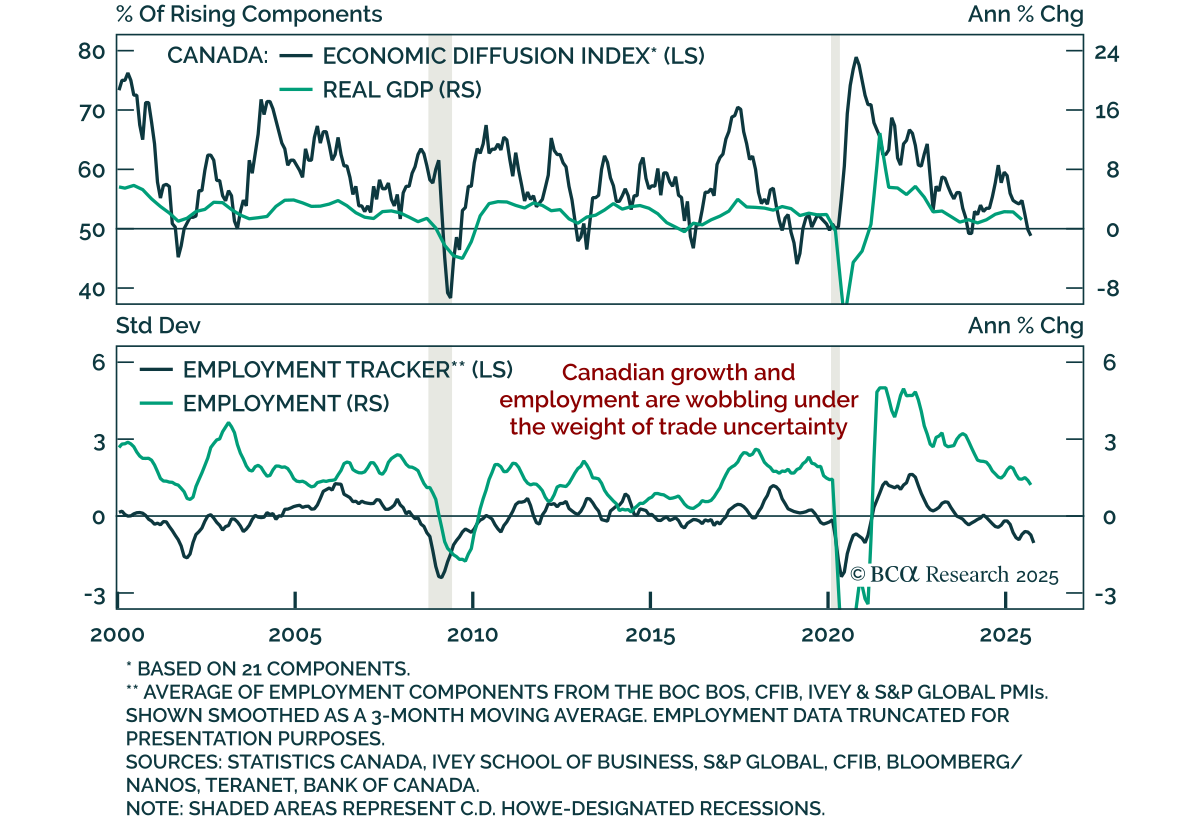

Recent Canadian data confirm slowing growth, reinforcing support for government bonds and steepeners. The October CFIB Business Barometer fell to 46.3 from 50.2, indicating contraction and underscoring the risk posed by small business weakness given their…

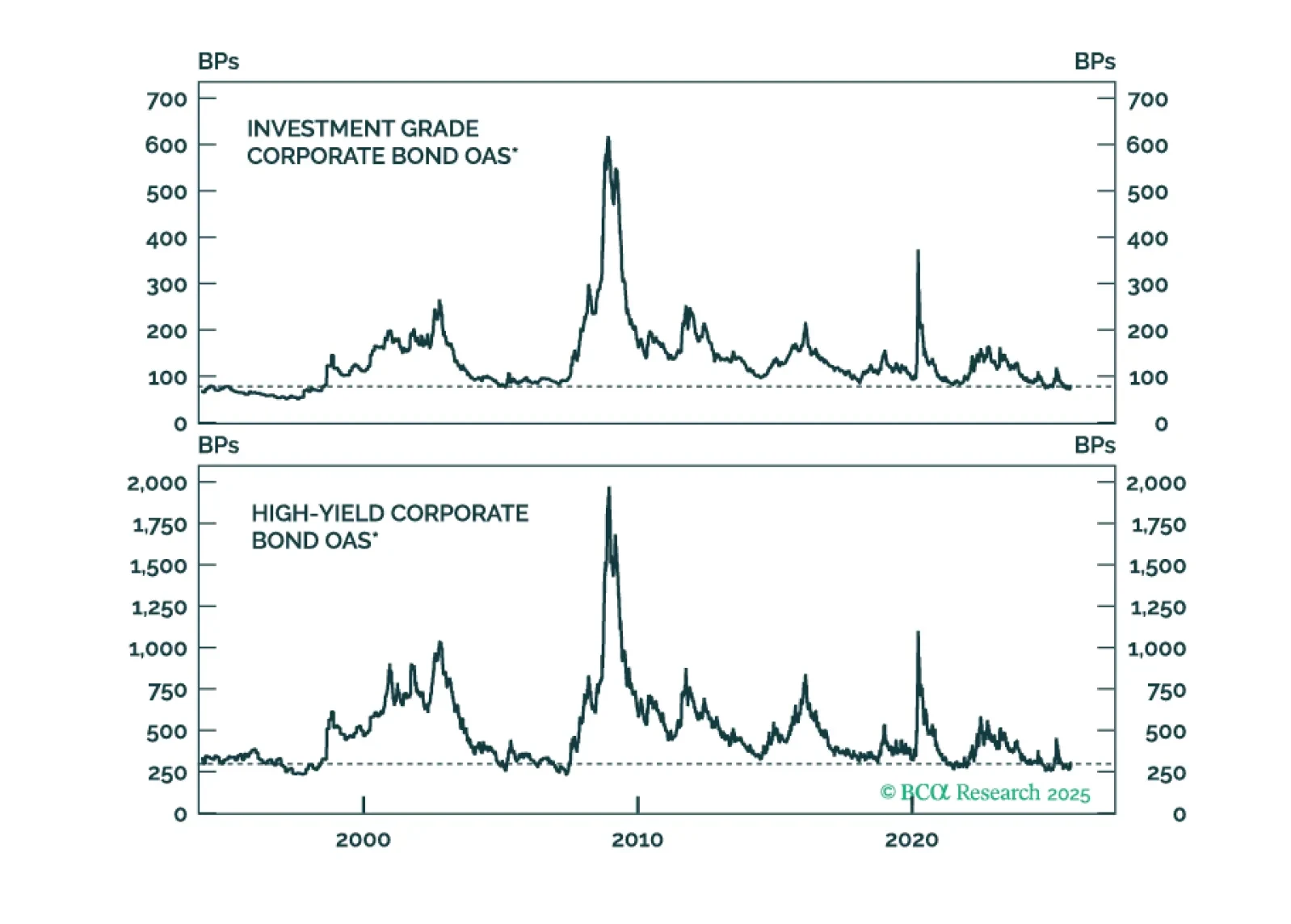

This week’s Special Report evaluates the reward and risk in corporate bonds. We address the question of whether low expected excess returns today are justified by low risk or an example of overvaluation.

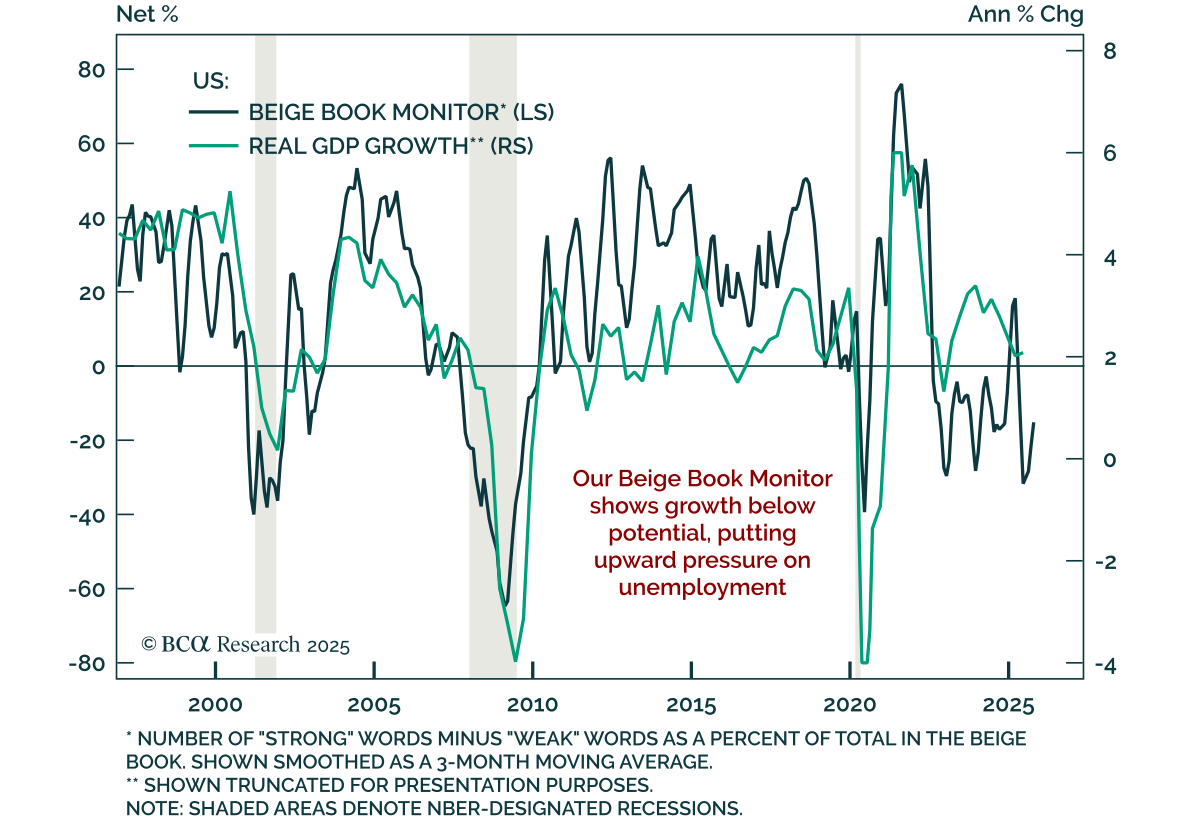

The October Fed Beige Book points to slowing growth as uncertainty continues to weigh on activity. Fed contacts reported consumer spending recently decreased, though auto sales were supported by EV purchases ahead of the expiration of tax credits. Lower- and…

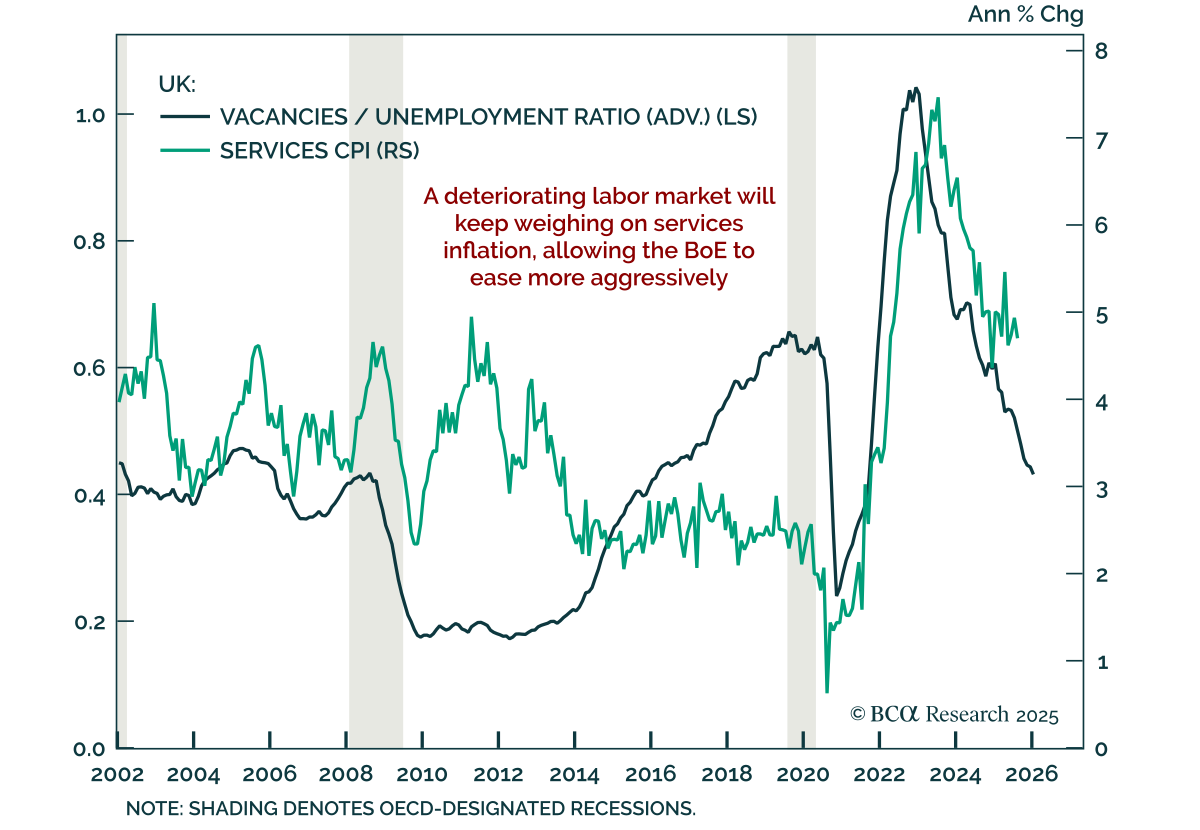

UK labor data weakened in August and September, reinforcing downside inflation risks and supporting overweight Gilts with 2s10s steepeners. Payrolls fell by 10k in September, while job vacancies continued to slide to cyclical lows as unemployment reached…

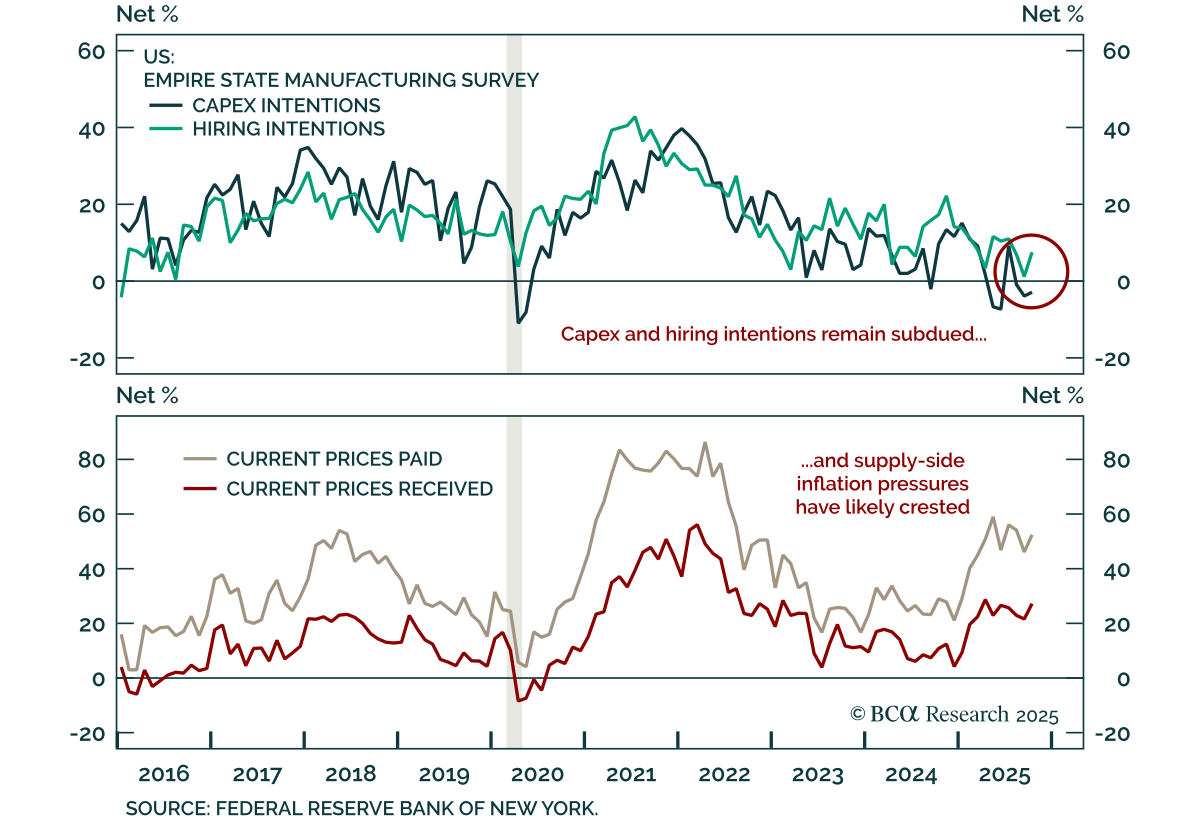

The October Empire Manufacturing survey beat estimates, but weak investment and hiring intentions temper its positive signal. The index rose to 10.7 from -8.7, indicating modest activity growth. New orders ticked up, and shipments increased after plunging…

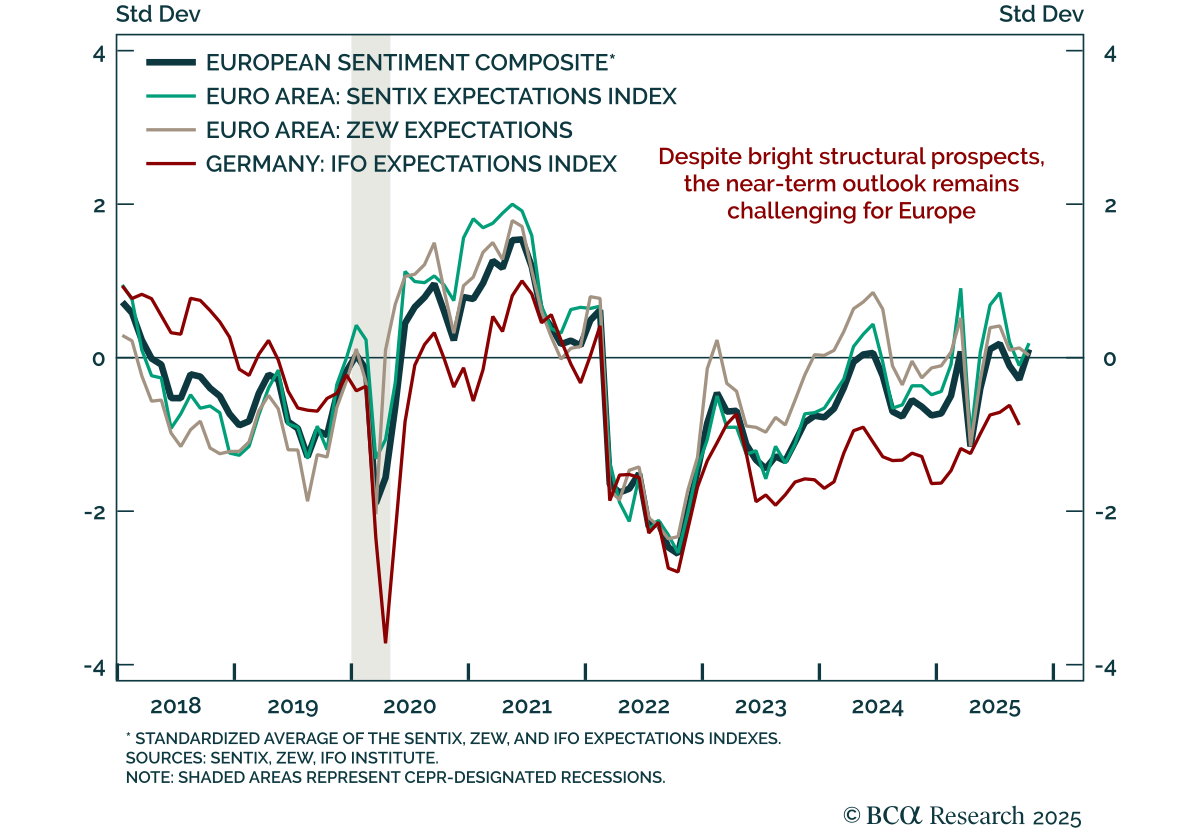

The October ZEW survey sent a mixed signal on near-term European growth, confirming limited growth momentum. Euro area growth expectations fell to 22.7 from 26.1, while German expectations missed estimates but rose slightly to 39.3 from 37.3. Current…

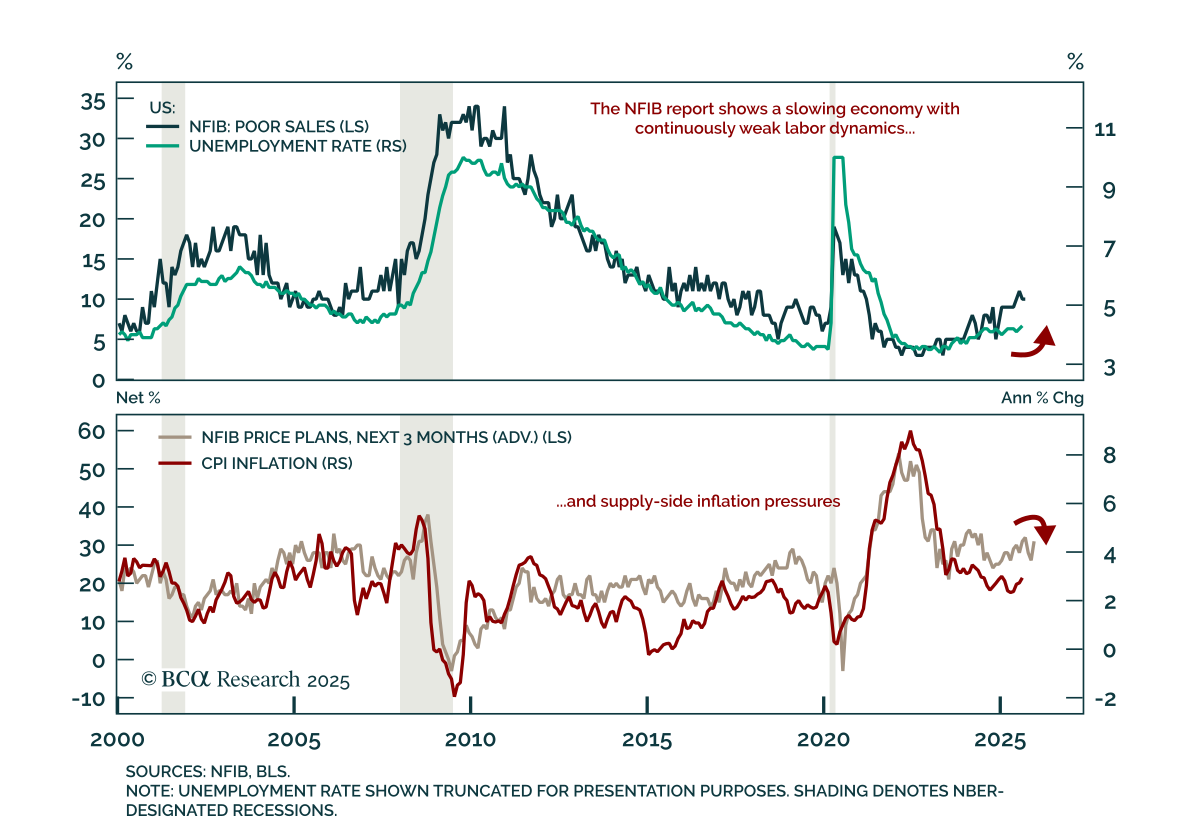

The September NFIB Small Business Optimism Index missed estimates, falling to 98.8 from 100.8. The decrease was driven by expectations, as fewer small businesses expect the economy to improve or real sales to rise. Firms also reported inventories as too high,…

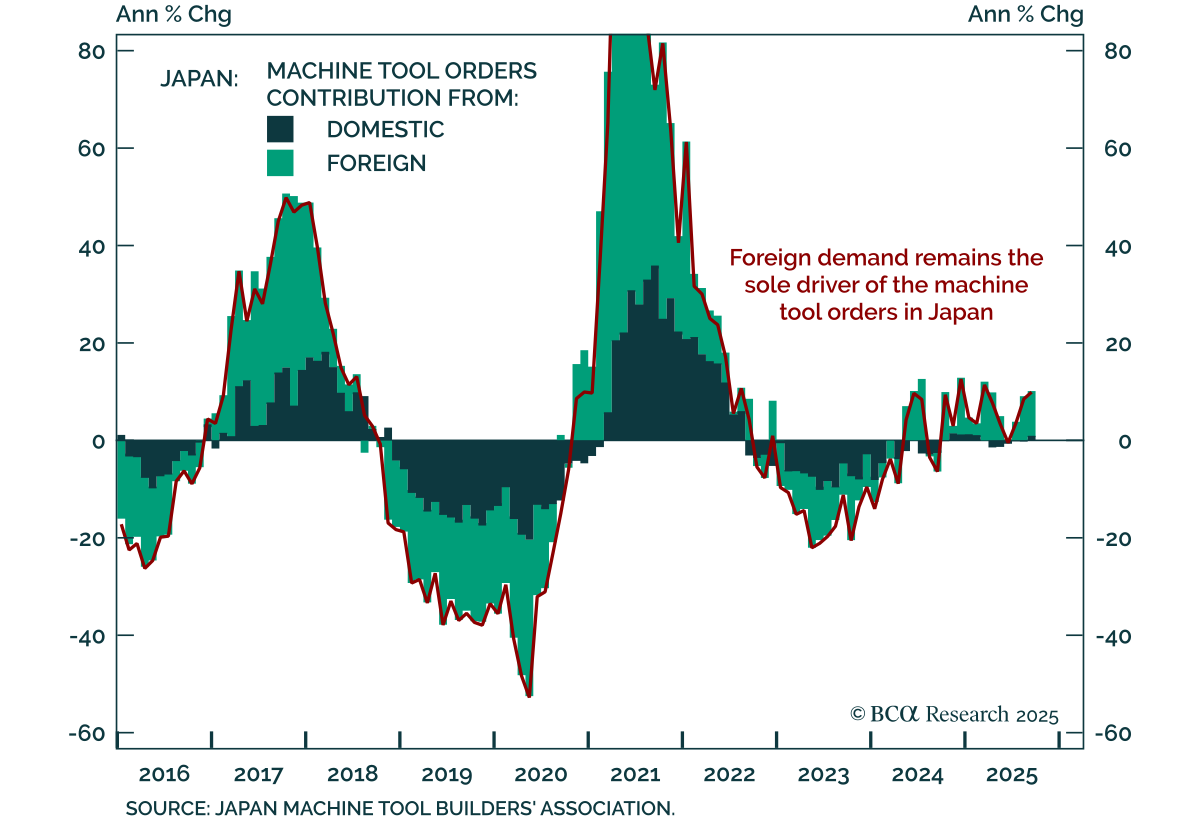

Japan’s September machine tool orders rose 9.9% year-on-year to a six-month high, led by a 13% jump in foreign exports, reinforcing the growing tailwind for Japan’s industrial sector and supporting a structural overweight yen position. Foreign demand remains…

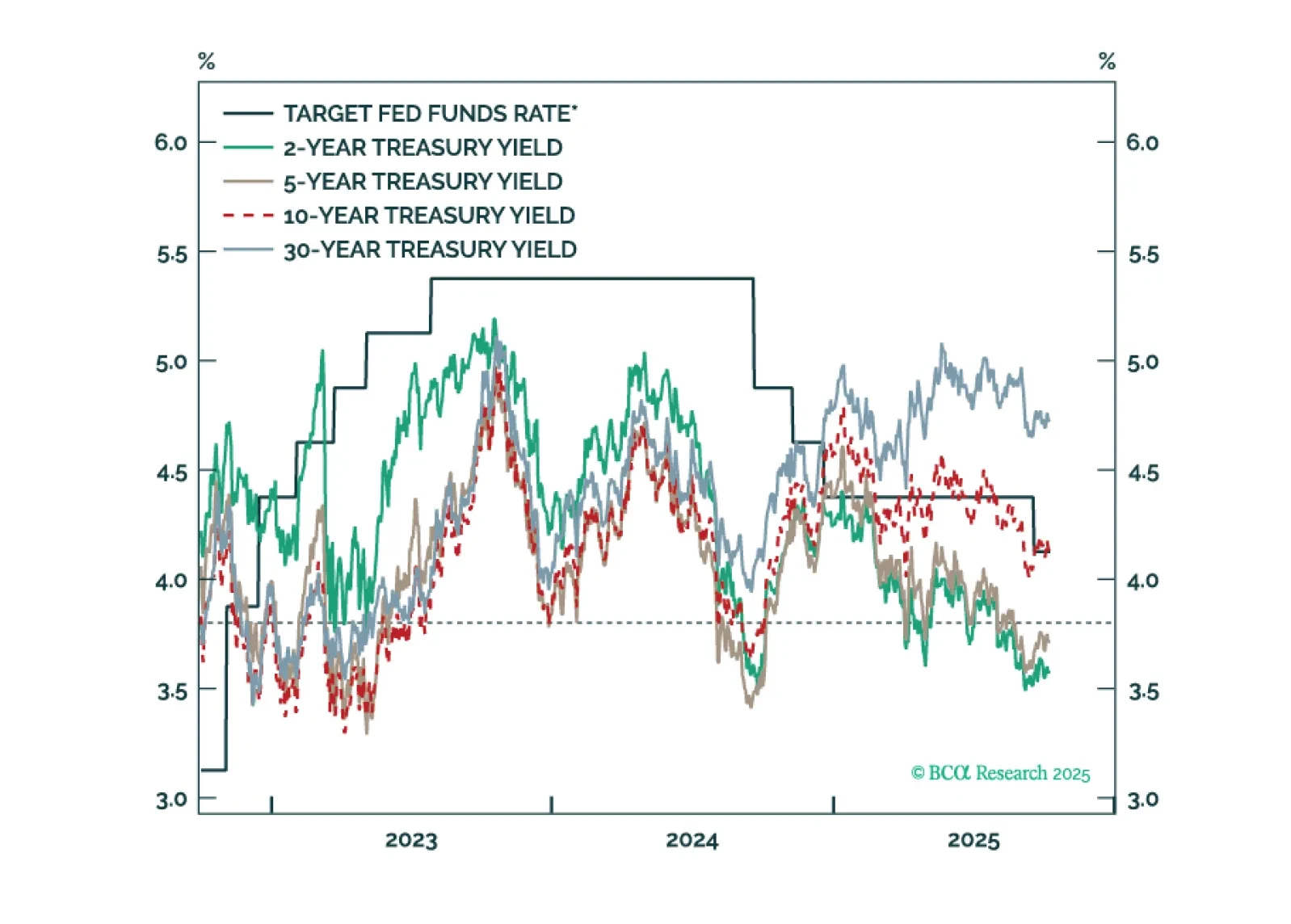

Treasury yields are generally following the pattern of past interest rate cycles, but with a larger term premium keeping the curve steeper than usual.

In this Q4 Strategy Outlook, we discuss where we stand on our recession call, the outlook for stocks and bonds in various scenarios, why investors are misunderstanding the impact of AI on corporate profits, whether the US dollar has entered a structural downtrend, our perspective on the yen, gold and other commodities, and much more.