Economy

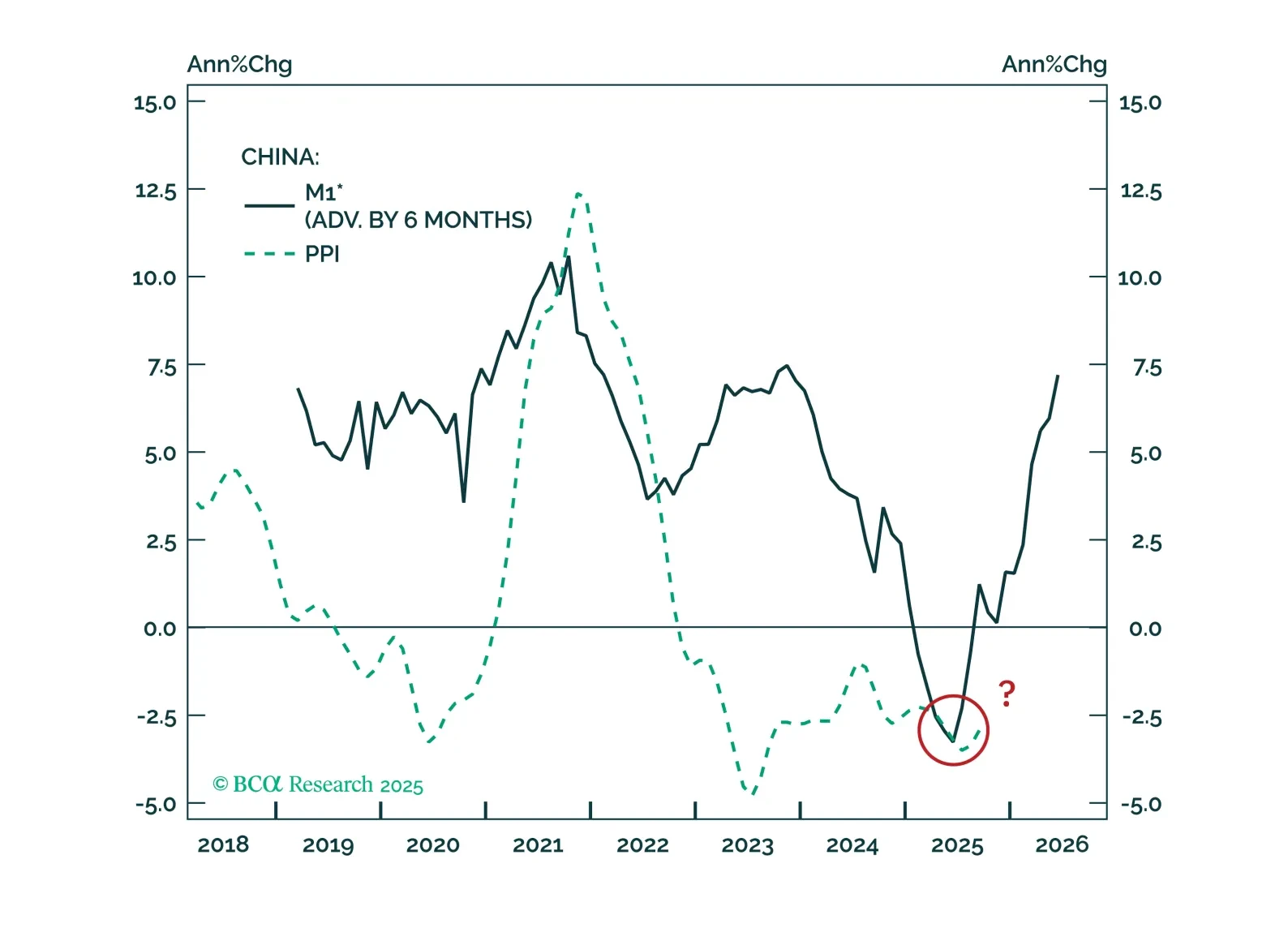

This month’s China High-Frequency Indicator (HFI) Chartbook decodes the conflicting messages in recent economic data, highlights key signals from our HFI, and explains what they mean for China’s economy and markets.

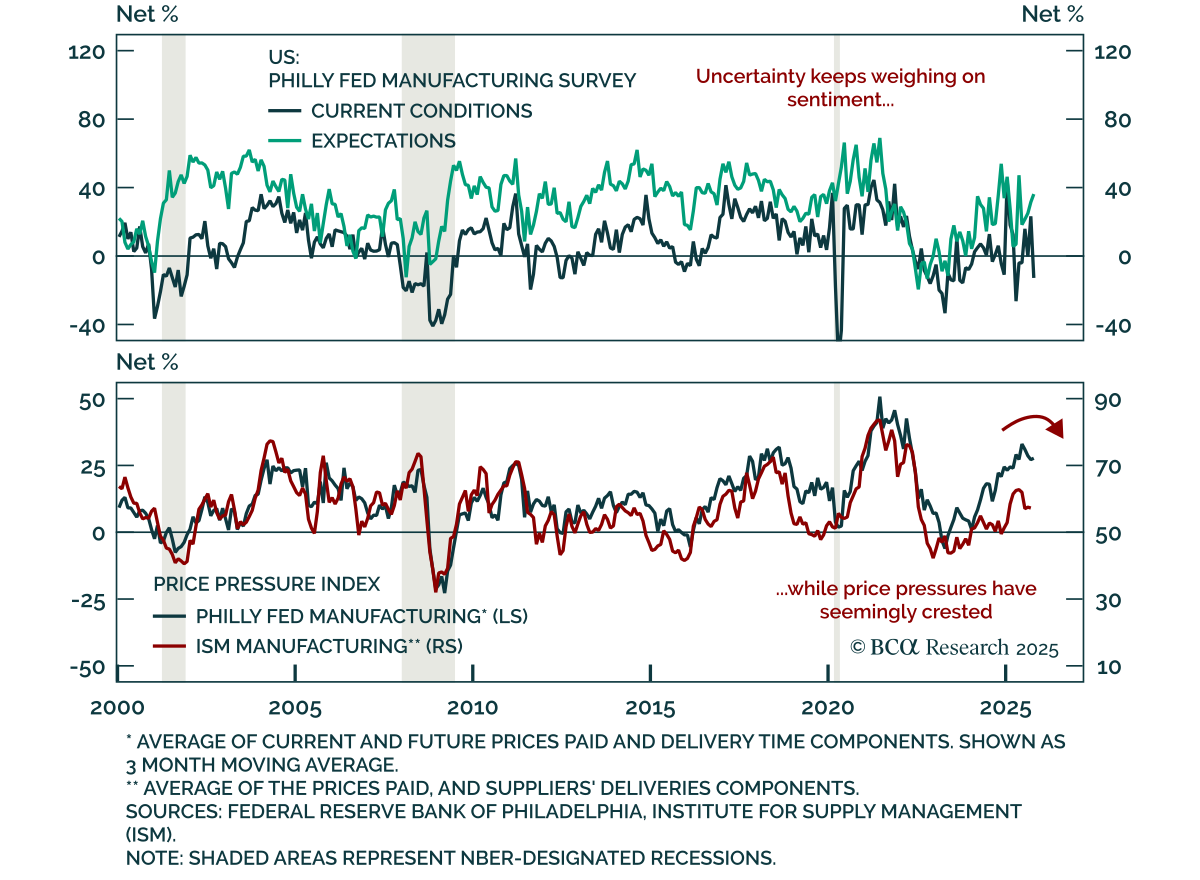

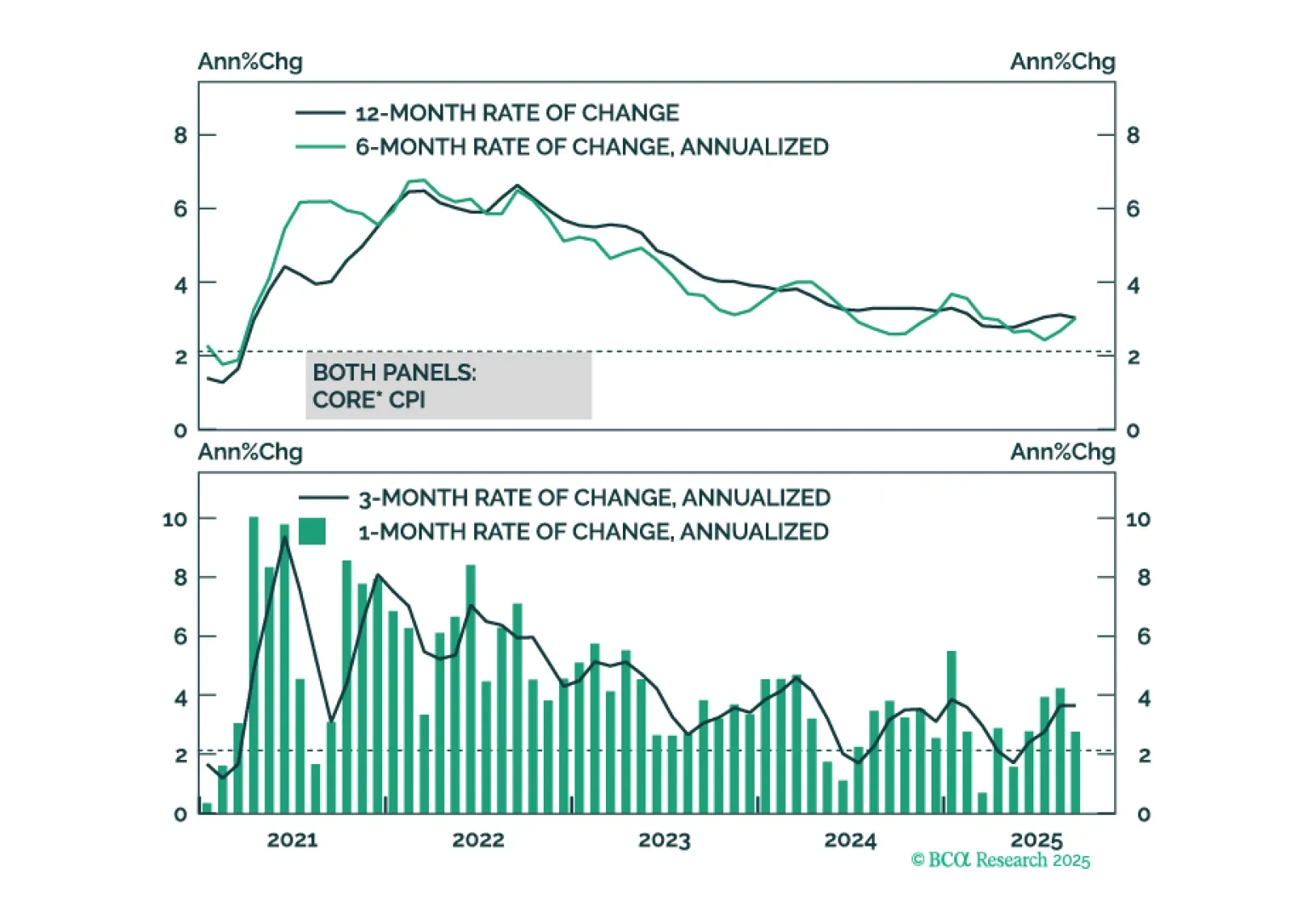

US inflation data continue to show no signs of price pressures beyond a near-term tariff effect.

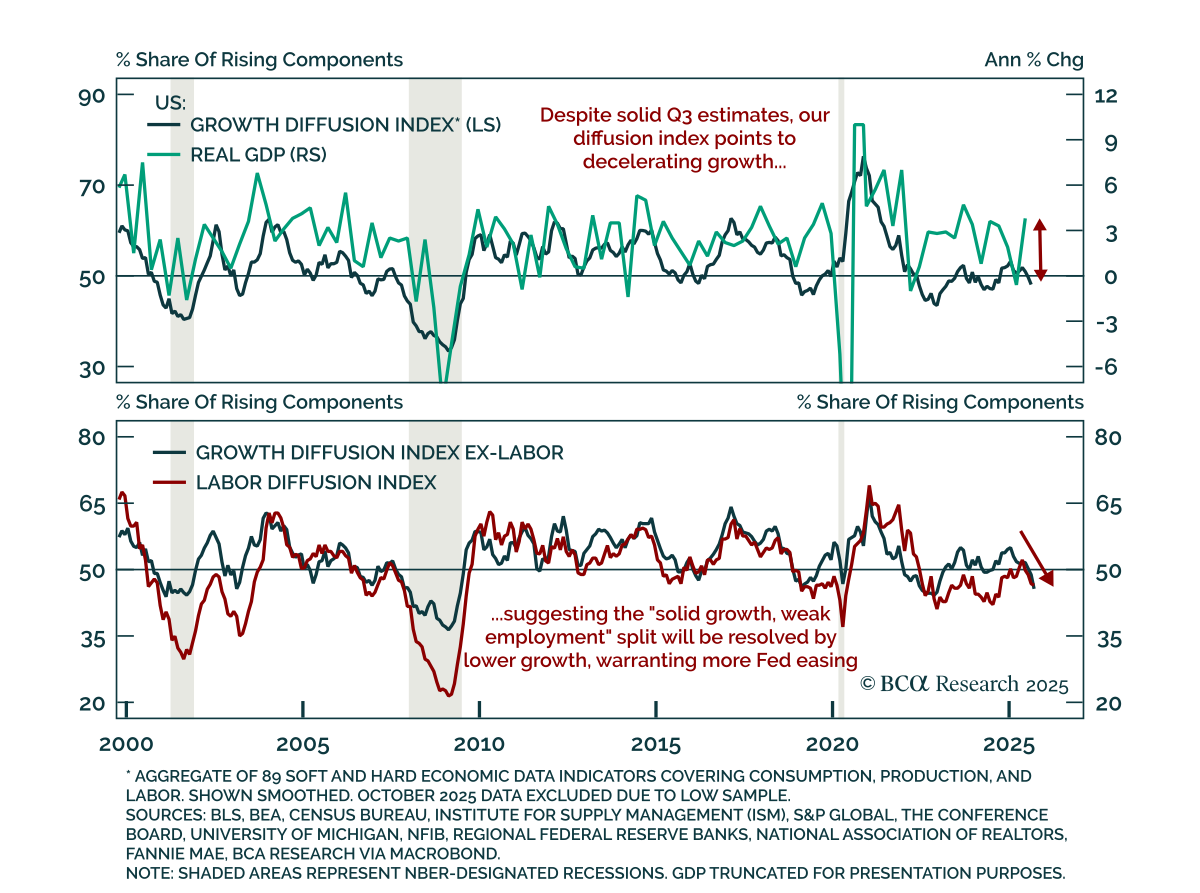

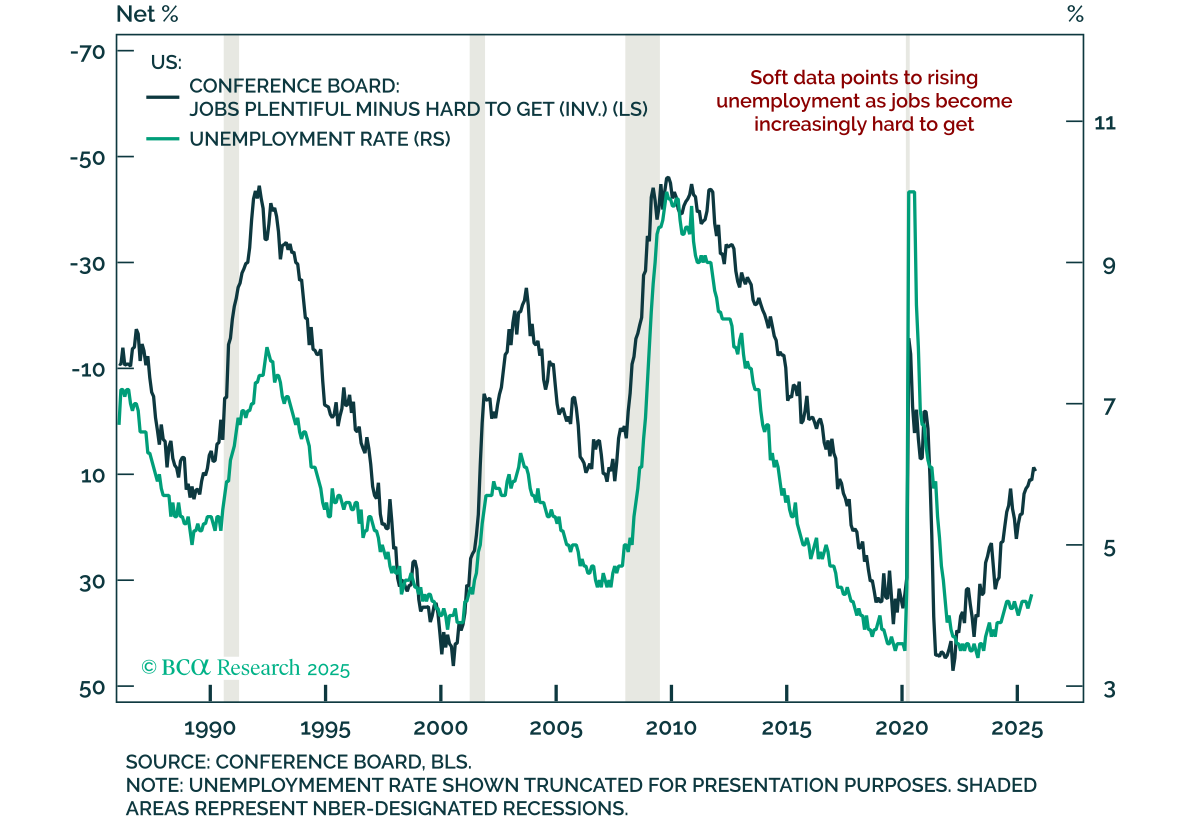

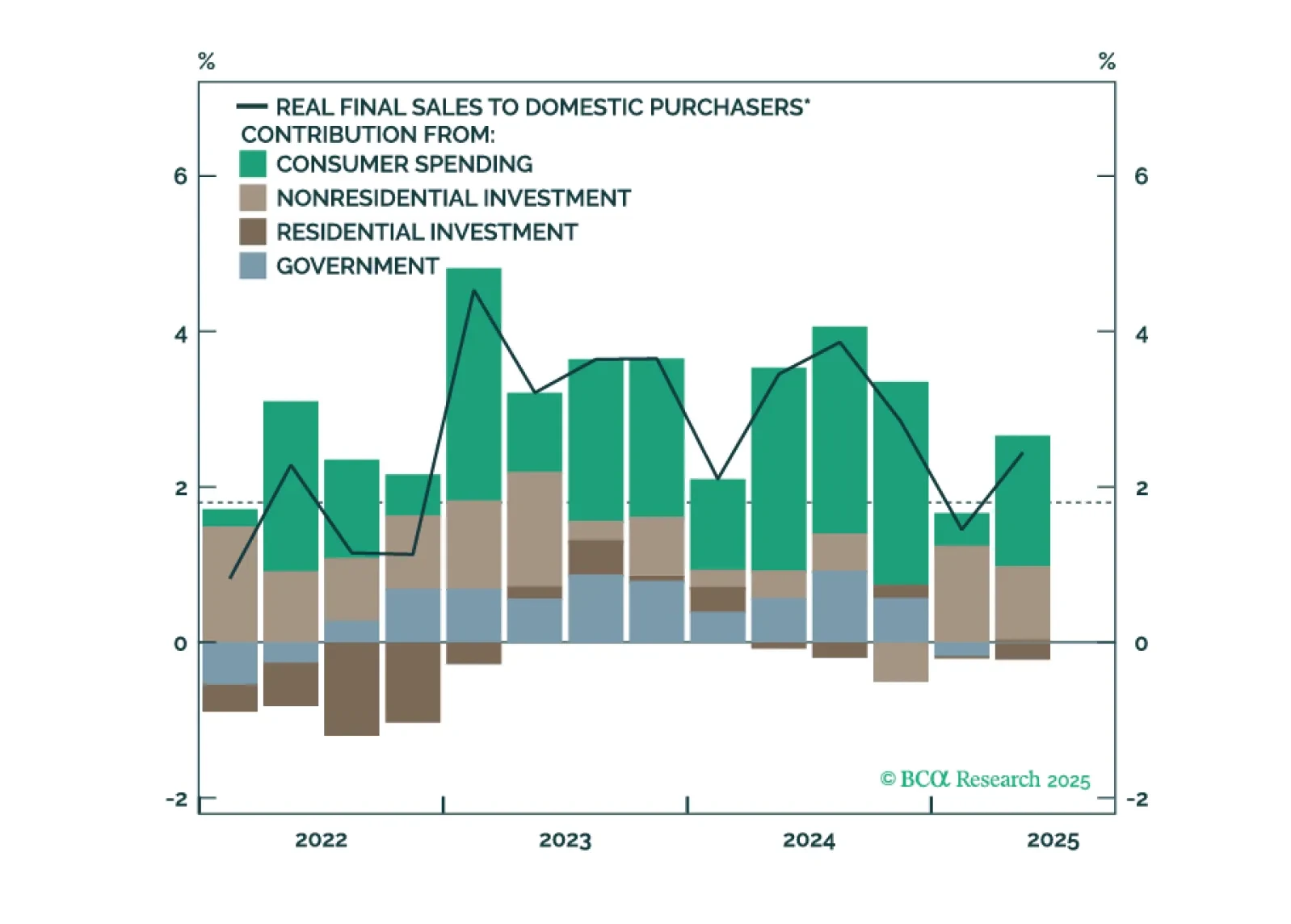

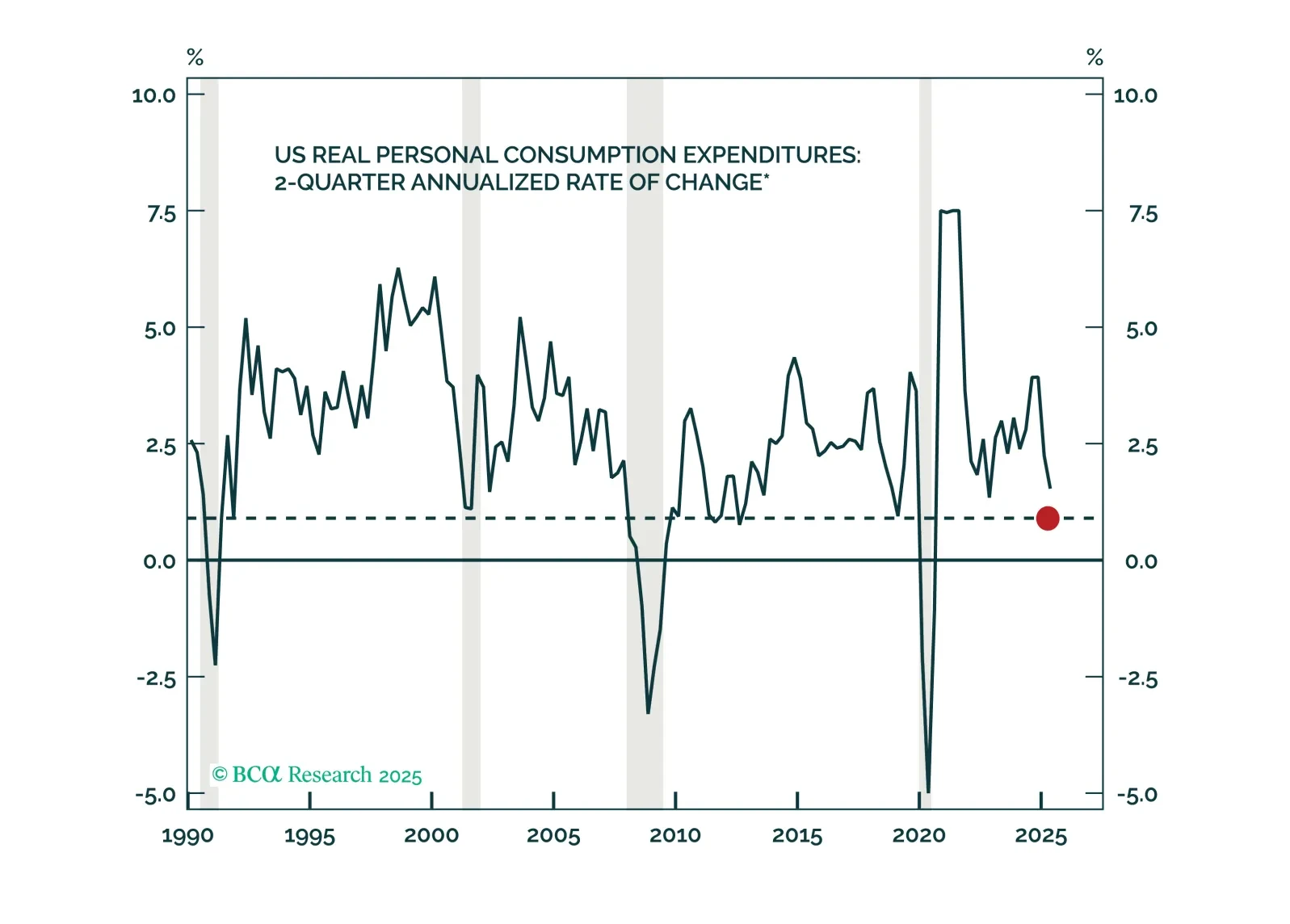

The Fed is poised to deliver a 25-basis-point rate cut this month, but a follow-up rate cut in December will depend on how the divergence between strong consumer spending and weak employment growth is resolved.

The most significant divide in the stock market and the economy is the gap between companies positioned to benefit from the AI boom and companies without a link to it. The former are surging while many of the latter are struggling.