Economy

To start 2026, we answer what we believe are the most important questions facing investors surrounding the labor market, monetary and fiscal policy, and AI stocks. Overall, we reiterate our overweight views on risk assets and highlight the risks surrounding the upcoming tariff decision.

MacroQuant has downgraded equities to underweight, favors a below-benchmark duration stance in fixed-income portfolios, remains bearish on the US dollar, and is still bullish on gold.

Every year, the Global Asset Allocation team compiles a list of our favorite books, essays, and articles from our strategists ahead of the holiday season. This year, we focus on writings by practitioners in the world of finance, business, and beyond. While diverse in their backgrounds, one theme stands out: Adaptation.

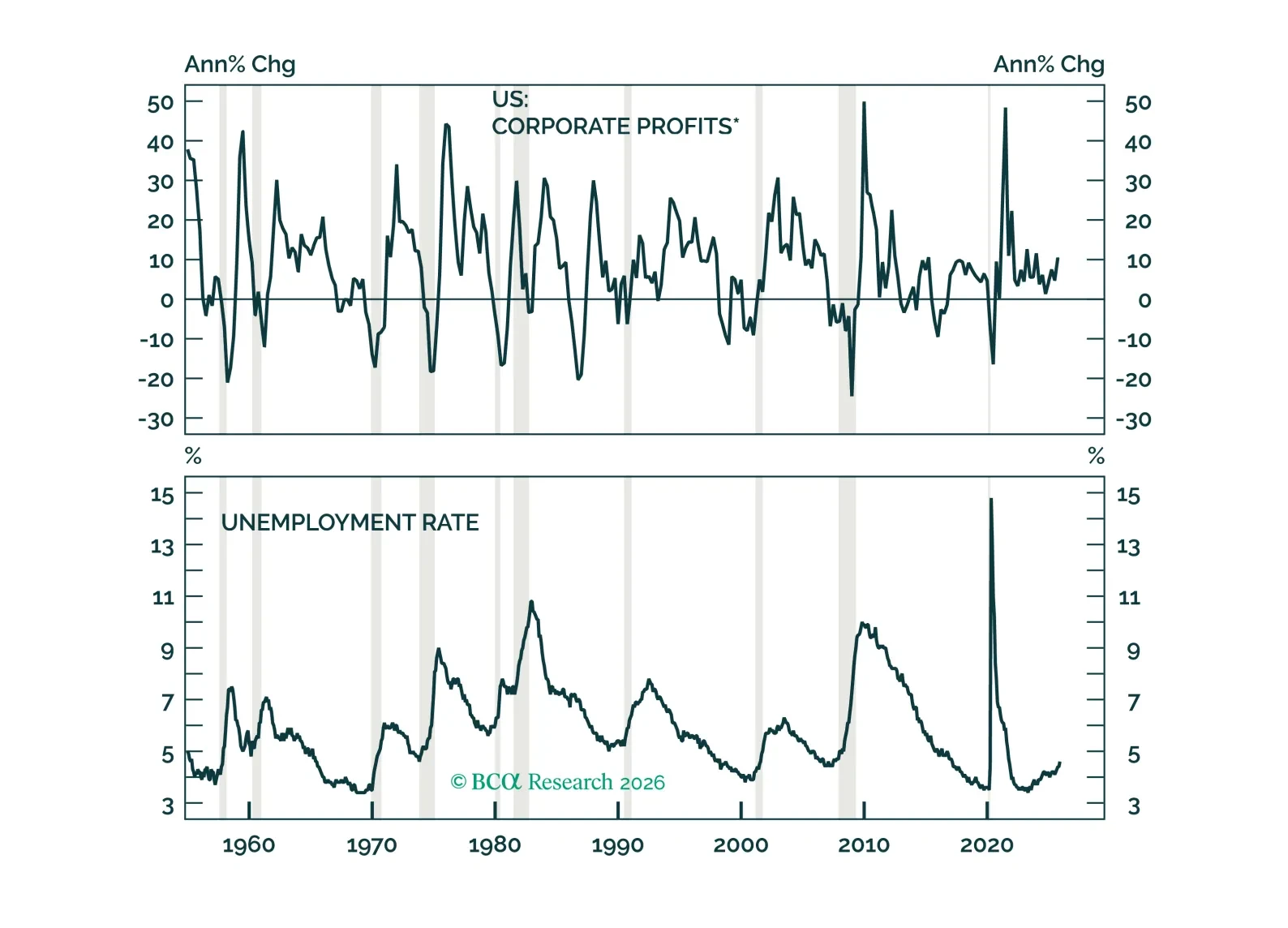

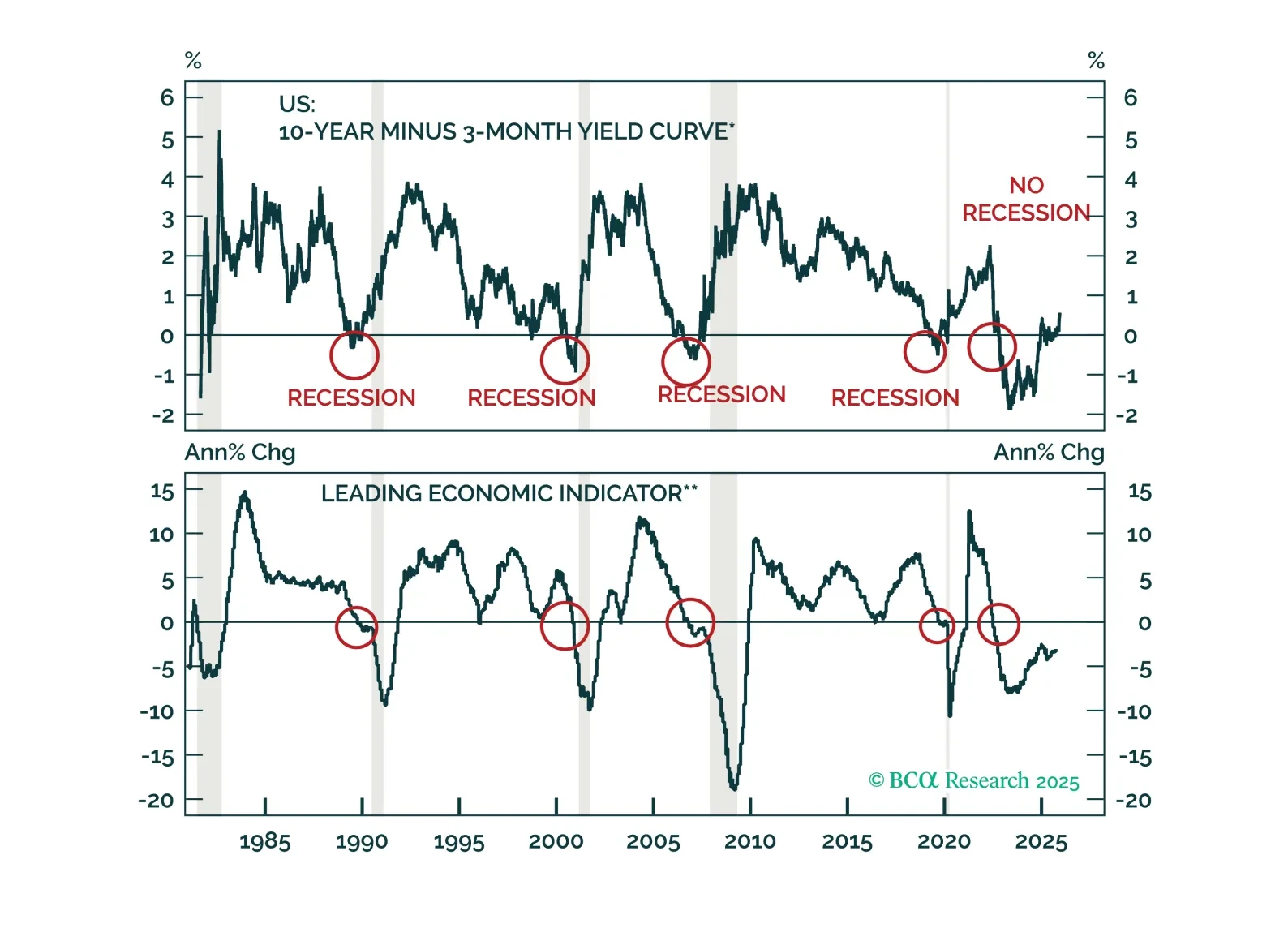

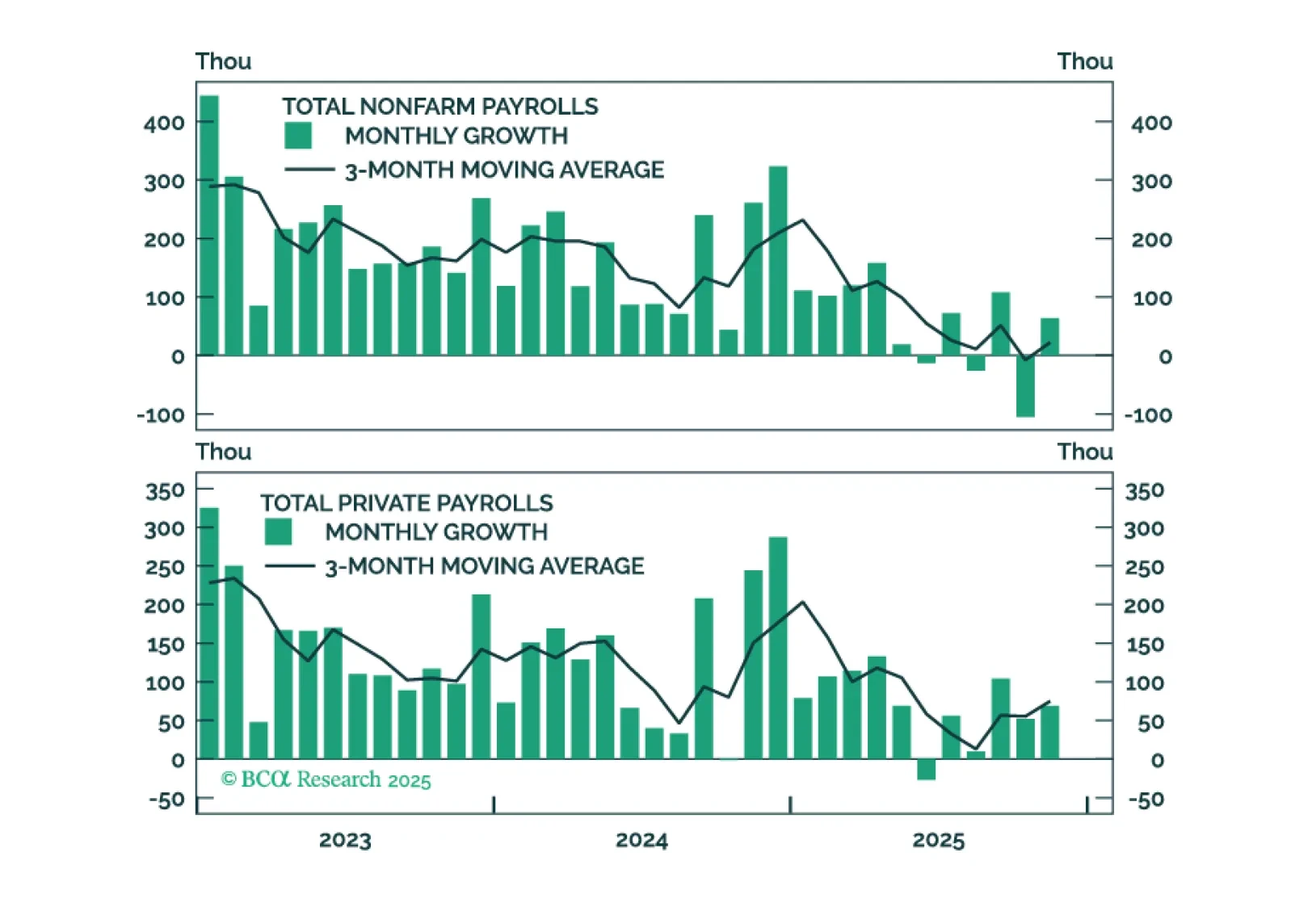

Employment Data Point To Dovish Policy Surprises In 2026

This year, we once again present our 2026 outlook as a retrospective from the future – a future in which the AI boom turned to bust.

Next week, please join me for a Webcast on Wednesday, December 17 at 10:30 AM EST (3:30 PM GMT, 4:30 PM CET) to discuss the economy and financial markets. We will also host a Webcast for APAC on Tuesday, December 16 at 8:00 PM EST (9:00 AM HKT+1 day).

And with that, I will sign off for the year. I wish you and your loved ones a very happy and healthy 2026. We will be back on Friday, January 2 with our MacroQuant Model Update.

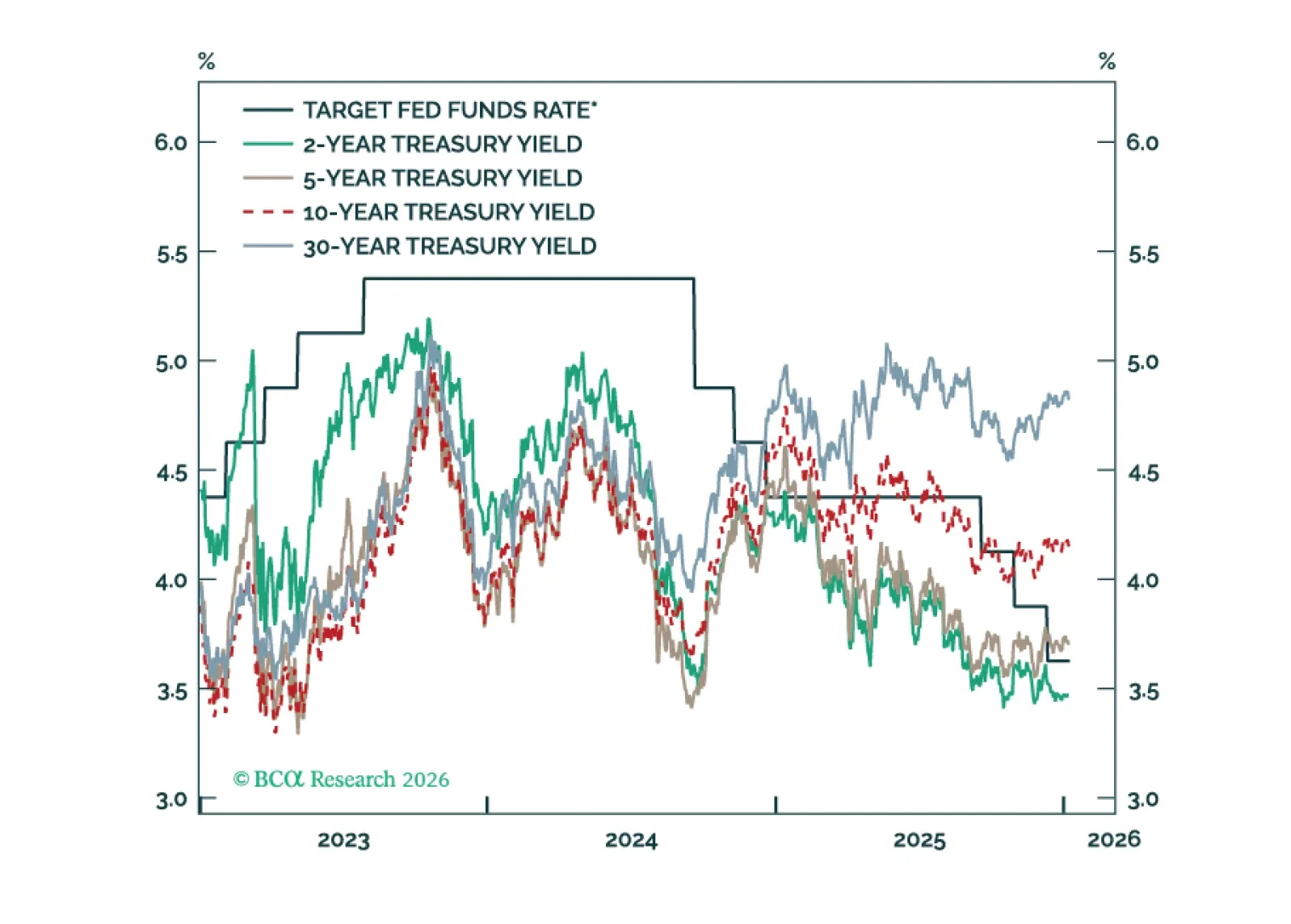

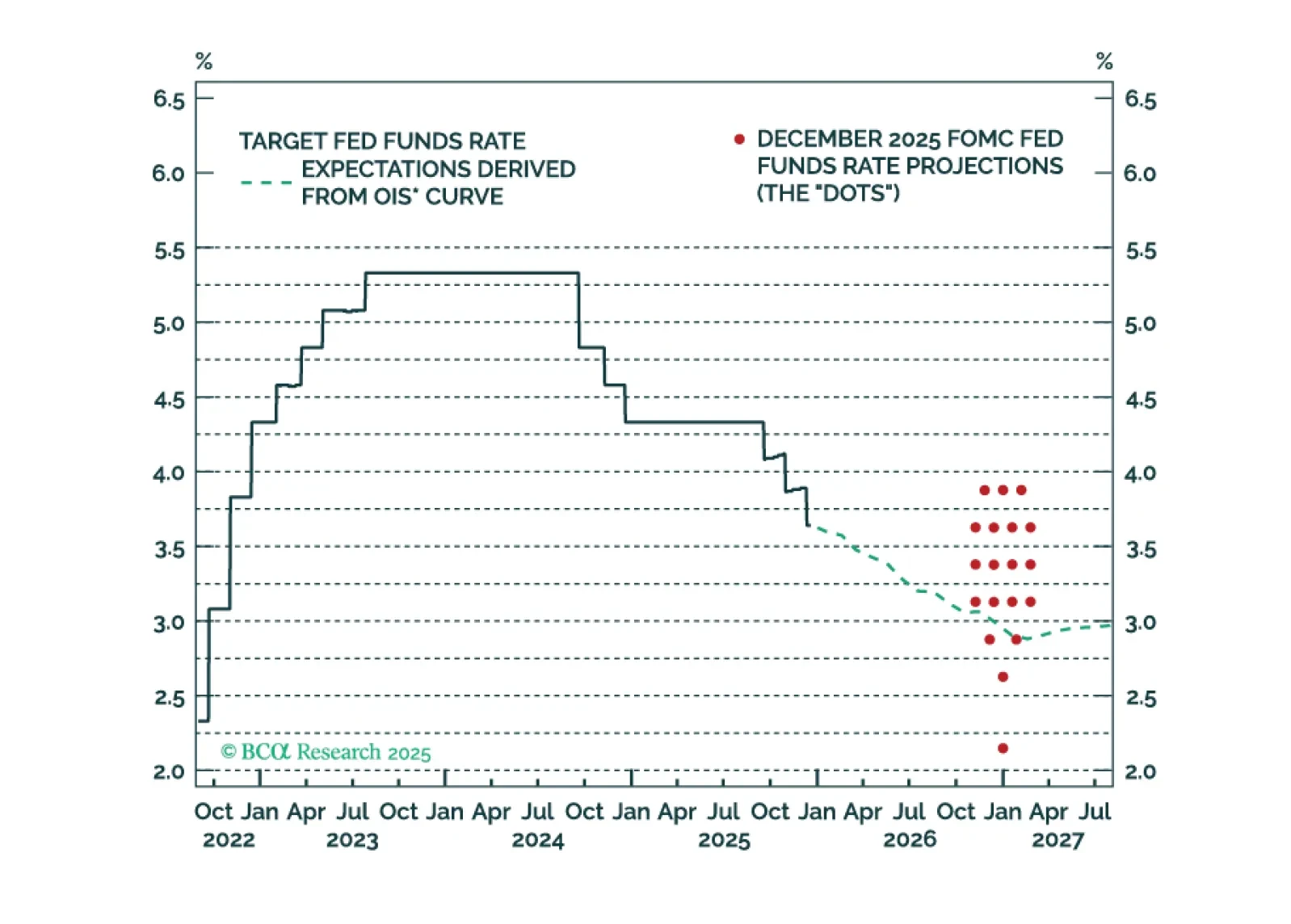

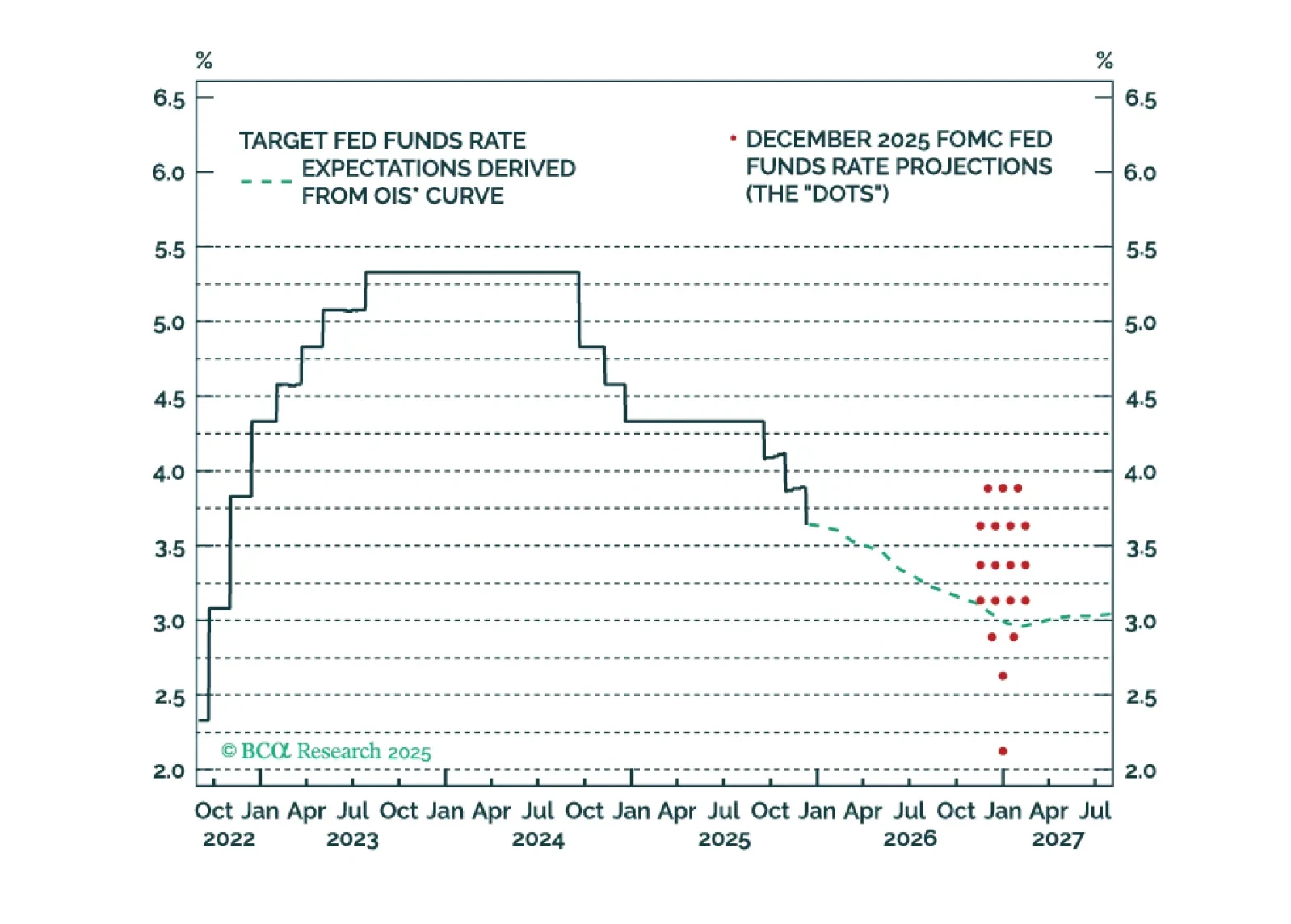

The Fed is on hold for now, but its 2026 economic projections are far too optimistic. The Fed will ease more next year than it currently anticipates.

Our 2026 Outlook presents our five key views for Europe’s macro landscape and markets in 2026 —a year poised to reveal the true strength of the recovery.