Economy

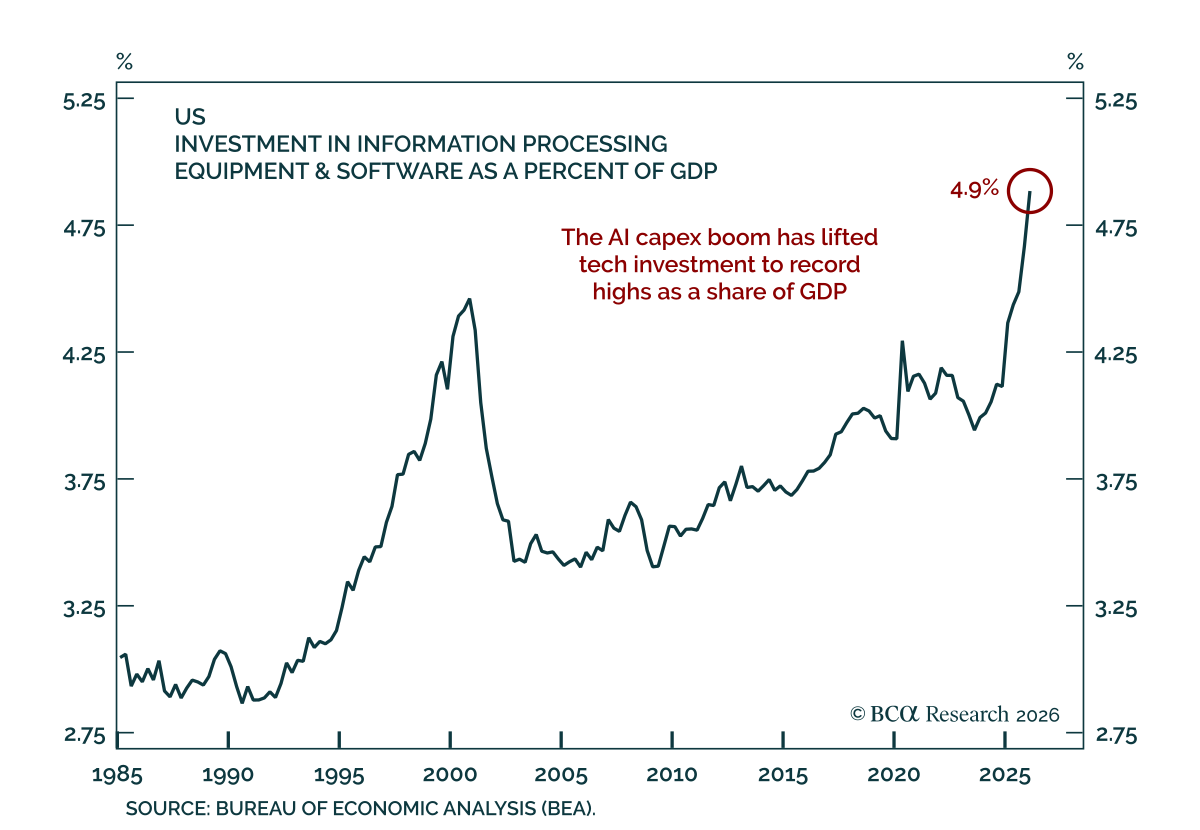

Our Global Investment strategists see the equity bull market entering its late stages and expect bonds to do well once growth slows. Lower oil prices and heavy AI capital spending should support the global economy through the rest of 2026, but our colleagues…

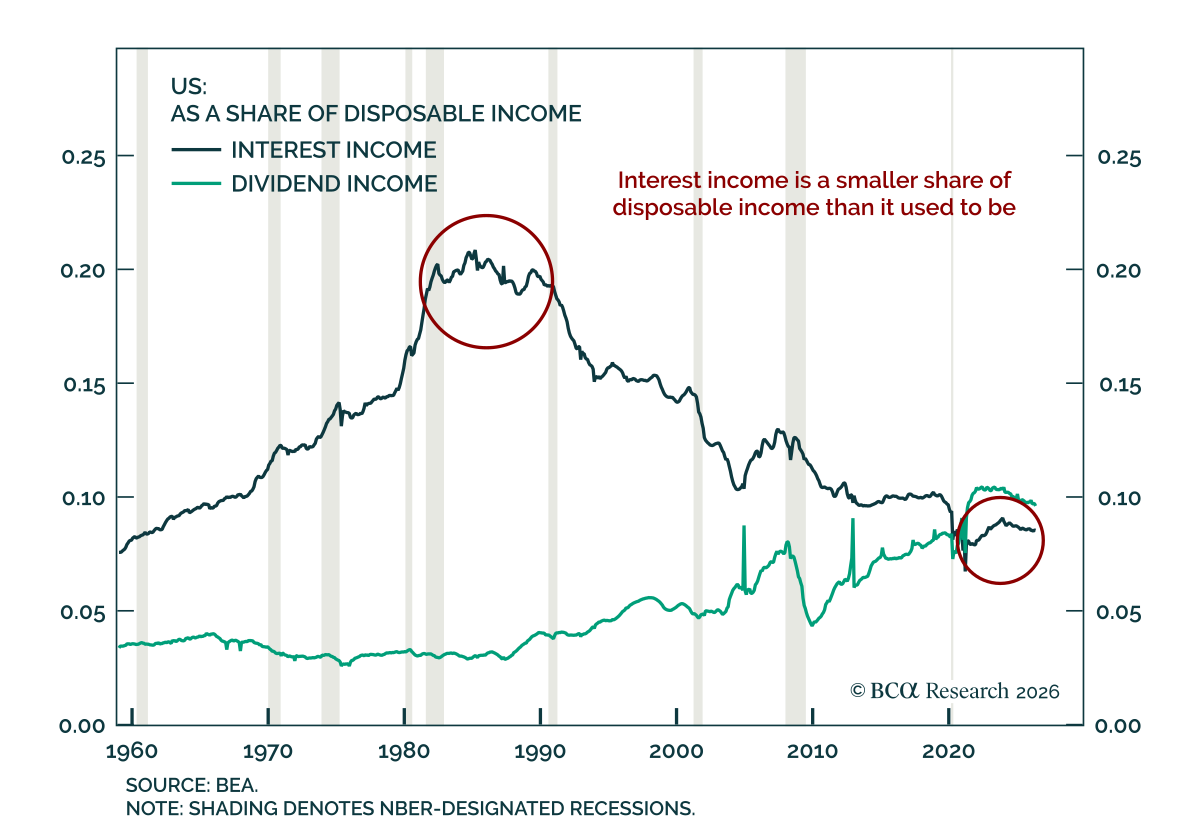

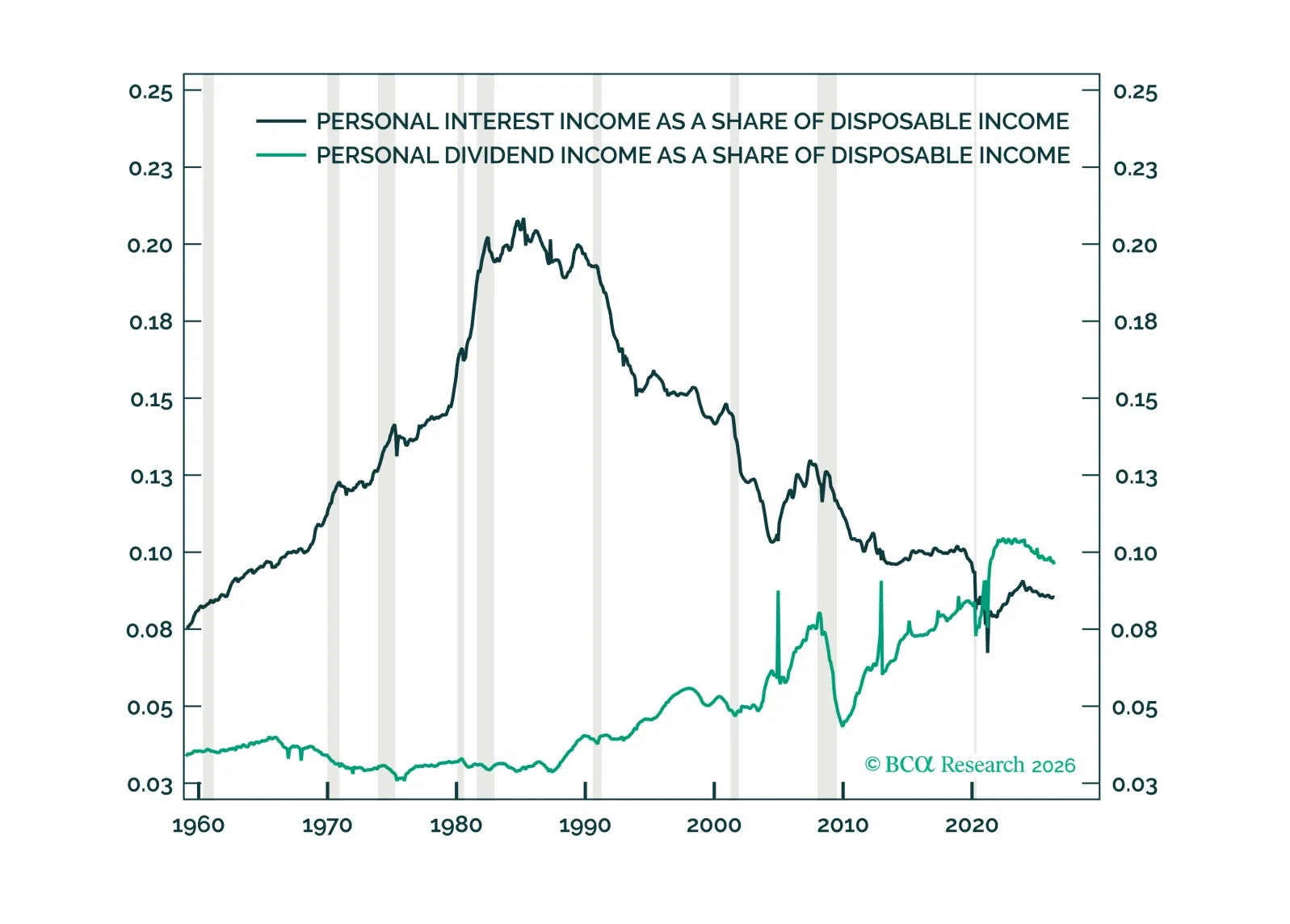

Our US Investment strategists argue that higher-than-expected interest rates are more likely to restrain consumption than support it. An idea gaining traction is that as rates rise, households collect more interest income and spend it, thus spurring…

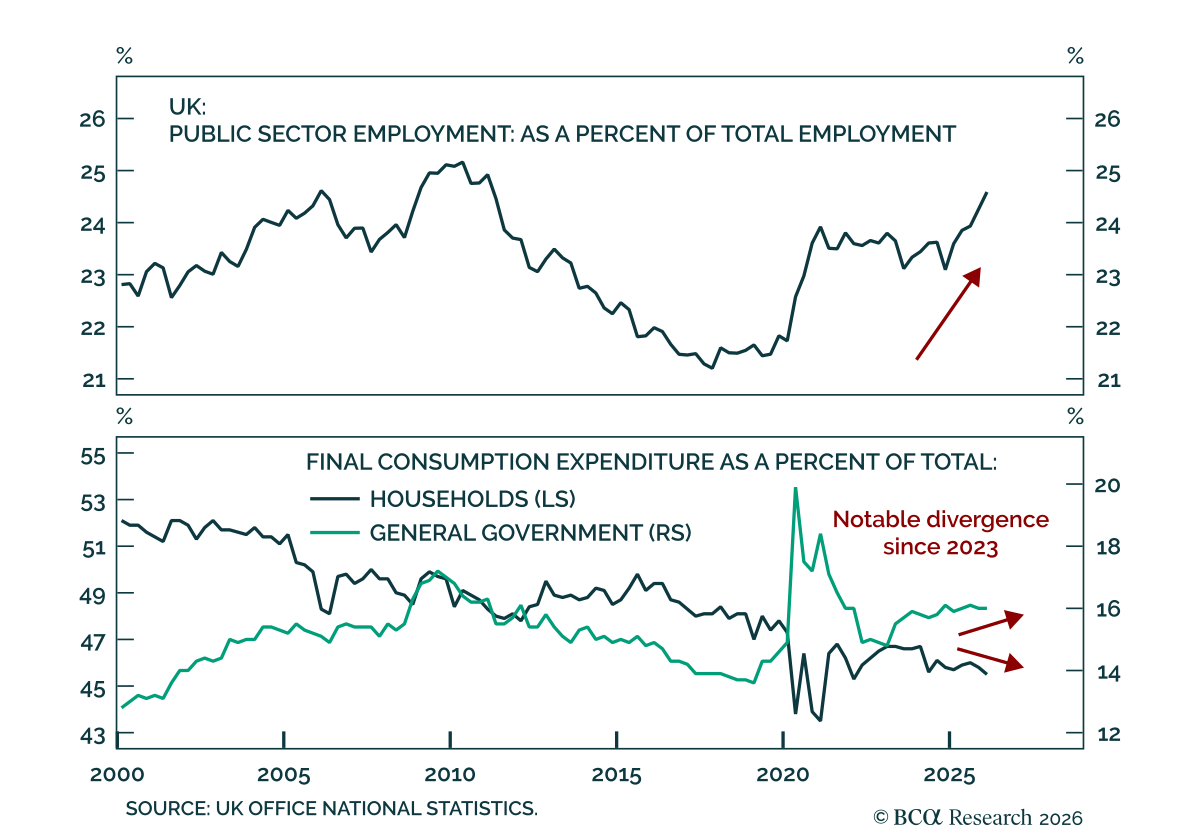

The UK economy entered the latest energy shock with recessionary signals already flashing red. While the rise in energy prices is unlikely to rival the 2022 crisis, it could still have a disproportionate impact on growth as the economy was already weak.…

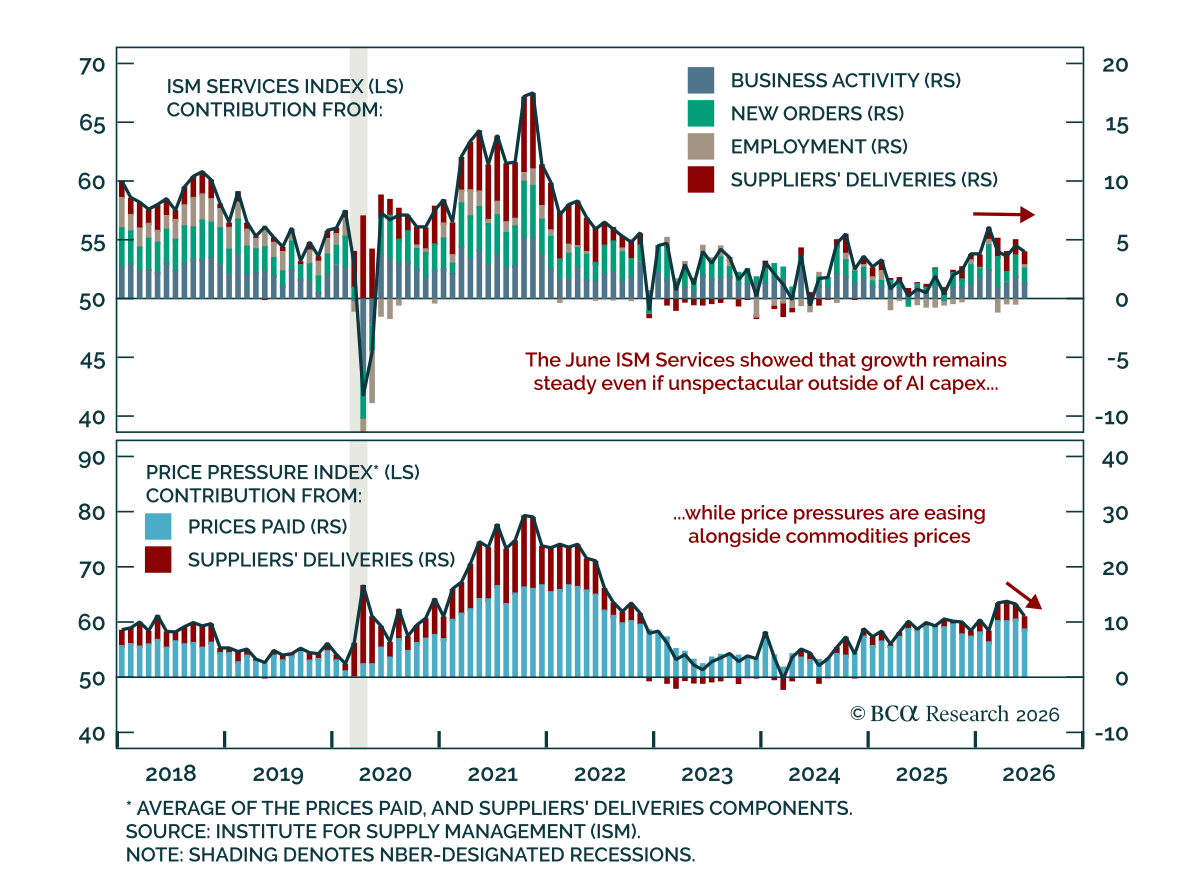

The June ISM Services survey was in line with consensus and reinforced the picture of a US economy that is neither overheating nor cooling significantly. The headline index ticked down to 54.0 from 54.5. The underlying picture was somewhat mixed, with new…

We are increasingly being asked if higher for longer interest rates could help spur consumption by boosting interest income. This report examines household income and balance sheet data to see if they might.

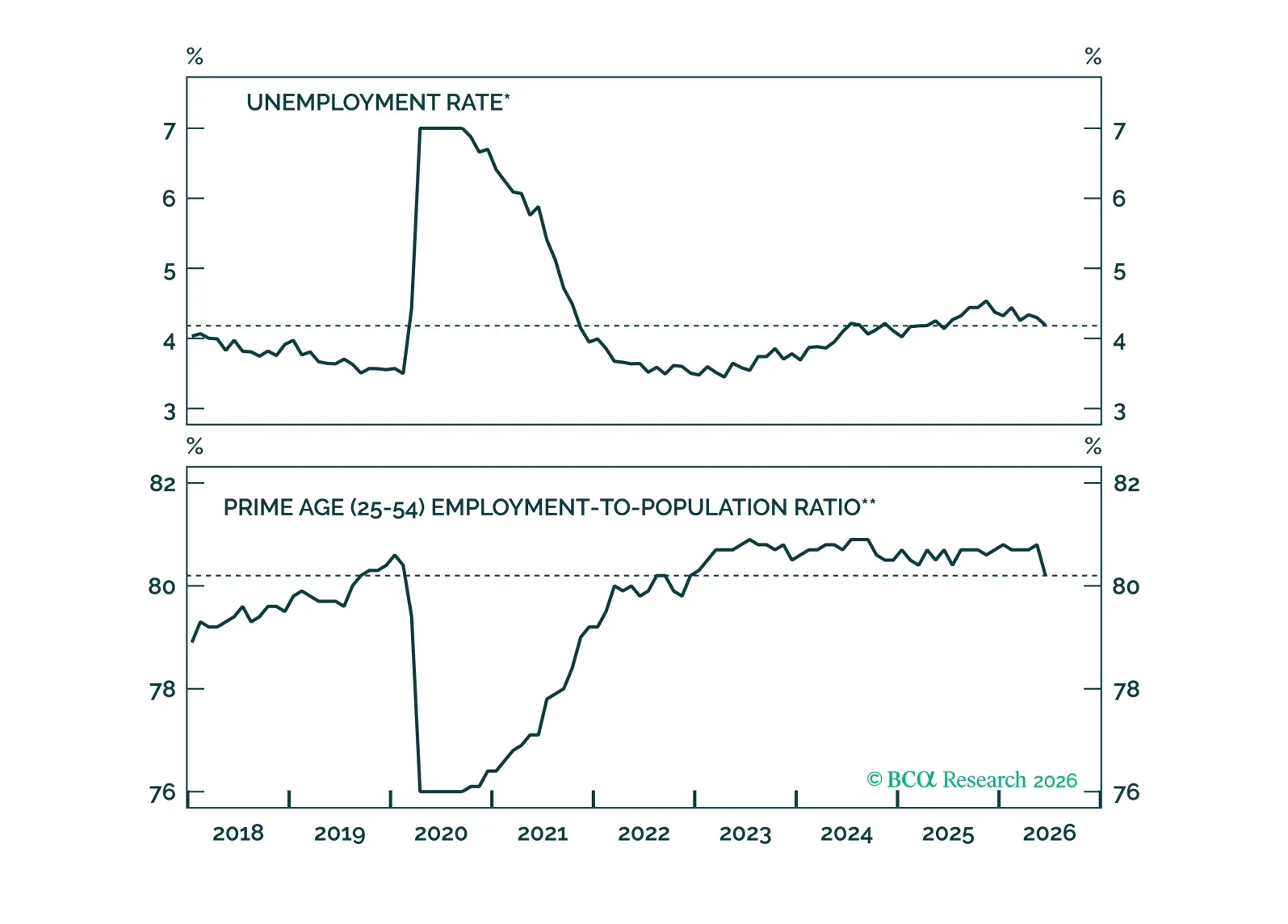

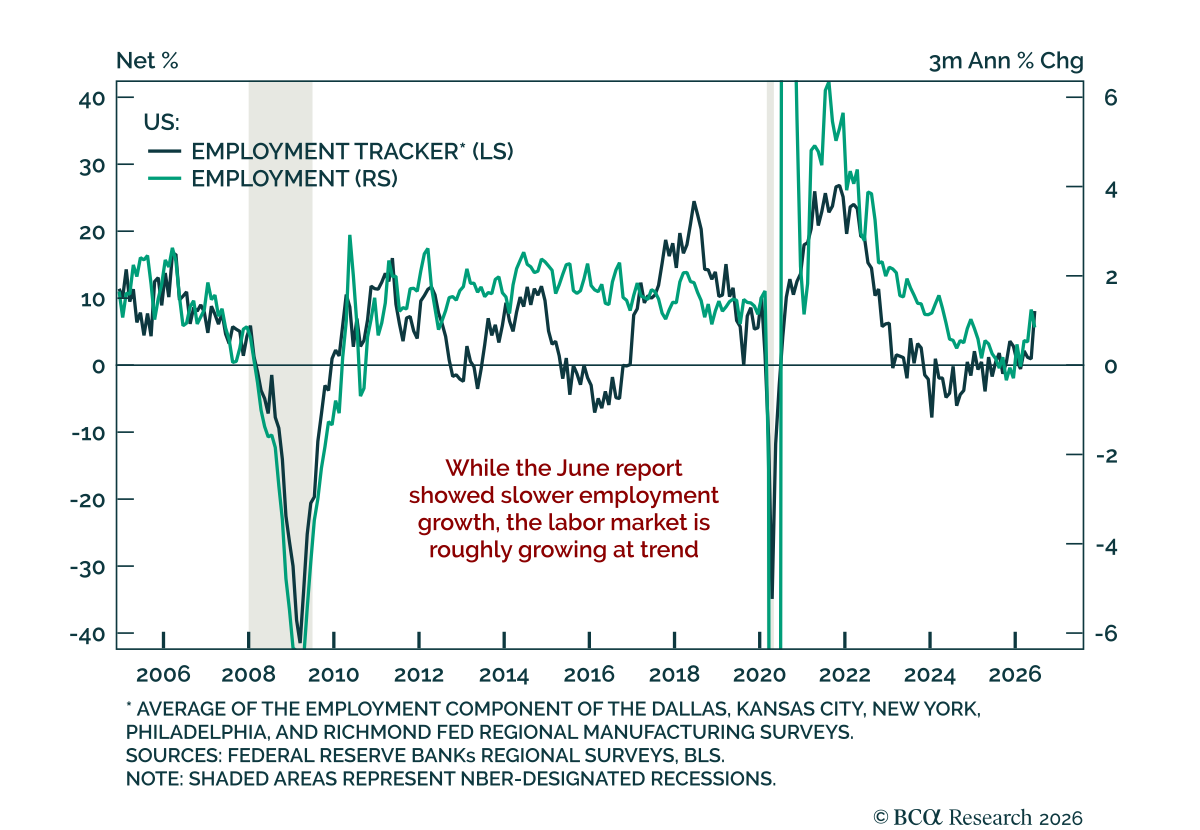

The June US employment report missed estimates, but still showed a labor market that remains healthy without overheating. Nonfarm payrolls rose by 57k, slowing from a downwardly revised 129k in May. Two-month revisions removed 74k jobs, leaving the 3-month…

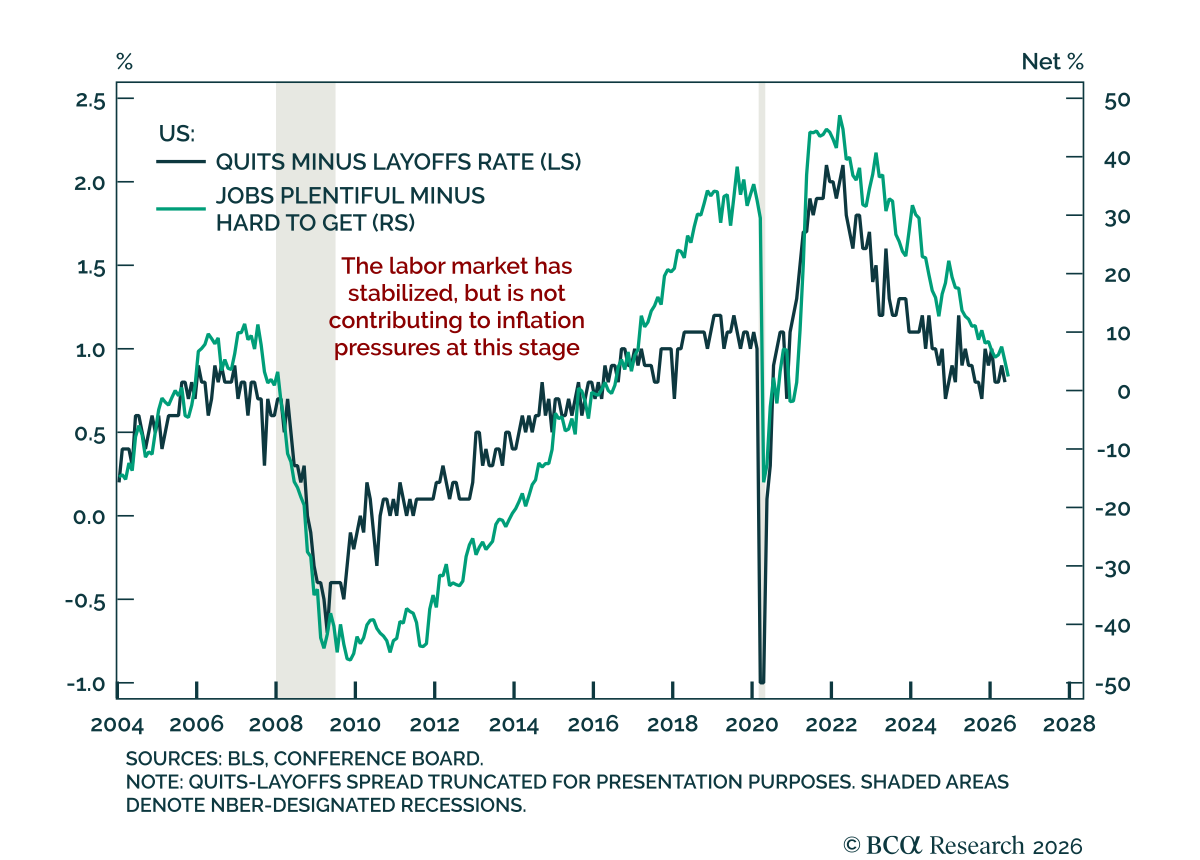

The June Conference Board survey sent a softer signal, but broader labor data still point to a stabilized job market and a supportive backdrop for risk assets. The Consumer Confidence Index missed estimates at 91.2. The index technically rose, as the previous…

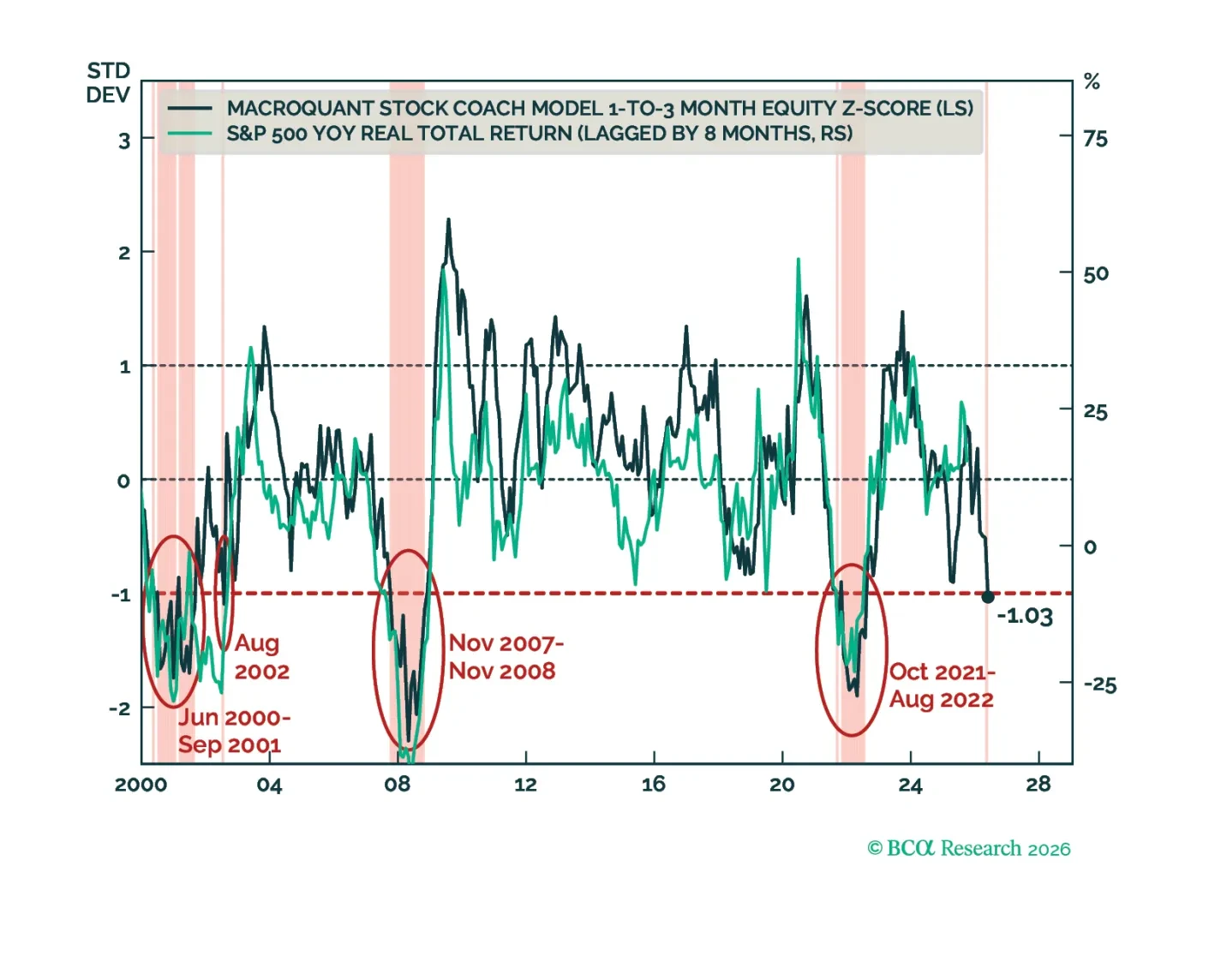

The equity bull market is getting long in the tooth. Bonds should perform well once economic growth begins to slow. The dollar will strengthen over the coming months before resuming its downtrend. While crude has likely found a near-term floor, we favor metals over energy in the long run.

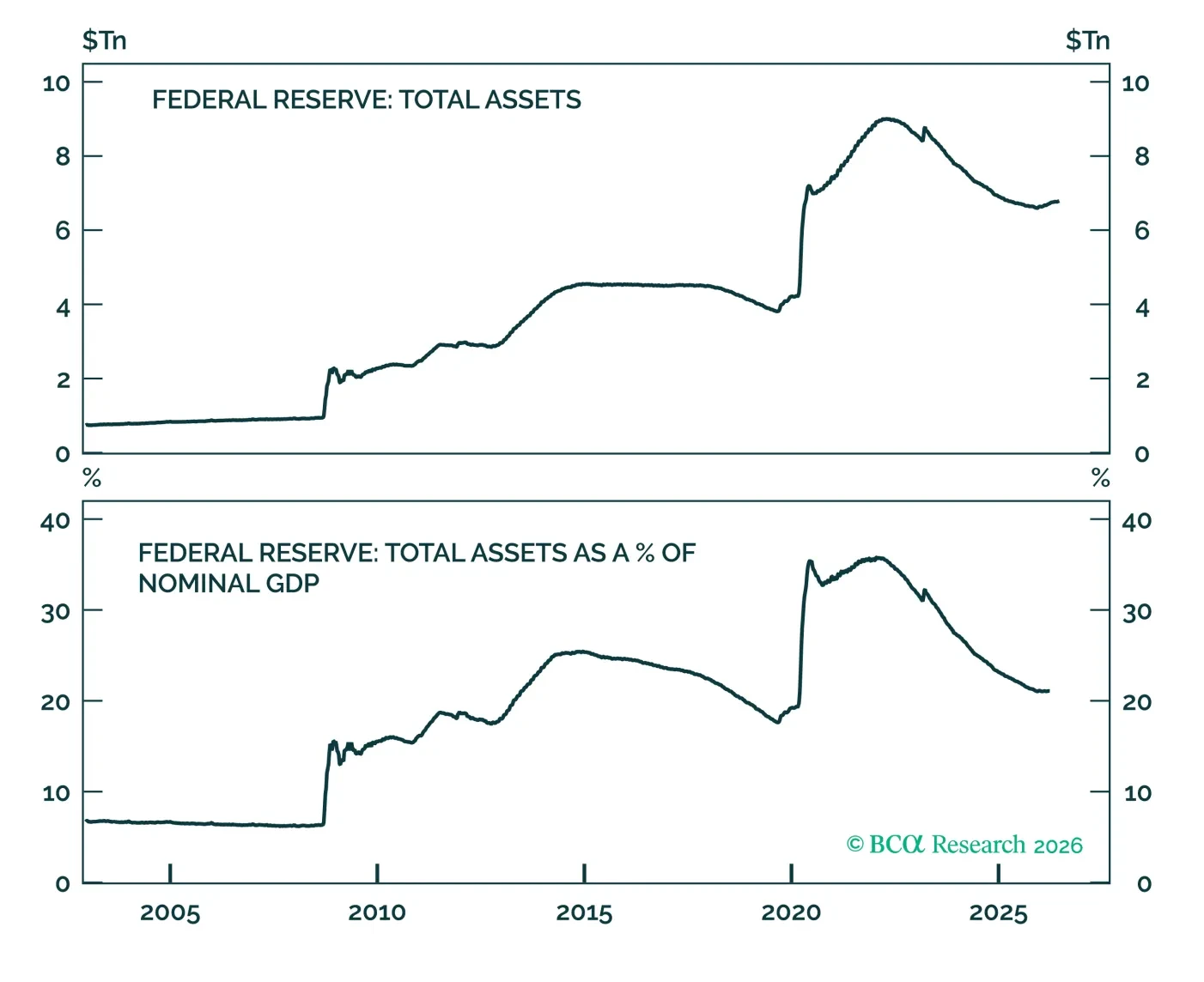

We discuss what recommendations to expect from the Fed’s balance sheet task force. We conclude that any future balance sheet consolidation will be smaller than many anticipate.