Economic Growth

The trajectory of China’s infrastructure investment in 2023H2 will be like what occurred in 2021H2. Growth will likely drop from the current nominal 10% to 0-2% in the next six months. China will continue promoting environmentally friendly infrastructure projects that may prevent a contraction in infrastructure investment in 2023H2.

The DXY will continue to have near-term upside, as economic growth holds up in the US, while it deteriorates in other parts of the world. Remain constructive on the DXY at current levels, but pivot to a short position on evidence US growth is boosting the rest of the world.

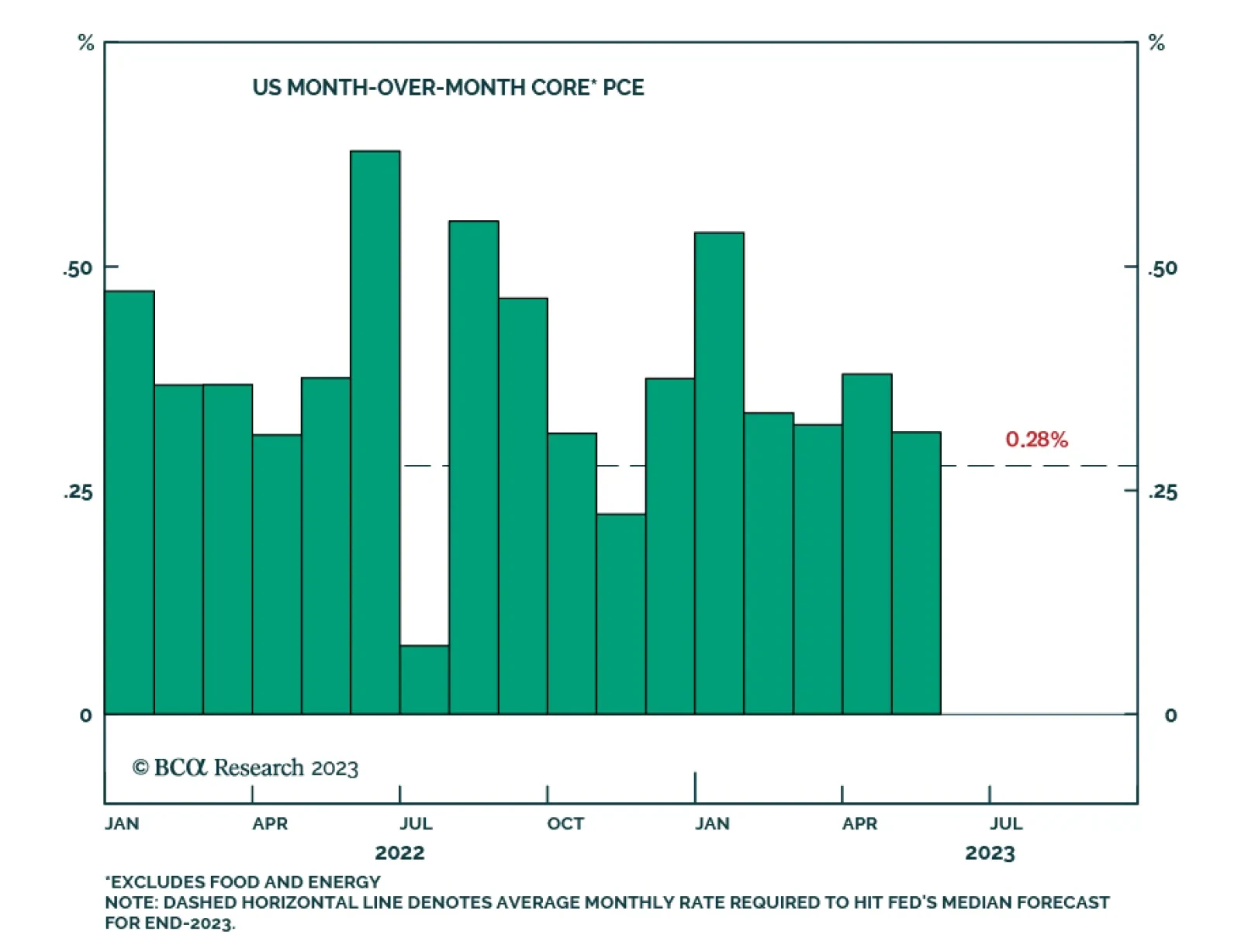

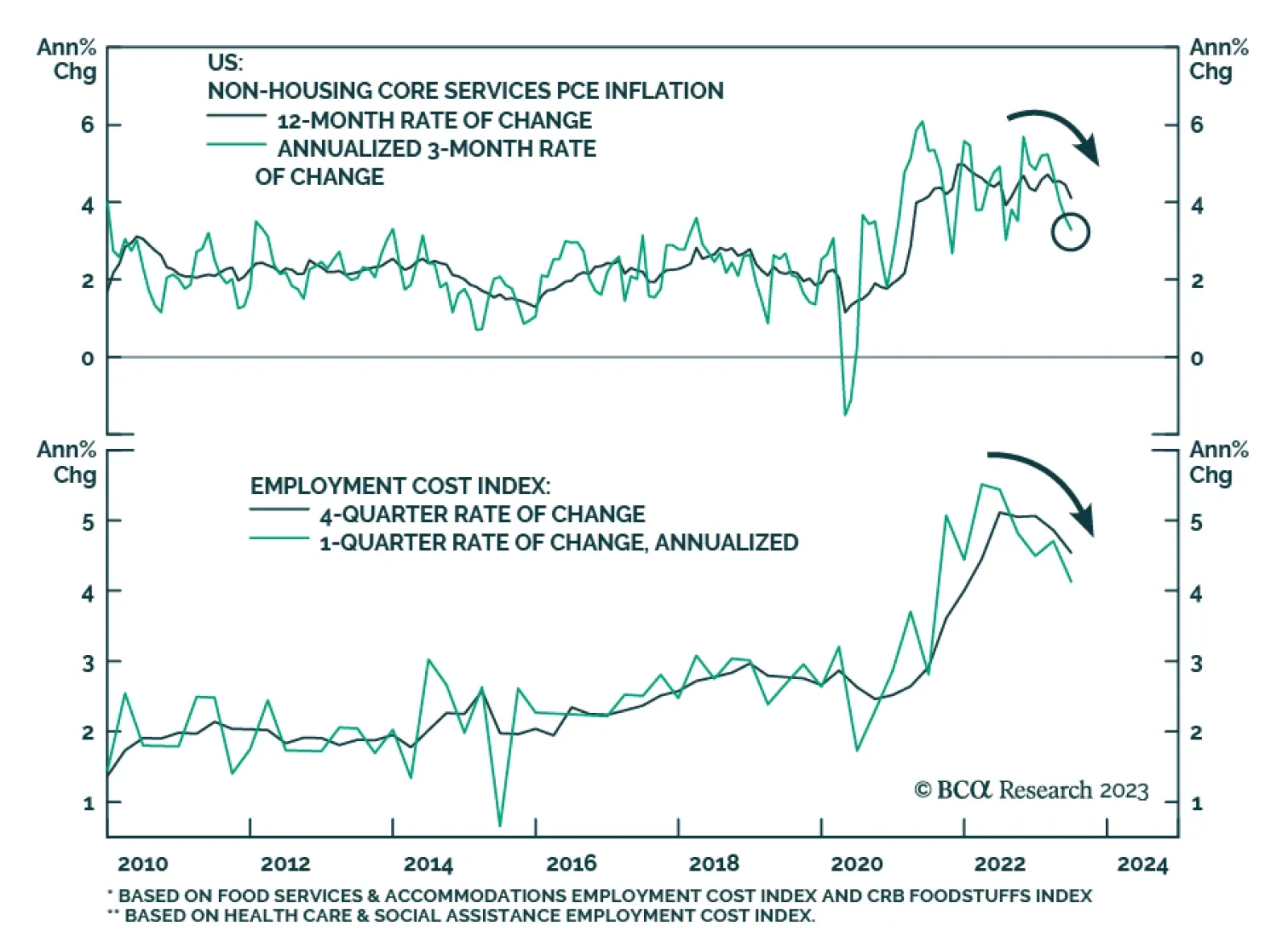

The US is not out of the woods when it comes to inflation, which means that it is too early to conclude that the Fed can stop raising rates. Any further increase in inflation risk would prompt us to turn more cautious on stocks.

A look at recent US data on economic growth and inflation, with an update on the implications for monetary policy and bond yields.