Economic Growth

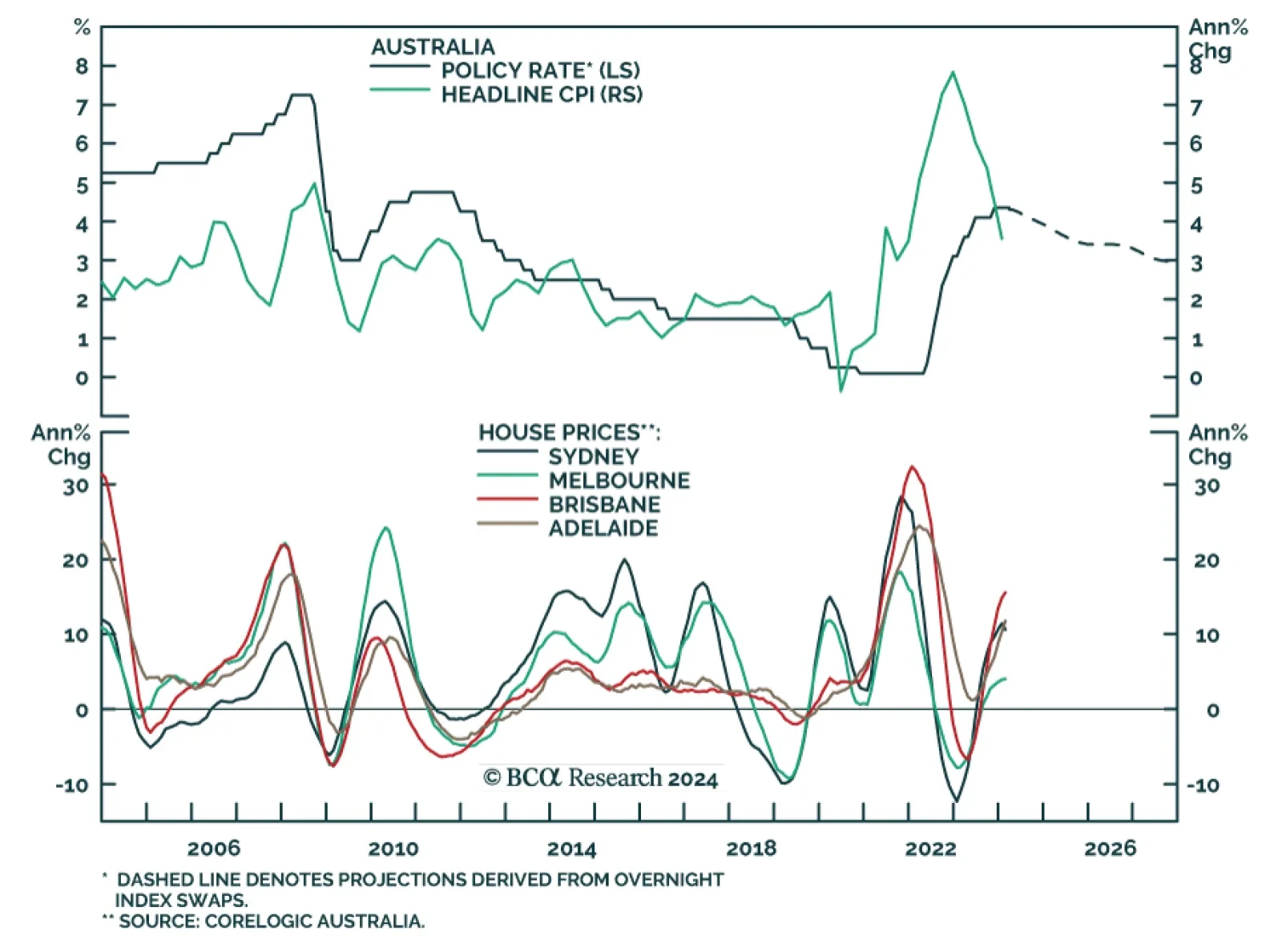

Australia's Macro Environment Validates Long AUD Position…

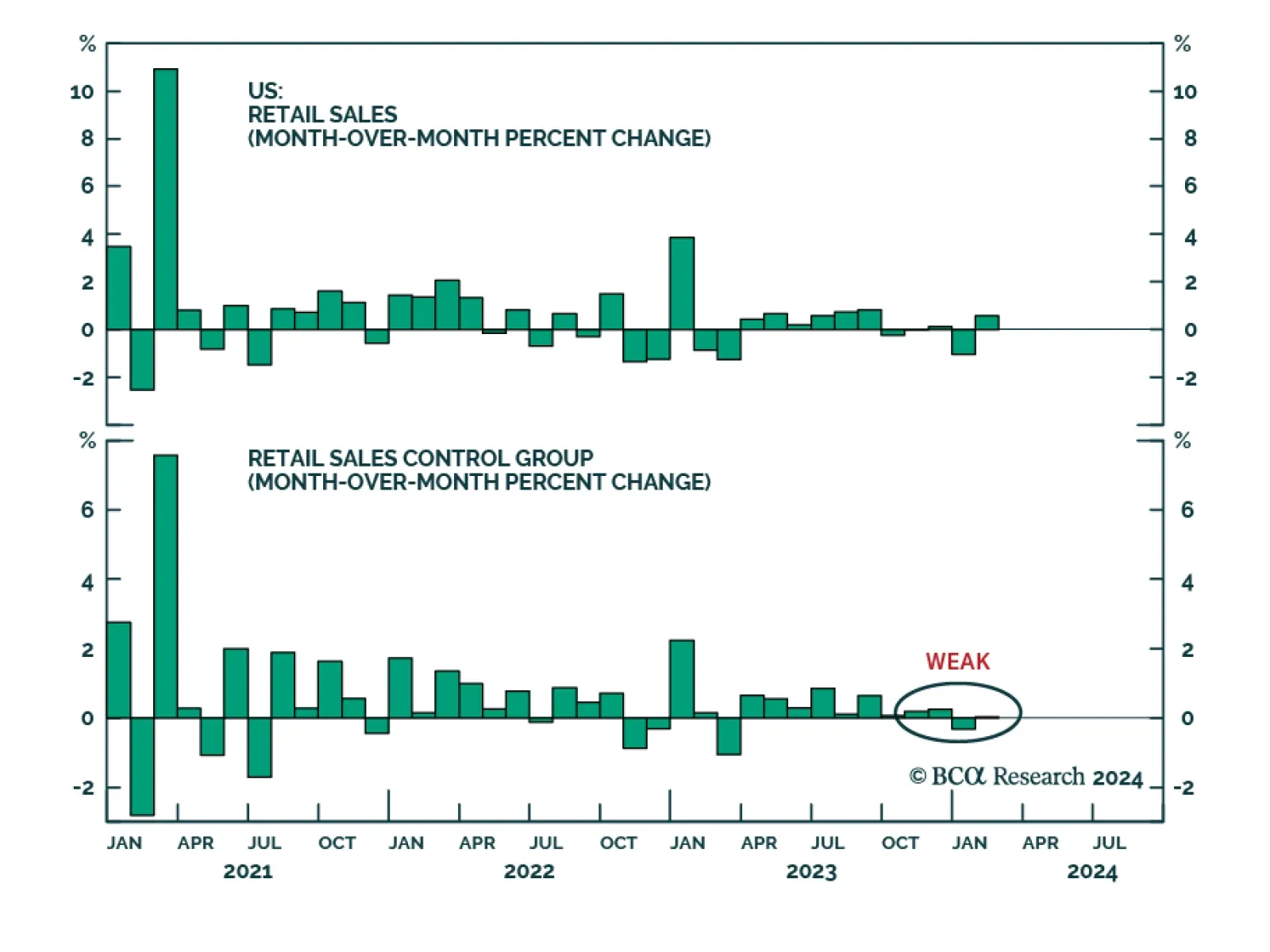

US: Retail Sales Disappointment Consistent With Weaker Household Sentiment…

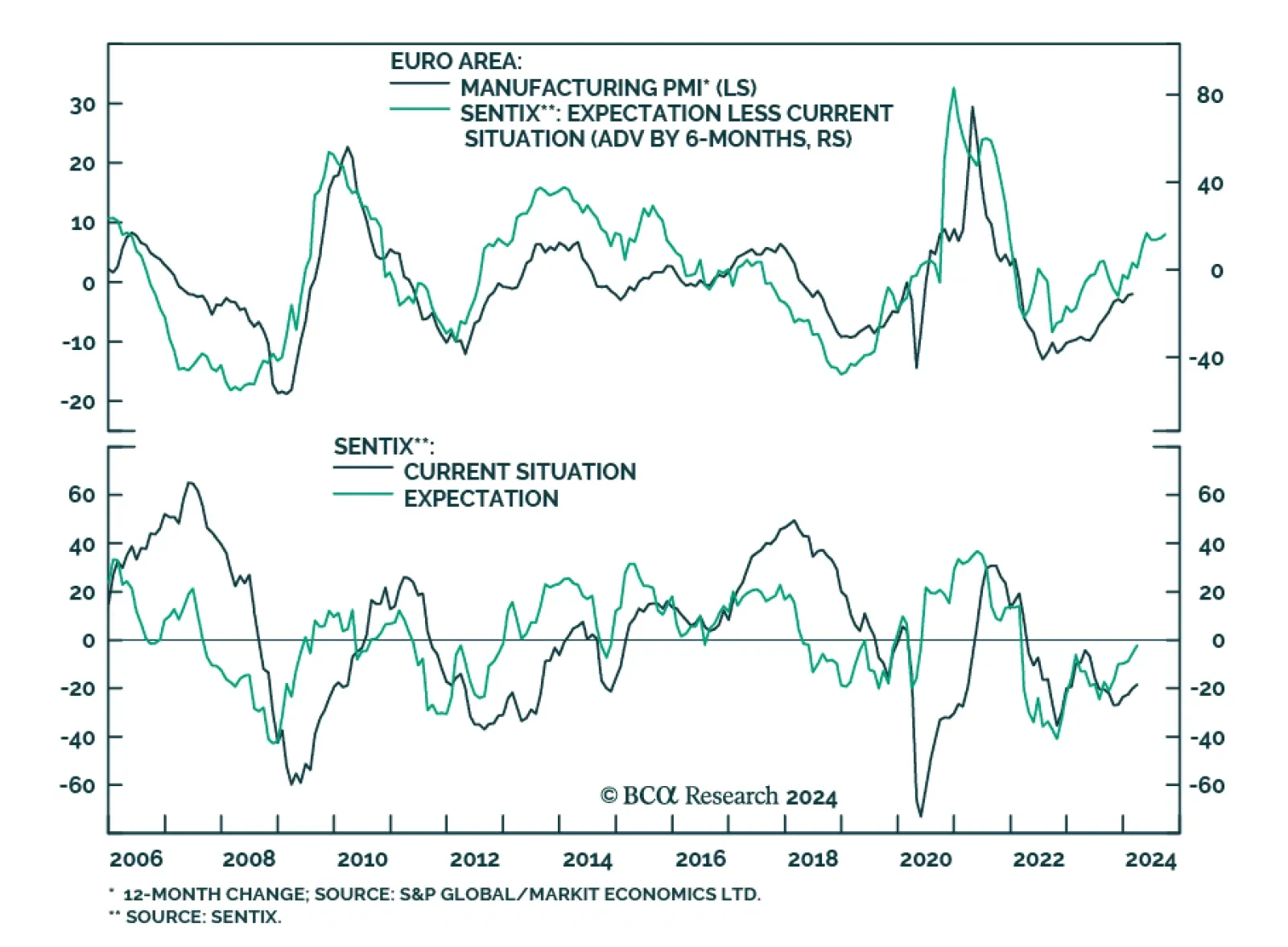

Sentix Signals Improved Eurozone Growth Prospects…

On The Timing Of The US Recession…

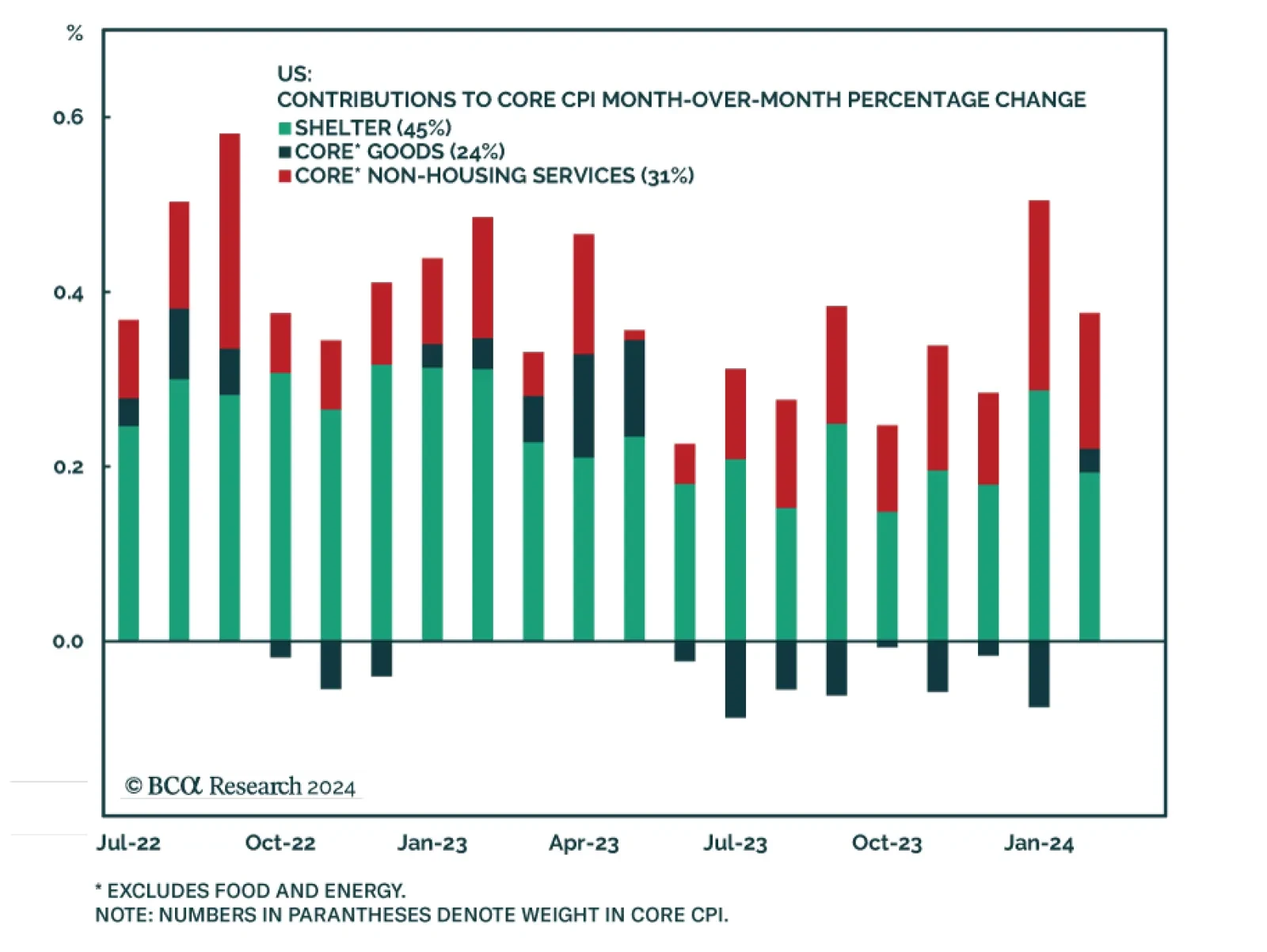

Another Hotter-Than-Anticipated US Inflation Report…

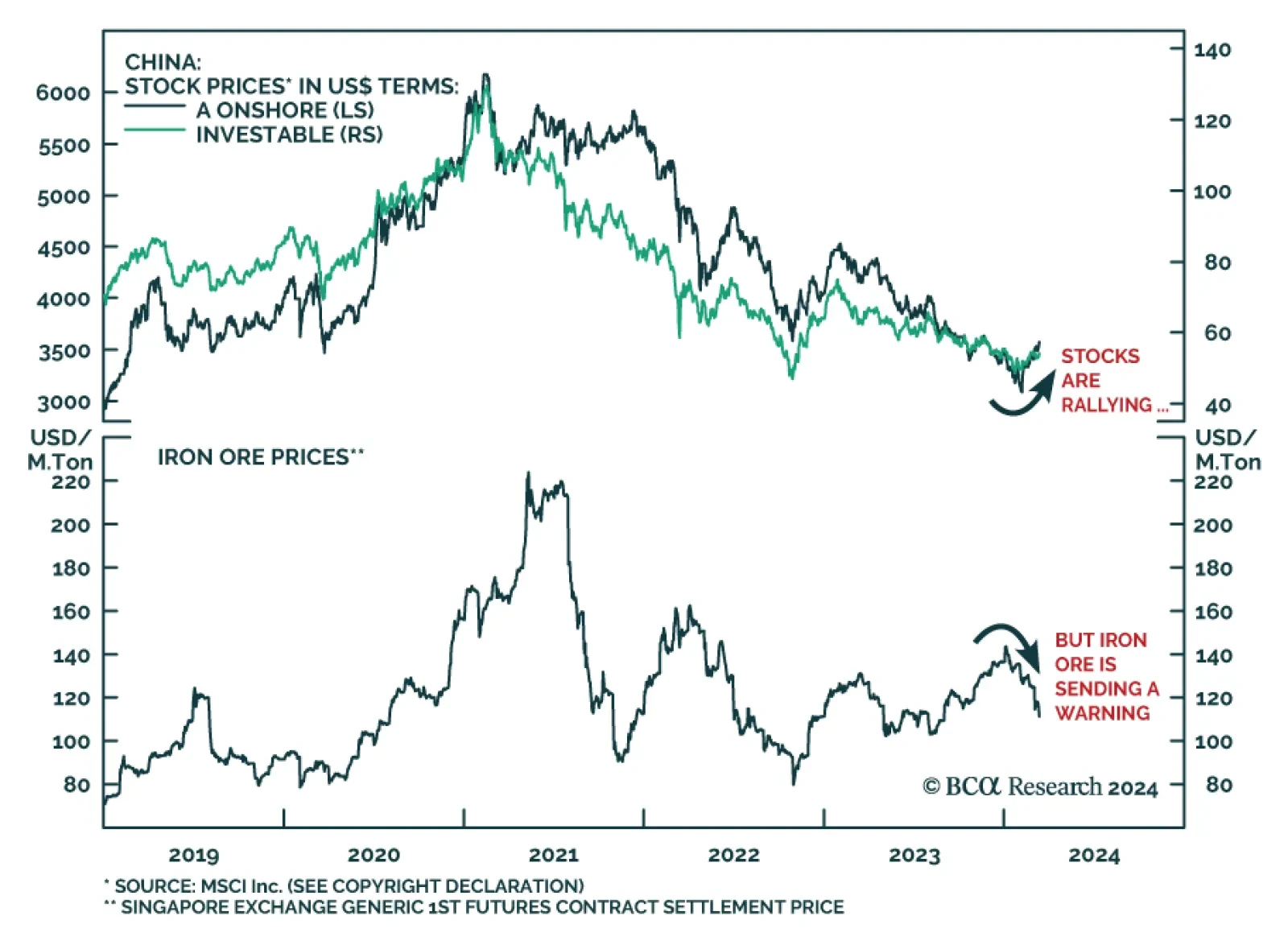

Chinese Equities: A Sustainable Rally Or A False Start…

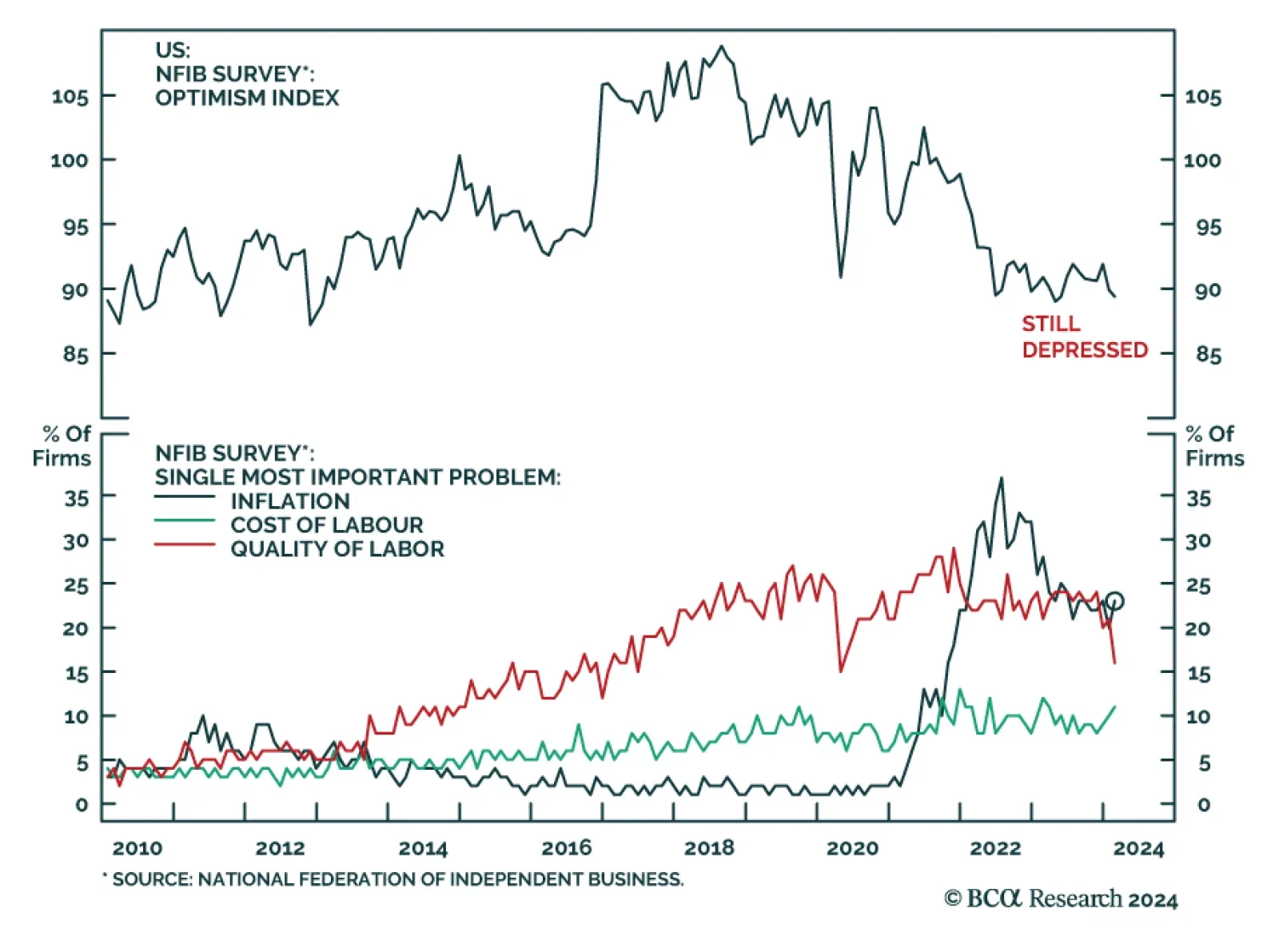

Inflation Is Once Again Top Problem For Small Business Owners…

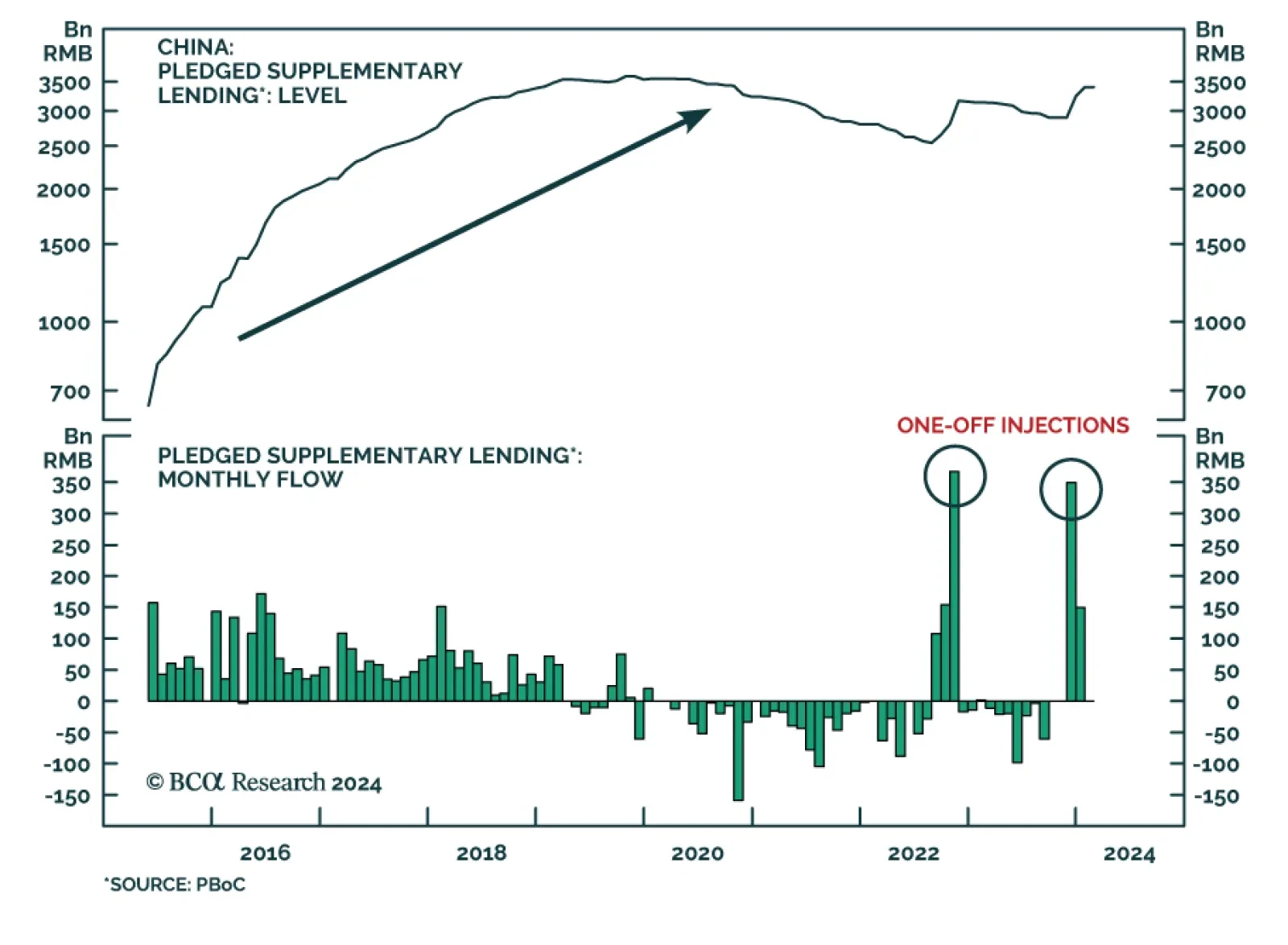

China's Cyclical Outlook: What Would It Take To Become More Positive…

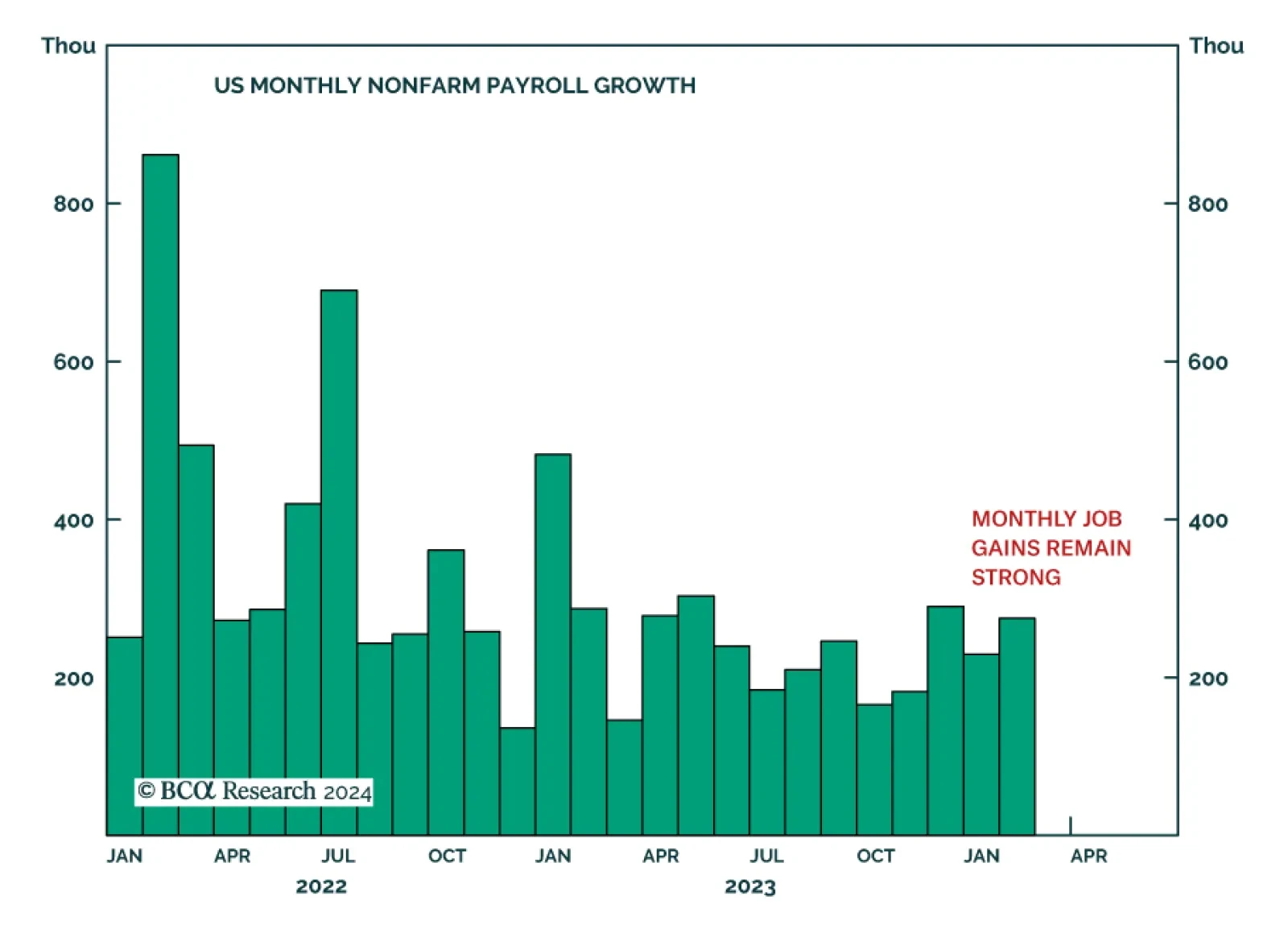

US Unemployment Rate Climbs To 2-Year High…

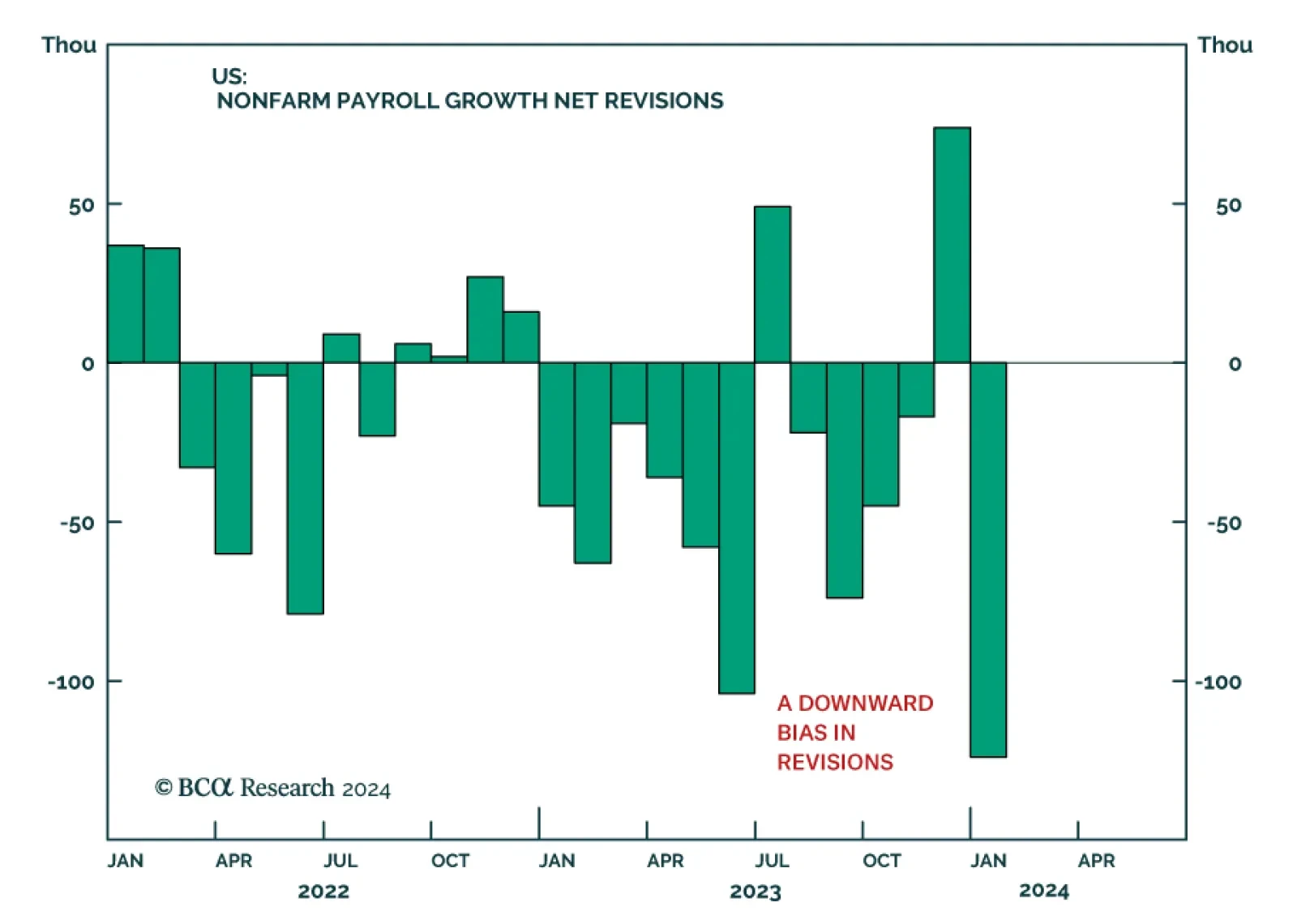

A Downward Bias In US Nonfarm Payroll Revisions…