Economic Growth

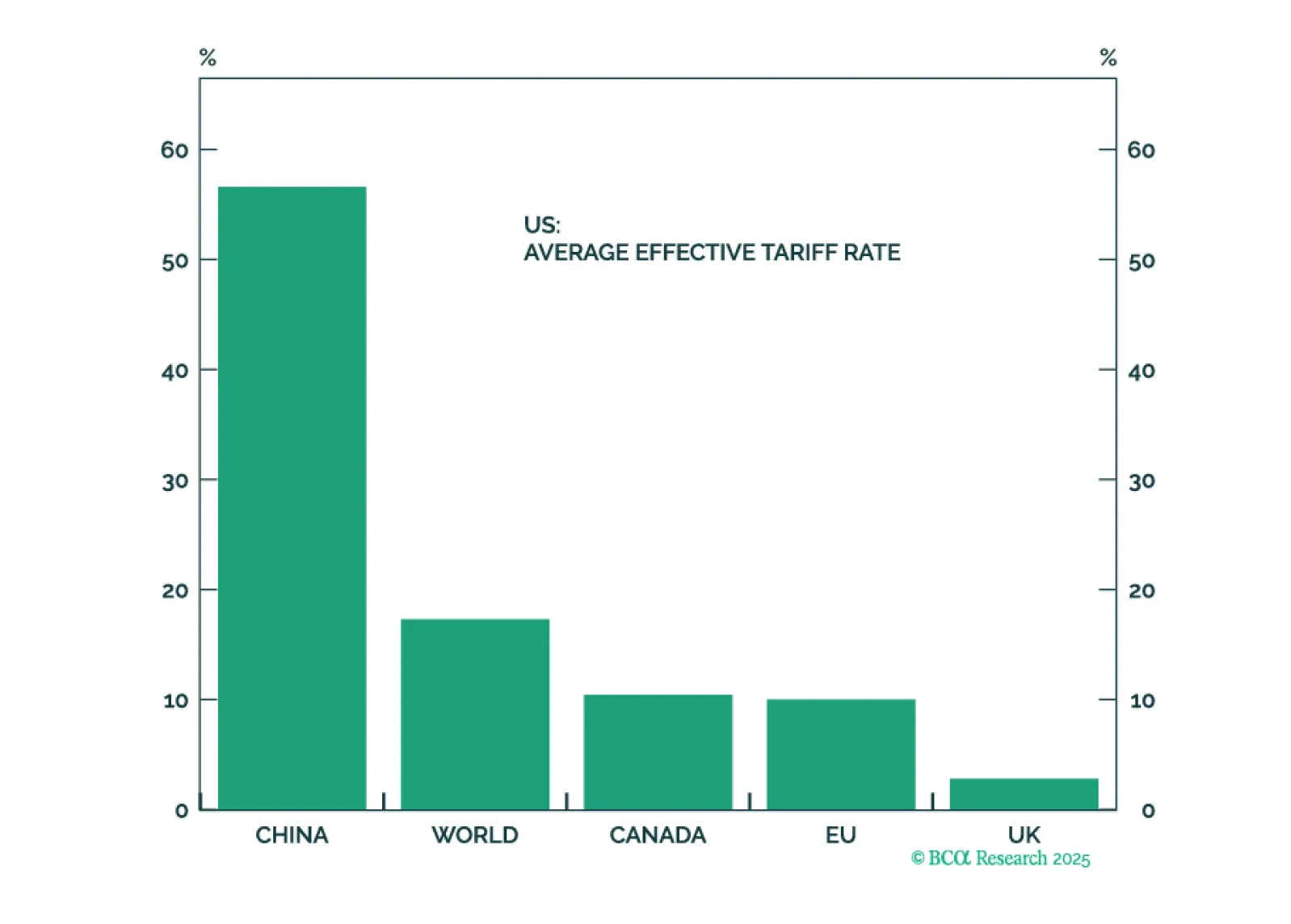

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

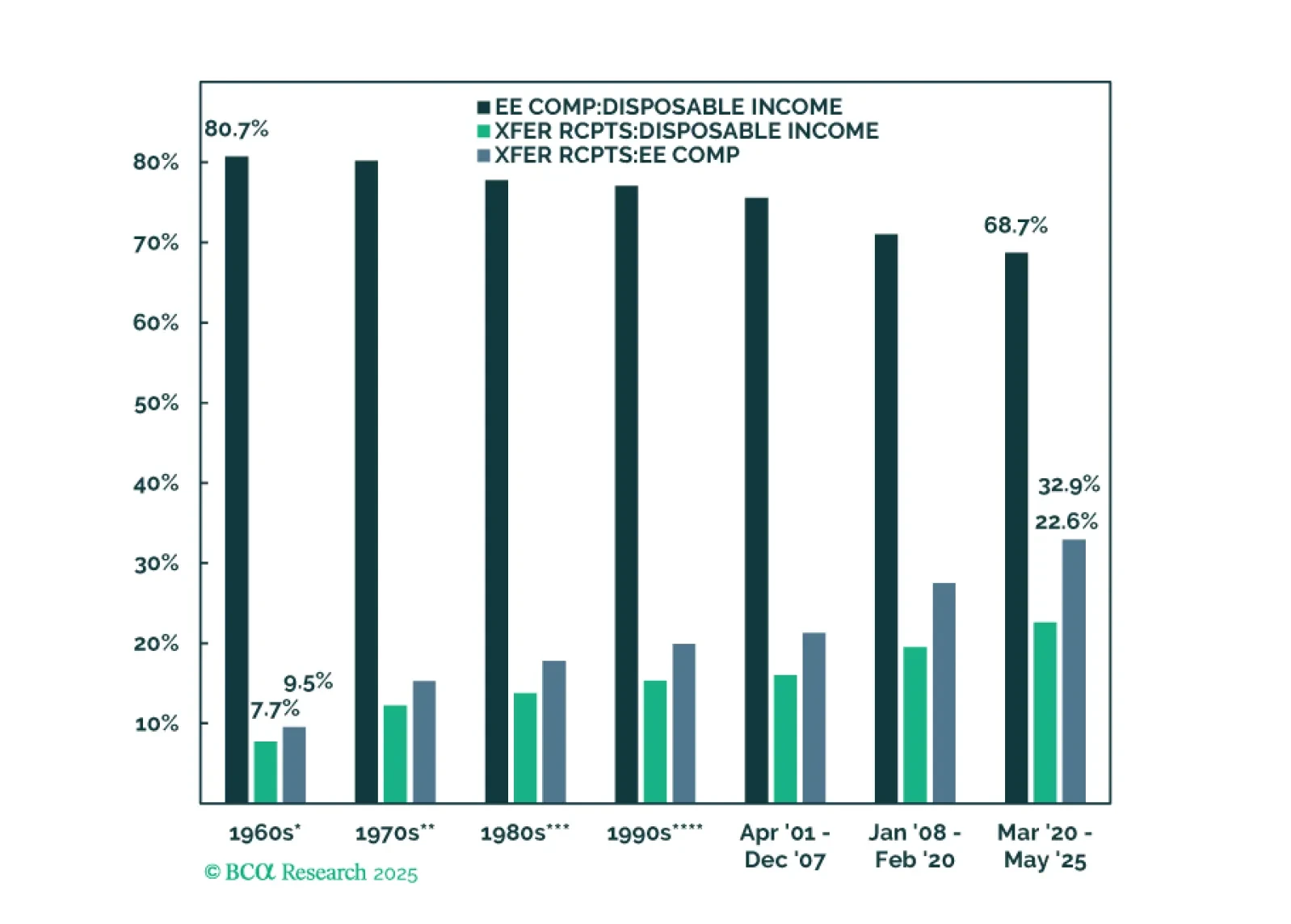

Our Special Report is a graphical comparison of the consumer’s position in the current cycle to every cycle from 1960 forward. The bad news is that disposable income is increasingly reliant on government transfers and the labor market is softening. The good news is that the balance sheets of households in the lower half of the wealth distribution have improved a lot.

Provided that humanity can overcome the existential risks posed by AI, real incomes will rise. Although most workers will ultimately gain from the transition to an AI-dominated economy, the biggest winners will be those who control the land and the natural resources beneath it.

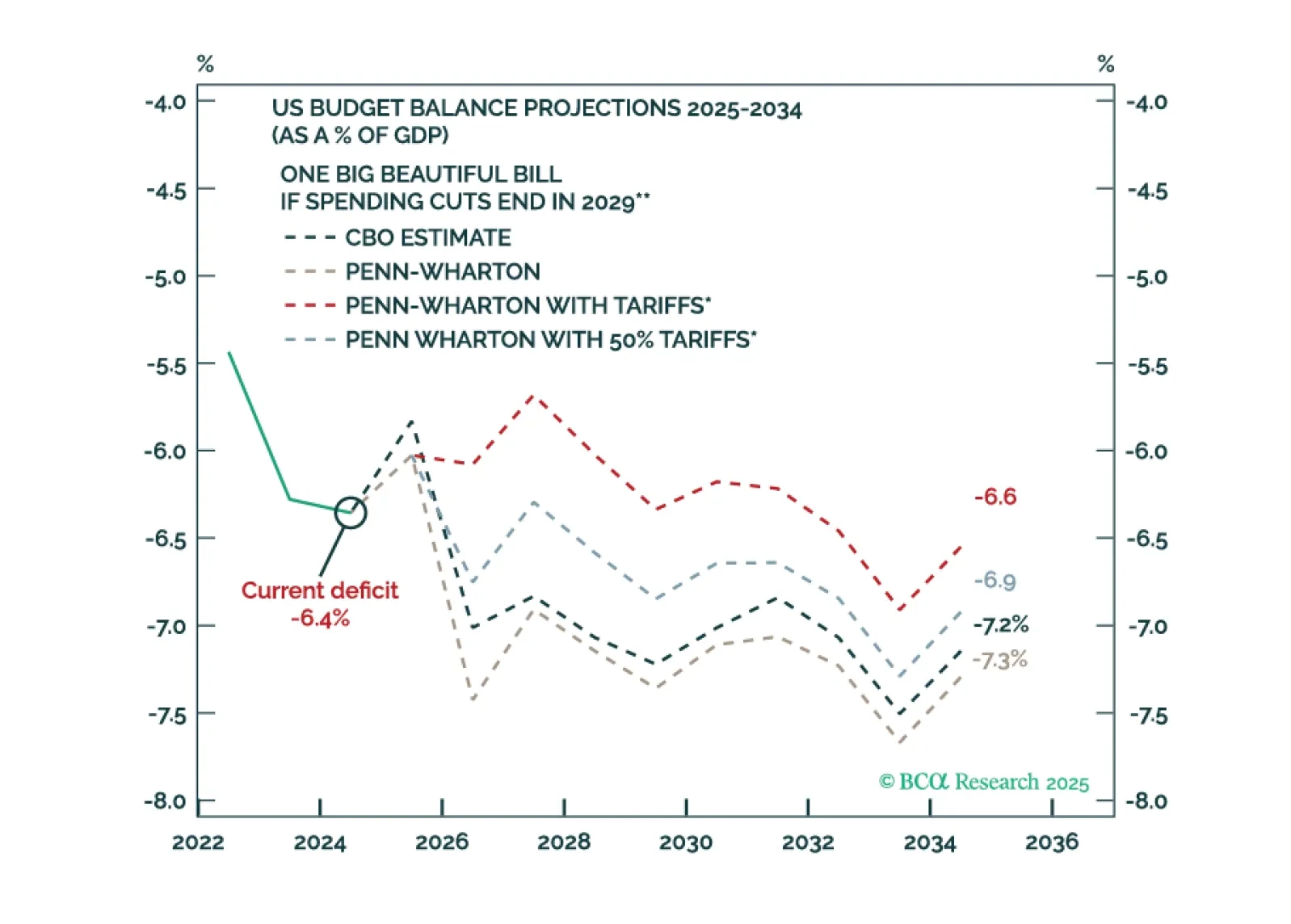

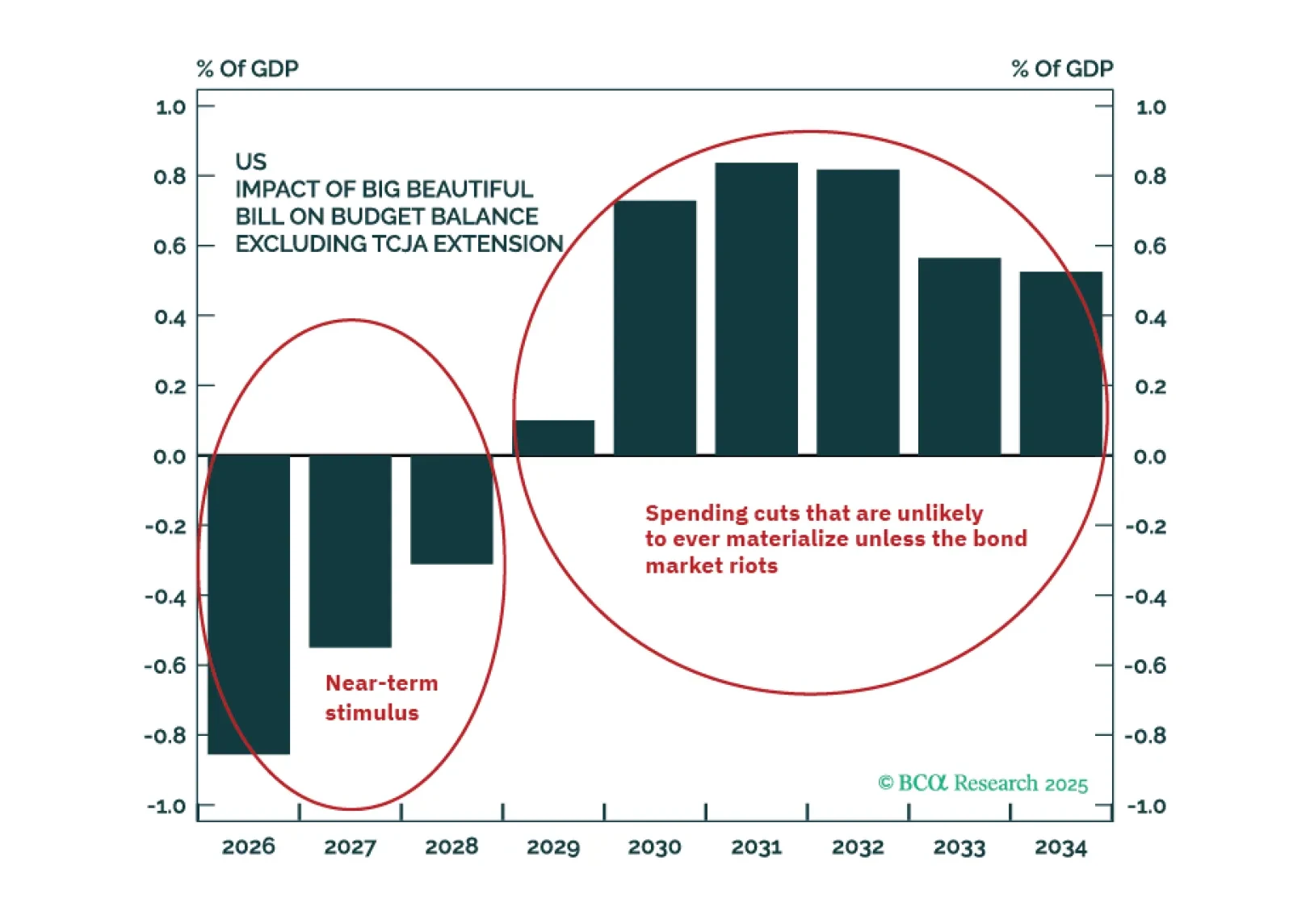

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

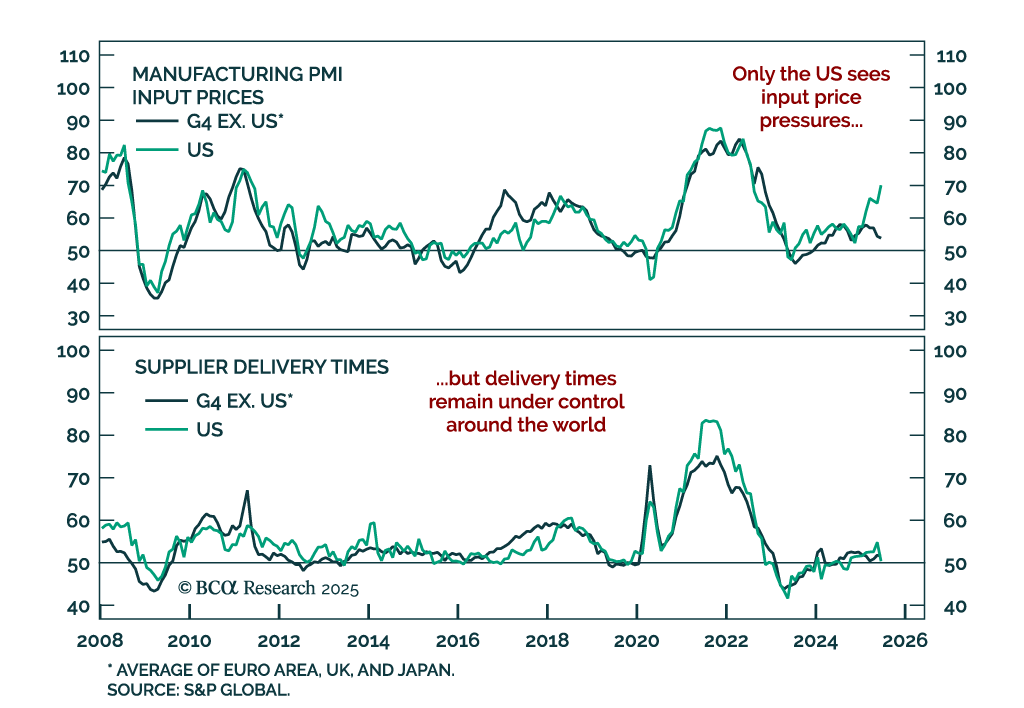

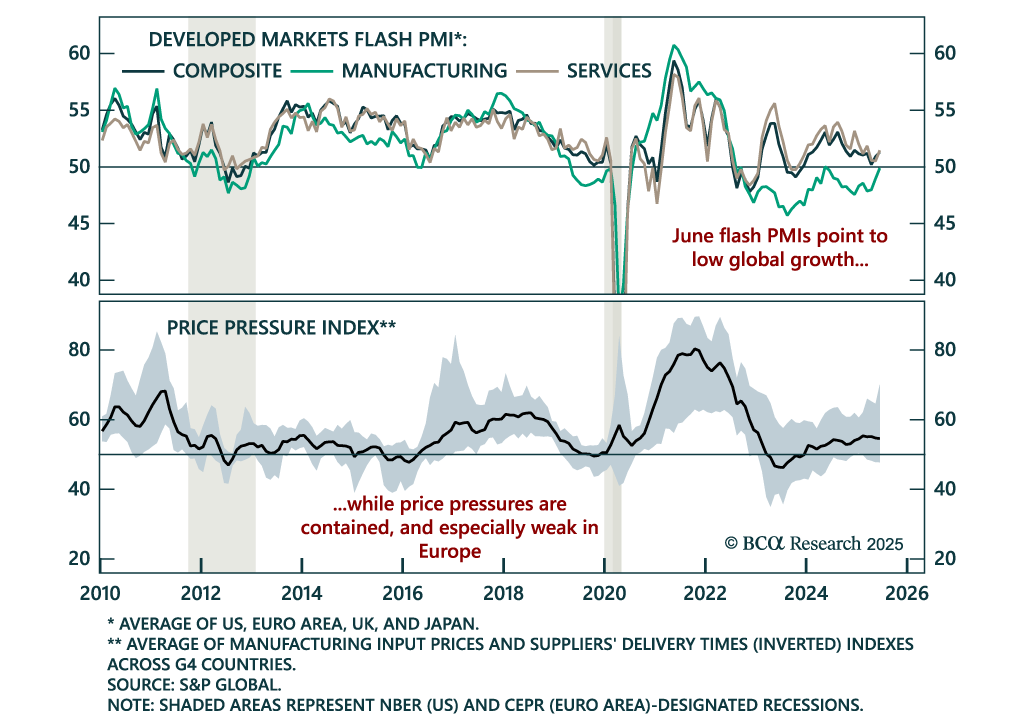

The US economy has held up better so far this year than we had expected. For the time being, investors should remain modestly underweight equities. A more aggressive underweight would be justified only once the “whites of the recession’s eyes” are visible.