Domestic Politics

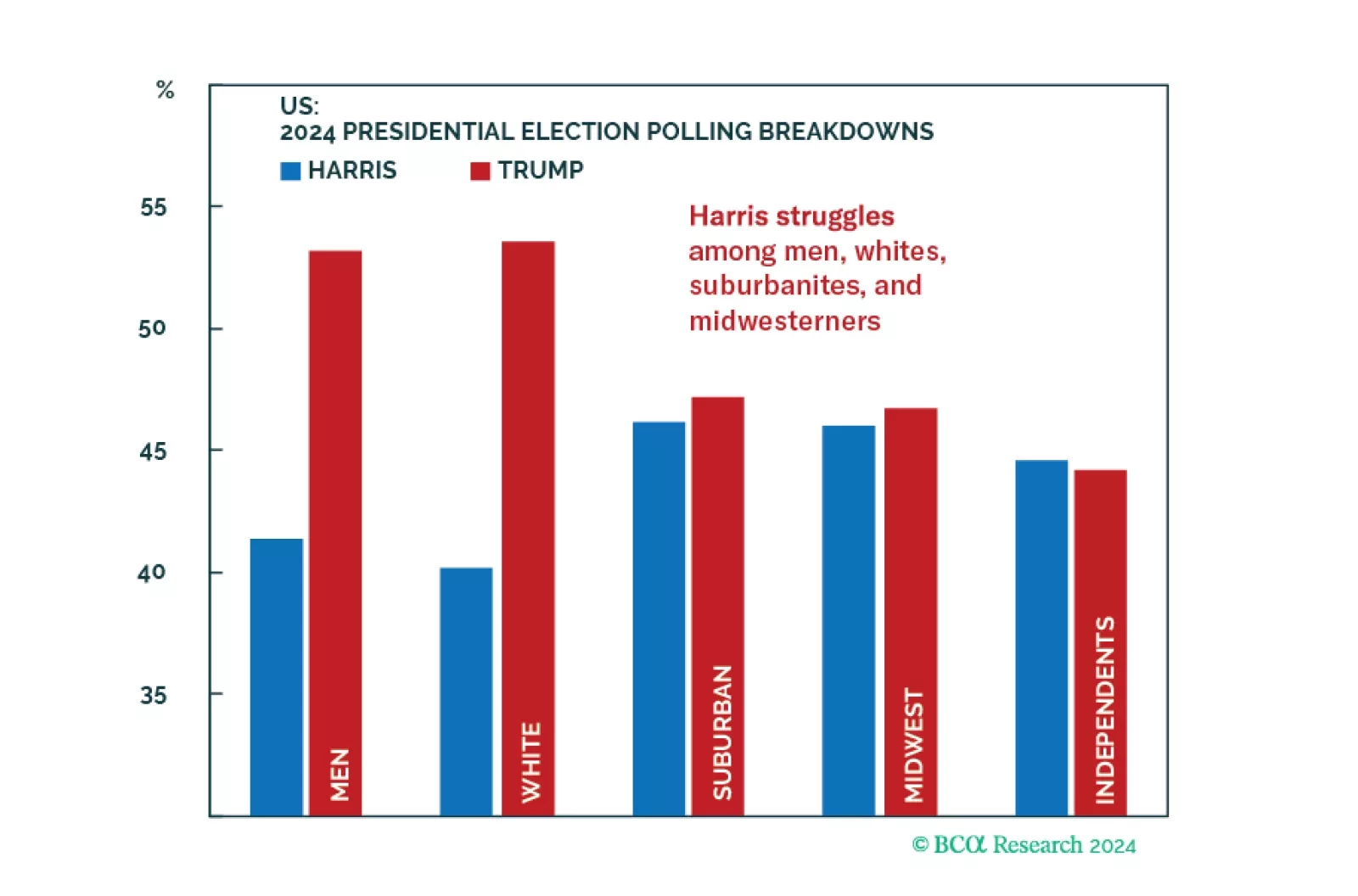

Favor Health Care and Utilities for defensive positioning amid economic slowdown and volatility as the presidential election approaches. A Republican Sweep favors Real Estate and Materials, while the second most likely outcome, Democrat gridlock, favors Health Care, and Information Technology.

Investors should buy protection against further volatility. The shakeup in early August was a taste of things to come. The US election is a pivotal moment in modern history that will drive up uncertainty, while other countries take advantage of US division and distraction.

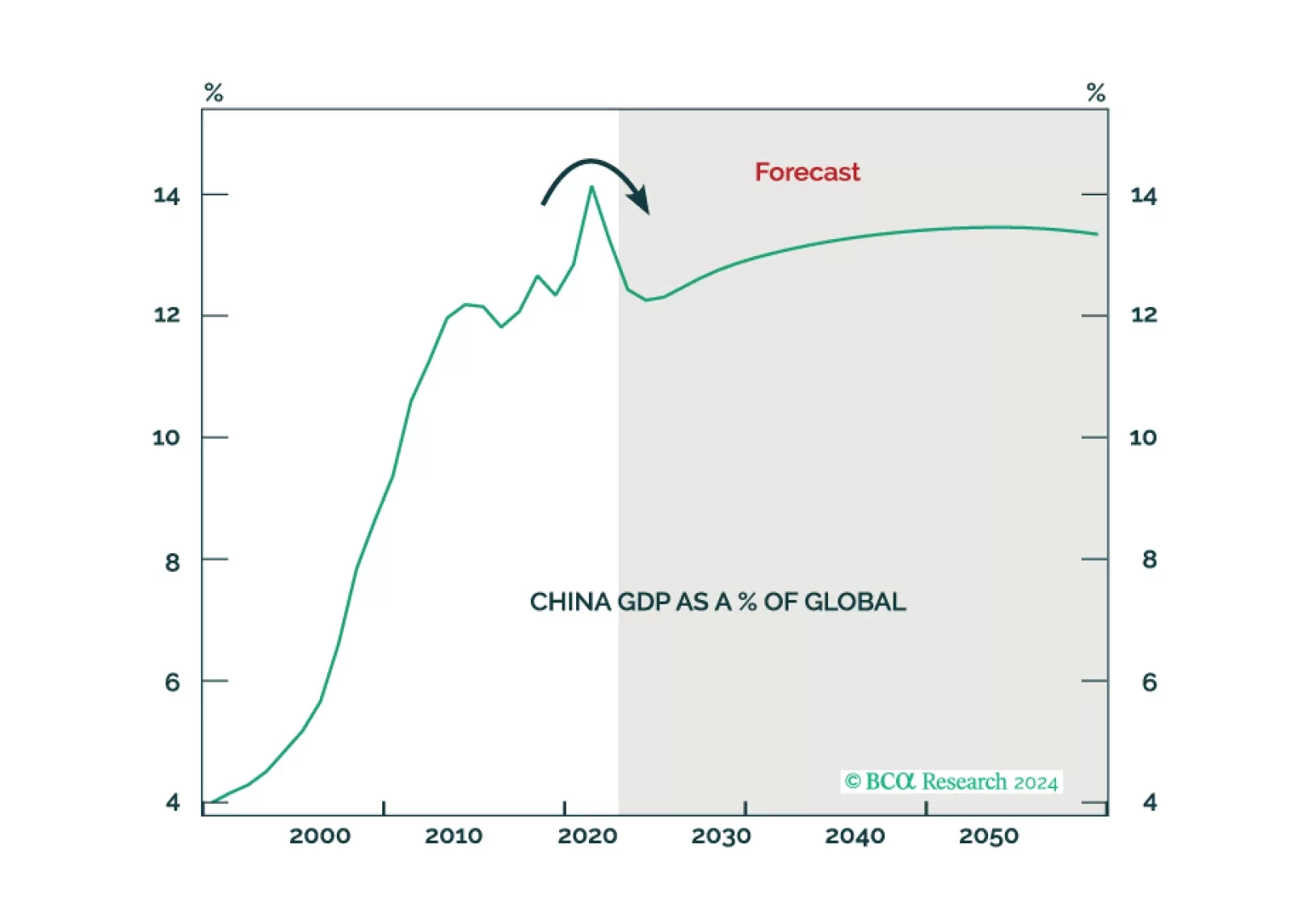

China missed the chance to change course on economic policy and now it faces rising social instability and western protectionism. This policy approach implies it is not afraid of escalating strategic conflicts in East Asia. Investors should continue to underweight Greater Chinese assets. Any US-China détente will come later rather than sooner.

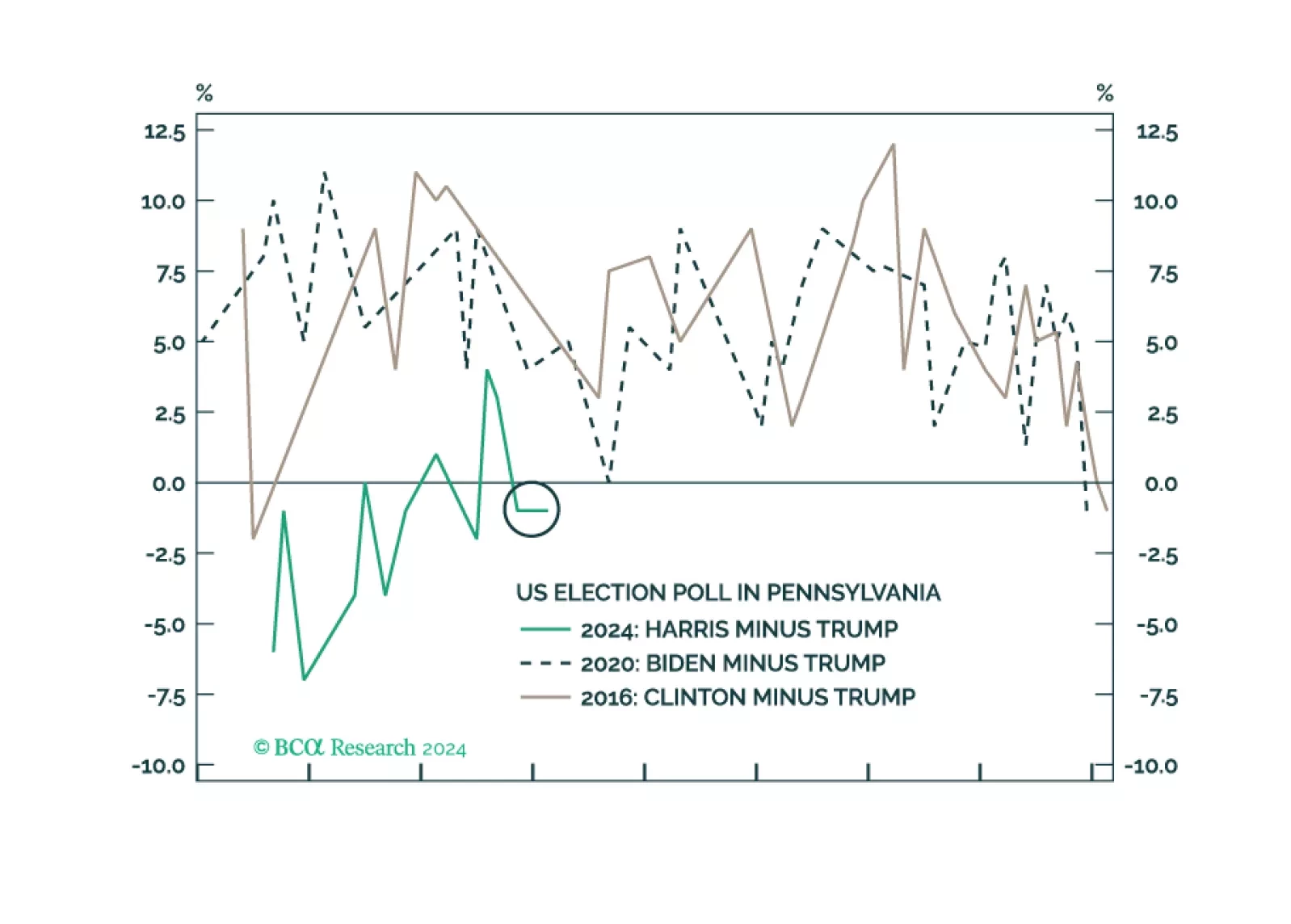

Harris picked Walz to patch up her weak side in the electorally vital Midwest. But the US election will continue to weigh on risk appetite, stocks, and high-beta assets because the odds of a single-party sweep are at least 50%, probably higher. Policy uncertainty and risk premiums will rise, not fall, in the coming months.

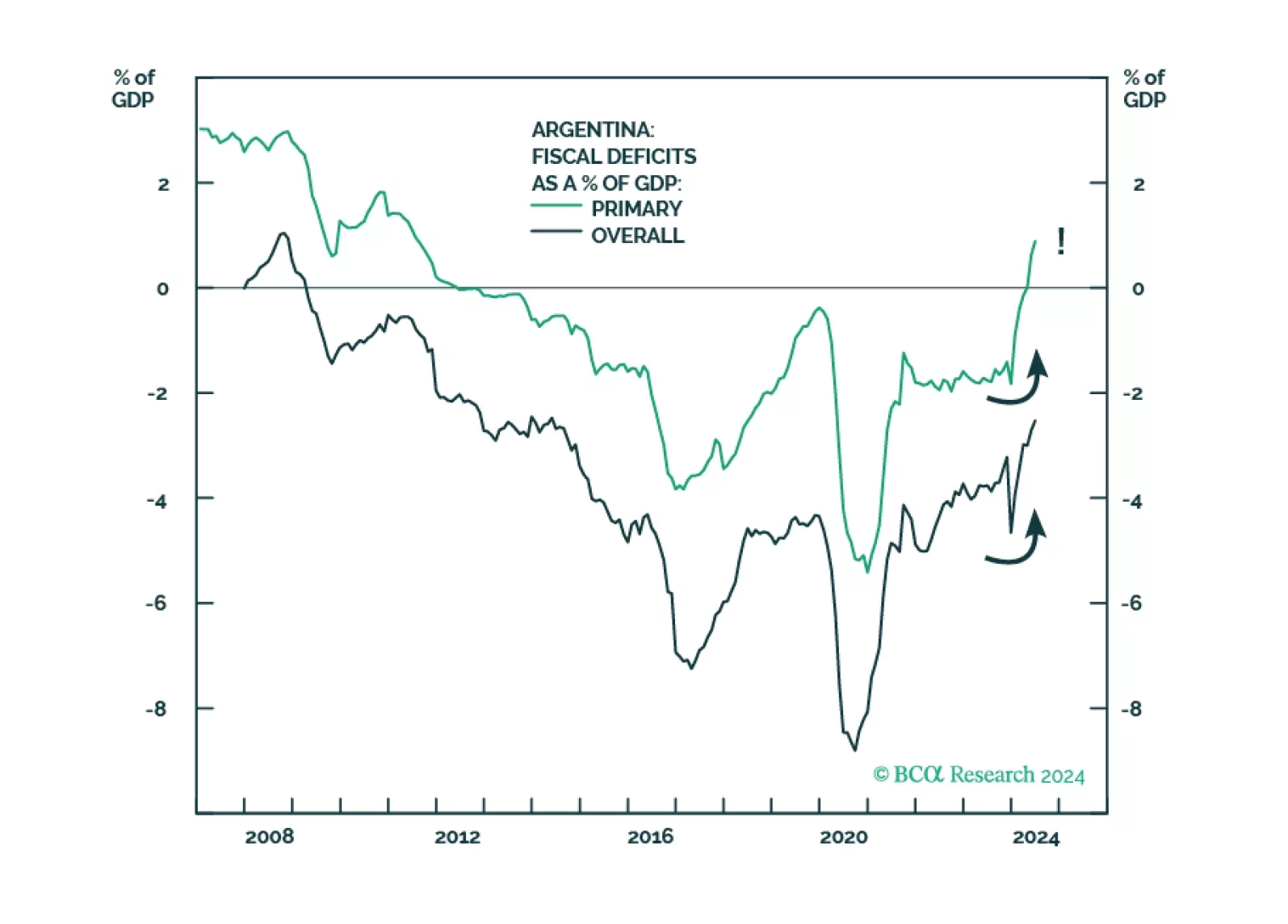

GeoMacro team partners with BCA’s Emerging Markets Strategy to examine political reforms in Argentina. Our colleague Juan Egaña argues that the time is not right to go long Argentinian assets and that Buenos Aires must avoid the mistakes of the Macri era: opening to foreign capital flows too soon without addressing structural macro imbalances. However, the Milei administration is on the right path with potentially global implications.

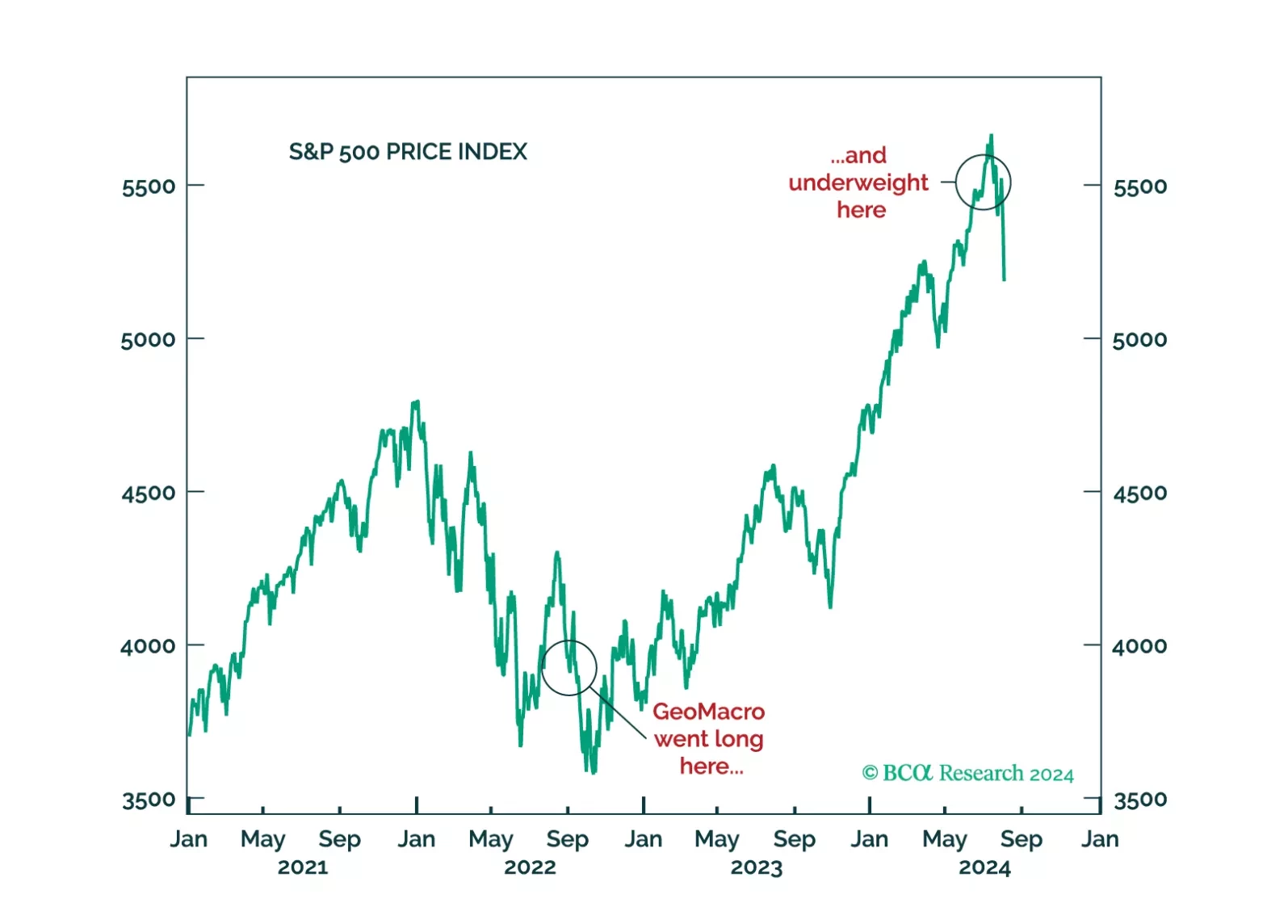

The decision by GeoMacro team on July 2 to short USDJPY and underweight equities has proven to be prescient. We still do not like the market setup from here on out. A recession would, obviously, be negative for risk assets. But even if investors avoid that scenario, the transition from cash- to leverage-driven growth is unlikely without a significant Fed rate-cutting cycle.