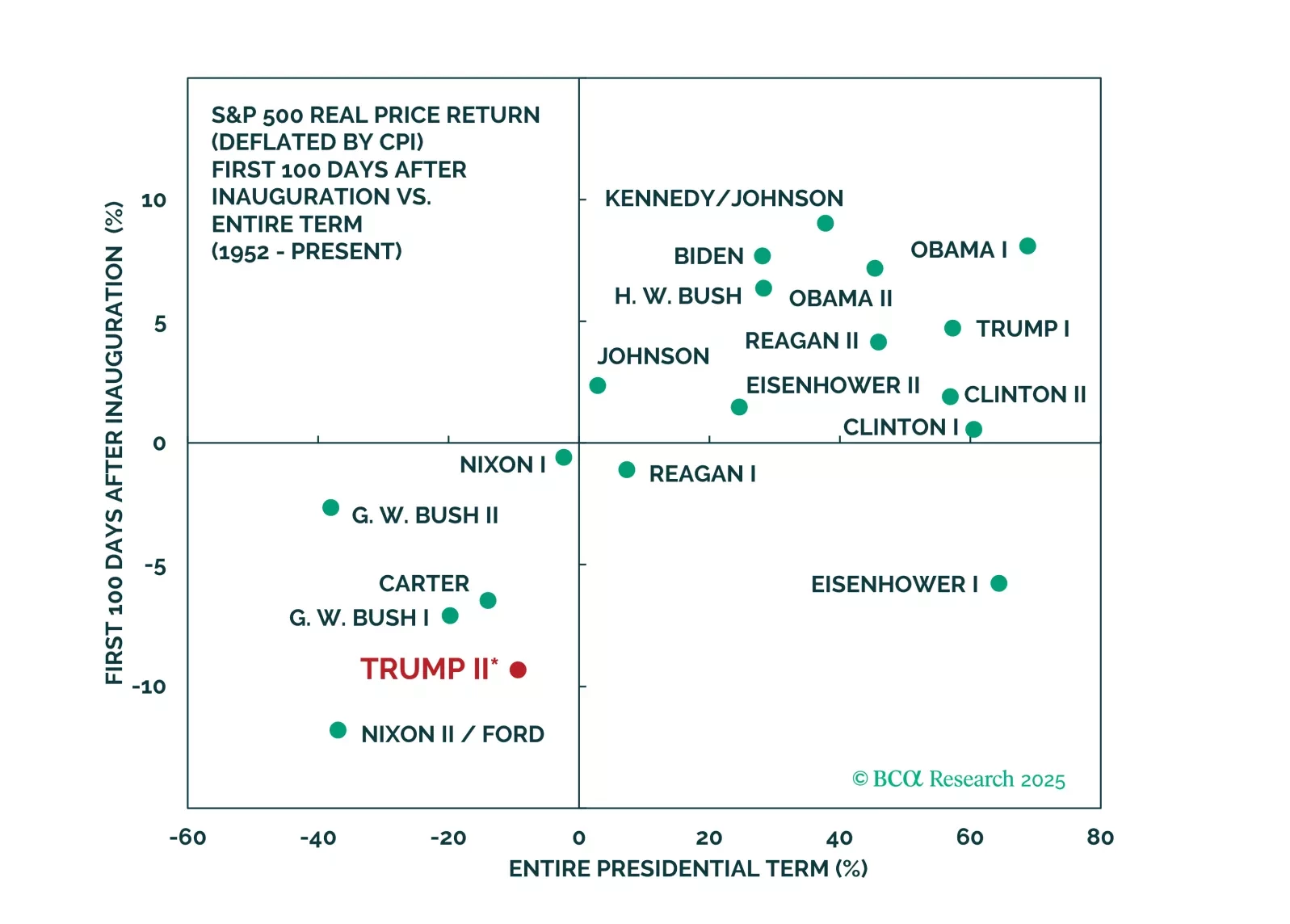

Domestic Politics

Acute geopolitical risks, like a massive oil shock, may be abating. But structural geopolitical risk remains high and could upset a blithe market. Cyclical economic risks are underrated as the US slows down and China continues to stumble. Investors should book some profits in anticipation of tariff implementation and a downturn in hard economic data.

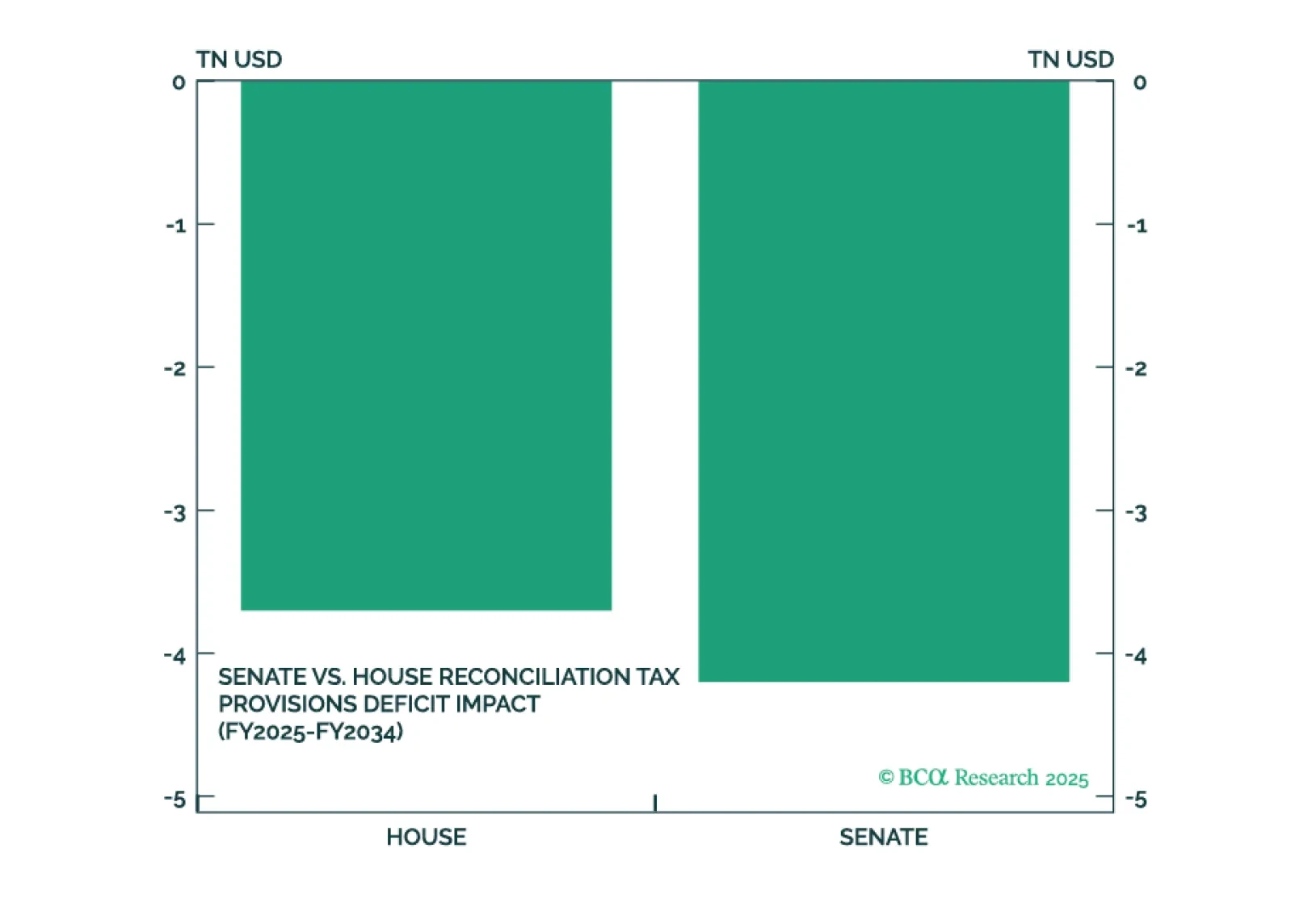

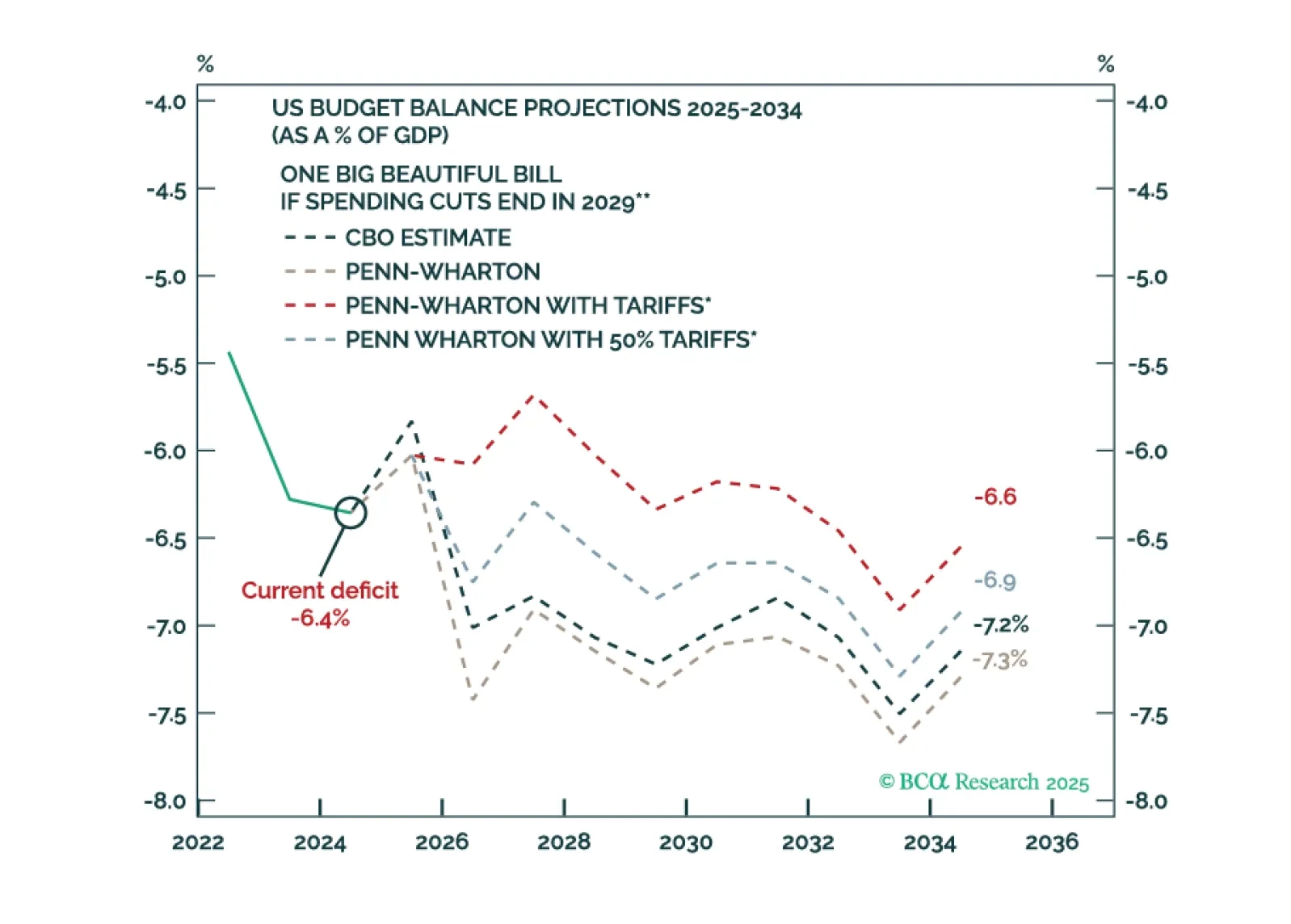

President Trump’s big beautiful bill will pass but faces near-term hurdles and will not tighten the government’s belt. It will combine with renewed tariff implementation to generate near-term risk for both the bond and stock market. The Iran crisis fizzled, saving Trump from a major oil shock that could have derailed his second term.

Bond market volatility will spike again in the near term. The Fed is committed to an easing cycle yet the Trump administration’s signature fiscal policy action will stimulate the economy. Tariffs are supposed to keep the budget deficit contained but they are inflationary.

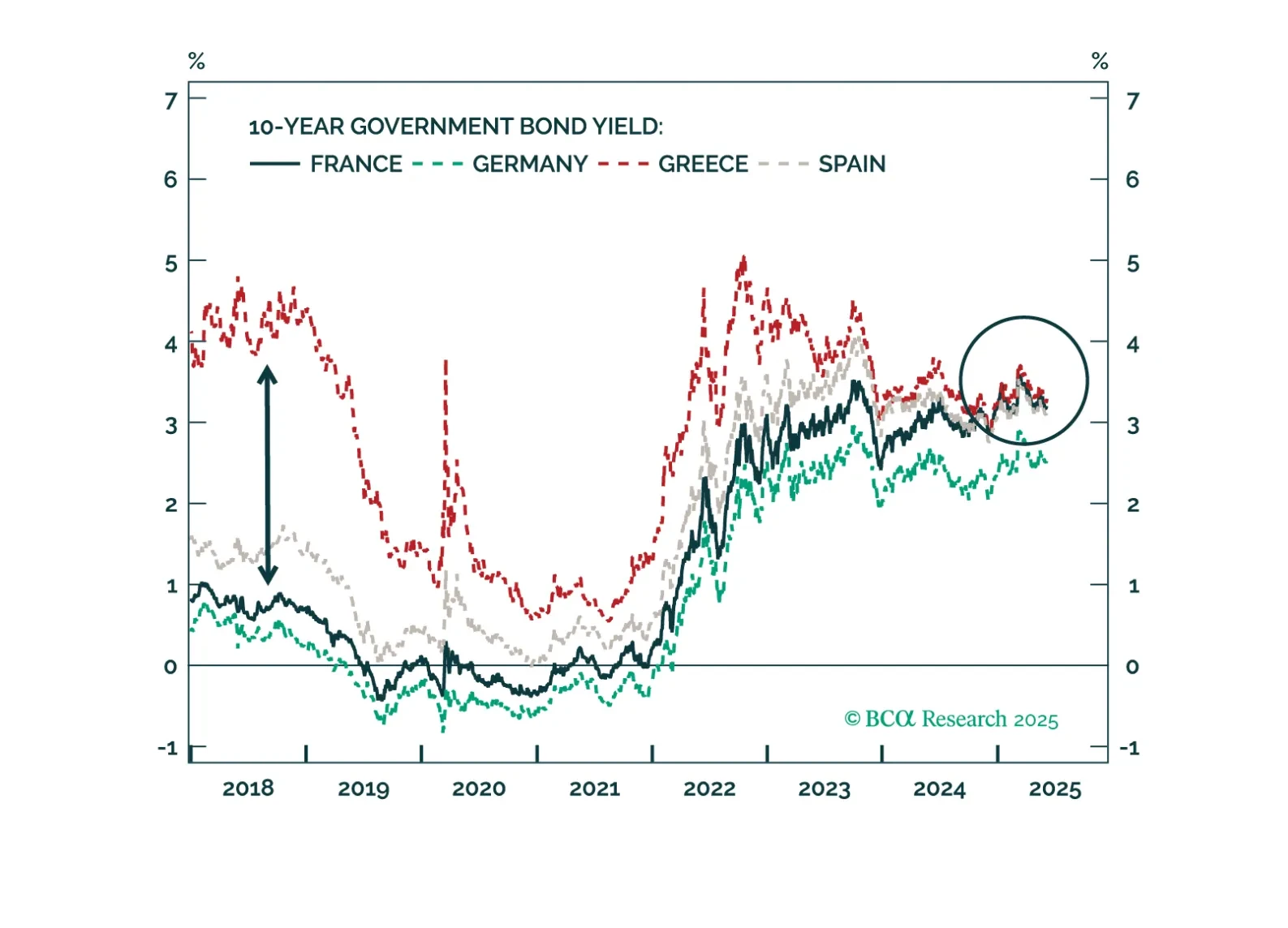

France’s political turmoil is far from over, and fiscal fears are growing. This is not a bond-friendly environment. In contrast, it is a good time to upgrade French equities. As the 2027 presidential race is about to begin in earnest, we make an early call on its outcome.

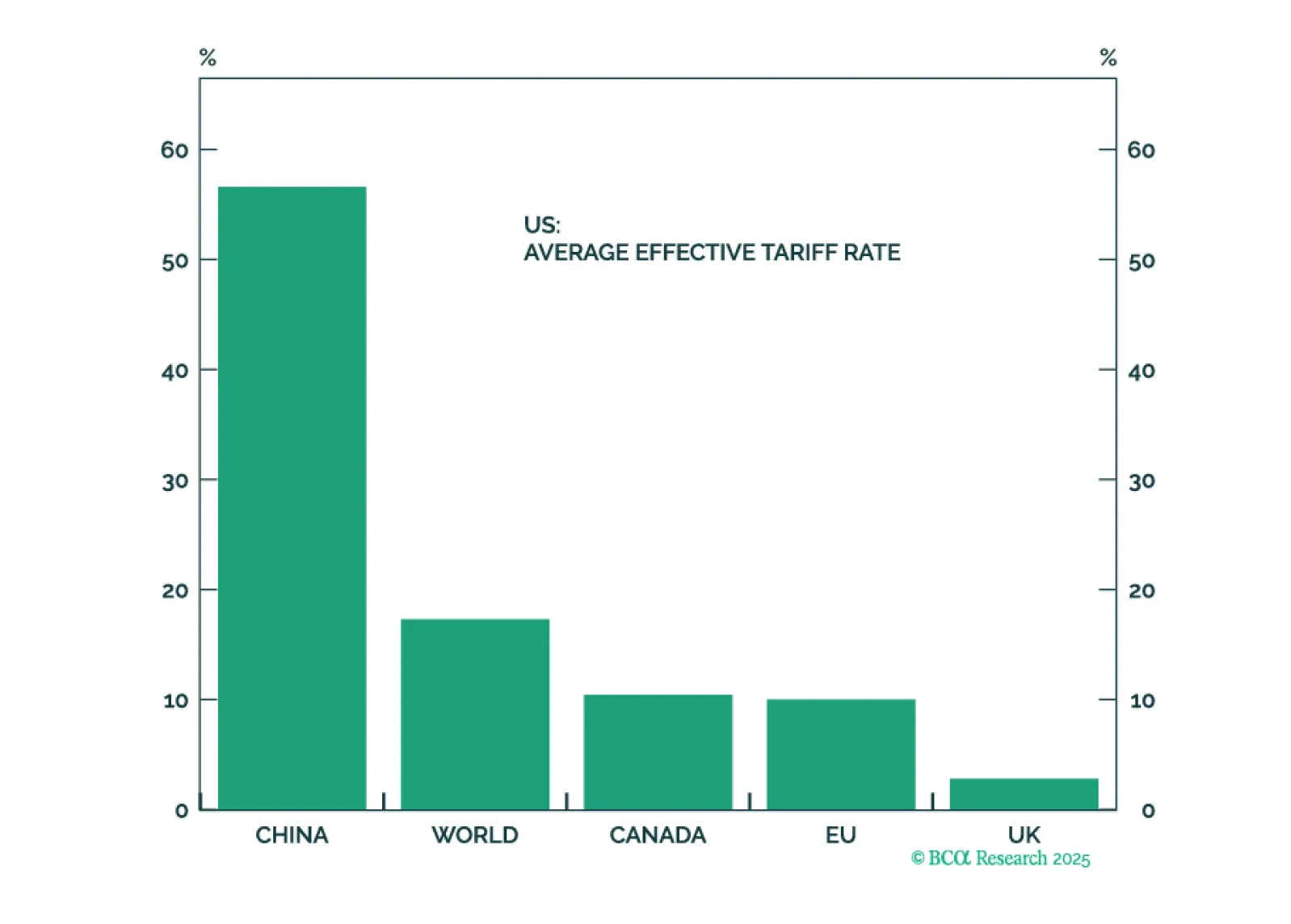

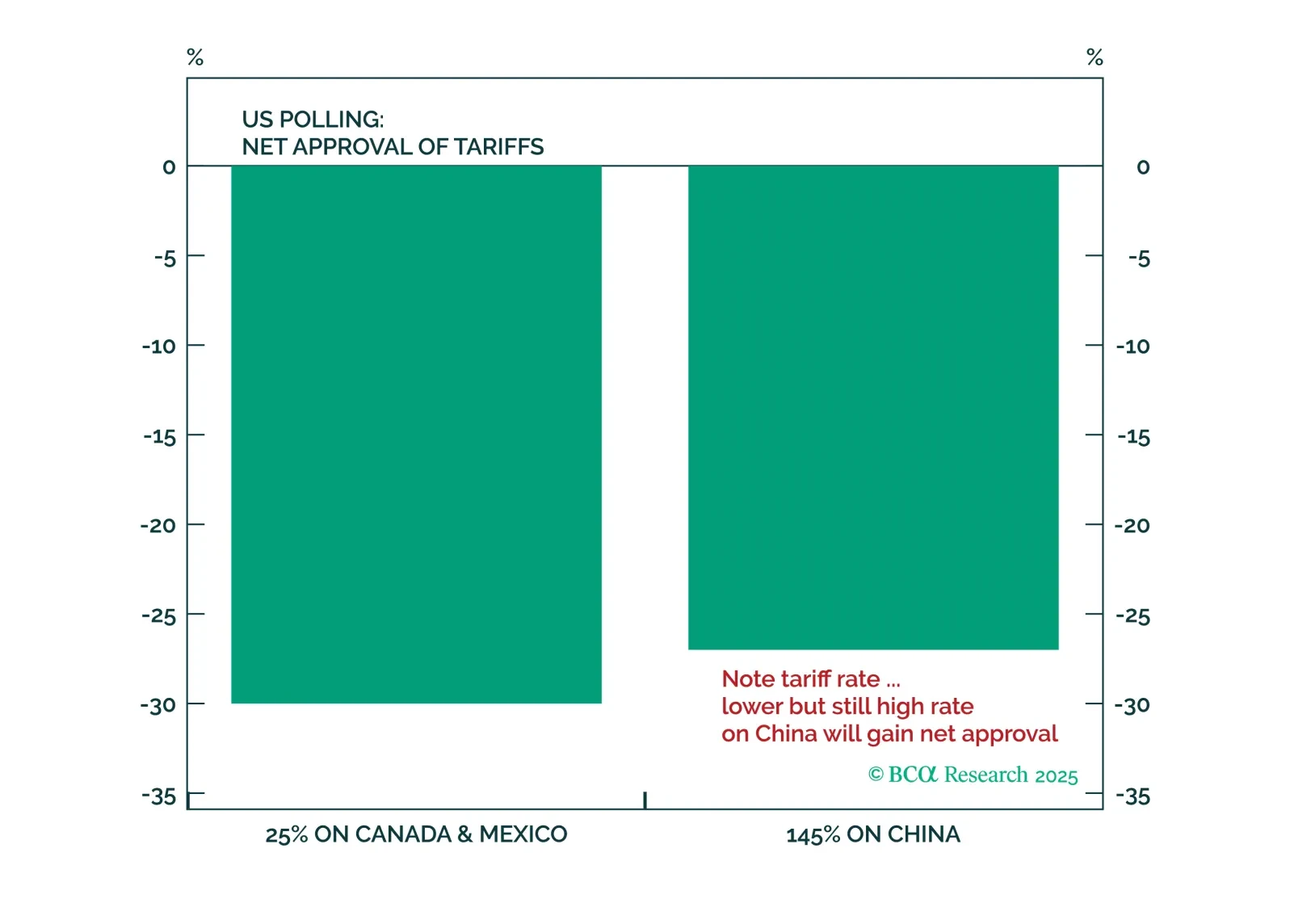

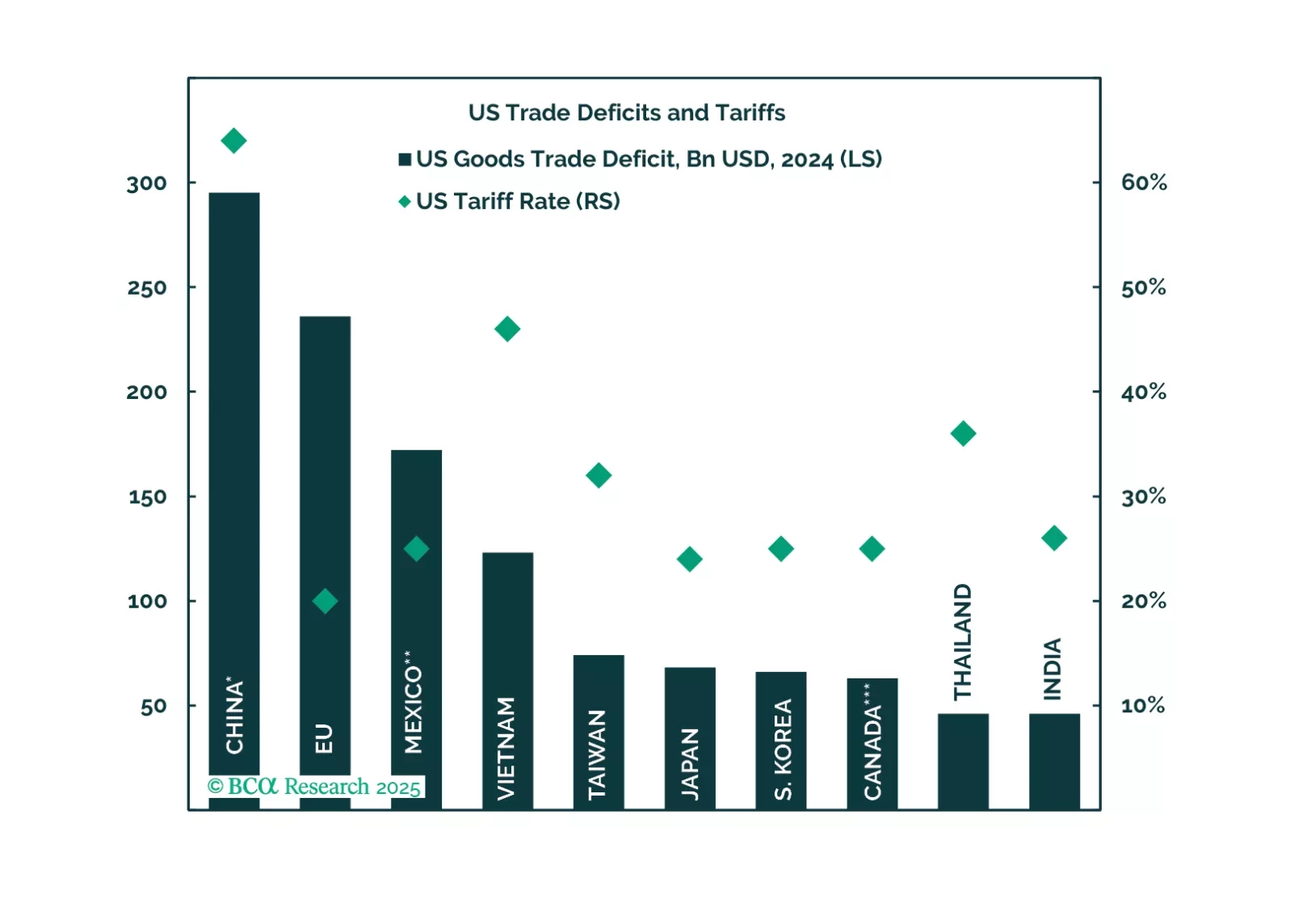

President Trump faces new restrictions on his trade powers coming from the US judicial branch, but they will not prevent him from continuing to restrict trade and investment with China. Rather, they will establish some curbs against entirely arbitrary executive tariffs, especially when wielded against US allies and partners.

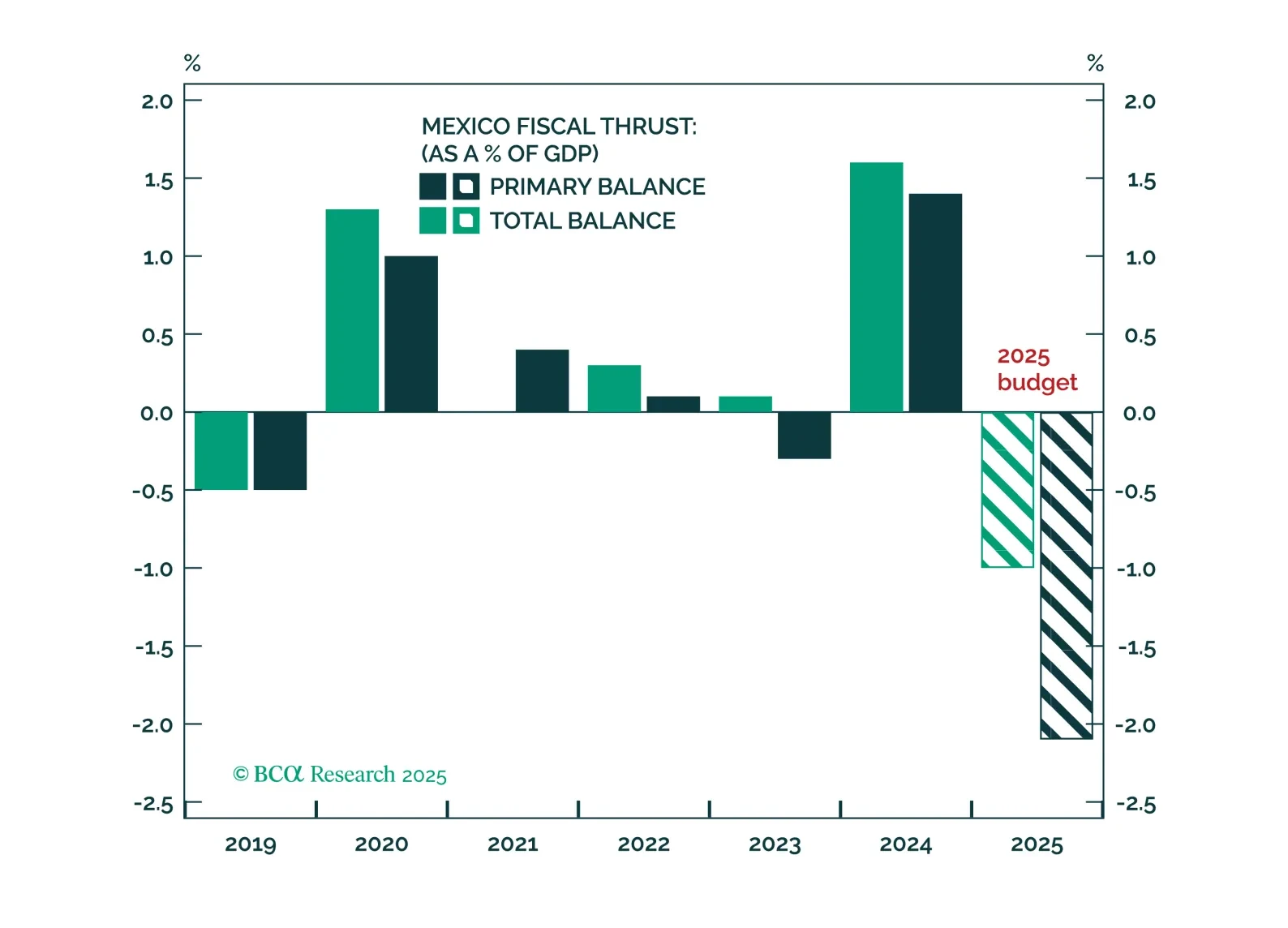

Short-term pain from Trump-related concessions, fiscal tightening amid a US and Mexican slowdown, and rising labor slack will weigh further on Mexican assets. But long-run, policy direction will capitalize on the nearshoring trend and resume the trend of Mexican asset outperformance relative to other emerging markets.

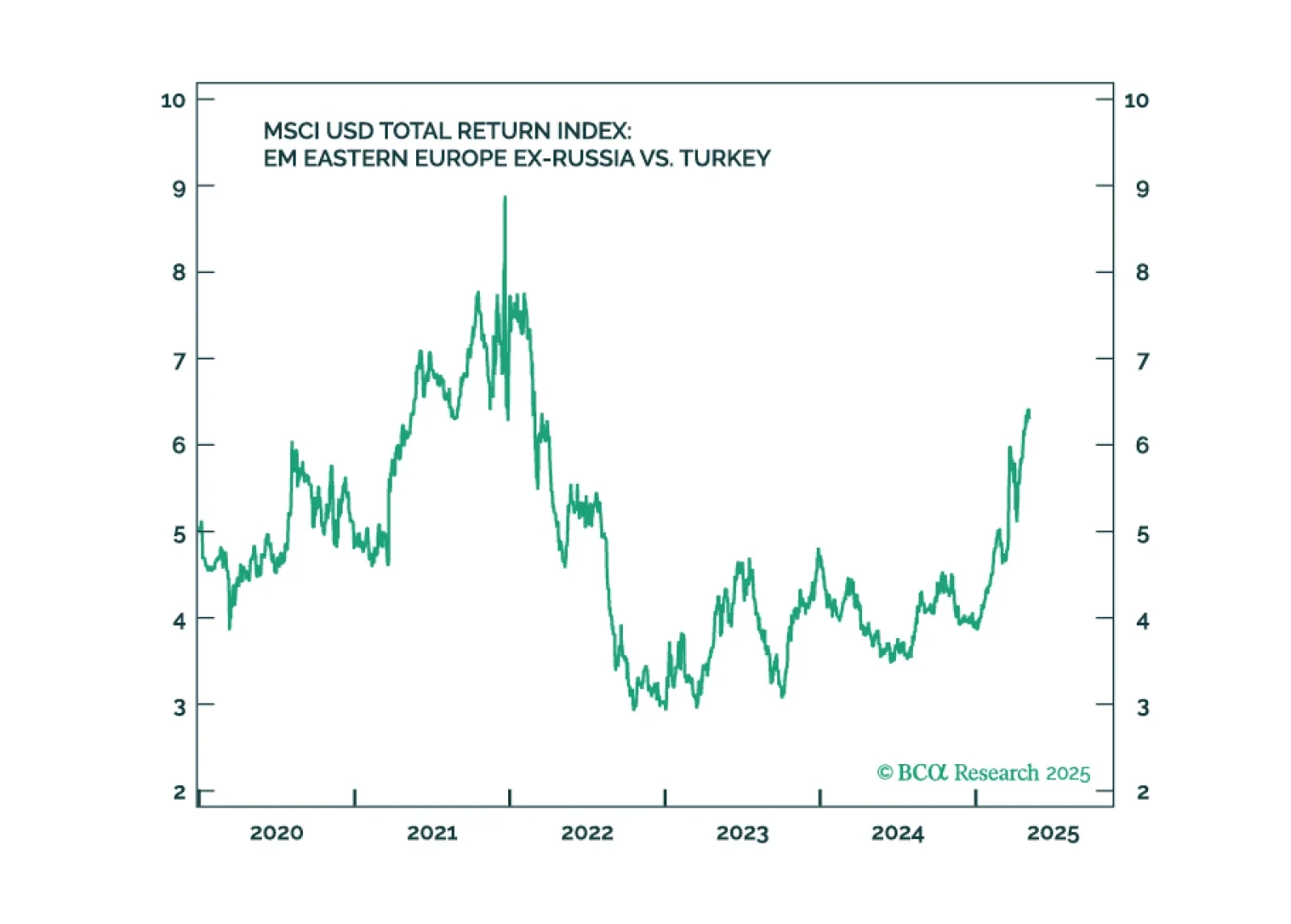

Erdogan's rule continues to decline. Social unrest will persist, governance will erode, and the macro backdrop will deteriorate further. We recommend underweighting Turkish assets.

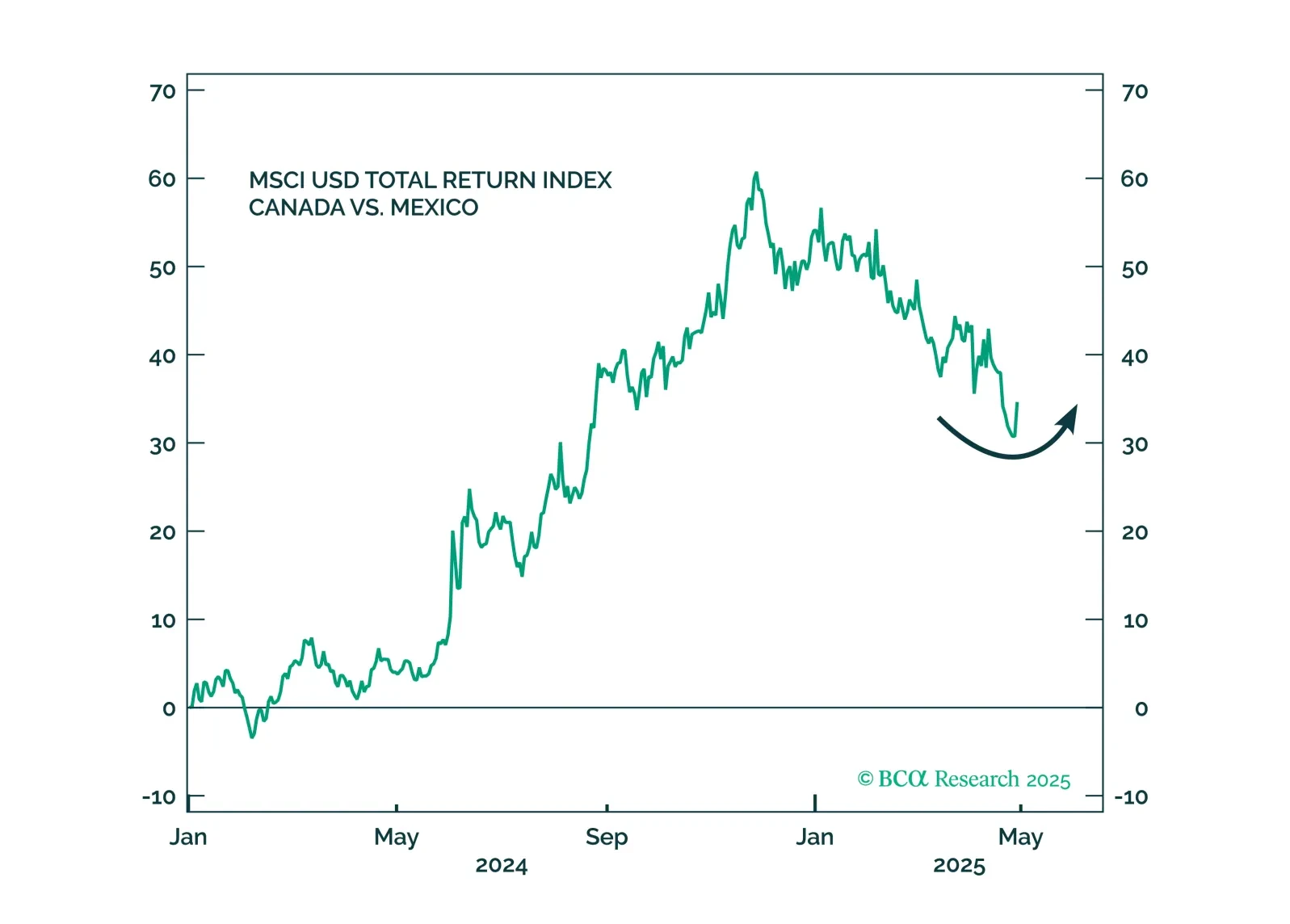

The US and Canada will resolve their trade dispute quickly, leading to a North American deal and better prospects for future relations, as well as for other US trade deals around the world. But even as tariff threats decline, the US economy will slow, weighing on its neighbors. Canada will fare better than Mexico.

Do not play the bounce in US and global cyclical assets as Trump backpedals from the trade war. China will talk, but the pace will be slow and the outcome disappointing. Fiscal stimulus will surprise marginally in the EU, China, and even the US, but still may not rescue the business cycle.

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.