Diplomacy/Foreign Relations

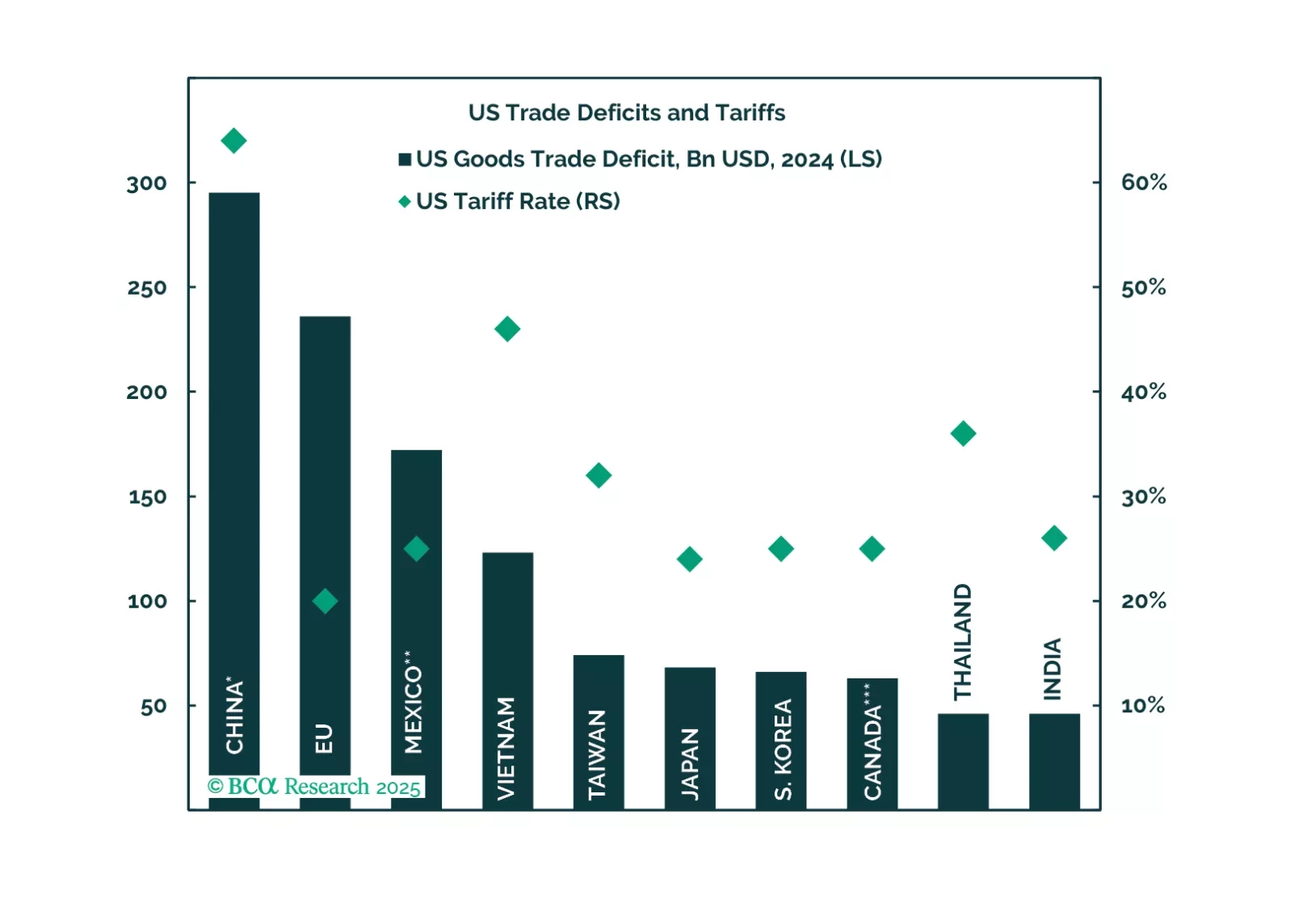

Trump's Tariff D-Day brings a negative surprise to financial markets already anxious over a declining US cyclical economy. Investors should sell risky assets, increase safe havens, and overweight US assets in the near term.

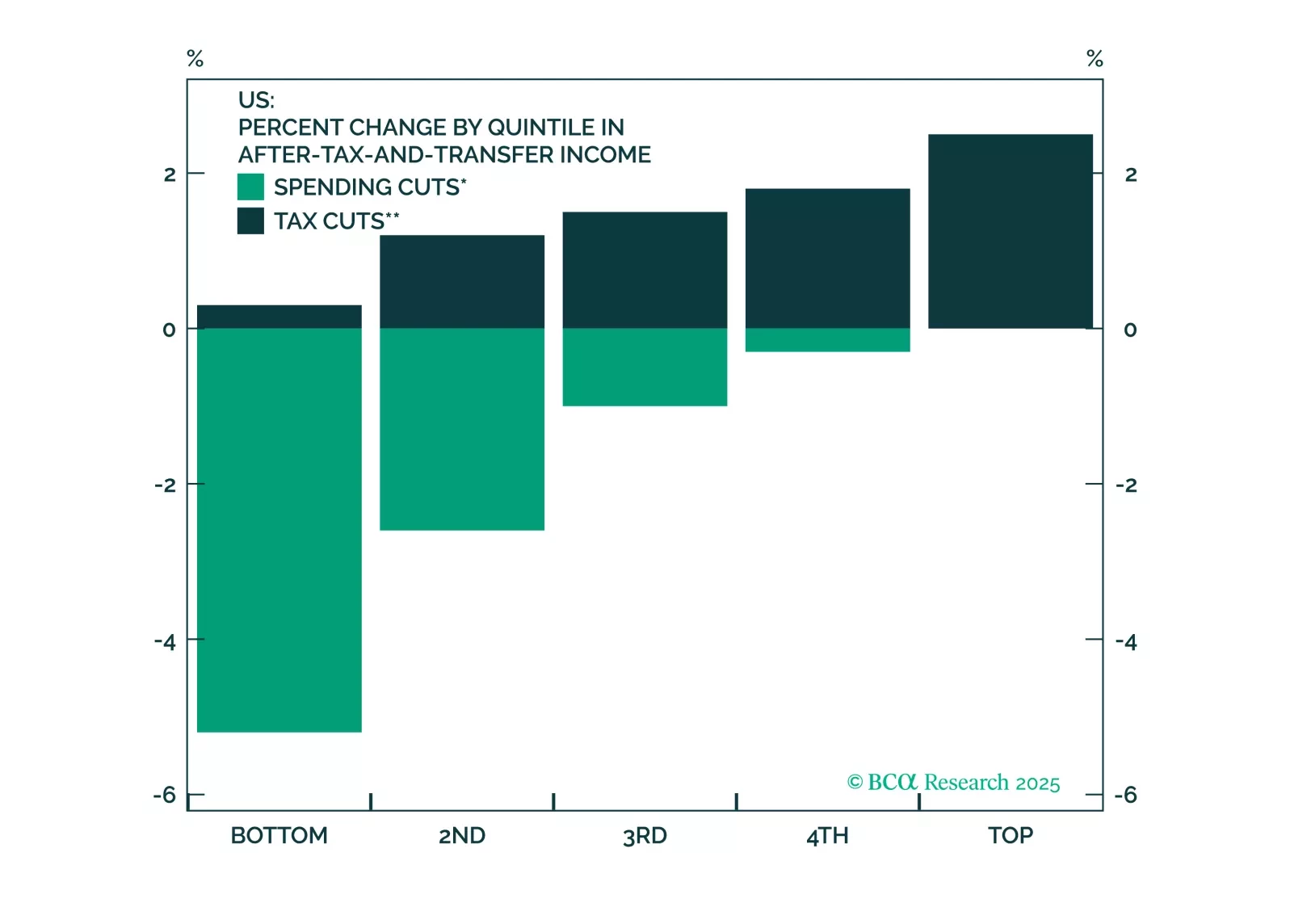

Stocks will continue to struggle in the second quarter as President Trump tries to implement tariffs. Tax cuts will only temporarily dispel growth fears, if at all. Middle Eastern instability will add oil price surprises to an environment that is looking fairly stagflationary.

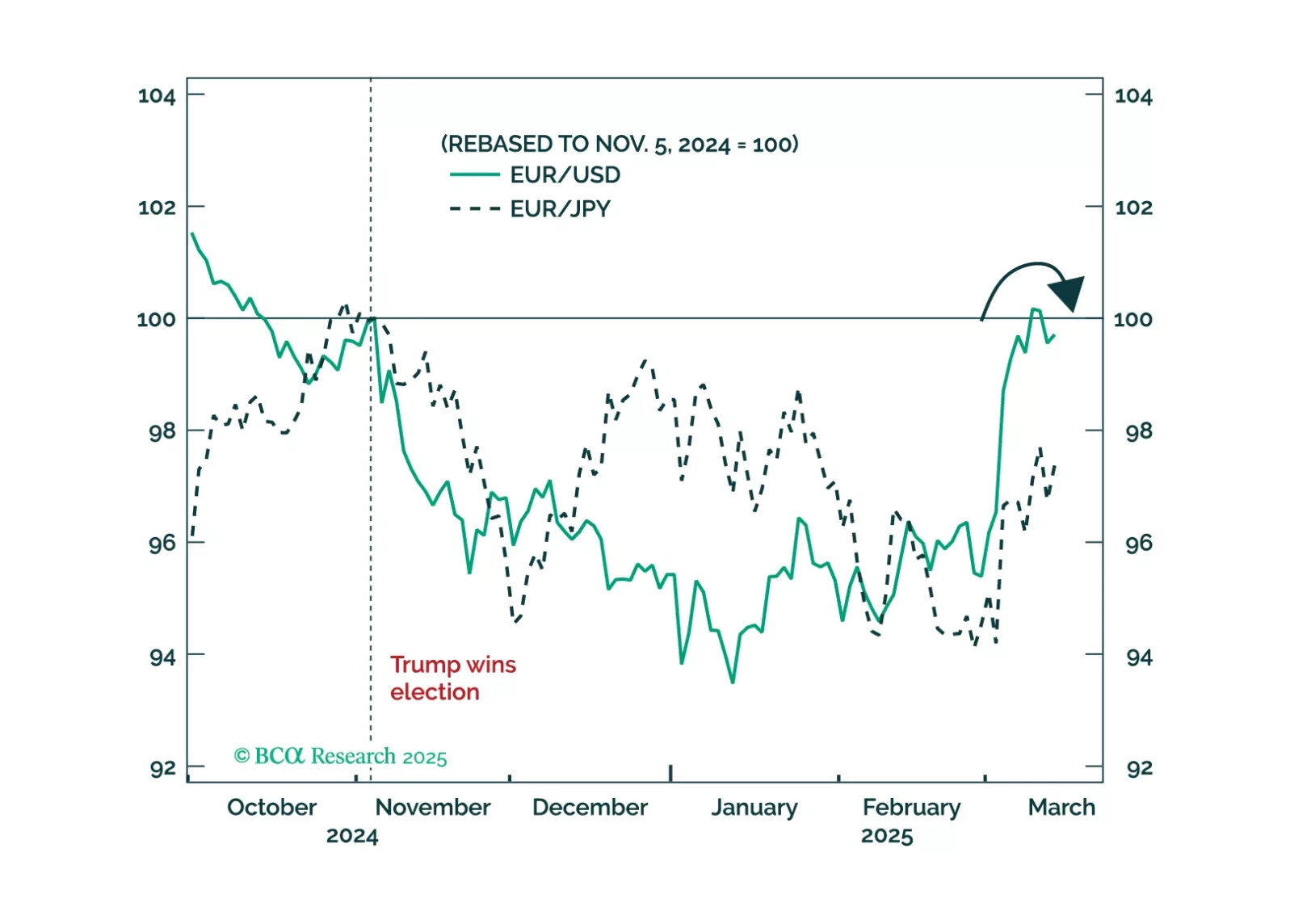

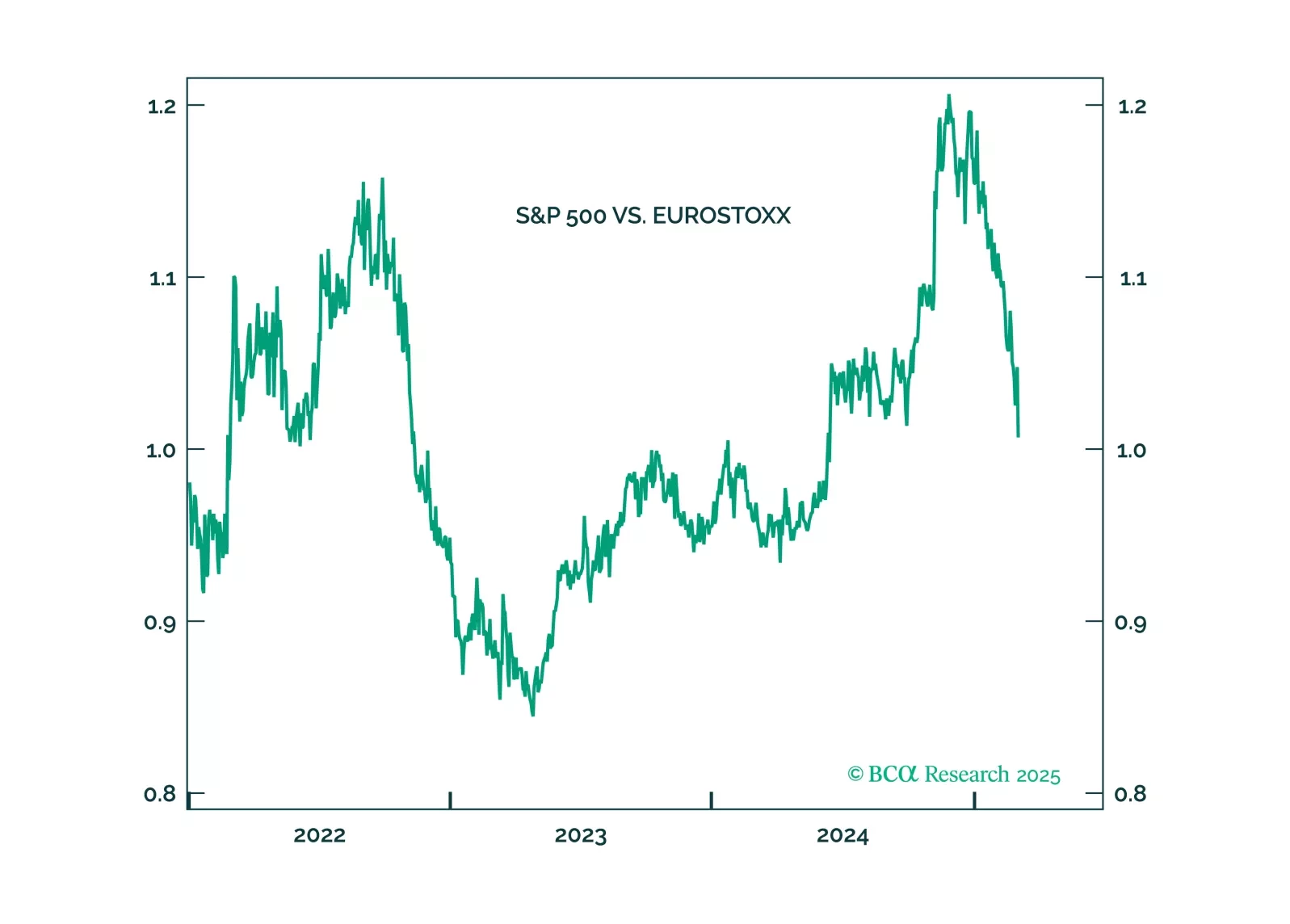

Trump’s foreign policy can be explained by rational US interests, but it requires settling the trade war with allies sooner rather than later. Book gains on EUR-USD for now.

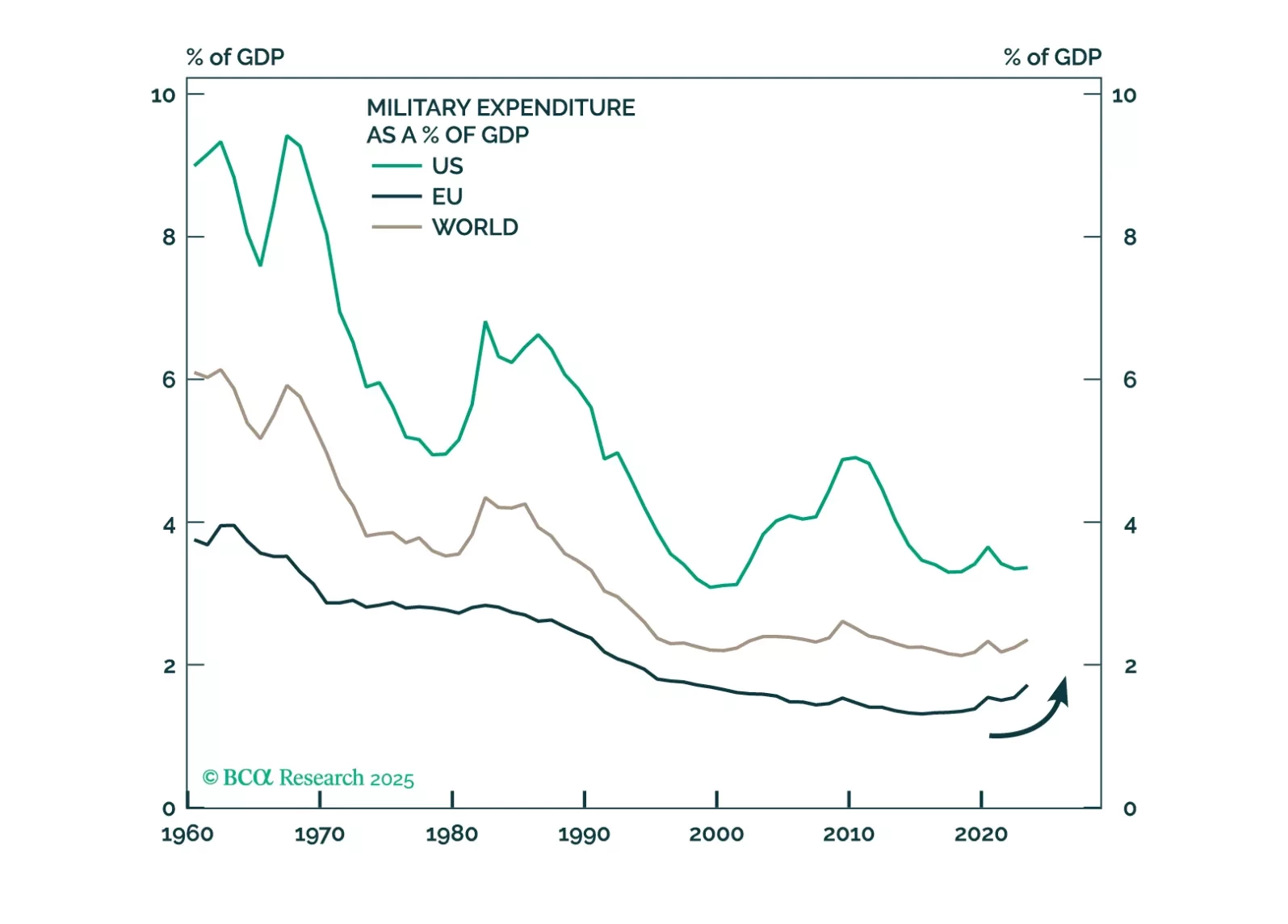

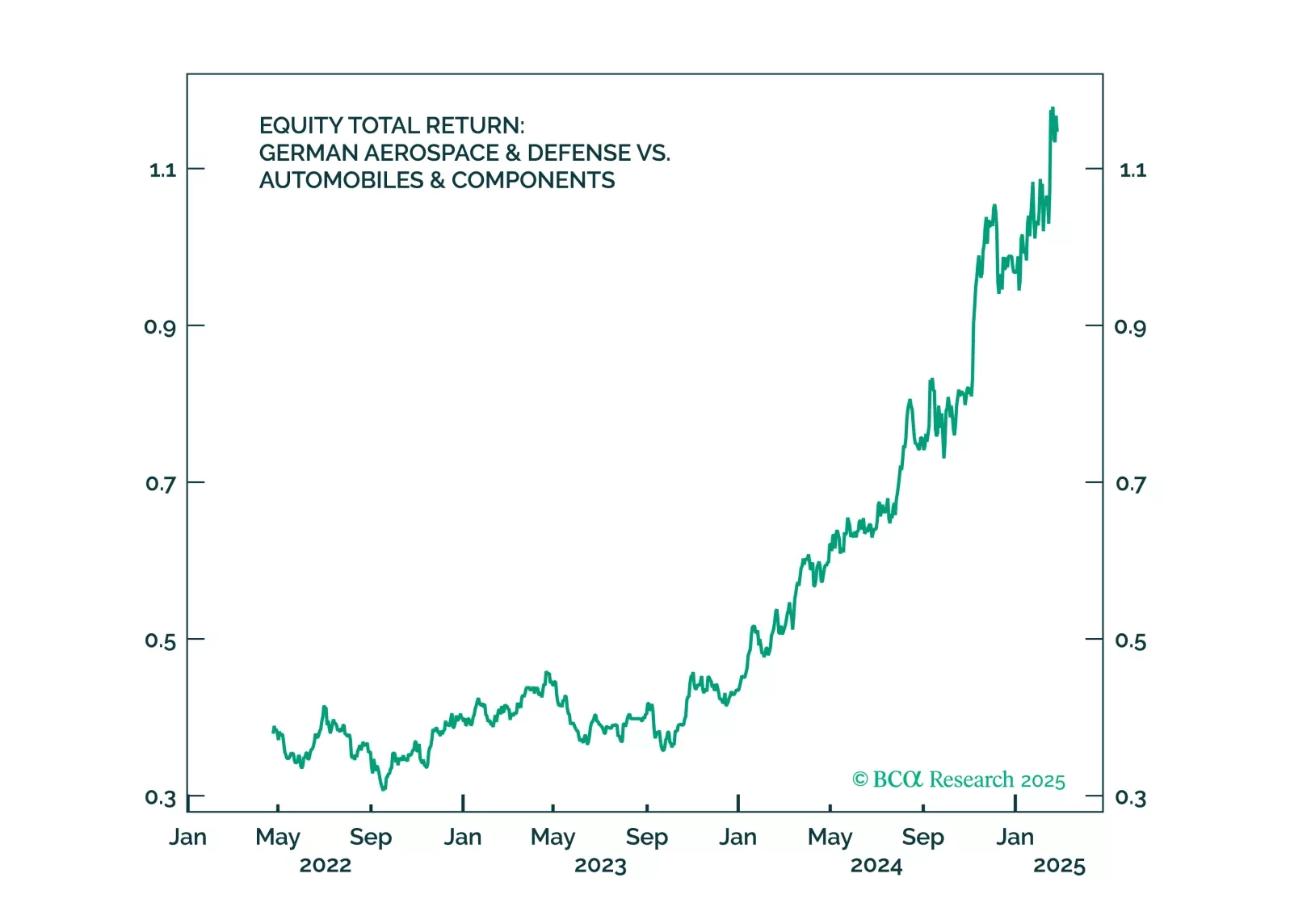

Fears of Europe’s decline due to Russian aggression and shifting US policy are overblown. President Trump’s tough stance on Ukraine is a strategic move to consolidate domestic support, not an abandonment of Europe, while Russia’s threat is exaggerated. As Europe responds with higher defense spending, stronger market integration, and greater political unity, investors should overweight European defense stocks and position for Europe’s broader market outperformance.

Trump will pull back from the trade war when stocks approach bear market territory. He will not withdraw from NATO. Favor European stocks on fiscal policy.

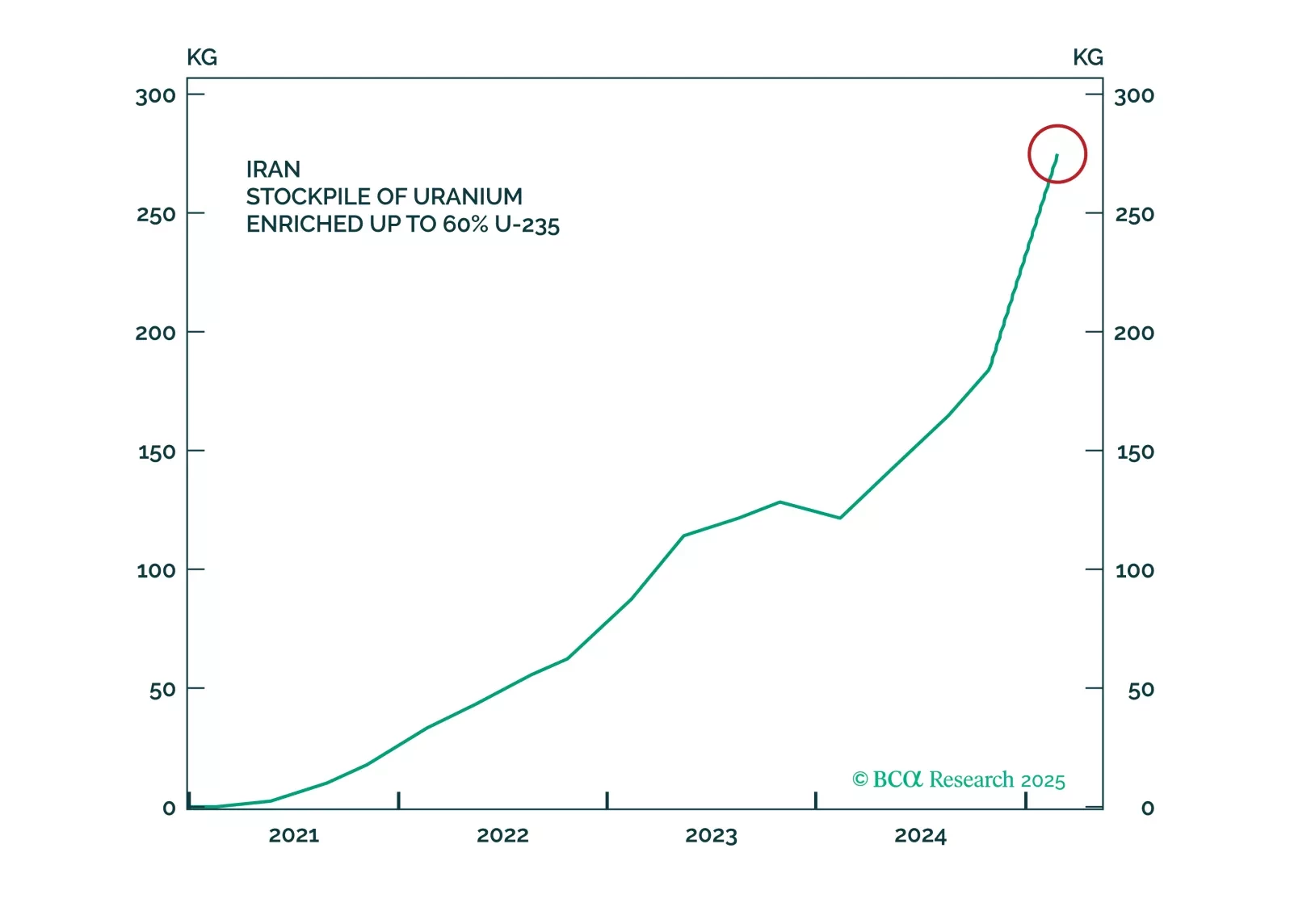

The tariffs on Canada and Mexico will come into effect as scheduled while the tariffs on China will be doubled. In the Middle East, Iranian response to any attack will threaten Middle Eastern oil supply. Meanwhile, Chinese fiscal support will surprise to the upside at the Two Sessions. But Trump's China policy will cause volatility. Now that the stock market is cracking, reinitiate defensive trades, such as long treasuries versus US stocks and long global defensives versus cyclicals.

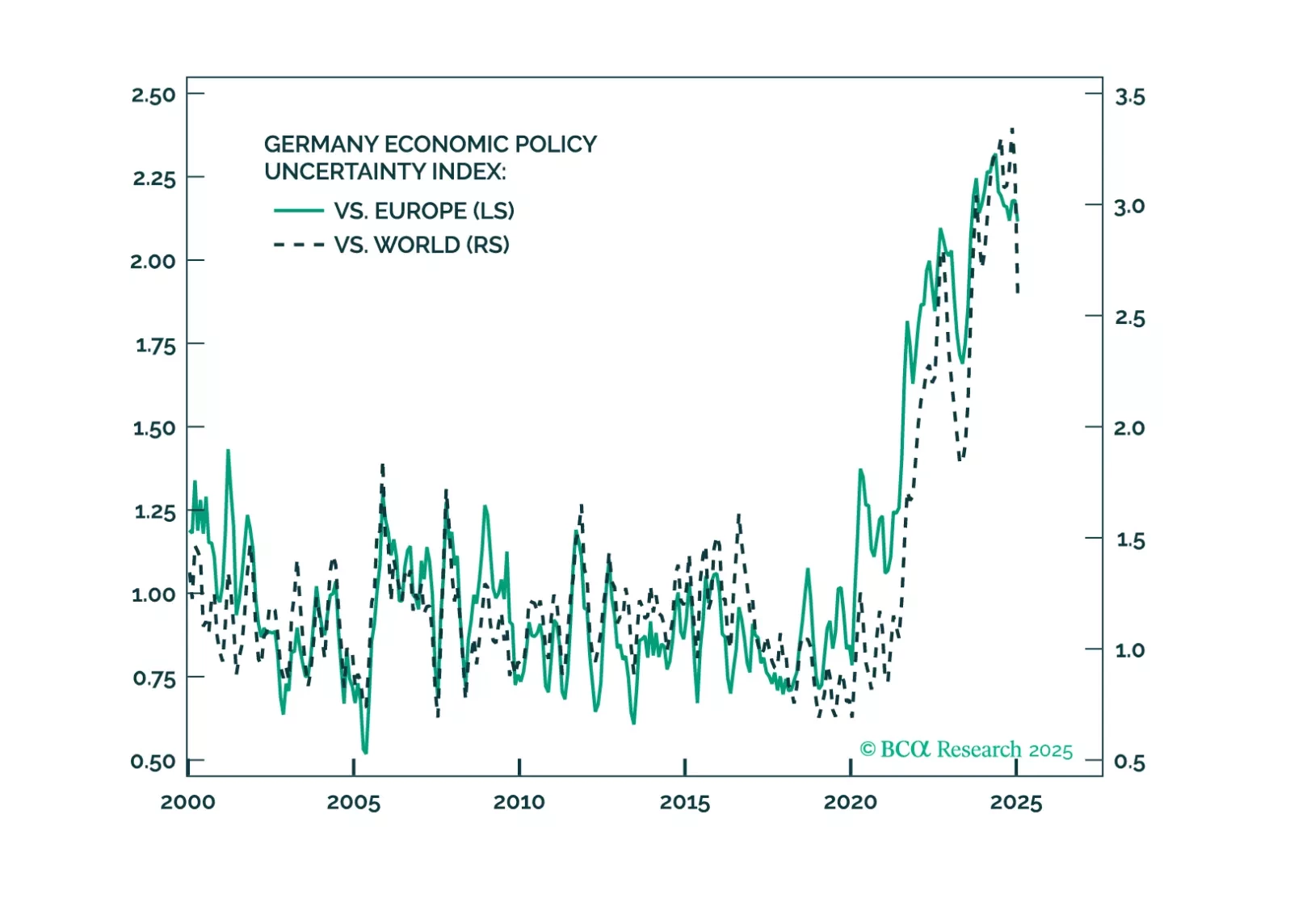

Trump’s ceasefire talks are positive for Germany – and so was the German election result. But Trump’s tariffs will hit Germany soon. Investors should use near-term volatility to increase exposure to Germany.

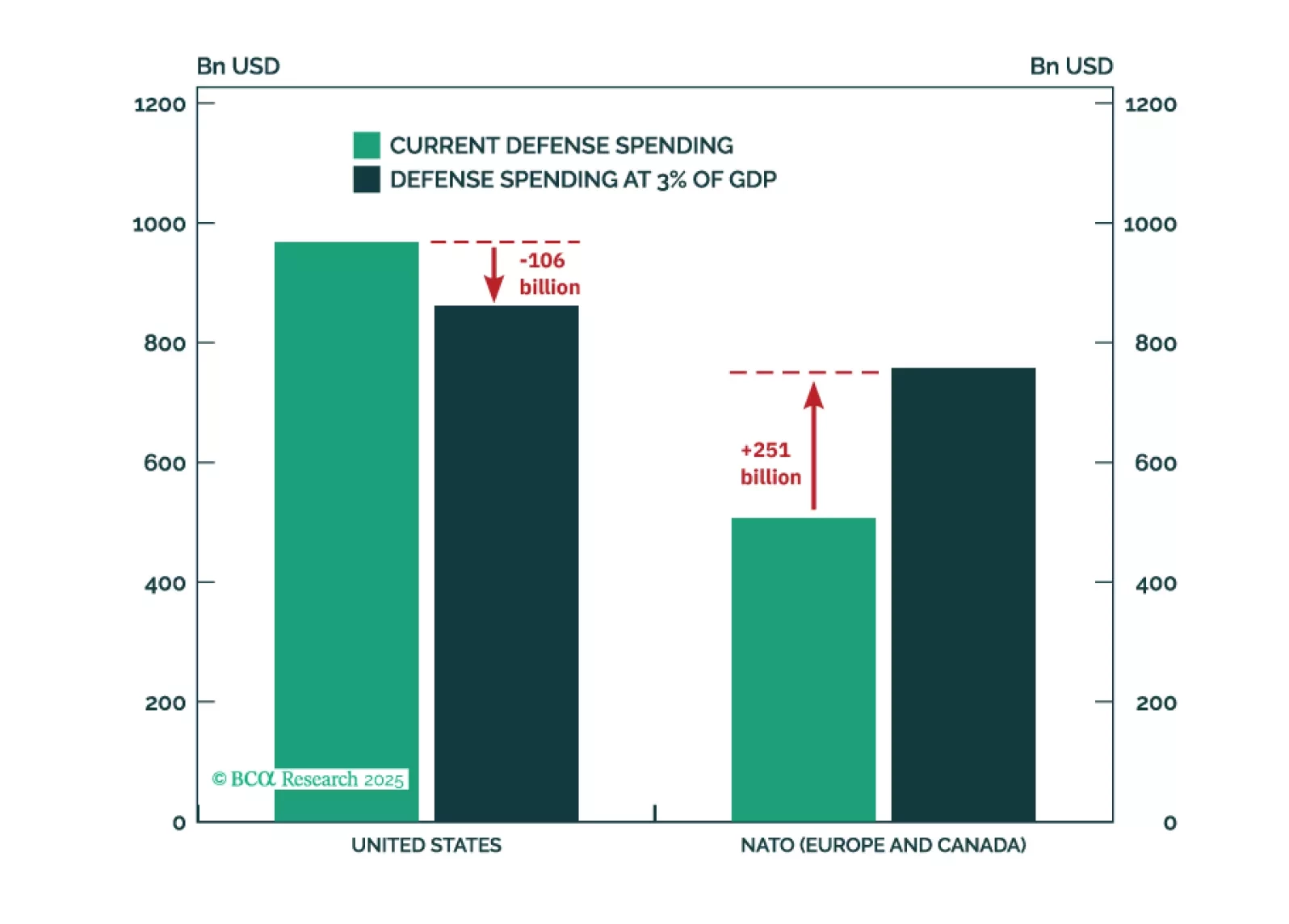

The Trump administration posits that the world owes the US for the provision of its security. In this report, we perform a quantitative analysis to come up with a naïve estimate of the cost of that peace. More importantly (and more seriously), our qualitative assessment argues that save for a number of frontline countries that rely on the US defense umbrella, the vast majority of the world faces manageable security threats due to the complex multipolar global environment and a growing number of alternatives to the US security blanket.

The rise of the far-right is challenging mainstream German politics. The CDU/CSU and SPD will govern Germany again after the election. A ceasefire in Ukraine will offer some relief, but Trump’s policies will keep tensions high.

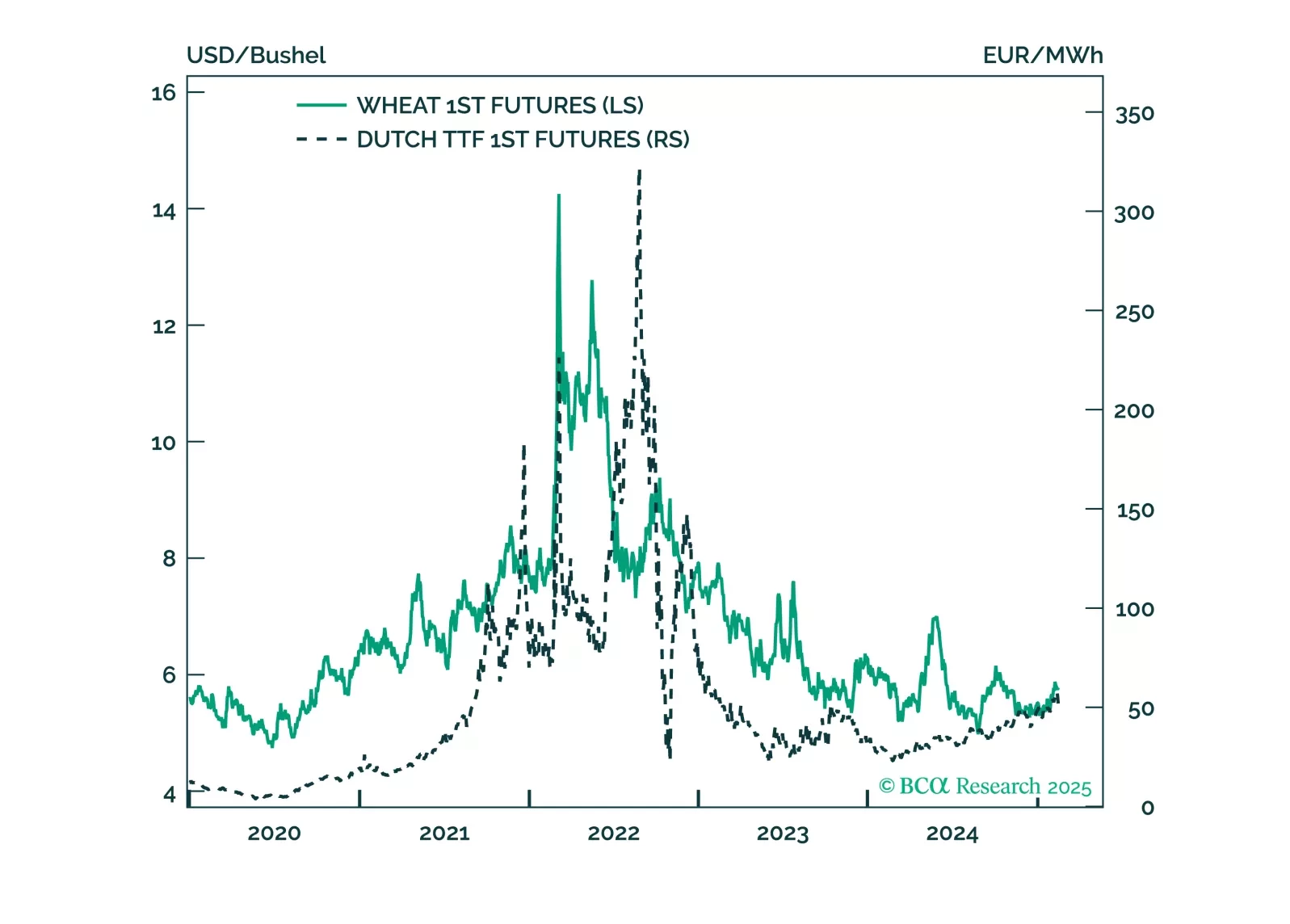

President Trump is negotiating a ceasefire in Ukraine. This will be a marginal headwind to some commodities which benefitted from the conflict like natural gas and wheat, and will be a marginal tailwind for European assets, specifically EM Europe. Use Trump’s tariff shock as an opportunity to buy European assets.